I liked this company - P/E ratio, Sales Growth, Growth in Profits, ROE, ROCE, and Market Segment, pretty much everything.

https://www.screener.in/company/512453/

Key Ratios:

P/E : 9.76 ( Wow )

Sales Growth (3Yrs): 17.50 %

ROCE: 44.72 % ( Again Wow )

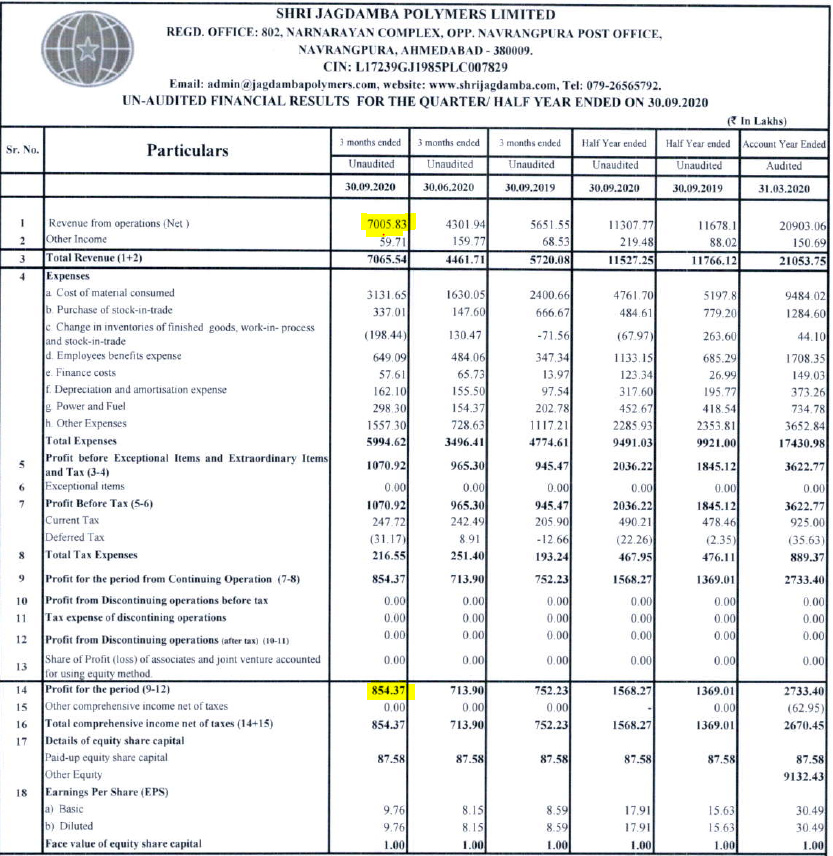

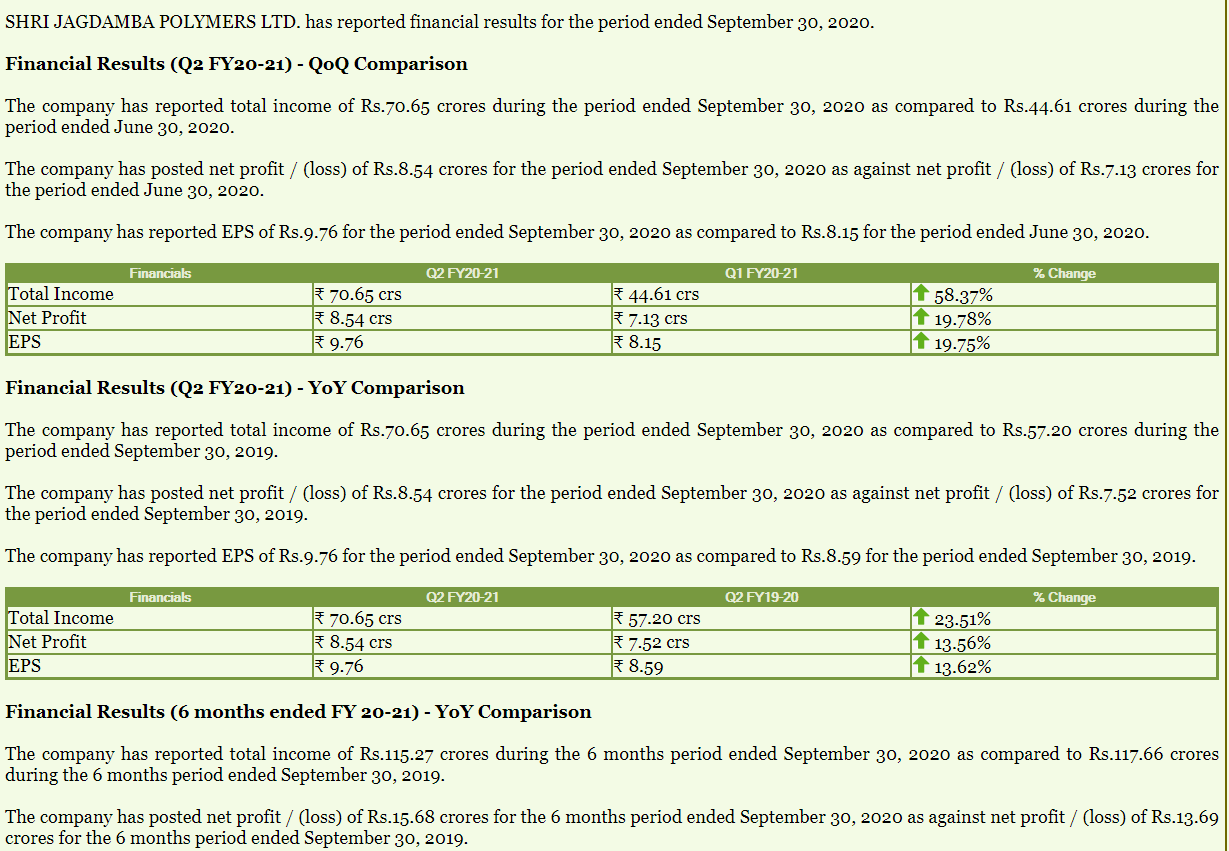

Narration Mar-14 Mar-15 Mar-16 Mar-17 Mar-18

Sales 89.19 110.40 122.13 146.88 179.09

Net profit 3.14 3.34 5.02 5.71 16.47

EPS 3.59 3.81 5.59 6.36 18.34

P/E 1.23 7.61 7.17 12.15 11.43

Price 4.40 29.00 40.10 77.27 209.72

ROE and ROCE - Above 20 % is usually hard to find, and that too in small cap.

Sales Growth - Above 15% over the last three years is also not easy to find, especially with the above combination of ROE and ROCE

How did I find this company ?

I read industry reports, and identify industries that has double digit growth potential for the next 3-5 years. Once industry is identified, I look at companies present in that industry. As per industry reports, there would be double digit growth in packaging industry, especially cardboard and flexible packaging. The cardboard packaging is done by multiple small players, and I could not find a niche player. One niche player is doing good, but their capex is quite high. In flexible packaging, there are few decent players, but their promoters were not trustworthy, IT raid and what not.

During my research, I come across Shri Jagdamba Polymers Ltd. Although it not pure packaging company, it belongs to technical textile segment which is expected to grow in double digits in India due to government support and large market. I thought that I found my diamond. There is not much trading on this stock, so I do not expect this stock to go through wild gyrations either.

