Today, the stock idea being shared is of a hotel company. Usually, investors refrain from investing in hotel companies because of cyclicality, concerns about funds being siphoned off from the company, promoter integrity. But, this company is different.

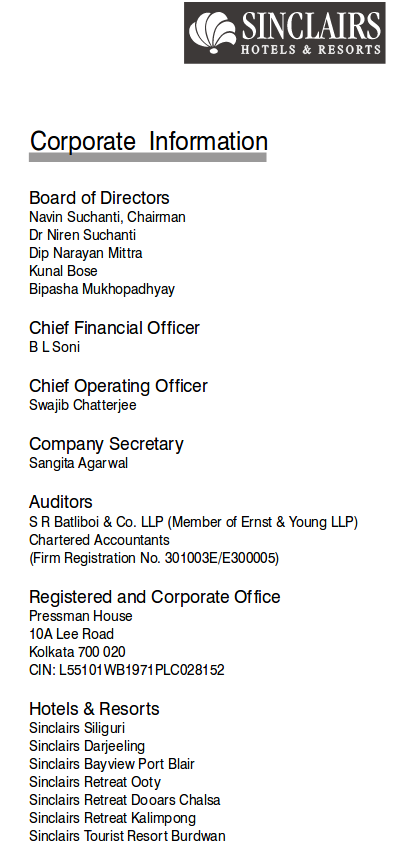

Sinclairs Hotels is a leading hotel chain with most hotels in East India. It has 7 hotels.

The locations are:

1)Burdwan

2)Siliguri

3)Darjeeling

4)Dooars

5)Ooty

6)Port Blair

7) Kalimpong

This company is promoted by the Suchanti family ( Pressman Advertising). Promoters hold 56.96 percent of the shares. Xander, one of the leading PE firms had invested in Sinclairs but they’ve now exited.

FINANCIALS

The company reported sales of 47 crores for the year ending March,2017. They’ve grown their sales at 26 % for the past 5 years. It’s a consistent dividend paying company. It has been debt free for more than 10 years now. Their net profit margin is upwards of 20 percent. The stock is trading at 19 times its earnings.

Now, more about their hotels:

Their hotels have received very decent reviews on various platforms. Their hotels in Siliguri and Burdwan feature at the top of the hotel lists on various hotel aggregator websites. As tourism increases, there’s no reason to believe that Sinclairs won’t be a beneficiary. Today, they have around 450 rooms and they intend to expand to 600 rooms in the next 3 years. They’ve undertaken a greenfield expansion in Rajarhat, Kolkata on a 1 acre plot. They have 396 employees. Remuneration of a key management personnel, who is part of the promoter group is linked to performance of the company. They’re incentivising performance. Prima facie, it does appear promising. Let’s all try to get a better understanding.

I would be interested in more thorough research than just focusing on the basics. Could you please detail out more on following issues:

-

What makes the company command the high OPM…competitive advantage/competencies etc.? Have the margins peaked out or their is room for improvement and how?

-

There seems to be a substantial difference in ROCE (22%) and ROE (10.7%) despite the company being debt free. The business prospects may be good but investment prospects look average. What am I missing?

-

What’s behind their current investments? They have jumped four times suddenly in last one year (from 6.7 to 27.4).

-

How do they plan to finance growth?

-

Risk factors?

Best,

Nolan

The overall performance of the company has been quite stable. I have received good feedback about the hotels and the online ratings are good. The balance sheet is debt-free and has been generating good cash flows so it is capable of expansion, but as pointed by @Nolan, there is no clarity on how they plan to grow in future. Though better utilization is expected out of Darjelling and Kalimpong assets and expansion of Chalsa and Siliguri. properties will come up soon. I will be waiting for the management to unveil the future course of action.

Regards

SJ

Dear @Nolan, They’ve invested a significant amount in debt funds of HDFC and SBI. Hard to tell what must have triggered this increased allocation to current investments.

For future growth, I believe we might see increased occupancy. Currently, it hovers between 40-60 percent depending on the location. There’s room for improvement in occupancy. The company is stepping up efforts on social media platforms. increased occupancy will enhance food and beverage revenues. Increase in occupancy will increase revenue proportionately but profits will increase disproportionately because no addition in infrastructure, manpower will be required to cater to the increased footfall. It’s very difficult to predict the future. But,the locations of their hotels are phenomenal, in my opinion. Big hotel chains haven’t entired these markets. Sinclairs is the only chain in most of their locations. Business travellers, middle and upper middle class travellers would be inclined to stay at a decent chain like Sinclairs than at some other place. Their tariff might be a little higher than competitors but family travellers and business travellers might be willing to pay the premium. Only time will tell if this hypothesis is proven right or wrong.

Risk factors: 1)Some regions of their operation are sensitive. Instability due to protests was experienced but the company did well, per an online review. Such frequent cases could deter tourists, in turn adversely influencing Sinclairs.

