Refer recent Berger paint research report, about the paint industry and competition from biggies:

Sirca Paint India has a leadership position in Wood coatings and other industrial coatings. Whereas Berger and other peers are biggies in their decorative paints segment. Even ICA pidilite (unlisted company of pidilite) which is a nearest competitor of Sirca India is struggling to position their wood coating products against Sirca quality. So Sirca’s main revenues are drawn from their coating products and wall paints segment is something they have started a year ago.

1 Like

Actually MRF vapocure is pretty good here in south india. We have used MRF products only for wood coating and grill coatings for our house.Also Asian paint is very good for wood coatings here in south india.

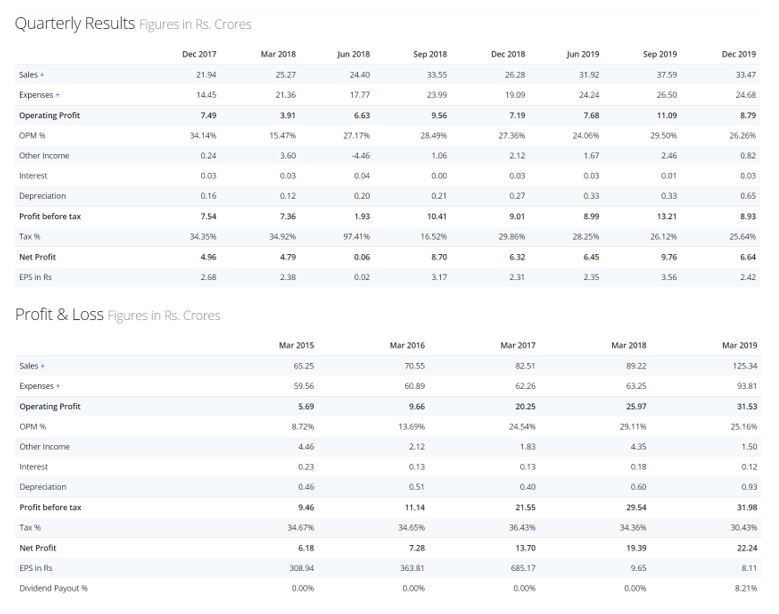

I was interested in paint companies due to severe fall in crude prices. Crude being one of major RMs this could be very positive companies. I was interested in this company due to NIL debt and high sales growth. The factories being located in Italy, one of the worst affected countries due to covid 19 is not a worry as I expect the production to come back to normal very soon. Being a badly affected country they will be more keen to step up production. Supply side looks fine with me other than some freight related issues. The matter of concern for me is the very high debtor days ie, 115 days more than a quarter. Whereas the debtor days for peers like Asian paints , Berger etc are 35 to 53. The receivables o/s are 42.99 crores whereas sales for Q3 was only 33.47 crores. Being a new entrant the company may have to provide a higher debtor days , so that dealers stock up more of their products. Or is the the company overstating it’s sales by just pushing the stock to dealers. If that’s the case there may already be stock for more than a quarter available with the retailer dealers. In such a case , sales may get severely impacted in the next few quarters and debtor days may further increase.

Anyone tracking the stock can help me on the high debtor days

Was tracking the stock. No positions taken due to the very high debtor days. Hoping to get a clarity on it

4 Likes

More or less a similar question by one of the investors during their last management-investor con call, for which the management has said they are fully committed to reducing the number of days going forward. I think that was evident in the management commentary, as it was 137 days as of Mar 2018 and that came down to 115 days as of Mar 2019. So you may continue to track.

This company is having a market cap of around 500 crores and was into lossess few quarters back as per financials on moneycontrol.While the sales have not gone up fast, the profitability in last few quarters has gone up . I find similar positive comments on moneycontrol message boards too pushing positivity about this small cap company. It would be prudent to do more research before taking a stake. Just a caution.

1 Like

Just wondering moneycontrol site has never been so accurate in terms of updates to the content. For accuracy, mostly I refer the financial data either from NSE site, company web site or screener. Just below copied the data from the screener snapshot of last few quarters / FYs data. Not sure if this data helps you in anyway.

Investors are advised to dig more about this company prior to any investment call.

These figures are not the same as on moneycontrol. However few things to be noticed that there is miniscule sales, huge variation in expenses, debtors higher than quarterly sales but v high margins. All these are pointers for further study.

It does not appear to be Monopoly business as they are other players too and therefore the kind of margins being reflected in results need further validation.May be someone more experienced in this field can help.

1 Like

Hi everyone,

I have tried and covered all the relevant points in the blog, it will be great to have your views ![]()

6 Likes

Need to dig deeper into few points

a. Increasing Trade receivables-39 odd Cr as of FY19

b. Increasing Inventory- 26 odd Cr as of FY19

c. Company has given advance to suppliers- May be to get better terms or any other reason

Will wait for this years figures to get more clarity.

