SILICON RENTAL

ABOUT

Incorporated in 2016, Silicon Rentals Solutions Limited is an IT equipment outsourcing company, providing end-to-end IT equipment on a rental and returnable basis in India.

Company provides laptops, desktops, printers, servers, and other peripherals like CCTV cameras, projectors, storage devices, etc., to small, medium and large corporations.

The lease period ranges from 1 day to 36 months.

They use these equipments around an average of five years

They make around 2x to 3x the investment for a new asset on an average over the whole life of an asset.

But then over a period of time, the rental that the asset gets reduces after two or three years.

And then after that, leasing starts to slightly deplete and then the asset keeps on being used for five years, six years or more.

They have around 35,000-plus machines.

There were 52 permanent employees on the rolls of Company as on March 31, 2023.

Has a team of engineers for support and maintenance of the equipment.

Offices in Pune, New Delhi and Kolkata.

The rental business started from 2016 but they were previously into services from the last 25 years, thus having in-house engineers.

The median remuneration of employees of the Company during the financial year was Rs. 85,283/- 2. In the financial year, there is 92% increase in the median remuneration of employees.

Derived 34% of the revenue from top 10 clients in FY22.

Use of IPO funds

- for capex (related to IT equipment).

- Repayment of borrowings

- General corp purposes.

Availability of all major brands like HP, Dell, Lenovo, Apple, Asus, Intel, AMD, Gigabyte, Sonicwall, Dlink, Cisco

Flexible Tailor-made rental schemes as per Customer requirements to acquire the requisite equipment

Their rental costs are attached to two types of costs.

- One is the fixed cost (cost of procuring the equipment) and

- The second is operational cost.

- For a shorter period of rental, the operational cost is high. For longer rental durations, the operational costs reduce over time, and they have always been keen to extend extra support for a long term association by forwarding the reducing cost advantage for their clients.

The other states which are contributing to their revenue include Haryana, Karnataka, Tamil Nadu and Gujarat

There are a few peers who are at par with Silicon, many who are bigger than them.

They don’t want to be naming them.

among the competitors, Silicon Will be among the top five.

New Branch opened during the year in Hyderabad

There was an interview by a mutual fund on CNBC, that interview alone created a lot of inquiries for silicon in a few hours alone. (view video from 9:30 mins)

Samco Mutual Fund में क्यों लगाना चाहिए आपको पैसा?, कैसा है Silicon Rental Solutions का कारोबार?

got various inquiries now at least 25 inquiries in the pipeline since the CNBC interview was aired on the television in nov 17

Customers

Serving clients across various industries & sectors including the logistics solutions, BPO,

pharmaceuticals, e-commerce, education, IT, insurance, research, media & entertainment, etc.

In F.Y. 22, served over 275+ clients in India

Customized offerings to customers as per their specifications & requirements.

Supports maximization of productivity without compromising on the IT budget

Client base was of 400, 7 months ago

Now 1000 plus clients.

Further New Clients added during the year 88

Top priority is to guide their clients and tailor-make the best suited rental schemes that will prove advantageous for their business.

They offer on-site support to help resolve any issue that a client may face. When a site visit is requested, they dispatch the appropriate personnel to resolve the issue at the earliest.

When the higher level clients want new tech and equipment, the management rents the old tech to organisations which do not require such high level tech like schools, call centres, libraries, etc.

Having great client testimonials from companies like snapdeal and tata group.

RISKS

Highest revenue from Maharashtra close to 87%. Revenue is highly concentrated from one state itself.

It’s a very high investment business, in the last few years the growth has kicked in as the investments were done previously.

very asset heavy biz, without getting new equipment cannot grow.

The CFO resigned on June 22

Related party transactions worth 2.75 cr with Silicon Electronic and

Giving 24 lakh as rent to MD per annum.

Cfo/ebitda was previously close to 100% for 20 and 22 then has kept on reducing.

Following the straight line method of depreciation, changed from written down value method, this caused a lower depreciation number in the P&L, therefore boosting the bottomline

“They don’t have a client which is more than 5% of the business.”, this was said by the management, but then they have said they have 35,000 plus equipments and also said that one of their customers has equipments to the tune of 2,500.

Even if I take equipments at 35,500, 2,500 to that one client is close to 7.1% of the total revenues.

Hence proving their statement false

clients – float the inquiry six months in advance via notes of finalising the place, the location and everything else. And sometimes, they get orders overnight where people want 100 machines, they want machines to be deployed within a day or two max. So there is no fixed turnaround time for clients.

This causes huge volatility in the cash holdings and if they are short of cash, they end up taking loans.

They do not take deposits from clients, they only do the due diligence; complete checks on the client, this can be a huge risk.

We also don’t know as to what happens if the equipment is damaged by the clients, as there are no deposits being taken from the clients, the clients may refuse to payout anything and Silicon may not be able to do anything.

The receivables need to be watched out for closely.

POSITIVES

The equipment rental software market size is expected to grow from $266.78 Million in 2021 to $430.61 Million by 2028; it is estimated to grow at a CAGR of 7.1% during 2021–2028.

Return ratios are fantastic ROCE- 34.6, ROE- 31.4, ROIC- 21%

Very high operating/EBITDA margins

Being at 153 crs MCAP, the company did a concall on NOV 22.

plan to open at least four to five new offices pan-India in addition to the ones already operational, and this will help to expand and generate more revenue.

The other advantage is that as they scale up, their expenses increase only marginally. This helps them in improving their bottom line.

have one-to-one connection with all their clients, help them to keep the relationship healthy and long term.