2) Changes in regulations

3) Economic slowdown affecting tourism

4) Launch of new hotels in these destinations

5) Natural disasters which might debilitate the group

For further growth, they’ve planned a hotel in Kolkata. It’ll be a 110 room upscale hotel in Rajarhat. On commencing operations, that could add not less than 30 percent to the current revenue.

i have some questions regarding it:

- In 2011, they bought Savannah Hotel Banglore and exited in 2013, why…?

- Why all PE fund exited in recent time…?

- As per my calculation total rooms comes to @354…

- What are occupancy level on yearly basis for last 3-4 yrs and what is the avg room rates per day…

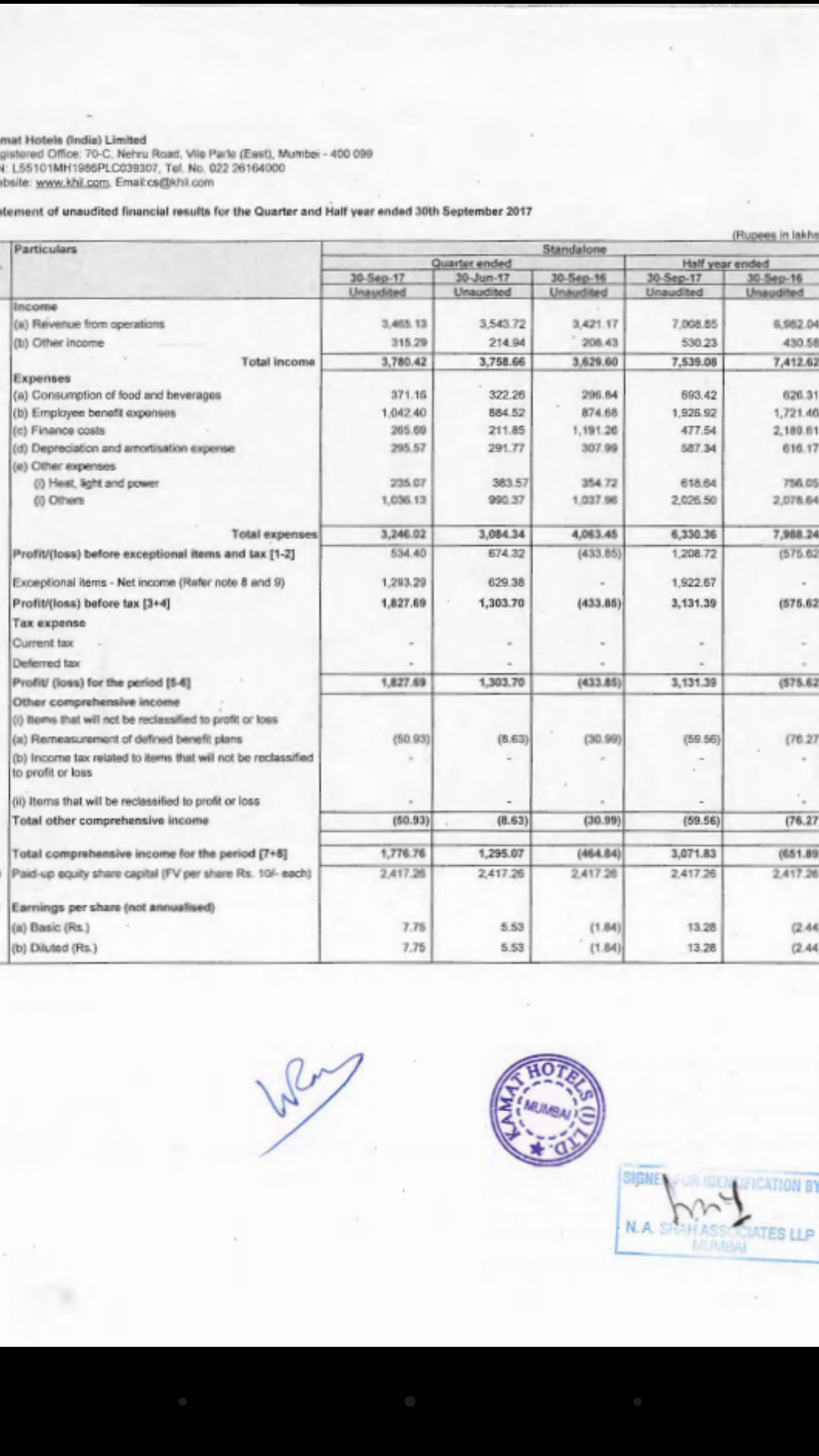

Comparatively In this sector Kamath hotels is now become turn around story, reduced debt and turn profit. excellent results…quarterly 7 & Half year EPS 13…Annualized PE comeout just 5…excellent return in one year… Wish continue to grow further as its lifetime ever achieved results… Quite undervalued- Kamat Hotels

Close to 70% of the EPS is from Exceptional Items. What items are those?

