Introduction

SPL has been engaged in real estate development for over two decades, mainly focused on the mid-market and affordable housing categories.It is a part of the Shriram group that has four decades of experience in retail financial services and various other industries

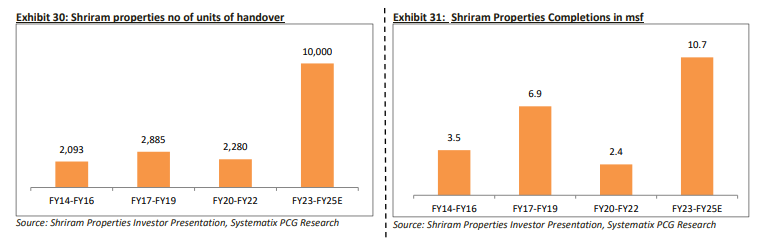

During FY23, they completed seven projects, three residential and four plotted, with a total saleable area of 3.8 million square feet and handed over more than 2,000 units/plots

For the nine-months ended Dec’23, overall volumes stood at 3.03 million square feet, up 12% year-on-year. Sales value at around Rs.1,654 crores was up 22% year-on-year. Collections are above the Rs.1,000 crore mark, and handovers to-date stand at 1,619 units, reflecting a 29% year-on-year growth

Business Model

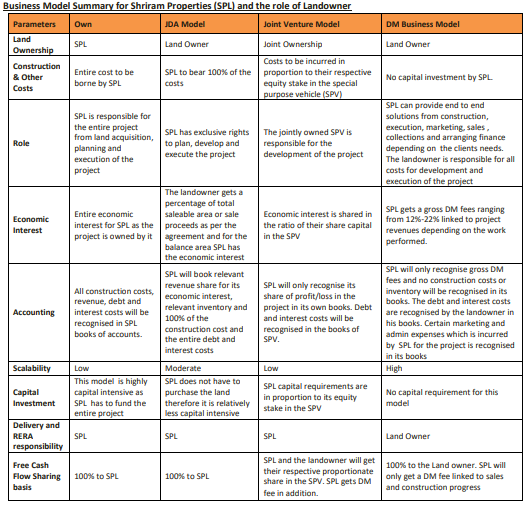

Company develops projects under 4 models.

- Own- where the land is owned by the company and end-to-end lifecycle is owned by them

- JDA- Here the land is owned by someone else, but SPL will construct and sell the units for the landowner. % of commission per sale is given to landowner all other revenue and cost is borne by the company

- JV- This is where the SPV also invests, where some capital is put in by SPL

- DM- Development management- SPL charges a flat fee and incurs no construction cost

Development Management (DM) model is value accretive and a growth engine: The company is focusing on the development management model which is aimed at small developers and landowners. In this model, the land is owned by the landowner and the company provides end to end solutions to their customers. The services include project planning, launch, sales, collection, construction execution and handover. Everything is done in the brand of Shriram. The services are provided for a gross DM fees of typically 20-30%

Source: Systematix report

ASK platform

The management has struck a strategic relationship with ASK Group in Nov 2022 to help fund its projects. Under the platform arrangement, Shriram Properties and ASK will co-invest in residential developments projects. Aggregate commitments towards the platform will be up to Rs 500 crs and the entire committed capital is expected to be deployed over 12 months from the date of agreement. ASK will invest through its managed Category II Alternative Investment Fund (AIF). The partnership platform will provide Shriram properties a committed capital availability and allow them to seize new opportunities for further growth and value creation efficiently.

(The company has explained this in the Bharat Conference held by Arihant)

Shriram - ASK Platform

-

Shriram Properties Limited and ASK Property Fund jointly formed a Rs 500 crs co-investment platform in Nov-22. to invest in plotted and residential developments project where ASK will fund 80% and SPL will fund the balance 20%

-

In the first stage of returns, ASK and SPL will get a 13% coupon on their investment. Apart from this SPL get a 10% DM fee in stages from the project. There are no guaranteed returns beyond the initial 13% coupon for ASK. Also after the cash flows are used to pay the coupon and DM fees, the balance cash flows if any are divided pari pasu and the returns for ASK are capped at 20% IRR. The balance cash flows if any belong to SPL.

-

The co-investment platform’s maiden investment in Shriram Pristine Estates, a premium plotted development opportunity, is performing well and exceeding expectations on volume and pricing since its launch in Feb’23.