Guided to cross INR 35 crores to INR 36 crores top line for the entire year, closed revenues at 36 cr. Hence walking the talk.

Something interesting in the works? Which can make or break.

The pipeline that they have as far as computers and computer accessories are concerned, is not yet exhausted. They have tremendous inquiries. They are looking at various orders at 200, 250 computers per company.

The advantage one can say is that the kicker comes at a later stage, where the rental keeps on coming and the depreciation has fallen down to a large extent.

Guidance FY 2023-24 06- Top line Growth by 40-50% (was 60-70% earlier)

Improvement in Net Margins

Minimum 100 new clients to be added

NUMBERS

Debt to equity at 0.04%.

Opm was 65% in 2020 and is now at 83% in 2023

Depreciation has tripled from 2020-23

Borrowings decreased from 17 to 2 crores from 2022 to 23

There are no inventory days, but receivable days have come down by a lot, close to 80 days now.

Trade receivables have increased close to 40-50% but the sales growth has also been close to that number only

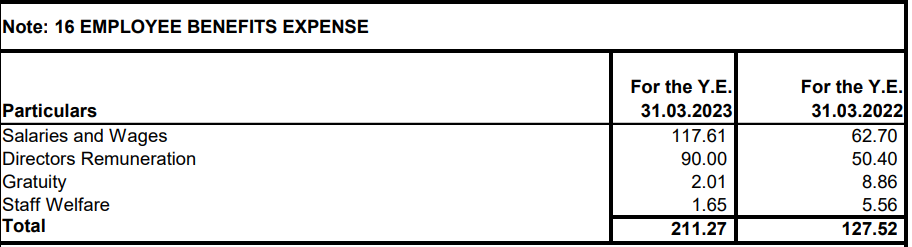

Employee benefit expenses doubled

Auditor expenses have more than doubled.

Miscellaneous expenses have more than doubled

Bad debts have reduced significantly.

The PAT margins are in the region of 30%

They are not interested in more than 1:1 in terms of debt, and will not go beyond that

GROWTH STRATEGIES

Focus on the expansion of the customer base

Continue to focus on expanding presence in the Tier 2 and Tier 3 cities

i)Large & small corporate house have started expanding their businesses in these cities

ii)Leverage expertise to offer customised services in various Tier 1, Tier 2 & Tier 3 cities in India

iii)Build capabilities across semi-urban markets in India to cater to the growing demands for IT renting services in these markets driven by the growth in the economic development in the tier 2 and tier 3 cities

There was no marketing being done by Silicon, they were growing organically according to them, but now the marketing initiatives will start.

They are going to launch themselves and are creating a marketing plan.

Now will use the ipo funds to grow branches outside Maharashtra and gain several new clients, while also reducing geographical concentration.

Marketing Strategies:

i)Focus on providing one stop solution for all IT hardware needs

ii)Focus on requirement of Customers

iii)Emphasizing on Services with value addition

iv)Continuous update of Systems and solutions offered

v)Timely service and support to gain customer confidence (extra service costs will increase as company grows if this is not monetised)

They are looking at certain places where it is possible for them to rent the equipment, which they are going to onward rent outside looking at those models.

This will help reduce the capex costs, and therefore lesser depreciation will be impacting the P&L statement

They are looking at more than a 30%, 35% spread on the rent and rent model.

MANAGEMENT

Technocrat promoters

Concall snippet, management seems very shareholder friendly.

MOAT

Their USP is that they provide end-to-end solution to their client

They provide engineers free of cost for any client having more than 200 systems. They take care of the IT department, the logistics and the service and support at all locations pan-India. This helps companies to mitigate the expenses and be free to concentrate on their core business and leave these non-profitable departments with depreciating assets to Silicon to handle.

They purchase equipment in large quantities, this enables them to negotiate the best rate when they procure them from the channel partners. They also have their inventory across the country. This helps them to work on very competitive prices and keep the costs down.

Takes care of everything, maintenance, upgrades, fixing problems.

They provide the computers, the backup, insure 100% uptime because they give standbys for every computer.

The headache of maintaining logistics service and especially when this work from home culture is going on.

So for the clients to deploy those 1,000 and 5,000 laptops/computers/other equipment to various different locations is not a small task - whereas Silicon has a mastery over this.

a simple example- Logistics, sending a laptop from here to Delhi for them probably with the top brand will cost them probably 2,500, which Silicon does at INR 900. So effectively, they’re going to save a lot of money on these things.

ENTRY BARRIER

Two entry barriers, first big investment by companies to get so many laptops/computers

then wait for a long time to get the rental yield on it (3-4%),

getting customers- customers need reliability and trust, because computers are an essential equipment and if they stop working, can impact the day to day operation of the client.

Getting bigger clients is more difficult.

‘’any insight which you would like to share in terms of the competitiveness

Where is the question? I mean you tell me how many people can afford to buy 100 laptops at one shot and just – and expect a return of just 3% every month, whatever, 3% to 4% every month and provide service. So where will they be to survive what competition there is? Is at a lower level where people need five laptops and 10 laptops at such – so when you’re looking at a bigger number and believe me, we have quantities to the tune of 2,500 machines that’s one location, one company. So how many people can actually afford to scale up to that level’’

CONCLUSION

There are many competitors in this space, and

i couldn’t find any entry barriers for this business, anyone who has capital can start this up in my opinion.

The customers would like to have the cheapest rental cost, and hence no switching cost in my opinion.

Seeing the returns earned by silicon, various companies may try to enter this business, therefore increasing competition.

The company may grow very well, but I couldn’t find a place for it in my portfolio.