Thanks for your observation and inputs. I read your post multiple times to grasp as much as I can from your words ![]()

1 Like

I did a long pending exercise…seems had been very casual and avoiding the hard work but words of @hitesh2710 made me dig deeper into this. I always wanted to check stock level CAGR for my portfolio, especially over different major time frames that I purchased them. This was primarily because I purchased same set of stocks at various levels over last few years and averaged up most of the time.

I must say I was positively surprised by the result. Pls note that the CAGR is in no way an indication that these stocks are good and would give similar CAGR in future. Also, these numbers are no indication of my portfolio CAGR as that is dependent on numerous factors like losses booked in stocks that were weeded out, allocation levels in existing and sold stocks, CAGR of sold stocks, current losses in some 1% holdings which I have excluded etc. (I have reasons to believe that overall, at Portfolio level, my CAGR would be around 15% only)

This is just an exercise for purpose of self-learning, deepening understanding of simple investing technique that I try to follow, understanding how individual stocks in my portfolio have performed, how staggered investing in same stock has performed, which stocks have not performed for me and reflect upon the why!

This is in no way a recommendation or endorsement of any stocks as any high CAGR can plunge anytime in short span and a low CAGR can increase anytime as well. Any CAGR over any timeframe can be misleading and not indicative of true returns that stock can give us as true returns depends on numerous factors and not just one. I am not eligible for any advice.

| Company | Percentage | CMP | Buy Price(s) | Holding period in Years (Approx, Average) | CAGR (Approx) | CAGR (Approx) | CAGR (Approx) |

|---|---|---|---|---|---|---|---|

| Tata Consumer | 15 | 950 | 150, 250, 600 | 10, 3, 1 | 20.27 | 56.05 | 16.55 |

| ITC | 11 | 455 | 170, 200 | 3,2 | 38.84 | 50.83 | NA |

| Trent | 9 | 2870 | 500, 750, 1000 | 3,3,2 | 79.05 | 56.41 | 69.41 |

| Pidilite | 8 | 2570 | 500,600, 2000 | 8,8,1 | 22.71 | 19.94 | 28.5 |

| Marico | 7 | 535 | 100, 270 | 10, 3 | 18.26 | 25.6 | NA |

| Midcap IT | 6.5 | NA | NA | 3, 1 | NA | NA | NA |

| Godrej Consumer | 6 | 1045 | 350, 550 | 8, 3 | 14.65 | 23.86 | NA |

| HDFC Life | 6 | 675 | 350, 450 | 6,3 | 11.57 | 14.47 | NA |

| United Spirits | 4 | 1070 | 550, 600 | 3 | 24.84 | 21.27 | NA |

| Nestle | 3 | 24600 | 15000 | 3 | 17.93 | NA | NA |

| Dabur | 2.5 | 550 | 250, 400 | 8, 3 | 10.36 | 11.2 | NA |

| Avenue Supermarts | 2.5 | 2050 | 4050 | 3 | 25.48 | NA | NA |

| Asian paints | 2.5 | 3220 | 1100, 1500, 2000 | 5, 3, 2 | 23.96 | 29 | 26.89 |

| Britannia | 2.5 | 4960 | 1000 | 8 | 22.16 | NA | NA |

| HDFC AMC | 2.5 | 3030 | 2000, 1700 | 3, 0.6 | 14.85 | 216 | NA |

| SBI Life | 2 | 1460 | 700, 750 | 6, 3 | 13.03 | 24.86 | NA |

| United Breweries | 2 | 1700 | 900 | 3 | 23.61 | NA | NA |

| Agro Tech Foods | 2 | 850 | 550, 500 | 8, 3 | 5.59 | 19.35 | NA |

| Hitachi Energy | 2 | 4790 | 1200 | 3 | 58.63 | NA | NA |

| 3M India | 2 | 31500 | 18000 | 3 | 20.51 | NA | NA |

All above figures are approximate, many out of my memory and I can be wrong in any or all of these numbers.

Disc: Invested & Biased. Not a buy/sell recommendation. Not eligible to give any advice. Post only for academic purposes and learning. I can be wrong in all my assessments.

14 Likes

Hi- Your portfolio stocks are well-discovered: large caps (mostly), non-risky[widely owned, established businesses, stable earnings], and richly valued. It would be good to see expected ‘earnings growth’ driver for each name in the portflio update. In turn, you will be able to judge the return potential of each name compared to the long term returns of the index.

