invested 1700 Crore, that CAPEX is going live this FY, and we are investing another 1500 Crore this FY which will go live next FY. With these CAPEXs coming in, the revenue should go up relatively faster than the other two businesses.

Revenue FY 15-16 940 Crores.

It is very difficult to pinpoint textile numbers because it depends a lot on the yarn prices, which fluctuates year or year, but broadly speaking these two CAPEXs which I just mentioned one which has gone live this year and one which will go live next year, these two put together should add something like 2500 to 3000 Crores to what is our already existing topline. So if we talk about FY 18-19 it would be 3000 plus 900 which is the current number.

From Annual report 2016:

The textile division reported a healthy performance as revenue grew by 26.55% from 725.40 crore in 2014-15 to918.02 crore in 2015-16. This superior performance was the result of a robust growth in sales volumes in the domestic market – by brands and through our retail channel. The Company’s focus on superior design creation and product development increased product acceptance in ‘Collection Sales’ in international markets which is expected to result in heartening volumes in the current year. In addition, the Company’s significant efforts in streamlining plant and business operations facilitated in strengthening the profitability of this division.

As per management revenue for FY 18-19 is projected at 3900 cr.

Considering the above points, would it be fair to imagine that this stock could be valued at 6x (2x P/E expansion and 3x increase in EPS) in about 3 years?

Phase 2 capacities will come online by October 15, 2017.

Once the plant is operating at avg. 90% capacity (expected to be by July 2018), they should have the possibility to make (in any subsequent 4 quarters after this timeline) a topline of 3600 - 3800 cr. with an EBIDTA of about 500 crores.

The management has announced their intent to reduce debt over the next 5 years and bring D/E under 1. Therefore, further expansion in the foreseeable future is ruled out. A zero growth stock is unlikely to get a P/E of over 6 - 8.

This is primarily an undervaluation play, and you may expect to see a price of 60 - 70 Rs. about 5 quarters from now.

I.M.H.O. Meaningful price increase beyond this should happen only when the next phase of expansion is announced.

During the prior cycle (2003-2008) Sintex Management were indisciplined in capital allocation and did not show any appreciable management quality talent.

They now have senior personnel from Welspun and Trident, and have said the right words during recent concalls.

The managements credibility can be gradually re-established if they really walk the talk - over the coming years.

I am not looking at this from a 3 to 5 year point of view. This is an undervaluation bet.

There are a number of high ROE / better quality companies to Switch out to once the valuation gap is bridged.

The company operates in a non growth industry. Companies operating in non growth have few advantages as well. Everyone knows what high growth industries are, and low cost competition is running into the same to compete. But in non growth industries, no one dares to enter looking at the margins, saturation points etc.