Disc: Not invested, tracking since IPO

I was going through that. They have clearly mentioned it in thier rhp as well, infact they were ready to give credit for 4 months in the near future according to rhp.

Thier cash flows have drastically turned negative in 2018 and 2019

The managementis saying now they will try and control the credit period given to the debtors as they can’t delay payment to the creditors which is mostly sirca italy they also have to maintain large inventory imported from sirca italy they told they are holding inventory of 5 to 6 months which is very large.

This is also good in current scenario as import from italy was not happening.

I think they will continue to have large working captial requriement as they are still expanding aggressively and they cannot push thier product with tight credit period to the dealers

These are the challenges of a new entrant. Even with comparable quality product, they have to extend credit to gain shelf space and compete with established players. And if they dont extend credit, they wont be able to utilize the newly built capacity. And so high receivables is almost sure in the future. And till they fix the working capital issue, re-rating wont happen.

Plus with social distancing, not many retailers will like to have painters and interior decorators in their house.

Plus low capacity utilization in 1st year may mean low operating margins.

Not invested. Just academic interest.

2 Likes

Sirca India were paint traders before 2018-19 and not manufacturers. So, comparing the inventories or working capital from previous years to now may not help.

The side I am really intrigued is their expansion in sales & marketing - having setup 14 studios and dealership gone up from 3 times from 500.

It shows, company is ambitious. And they have the vision to expand Sales & marketing, when plant was still about to open. Their corporate governance - till now - no reason to doubt it. They have migrated from SME to main board in a short time. Used the funds of IPO for the purpose they took it for and now completed the plant.

So, I dont see any reasons till now to doubt them. But these are tough times. Lets see how they do.

I think in short term the lockdown will do good. They can burn off their existing 5-6 inventory when lockdown eases.

Disc: Tracking only. If there is a dip in price, I may also dip in to buy.

1 Like

Paint dealers side inventory info:

very good, how the biggies are helping their dealers:

Some issues to ponder upon:

- EBITDA margin of Asian/Berger is 16-18% despite having scale efficiency/experience. Can Sirca maintain 25% as mgmnt is saying? Esp. as they do domestic manufacturing of cheaper priced paint vs. Italian imports + as volume rises. Even Pidilite EBITDA margin is only 20%. Even Sirca’s direct competitor and Pidilite subsidiary, ICA Pidilite is only getting 10% EBITDA margin on 168 cr sales (2019FY, per Pidilite AR). FYI - ICA is also domestically manufacutring the product.

- This risk is high as company does not have manufacturing experience - so no precedence of being able to achieve 25% margin.

- Niche product category raises risk IMHO. Asian paints and Berger have diversification benefit. Sirca is too concentrated in narrow wood segment. Tough to get 20% + P/E rating even in bull times. Think about Bajaj Consumer Care and Zydus to see what concentration/niche category does. In both cases organic diversification did not work. Zydus was smart to diversify through inorganic acquisition. Bajaj consumer is langusihin at 10 p/e ratio. Yes wood paint is a growing category but single category risk is high here - it is more like a hit/miss type

- Salaries expenses incl. of promoters are rising faster than sales

No investment. Academic interest only

5 Likes

There won’t be an end to an assumed issues. To that extent it holds true for any big / small company and as someone rightly said “all stock market investments are subject to market risk”. As regards to margins, the management has delivered so far what they said. Sirca India is not a new entrant to this business and based on the management commentary, I believe they know what they are saying as they are in this business for past 15 years and they know what they are doing for future. Btw; do we have a choice except to trust the management and hope for the best. I am sure all our current investments into other companies is based on those principles.

As regards to second point. Sirca India manufacturing and quality is under the supervision of Sirca Italy management and Technicians. So no chance of compromise on the quality of products or efficiency. Even if they want to be Indian mindset, they can’t as Sirca Italian brand is at risk.

As regards to other points, Sirca India is not just targeting Pan India market, but also Srilanka, Nepal, Bangladesh, Dubai markets. So for the size of Sirca India, this size of market is enough for them to grow them gradually.

As regards to last point, not sure if you are tracking the investor presentation and management concalls. The salary expenses are bound to go up as they are building the sales force at pan India level penetration, which was not the case previously.

Wondering those Bajaj, Zydus businesses are an appropriate like to like comparison with Sirca ?

1 Like

Management have said they are maintaining the same quality as Sirca Italy - they have had people from Italy guiding them every step of the way. When it comes to Sirca India - they have had skin in the game for last 12 years and built relationships with OEMs like Godrej CP, Jindal Stainless etc. This has been their only focus while likes of ICA Pidilite came in 2018. I am not saying they will compete with Pidilite & Asian and all big companies. But they have a niche product and focussed only in Delhi and North India. And now, they are growing in other areas with studios & dealership.

