Agree. Even with very conservative growth assumptions, EPS should be 3.99 fully diluted and once market sees pre-fab stabilizing, PE should expand. It is already at 15x trailing EPS (excluding all the one-time expenses), so normalized will be closer to 20, my guess is. Yes, unless cash flow are are fudged, 95-100 should be easy to achieve in about a year.

Disc: Bought at 75, averaged at 60s. Net cost 69ish.

Can anyone share any light on the nature of the contracts in the CM business with respect to input (crude) prices. Are they on a cost plus basis? Similar question regarding the retail business, how often can you pass through price changes to the end customer?

Same question was raised few quarters back in a ConfCall. CM B2B segment is cost plus with a lag. So margins do not suffer which looks true going by the financials. No idea about retail, must be same like nilkamal or wimplast. Not sure what they do.

While one can’t deny the possibility of the promoter infusing funds by borrowing money from market by further pledging his stake, but we also need to note that the share is trading at an all-time low, so it can also be enhancement of pledge to match the overall collateral. Also, I don’t know whether infusion of funds as equity in the company by promoters, pledging their wealth is a big negative, though its a risk for sure.

The promoter has already paid the 25% of the warrants in March-2018. Why the pledge now? They would have infused 150 crores approx via warrants which was supposed to be used for reducing the debts.

There is a loss of revenues of 100 crores in custom moulding business and loss of PBT (12.70 crore) in this quarter.Cost of interest has also increased by 12 crores for this quarter.15 crore has also increased in employee benefit expenses.

This overall has contributed to worst results in my opinion.

I am unable to see any hope in this business.

Let us see management commentary on investor meet.

All views are invited. We must discuss the prospects of company and arrive on some conclusion.

I attended some parts of the concall today. They have received some RS. 1190 cr from KKR in the their in the customs mouldings entity in an all debt arrangement (clarified several times during the call). The ROI on this will be ~8.75%, whereas their overall borrowing cost is ~10%. He further clarified that the increase in pledge was due to promoter raising funds to subscribe to warrants.

One positive thing from their presentation was, focus on the debt reduction. Current D/E ratio stands at 0.89. Will have to observe few more quarters to see if they are true to their words.

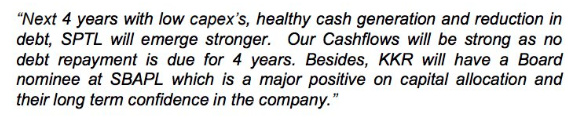

In an investor presentation , they have mentioned that they do not have to pay debt for next 4 years which according to my understanding that they are going to pay interest for 4 years without reducing debt.Is this a right approach?

Can someone throw more prospects of deal with KKR, and how it is favourable in terms of company and investor.

They wanted to reduce debt by Rs 5000 mn by FY19

An extract from presentation .

Further FY19, we plan to cut down our

debt by another Rs 5000 mn by excercising remaining warrants by

December, and through internal cash generation. The warrants entail

promoter stake wlll increase to 37% from 28% at Rs 90 per share.”