In the current state, chances of valuation rerating are dim. Returns will be similar to future earnings growth as long as current valuation (shown below) sustains:

| Company | MktCap | Mkt. Cap/Sales | EV/EBITDA | Mkt Cap/NET Oper. Profit (PE)…Data without OI and till Jun2023 |

|---|---|---|---|---|

| ITC | 574000 | 8 | 22 | 31 |

| ASIANPAINT | 311044 | 9 | 46 | 72 |

| DMART | 265000 | 6 | 72 | 116 |

| TRENT | 106086 | 12 | 96 | 534 |

| NESTLEIND | 239000 | 13 | 58 | 91 |

| PIDILITIND | 134000 | 11 | 62 | 99 |

| BRITANNIA | 119150 | 7 | 40 | 60 |

| UBL | 45365 | 6 | 79 | 170 |

| MCDOWELLN | 79000 | 7 | 45 | 70 |

| TATACONSUM | 88368 | 6 | 45 | 79 |

| MARICO | 70000 | 7 | 38 | 56 |

| DABUR | 97000 | 8 | 44 | 71 |

| GODREJCP | 107000 | 8 | 42 | 66 |

| 3MINDIA | 35000 | 9 | 52 | 79 |

3 Likes

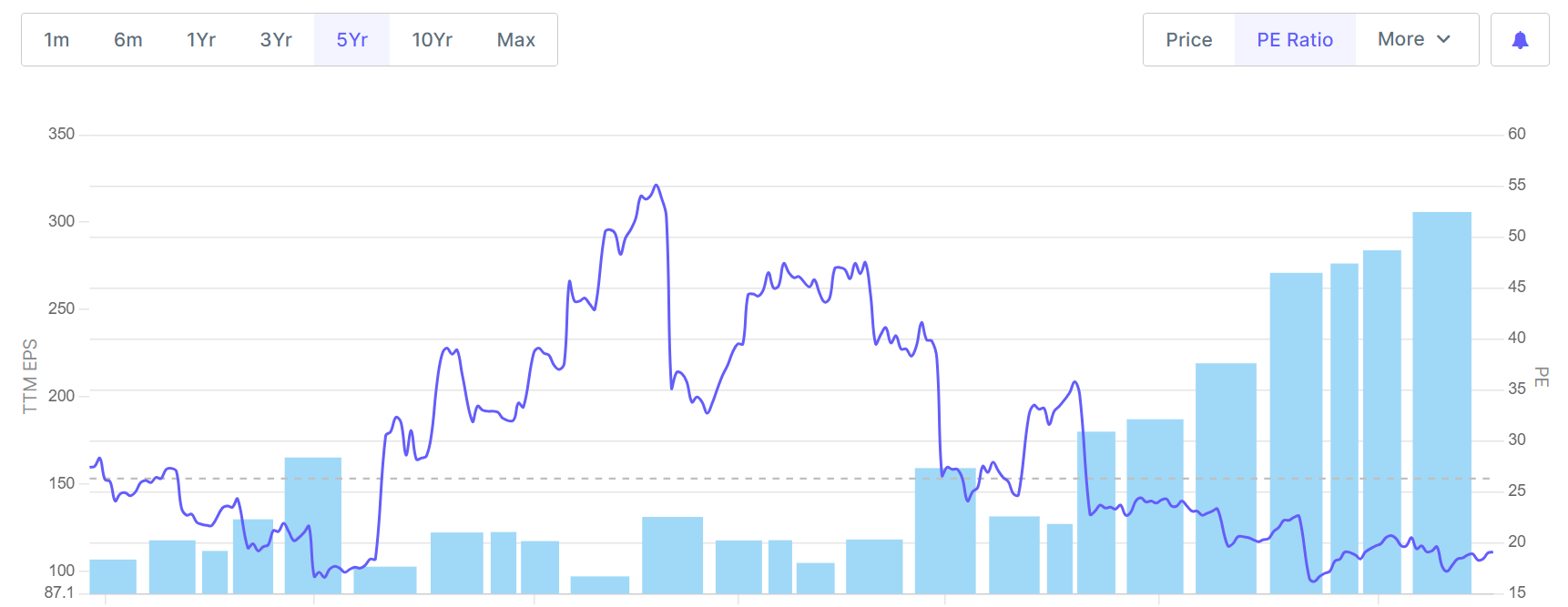

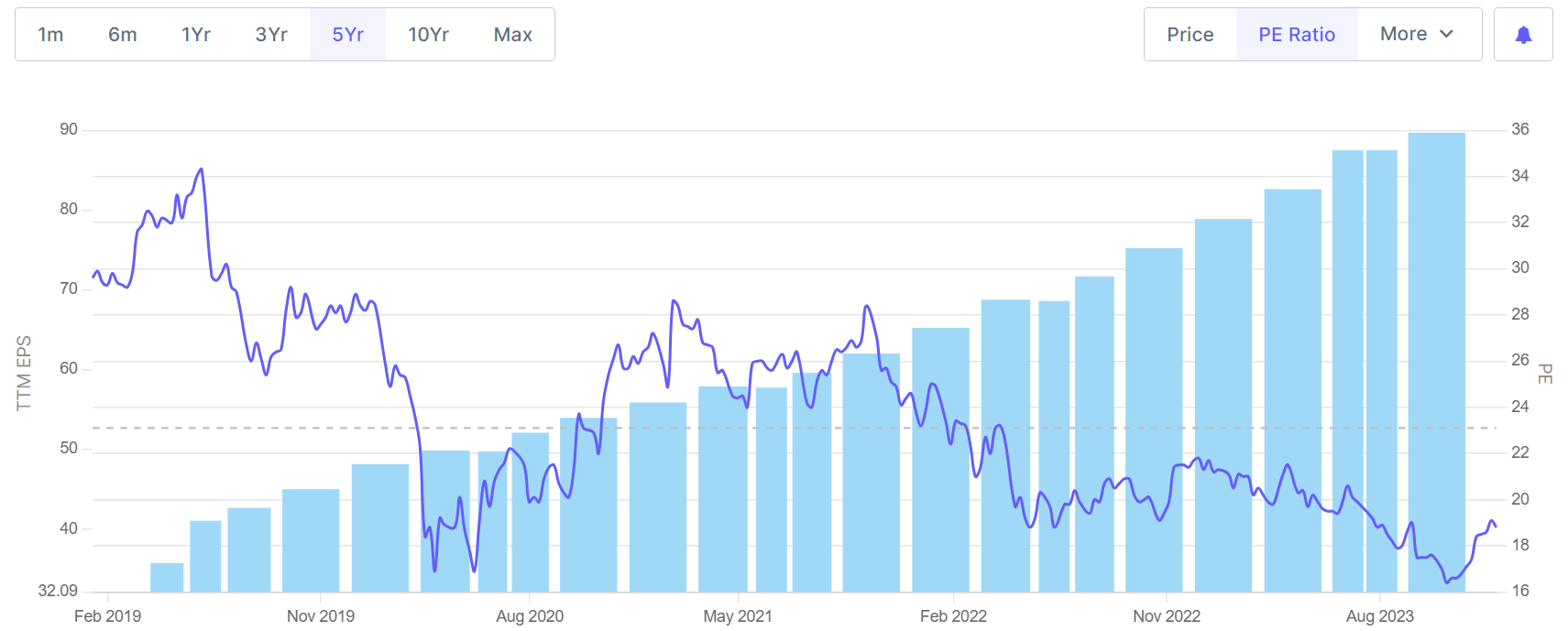

In case of Trent, zerodha shows 168 as PE while screener shows 176 but you are saying its 534, so which one is correct?

Hey- As mentoned in the table header, I derived net income using only the operating profits [ignored Other Income].

1 Like

Is that a correct measure? And what difference it makes to just judge on net operating income excluding other income? And is there so much difference between two incomes in case of Trent that PE is becoming 4 times?

1 Like

That’s not a norm, but I do so since one pays for the operating income of the business. Other Income sources are multi-dimensonal and non-comparable across businesses. The adjustment calibrates the differences to have a better comparison across buisnesses.

I cross-checked and my data has lag of 1 quarter [revised the header in the earlier note]. Intent was to roughly highlight rich valuations for most names in the portfolio.

2 Likes

For Trent, doesn’t other income come from its two major JV’s i.e Star Bazaar and Zara. Im not sure but if that is the case then it shouldn’t it be considered as operating income.

1 Like

Your method is correct, I only count EBIDTA for valuations and growth matrix, other income is always a grey area.

You bought Trent at increasing price points. What will be your action (and it’s rationale) for Trent if the price goes south?

