This is a stalemate market. We may probably be at the end of this market where a definitive move may happen in either direction.

I have personally remained strongly entrenched in my current portfolio (5-7 picks) which you know & have completely diverted my attention from stock market.

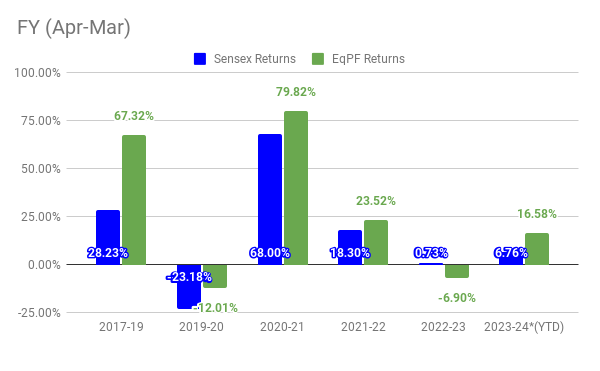

I believe, the excesses of 2009-2021 bull market is being corrected. The high quality stocks have gone parabolic & are under going time wise & price wise correction. If the business fundamentals remain same, they will pick up steam once this macro situation gets entangled. P/E is price to execution ratio. Those managements who execute (E) will get high P, other will get as long as bull market narratives last or competition catches up.

Specific to consumer names,

Durables is a dog eat dog market with Korean giants LG & Samsung being the foxes in the same market. Cut throat competition, wafer thing margins & mostly a commodity. Difficult to make money. Even the Tatas are finding it difficult. Havells is learning the lesson the hard way (Lloyds acquisition). Every one in the world now knows about “India’s consumer story”, so new competition is entering.

Retail is tough business. Very tough. Extremely tough. Dmart got it right & probably will be a steady compounder but not a 10 bagger in 3 year types. My personal preference is Metro over Bata. I personally feel, Bata is losing its mojo. It is not getting the strategy right at both entry levels & premium. I believe metro here is getting the game better. Sales growth, the management, execution, strategy, the promoters background all seems to be better here.

Even NIKE could not make any dent here in Indian market. Indian are value conscious & less vanity. A celebrity & a high voltage campaign can only take so far. Page never had a celebrity endorse Jockey in India. So did Royal Enfield. Both are fabulous business. Of course there are brands who got it right bit having a celebrity is not a sure thing for success, especially in India.

Restaurant (QSR): I have written on this recently in my thread. Please go through.

My thinking,

If normalised sales growth is less than 10% for 3 years, I think we should re-evaluate. The nominal GDP growth itself is above 10%. A successful company should be able to grow its sales at at least, 50% more than nominal GDP growth. Else, it is growing along with the wind & not doing anything on its own. Management is lazy or market dynamics are bad.

I personally start looking at something if it has grown sales at 15% or more. This takes out 95% of the companies.

Spirits market in India is besotted with so many regulations & is a STATE MATTER!! Management has to deal with all the Indian states individually. On top of this spirits is a taboo in India unlike the west. Still I think there is growth in this market & probably they are at the turning point if government acts right.

Not even 1% deserve a forward PE of 40 times. Differentiating between what deserves & what does not is that elusive chase for market participants!!!

This is the best time to re-balance personally. I would see for price pop & if there is not any fundamental change, I would seek exit on the least competitive positioning stocks & switch to better fundamentals one. The prices of most stocks were hammered a lot, so, there is a possibility of “regret” if stocks pop up a lot after selling. But all this we need to take in our own stride & follow a process consistently for a long period of time for it to show results.

Have conviction on our stocks. How? By studying, comparing with what is available in the market, compare it to stocks in other markets like US, compare with their growth rates, ROE, untapped potential etc. And once we have a strong conviction, we need to hold ground during strong sell offs with patience, time frame, mindset, temperament. OTHERWISE, strictly follow technical analysis with STOP LOSS as GOD.

Despite all this, we may get a COVID crash and cause utter confusion & chaos!! Being a trader/ full time investor is not easy. This is not for 99% of the people.

If we do our best with full integrity, the best is yet to come. Rest are all pit stops.

Disclaimer: I hold some of the stocks mentioned & this is not a financial advise or stock recommendation as I’m not a registered RIA.