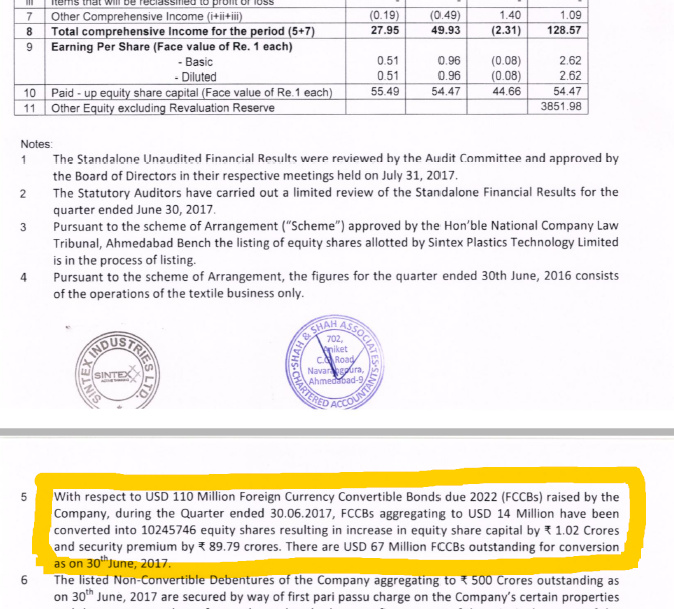

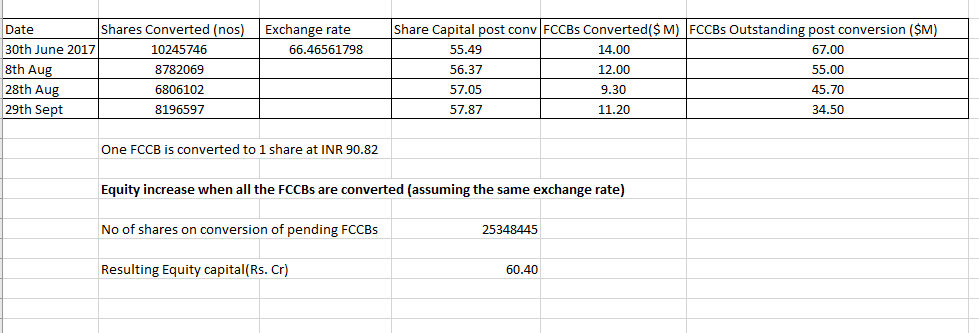

Sintex has been converting the FCCB’s which are due in 2022, at a steady pace. On one hand it is reducing the debt, on the other hand, there is dilution of capital and increase in free float which is pulling the valuations down.

I have tabulated the recent conversion and the consequence to equity capital on conversion of all FCCBs.

As per the FY17 Annual Report, the conversion price (currently Rs. 93.8125 per share) on FCCBs may be reset on 25 Nov 2018 and 25 Nov 2019. The interest rates will be 7% till 25 May 2018 and 3.5% from 25 May 2018 to 25 May 2022. Though I am not sure what will be conversion price if the resets happen, but in my opinion as the interest rates are lower from May 2018…the conversion price may be set lower (higher dilution). Therefore, it may well be better for them to convert the $67mn FCCBs before Nov 2018, which will result in issuance of ~48.2 mn shares (8% dilution on the extended base). Based on the conversion done between July-Sept 2017 (23.8mn as per BSE filings), according to my calculations $33mn were converted in Q2 FY18, which will leave them with balance $34mn FCCBs at the end of the quarter. So almost 50% dilution has already happened and reflecting in the CMP. I wouldn’t be surprised if the convert the FCCBs entirely by Q3. Also I think the savings in the finance cost due to conversion of FCCBs can be around ~20cr for FY18.

This stock may drift towards 23 or lower!

Nice thread!