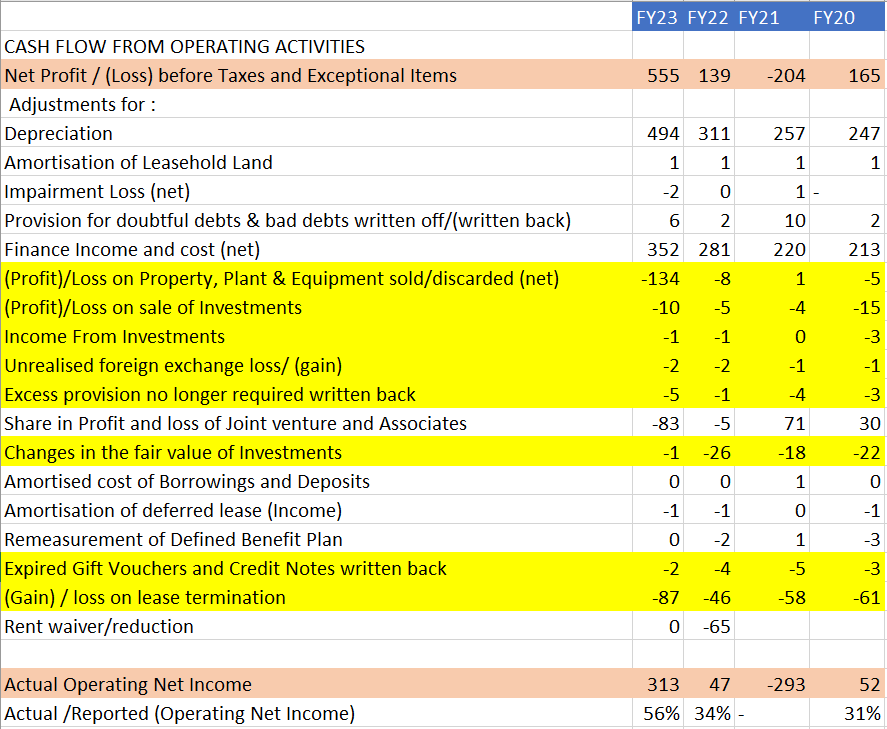

On reconciling the last 4 Yrs. PnL and Operating CFs, I conclude that Reported (Operating) Net Income is inflated due to various 1-Time or Non-Operating sources [Yellow Colored]. In turn, rich valuation looks poor as compared to the real valuation.

3 Likes

Thanks @Surender for your practical and data driven comments. I somewhat agree with you above that in most companies I hold, relating of PE looks dim as they are already highly valued.

This is a big exercise for me to streamline and jot down my thoughts. Would try to do that someday for each stock. For now, to give you a brief of it is exactly what Hiteshji mentioned…to hold such stocks we need a different mindset. It seems data would hardly support an investment thesis in most of these. Future growth drivers are also like sharing a common vision with the promoters & management we trust based on the journey done together in terms of holding and tracking company’s evolution and decision making in both good and bad times…..

I would say the process and mindset is more qualitative than quantitative in such cases. For eg. having seen Tata consumer evolve from global focused global beverages to domestic food play consumer products…..who would have anticipated each and every piece of this journey except a shared vision and hope? And as hope shapes up as reality you tend to gain further conviction even on the upside….

disc: invested & biased. Not eligible for any advice. Post only for academic purposes. I can be wrong in all my assessments.

5 Likes

Although I refrain from giving any buy/sell posts, but as you specifically ask and more from a fundamental of my investing strategy of following Simple rules….if Trent falls maybe 20% or so, I may do nothing and simple hold…while if it falls by 40% or so, I may be happy to add to my position as I feel my allocation to Retail and specifically to Trent could have been better to begin with had I been more mature when adding it earlier at lower prices.

Pls take above post with pinch of salt as I may not do exactly what mentioned above as any buy/sell/hold decision may have multiple variables and evolving conviction/mindset…..

Regarding your data, I trust all would be accurate and as thought provoking as the fact that Tatas built Zudio from the ashes of the Pandemic, the seeds of which were sown few years earlier….No analyst or investor including me would have anticipated the growth of Zudio. The big narrative Nykaa made a IPO debut at probably 1 lakh crore market cap when Trent was probably at around 30K with all the real growth engines in place to fire….Having burnt my fingers in the Nykaa narrative and seen Trent’s multiple growth formats fire in person, it was a blessing in disguise to see more value in Tata’s Trent….wish would have invested more at lower prices had been mature enough….

Dics: Invested & biased. Not a buy/sell recommendation. I can be wrong in all my assessments. Not eligible for any advice.