Financials

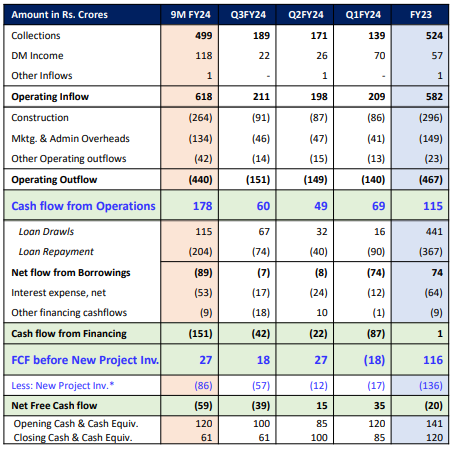

So far FY24-

- Satisfactory 9M performance despite Q3 adversities

- DM remains steady contributor: 10% of total revenues; volume share to rise further with launches

- 60% of Revenues to-date driven by recently completed projects - Grand City, Shankari, Southern Crest, Liberty Square and Park63

- EBITDA up 14% YoY, PBT up 11% YoY, PAT at Rs.55.3 Crs

- EBITDA margins at 25%, compared to 21% in 9MFY23. Increased confidence on stabilising around mid-20s in FY24

- Earnings would have been stronger but for delayed Ocs; Most of the OCs received late Dec’23 / Jan’24 Recoup of deferred revenues in Q4 FY24; SPL’s full year expectations largely intact

- Cash From Operations at Rs.178 crs, compared to Rs. 115 crs in full year FY23

- Interest cost flat, overall finance cost up 15% YoY due to one-time costs related to Shriram 122 West acquisition.

- Cost of debt stabilising around 11.5%

- Q3 suffered on delayed receipt of OC’s and consequent deferred handover/sale deed regn resulting in deferment of revenue recognition to Q4 FY24

- deferred launches impacted potential DM Fee income from new launches for the quarter

- YTD interest cost also reflects one-time interest cost of 12 Crs absorbed during H1FY24, associated with the acquisition Chennai project (Shriram 122 West) till its transfer to ASK co-investment platform

- Gross debt to be on declining path again in FY25; Cost of debt stabilizing around 11.50% levels

- Gross Debt at Rs.508 Crores; Net Debt Rs. 447 Crores

.

Projections

- Total revenue from operations is expected to grow at 27% CAGR from Rs 431 crs in FY21 to Rs 1,132 crs in FY25E.

- EBITDA is expected to grow at ~32% CAGR from Rs 50 crs in FY21 to Rs 150 crs in FY25E

- PAT is expected to grow from a loss of Rs 68 crs in FY21 to a profit of Rs 115 crs in FY25E.

- 70% of aggregate revenues over next 3 years to come from volumes sold as of Mar’23

- 55% of aggregate DM fees over next 3 years to come from projects launched already

- Nearly Rs.300 Cr of FCF likely in next 3 years at an enterprise level

Project execution

- Handed over 1,600 units in 9M

- OC for 1,000 units received only in Dec’23, to support record high handovers in Q4

- 3 Bangalore Projects received OC – (Greenfield, Chirping Woods T5, Liberty Square) – ahead of RERA timelines

- On track for FY24 handover/revenue recognition targets- 3000 units handover v/s 2000 units in FY23

- Avg. realisation up 15% during 9MFY24, beyond the ~8% hike seen in FY23. This in comparison to avg. price hike of 7% in Bangalore & 4% in Chennai

- The mid-market avg. realization rising gradually - at Rs.6,200 vs. 5,000/sqft in FY22

- 42 projects with 44 msf development potential

- Includes 24 msf across 26 projects in ongoing projects.

- LOGOS deal to be closed in FY24, subject GoWB approvals

Pune Market Entry

- 1.7 msf resi project at Undri, Pune on DM Model

- Target launch by Mar/Apr’24

- Strong project pipeline to support growth momentum

Risks/Ongoing problems

Geographical concentration- Bengaluru

Promoter Holding is low- under 30%

Recent IT order- was regarding an old matter of Gateway office parks and dispute of the value of orders that the company got. The order is currently in dispute in high-court when the IT order came to pay for 2xMAT on income tax, so the company believes it should be dismissed and is unfair.

The ongoing litigation with West Bengal government regarding 4% royalty payable on sales resulting from the development of the Kolkata plot which it has challenged. The liability amount is Rs 194.47 crs and along with accrued interest of 6.25% the value of the liability in the books is Rs 212.29 crs as on 31st March 23. The fair value of the liability is expected to be about Rs 260 crs by the end of monetisation of the Kolkata land parcel as on 31st March 2026.

In the past there has been timeline problems with legacy projects. Last 2-3 years there has been an overhang due to the same.

Another INDAS treatment where private equity investment got treated as debt increased the deemed interest burden.

Conclusion

Company estimates that they will be able to make 300 crs in FCF in FY26, and my back of the envelop calculations believe it should be somewhere between 300-330 crs, if the current projected pipelines happen in a timely fashion and there are no unforeseen costs.

Based on that, the company at 2070 cr Market cap, it is trailing at 10 forward PE. It isn’t overvalued and has the levers to outperforming the market.

Sources:

Company Presentations and documents, Systematix Report, Credit reports, attended concalls

Disclosure- Not invested due to other personal reasons