Global wood coating industry is growing at 8%. Even the likes of Pidilite & Asian paints are only starting those departments now. The runaway is huge in India. There is a space for all these players to grow.

3 Likes

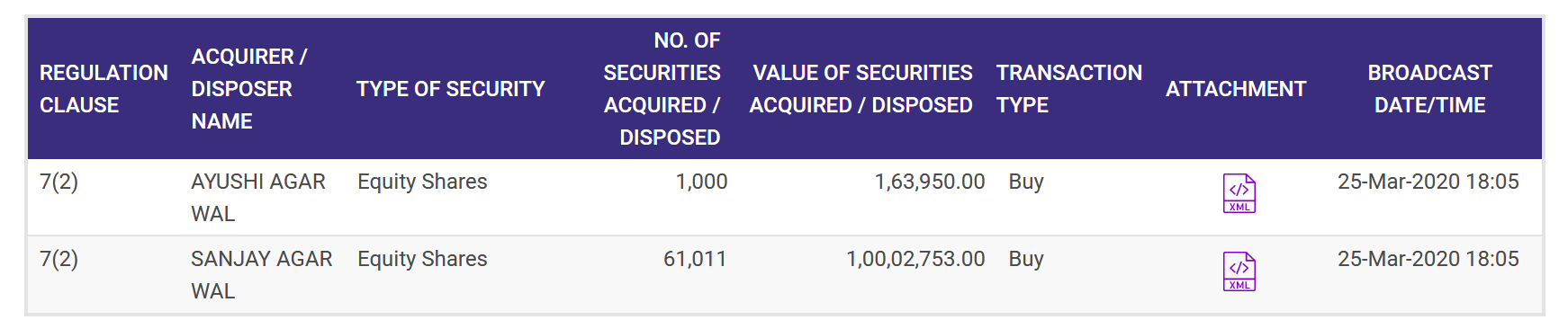

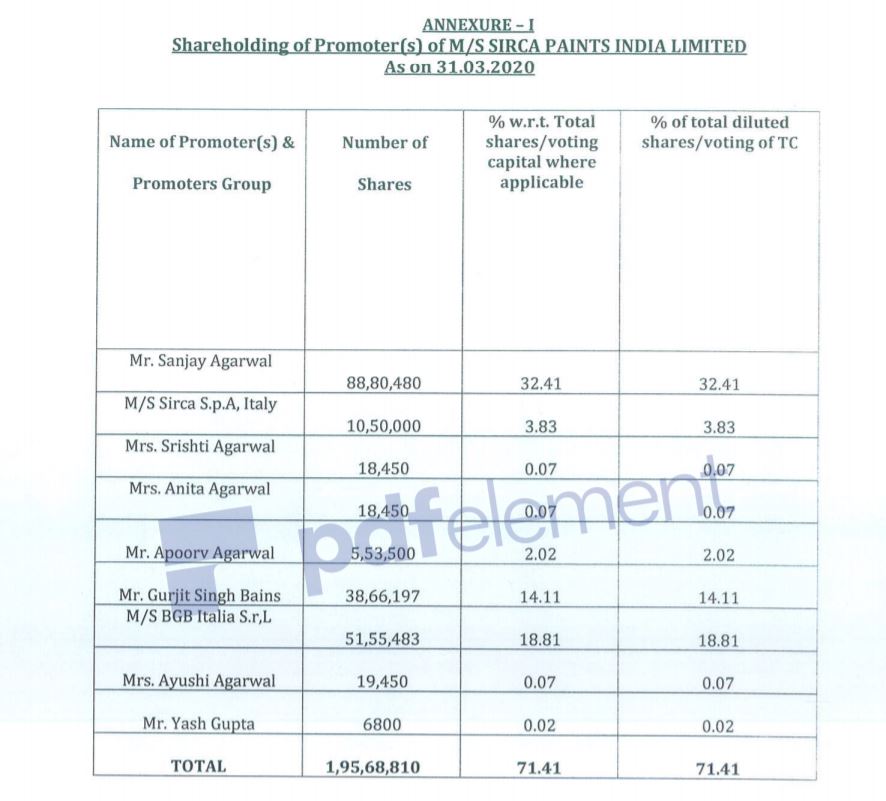

Based on today’s company disclosure, it is interesting to watch 2 more names (Sirca SPA Italy & Yash Gupta) classified as promoter and promoter group in the shareholding. As a result now the promoter & promoter group shareholding stands at 71.41% as compared to 67.55%?

Source of info: NSE

3 Likes

Finally some good news that, Sirca Paints has partially resumed their operations at some of its locations offices, depots and warehouses wherein lock down restrictions have been relaxed.

Source of Info: Today’s NSE filing.

1 Like