8 Likes

Off late I have not added any new names to my Portfolio. It’s been a long time I have evaluated anything new either. I might have added to existing names or sold some for personal needs but been very inactive in terms of portfolio creation…its been a rather portfolio management last year or so…

I am thinking of coming out of this new found tendency and bring some activity, be it only in thinking, with respect to new names or even if any existing one is at a stage of addition/Portfolio creation…

It may not be right time to do so with market on steroids, at new highs and overvaluation all around…but what it may do is make me well prepared when the going gets tough…

If I remember I once did a Trent Vs Nykaa and that helped me a lot…it was more like comparing the narrative of a new age company/ a new IPO with an existing & then boring business… My Nykaa investment debacle made me gain more conviction in Trent!

I want to use this concept a step further in the way I look at stocks, businesses. This is not a sole criteria but just one additional way of looking at the listed universe of stocks…What I would do is try to create a Nykaa/Zomato type narrative and sell it to myself for an already listed business and imagine had that company be coming afresh for an IPO, how much inflated the narrative, valuations and market frenzy would have been for it. Not that I would fall into the trap of my own narrative and end up buying it for this sole reason…but I would be able to see the same business with a different lens…I know it sounds crazy & not at all simple investing…I guess but deep down I know what it does and more so as I re read it…would write more about it next time…

Probably would start with relatively smaller caps or some relative underperformers…lets see…

3 Likes

Current market is overheated, exuberance at its peak rightnow, very difficult to find investments at reasonable valuations, turnaround, hated sector investment is best approach

Your Correct.

But even in Hated sectors like fertilizers and Oil and Gas there are very few good opportunities. And all i see on this forum, youtube and twitter is small cap pumps.

Would love to know which sectors/companies you would even venture to look at.

Thanks for the response. Abrfl i have looked at since the pandemic but somehow it never has the consistency in growth or operational excellence that makes it a steady performer. Inconsistent direction of management, a constant M&A plan that has not given outsized benefits. Would love your outlook on what works here or what are the triggers that would help it work in future,

NH, i agree with you is a sweet spot with fantastic and disciplined founder, Have not checked it closely but seems will have to do so. Thanks for this.

I feel companies in Banking/Finance sectors are somewhat under valued. I also feel Dr Reddys as a value investing opportunity. However, I am seriously wondering why these companies remain undervalued in these heated times.

Dr Reddy:

HDFC:

Random thoughts

Thinking over my current portfolio set up around 20% is in common FMCG names like Marico, Godrej consumer, Dabur, Britannia all of which had been a quick 3-5x for me (baring a Dabur) and since then have been stagnant for 2-3 years or maybe even more…

I am doing this check for only those FMCG names I have been holding long term & which have not performed well since covid recovery and couple of bull markets we had since then…

Things to ponder -

- Had it been better to have sold them off at first signs of consolidation 2-3 years back and jumped ship to another sector. I would have loved it had 20% of my this portfolio would have been in excellent companies of Capital goods, engineering …maybe a simple L&T large cap would have been an excellent purchase 2-3 years back…or an ABB!

- I might have fared much better if I switched ship but not sure if had been on my toes currently on when to sell, when to sell, when to sell the new names!!

- My current portfolio has beaten nifty pretty well over long term (not sure about midcap index though) with this 20% and another 10% in Insurance etc. Sectors not doing anything last 3 years or even more (thanks to some other names which made up for them)…Is that a good thing or bad, only perspective can tell…I can be sad thinking these laggards pulled me down or be confident that when these also start performing, I would do much better…

Thoughts are so very cyclical…inherent nature is probably not…lets see…

5 Likes

L&T did not perform for 10 years, HUL did not perform for 10 years than outperformed for 4 years and now in same league. Valuations are high PE 50-80 and it is said that they are destined to get this PE. No doubt that they are portfolio stocks but seeing all stocks rising 3X, 4X and your not moving gives lot of pain.

I have adopted a strategy of rotation and that has worked very well till now. Staying away from PE above 50 and less than 5. Finding cycles in phase 1 or entering phase 2, churning 40% of Portfolio and keeping 60% high conviction bets where more than 20% growth is visible atleast for 3-4 years.

Its like spring concept, in bull markets try to stretch your spring as far as you can by any means, trade, Small cap, large cap, sniff trades, that will help you during bear markets when spring gets contracted and every stock goes down as market can justify PE of 60 and PE of 20 for same stock, its all about us(human phycology)![]()

![]()

![]()

6 Likes

Hi @Investor_No_1… Any thoughts around HUL? Any specific reasons why you have not added it to your portfolio? Would you add at these levels, considering the long consolidation?

I try to do covered calls in large stocks and currently hold HUL and Marico from the FMCG pack. Marico gives a decent yield, HUL tends to be lower yield but I think it is at a good level and some more time correction will position it well for some consistent growth.