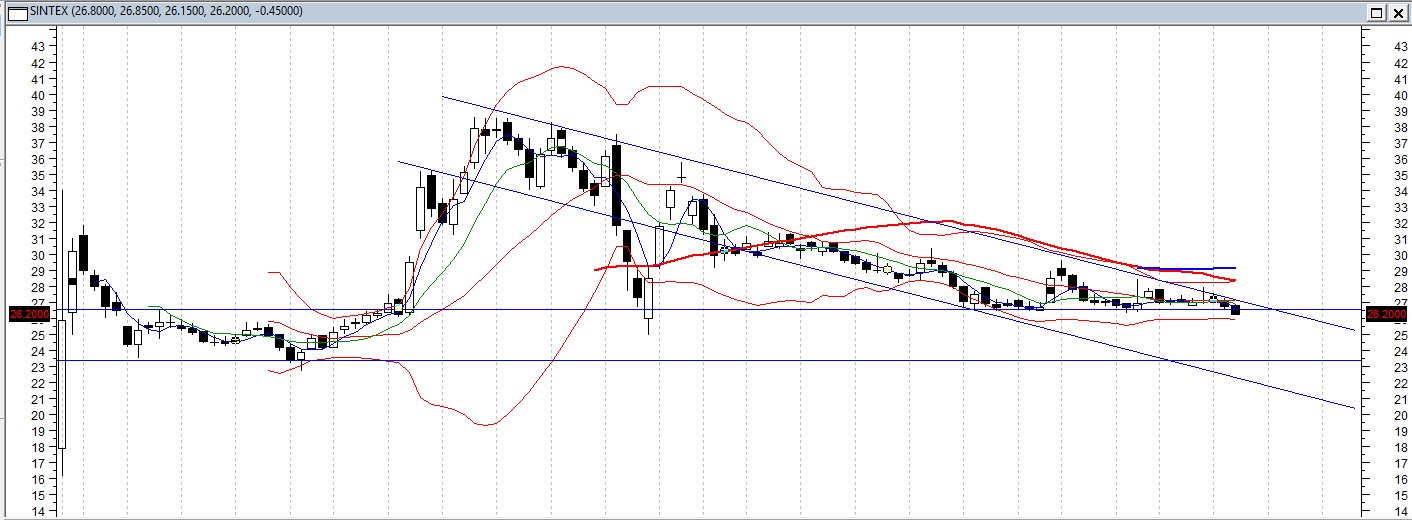

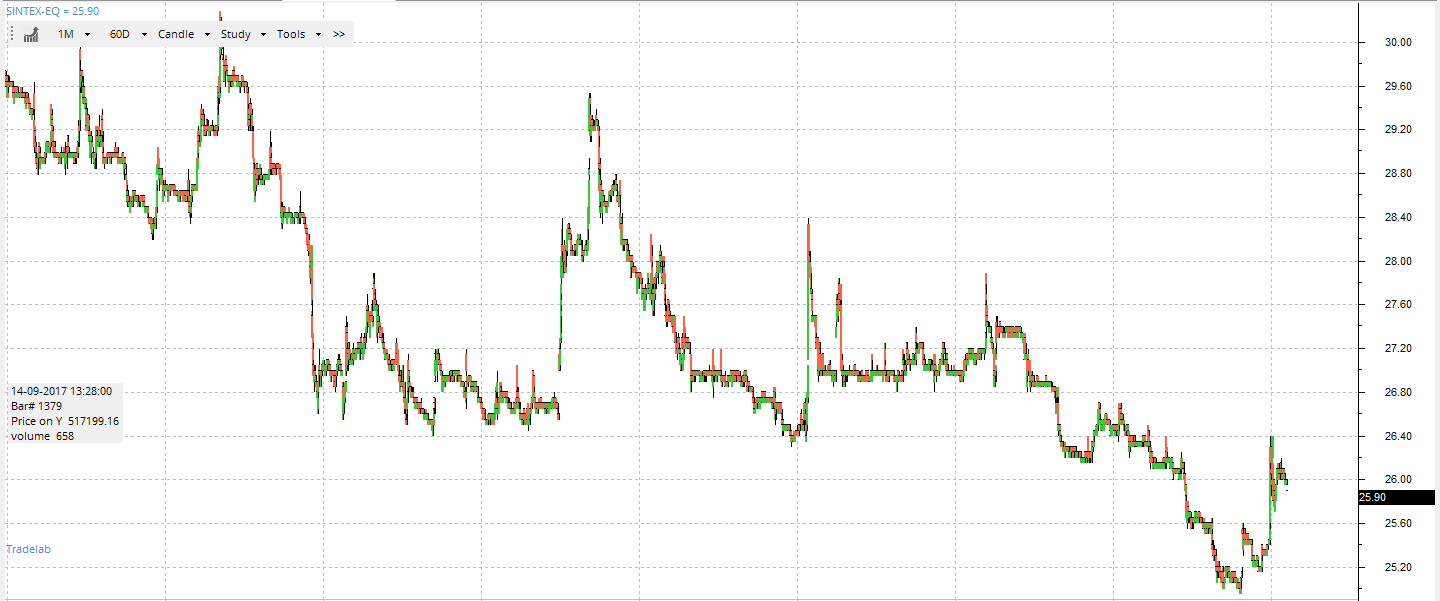

I have become interested in this company, as it may prove to be a value play. However the prices are likely to drift lower, as per the charts. For three months the prices have been moving southwards in a channel. Today’s closing price is lowest of these three months. 50DMA is below 100DMA. The prices are likely to drift lower after remaining close to the resistance line for several weeks. This was in anticipation of the Q2 results, which are not encouraging. Historical lowest closing for the stock is 23.4. In my opinion, the stock is likely to retest these levels.

The views of the borders are invited regarding the appropriate entry point in this stock. This is a cyclical play now, and we need to be careful about the entry point in this stock. New capacity will become operational during this quarter. This may positively or negatively impact the bottom line of this quarter. Further cotton prices (Indian and international) and raw yarn prices will be important Can somebody dig out these trends?

Agree with you Mr. Agarwala, stock will remain under pressure, technically weak, but you never know some good news or announcement and it will spurt up.

FCCB’s is also one issue which will have negative effect on the stock sentiment and its price.

I believe one can start accumulating the stock slowly in price range of 26 to 20 and time frame of accumulation can be next three months.

I am expecting the stock to appreciate by a good amount in a year or 18 months time.

Resistance at 26.40

The chart of Syntex Industries shows important resistance at 26.4. There were several bottoms at this level during previous weeks. Once that support level was broken, it became a resistance level. Unless this level is crossed with good volume, Syntex Industries will remain bearish.

Phase 2 of 3 lakh spindle is on ,they are now gradually increasing capacity utilization ,what is the reason for downward movement? Views invited ( Disclosure: Holding in my personal portfolio )