@sanu1802, Many thanks for participating in the discussion. Yes, I made a mistake. The total room inventory is 360. In the year ending March,2017 they earned 29.3 crores from room tariffs. As per management commentary, average occupancy has been between 45-50 percent depending on the property and location. Assuming 50 percent occupancy, the average room rate comes to around 4520 which is in line with the tariff provided by online booking portals.

@sanu1802 Regarding the exit of PE groups, I don’t think it’s too concerning a development. They had entered 10 years back, in 2007. The founder of one major PE group had once said in an interview that their assets are always on sale provided the price is right. They probably got a decent return or an opportunity where they can deploy their funds and earn more. In my opinion, it’s not a red flag but just better utilisation of funds by PE funds.

@sanu1802 Answering your question about room utilisation, in a 4 year old interview management had said that that occupancy averages around 50 percent. Taking that into consideration, their revenue from rooms has increased by 22 percent. It means they’ve been successful in raising prices. It’s indicative of decent pricing power. Please share your thoughts.

@ranjan10, What exceptional items are you referring to? I can’t find any mention of that.

What is the source of expansion news?

I do not see any hotel at Rajarhat in the list of hotels provided by them in Annual Report 2017.

You should provide detailed analysis of management personnel renumeration.

@ranjan10 Kamat Hotel should not be discussed in this thread. Thanks

@Gaurav_Agarwal Many thanks for participating in the discussion. They currently have 363 keys- including rooms and suites. They’re planning to expand in Kolkata by setting up a 110 room hotel in Rajarhat. The construction hasn’t been completed. It’s under progress. It will increase their key count to around 470. I had mentioned in a previous post that I had inadvertently written 450 rooms instead of 360 rooms. I was misinformed beacuse of some old materials I had read.Construction of the Kolkata hotel entails an investment of around 80 crores, as shared by the management in an old interview. I’m not aware about the current status of the Rajarhat hotel. The Rajarhat hotel is also mentioned in the upcoming hotels section of the website.

Regarding remuneration, Mr. Navin Suchanti, who’s the Managing Director takes 2 percent of the profit as remuneration. As a result his remuneration last year was 27.88 lakhs (2% of 13.95 crores which was profit before tax). The CFO was paid 15.32 lakhs and the company secretary was paid 3.52 lakhs.I’ve shared the remuneration of all key managerial personnel.

I’ve tried to answer your questions. If you’ve any other questions please do share it I’ll try to answer it.

I did not even realize that the results posted in this thread was of Kamat. I was under the impression that it is of Sinclairs. We should not have allowed that to happen in the first place.

Thanks @shreys for answering my questions. I hope you will appreciate that, we all need to vet the story thoroughly to separate wheat from chaff.

Can you please share that old interview?

I could not find any mention of it in 16-17 annual report. Even in q2fy18 press release they have not mentioned anything about this hotel. You should check out if this is happening at all.

I completely agree that we must evaluate a company on all parameters before investing our hard earned money. I’ve shared a link of article of 2013 sharing their plans to expand in Kolkata.

They’ve executed their Kalimpong project as they said. However, the lack of updates about their Kolkata project is concerning. We must try to find out more.

The company for the first time in their Q2 results probably provided more information about their business and also outlined their expansion plans:

Quoting them verbatim

"

- the Company’s hotels in Darjeeling and Kalimpong were closed from 15thJune, 2017 to 30th September, 2017 due to political unrest in the region. Normalcy has returned to the region and the Company’s hotels in

these two locations have started full operations and seeing steadily increasing traffic now.

It is expected that occupancy levels at these properties will soon reach the targeted levels. - The Company’s strategy of driving both tourist and corporate segments has paid good

dividends and resulted in a steady increase in both occupancy as well as average per night

realization per room and given a substantial boost to the food and beverage sales of the

Company. The Company’s properties offer great value for money and are rated highly on

the various industry and tourism websites. -

the Company

is building an additional 50,000 sqft of banqueting space in Dooars and Siliguri. The Siliguri

facility of about 30,000 sqft will be ready by January, 2018, while the Dooars facility is

expected to be operational by March, 2018. - Sinclairs Hotels has strong fundamentals with Reserves and Surplus of Rs.7809.20lakhs (as

per Audited Balance Sheet of 31st March, 2017) on an equity capital of Rs.557 lakhs. The

Company is debt free and has substantial cash reserves, which can be leveraged for future

growth.

"

The company has reigned in expenses during Q2 which has greatly helped shore up the bottomline.

Details about their upcoming 114 room hotel in Rajarhat:

http://www.sinclairshotels.com/upcoming-hotels

@shreys @hemtan100

We should write to the company to know their plans for this hotel.

-

Also How will they fund this project?

-

Have they bought the land? If yes, who owns it and who paid for it? What would be cost of land in this part of Kolkata?

@Gaurav_Agarwal Sure. It seems they’ve already acquired the land. In an interview, Mr. Suchanti had mentioned that land acquisition has been completed. They were awaiting approval from the concerned authorities to commence work.

However, that was 4 years back.

ROCE is greater than ROE as the company is debt free and not all the equity is employed as capital. They have cash in the form of Current investments.