Simmonds Marshall ,

Market Cap : 96 Cr ,

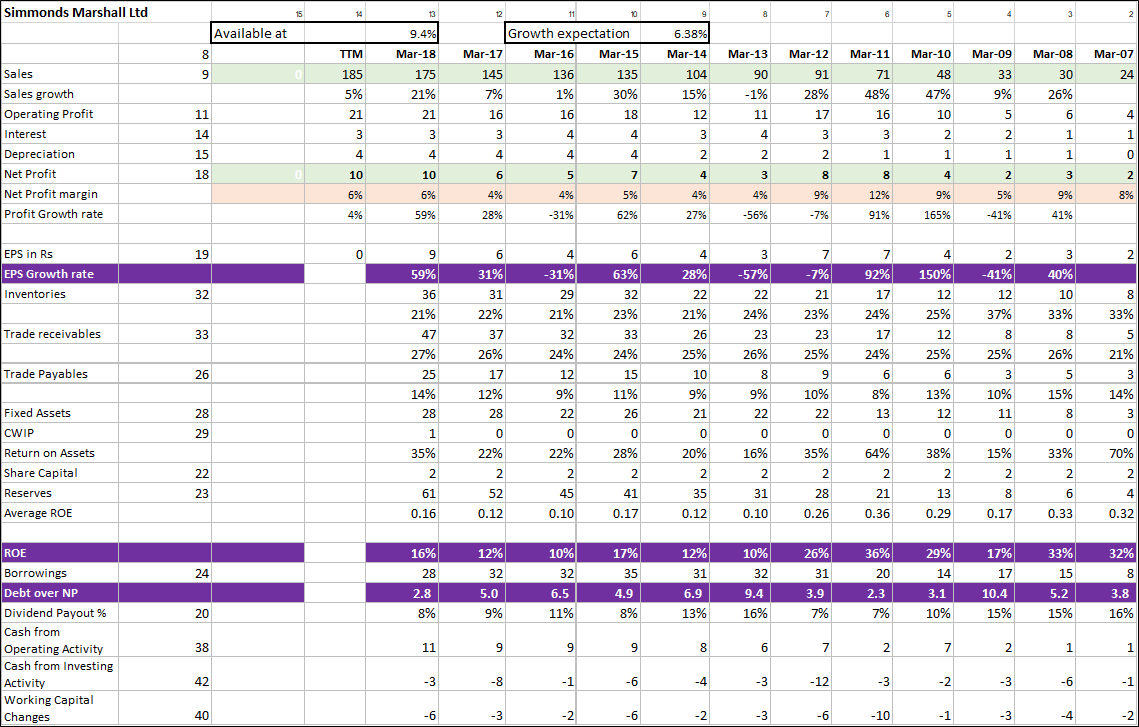

March 2018 Sales : 190 Cr ,

Profit : 10 Cr

Promoter: 57%

Sales Growth 3 Years: 9.21%

Profit Growth 3 Years: 10.38%

Sales Growth 5 Years: 13.93%

Profit Growth 5 Years: 23.24%

ROE around 15%

ROCE around 15%

Promoters Remuneration : Around 11% of Profits

Incorporated in 1960, it is promoted by Mr. Shiamak Marshall. It manufactures nuts and bolts for the automotive segment and caters primarily to commercial vehicle and two-wheeler manufacturers. The company’s manufacturing unit in Kasarwadi (Maharashtra) has capacity to produce 5,500 tonnes of nuts per annuum.

In 2011-12, Simmonds Marshall acquired M/s Stud India, which manufactures studs and supplies mainly to heavy commercial vehicle manufacturers. During 2013-14, Simmonds Marshall entered into a joint venture with Francis Kirk and Son Ltd (Francis Kirk; UK) to manufacture fasteners for the UK market; the manufacturing will be undertaken at Simmonds Marshall’s Kasarwadi plant and the products will be marketed by Francis Kirk.

Company has one associated company “Formex Private Limited” where it holds 49% share. Total investments in this company was around 12 Lakh while it reported a loss of 9 Lakh in Consolidated Statements of March 2018.

Financials :

Pros:

Established position in the domestic market and has healthy relationships with its customers for the last 10-15 years. Key clients include Honda Motorcycle , Ford , Fiat , Ashok Leyland Ltd , Mahindra , Suzuki.

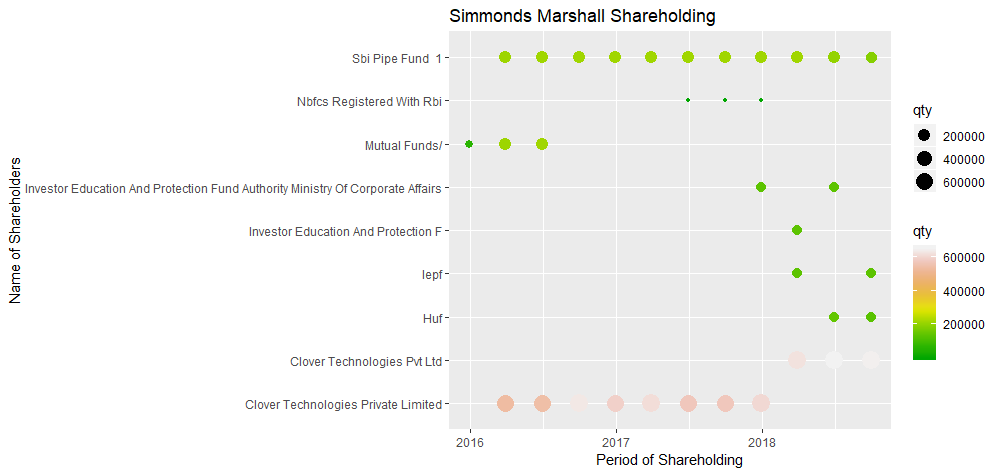

Promoters have not sold any shares nor diluted the equity in past some years. Also they usually acquire around 20000 Shares every year since 2016 last being done in October 2018.

Negatives :

Very low Equity Float of 1.12 Cr shares of Face Value 2 each. Any Market crash or bad news makes it difficult to take an exit.

Limited Market Size as it provides only Nuts and Bolts to 2W and Commercial Vehicles and no mention of any diversification in Annual Reports.

Dependence on the auto sector and any downside in auto industry will directly impact the business of the company.

Working capital-intensive business due to higher inventory requirements as well as high receivables though the Receivables to Sales number are stable around 25% .

Rational For Investment:

At CMP , it is trading around 9X TTM PE. Annual Sales around 190 Cr and is available at Market Cap of 95 Cr. Increased consumption and favorable demand from Auto sector may aid growth for the company in future.

CRISIL Rating has more details on the company Prospects :

https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/Simmonds_Marshall_Limited_September_07_2018_RR.html

Disc: Invested