Hi,

I have been active for a few years now, never though of doing this, but I feel writing down your thoughts is the best way to grow. I usually invest with the following criterias:

Market leaders, Zero or negligible debt, Strong brands, understandable business model, Strong ROE. I have a very long infinite holding period, and very cautious about my entry price. Most of the stocks in the below list have been acquired during the steep corrections in the past 3 yrs.

I do take opportunistics bets to the tune of 10% of my portfolio.

Would request feedback on the investment style or point out any red flags wrt to sector or stock exposure

5 Likes

Good ones. Apart from ROE, please look at the below also:

- Revenue growth y-o-y

- Low dividend distribution (because of which ROE should go up if money reinvested well)

1 Like

Thanks. Most of these are growth stocks, with a basic check of >10% rev growth over 5 yrs.

Also, few stocks like APL,Nocil have completed a decent capex cycle, and should start paying good dividends in the coming years

Suggestion is to move more money into the stronger balance sheets in a correction during CY Q1’2021. Sell the non-performers and keep churning slowly. Also, when portfolio gets out of whack with some gaining too much, sell those and do a rebalancing. I have the hardest time doing it since I have RIL, HUL, LT, TaMo, TISCO and they hold high %, and when these stock hit New Highs, I start selling a bit of those shares (100-150 shares slow sell, which I call as SIP Selling).

KKP

Thanks for the reply. I am uncomfortable selling, if the growth story intact even if it skews my portfolio allocation. Would want to ride the growth period of the company and sell only when the growth stagnates.

1 Like

Hi Sidkat

My thoughts.

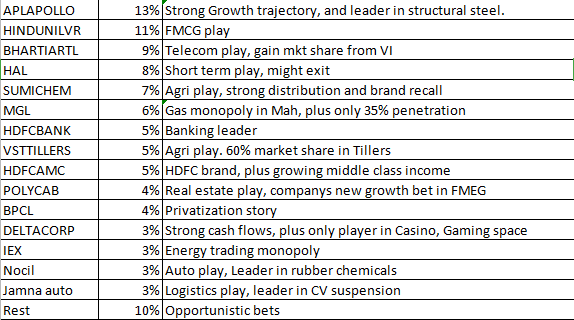

Holding which i Like APLapollo,HUL,Sumitomo,HDFCbank,HDFCAMC,Polycab,IEX.

Feedback/thought on below companies:

VST Tiller: They haven’t able to grow business last 5 years. Pre-covid itself their sales going downhill and OPM going down.ROCE going to single digit from 20+ which they had few years back.

Mahanagar Gas: Similar fate where their moat at Mumbai area but they couldn’t able to increase sales + PSU backed. Any day govt may change policy.even 100% they achieve how much sales they can grow in mah plus as other location expansion wont happen easily due to geo limit situation.Whole market itself limited number .its big fish in small pond situation.

Nocil-> OPM going downwards recent years , Promoter holding going downwards.any specific reason to hold this.many credible chemical company available .

Janma :- Its better to play main player like Maruti or M&M then supplier like jamna. Auto company itself going tuff time in market cycle and their supplier don’t even need to say a word pain they go through.

HAL,BPCL-> PSU and I avoid.

DeltaCORP -> Promoter holding low,Roce going downwards. Not generated return to shareholders.

Until we know entry and exit above stock look cyclical and tend to perform based upon market cycle.

If you wish add defensive IT/Pharma/consumer .

1 Like

Thanks for the detailed response. I am betting on cos like Nocil,Delta corp since majority of capex is over and expect the asset turnover to kick in. Agree on the PSU front it was more of an event play and will not be a part of the portfolio anymore. Avoid pharma as dont understand the terminologies and beyond my understanding.

1 Like