There are three major issues.

a. R&D - To grow in technical textile, a company must spend funds in R&D, whereas Jagdamba did not spend in R&D. This point is OK, as they can ride growth for sometime as there is large demand for their products at this time and next 2-3 years. However, there are multiple MNCs and few mid cap Indian companies in technical textile space that are doing research and trying to move up the value chain.

b. Salary of MD - Over the last five years, our MD had increased his salary by 50% multiple times. As of now, it was below Rs. 1 Cr which is not bad. I can live with this, and hope that he would not give such a high jump every two years.

c. Two major conflicts - In one similar company ( technical textile and packaging space ), the MD holds above 25% stake, and it seems that this company is run by his son. The son is also shareholder in the main company ( Jagdamba ). Basically, the promoter of the main company consists of husband, wife, his son, and one lady ( most likely wife of son ). These four guys hold shares in this another company. As per one article on internet, all four live in a single house in Mumbai. The two companies ( main company and company probably run by his son ) are doing business with each other as well. The MD and other director of main company are running another company. Why do not they merge all these companies ? What is the succession planning ? Are these companies not competing for the same customer or at least same market ?

I could be wrong in my assumptions, and I am sorry if I offended directors of the company. I do not want to hurt anyone. I just want to be careful with my hard earned money.

Disclosure : Not Invested