Incorporated in March 2018, Shree Karni Fancom Limited specializes in Woven Fabrics, Knitted Fabrics, Coated Fabrics, and 100% polyester, and sources yarn, resin, acrylic, and coating chemicals to produce specialized technical textiles.

Product Portfolio - Application

A) Interlining Fabric - Jackets, wallet and hard luggage

B) Tafeta Fabric - Back-packs, rain cover, umbrella, vehicle cover, soft and hard

luggage

C) Matty Fabric - Soft and hard luggage, back-packs

D) Air Mesh - Backpacks, shoes, chairs, masks, helmets, medical arch support.

E)PU Coated Matty - Back Packs

F) WR Coated Lining - Back-packs, rain cover, umbrella, vehicle cover, soft and hard

luggage

G) AF Coated Lining - Back-packs, soft and hard luggage

H) PVC and EVA Lamination - Soft Luggage

Expansion

Company is setting up a new dyeing facility (backward integration) and manufacturing of bags (forward integration ). It has purchased land in close vicinity to its existing facility

Management

- Rajiv Lakhotia

- Manoj Kumar Karnani

- Raj Kumar Agarwal

- Radhe Shyam Daga

Manufacturing Set up

- Knitting Unit - 90 tonnes/month

- Weaving Unit - 70000 mtrs/day

- Dyeing/coating Unit - 100000 mtrs/day

To ensure to supply quality products which meet the applicable standards, they have set up a Research and Development facility (“R&D facility”), which consists of quality assurance and quality control teams who check and conduct various tests in their ‘in-house laboratory’ on the fabrics at various stages starting from grey cloth to the finished fabrics manufactured.

Acquisition

Company has acquired a 66.67% stake in IGK Technical Textile LLP w.e.f. October 31, 2023, which is engaged in weaving, coating, sizing, and embossing of specialized technical textiles.

IPO Details

Co. raised 42.5 Crs through the IPO and got listed on March 14, 2024.

The Net proceeds will be utilized for:

- Funding the capital expenditure setting up a dyeing unit in Navsari District, Surat, Gujarat;

- Funding the purchase of new machinery

- Working capital requirements of the company;

- General Corporate Purposes.

Clientele

Khadim, VIP, Samsonite, Bata, Hidesign, Tommy Hilfiger, Safari, Benetton, Swiss Military etc

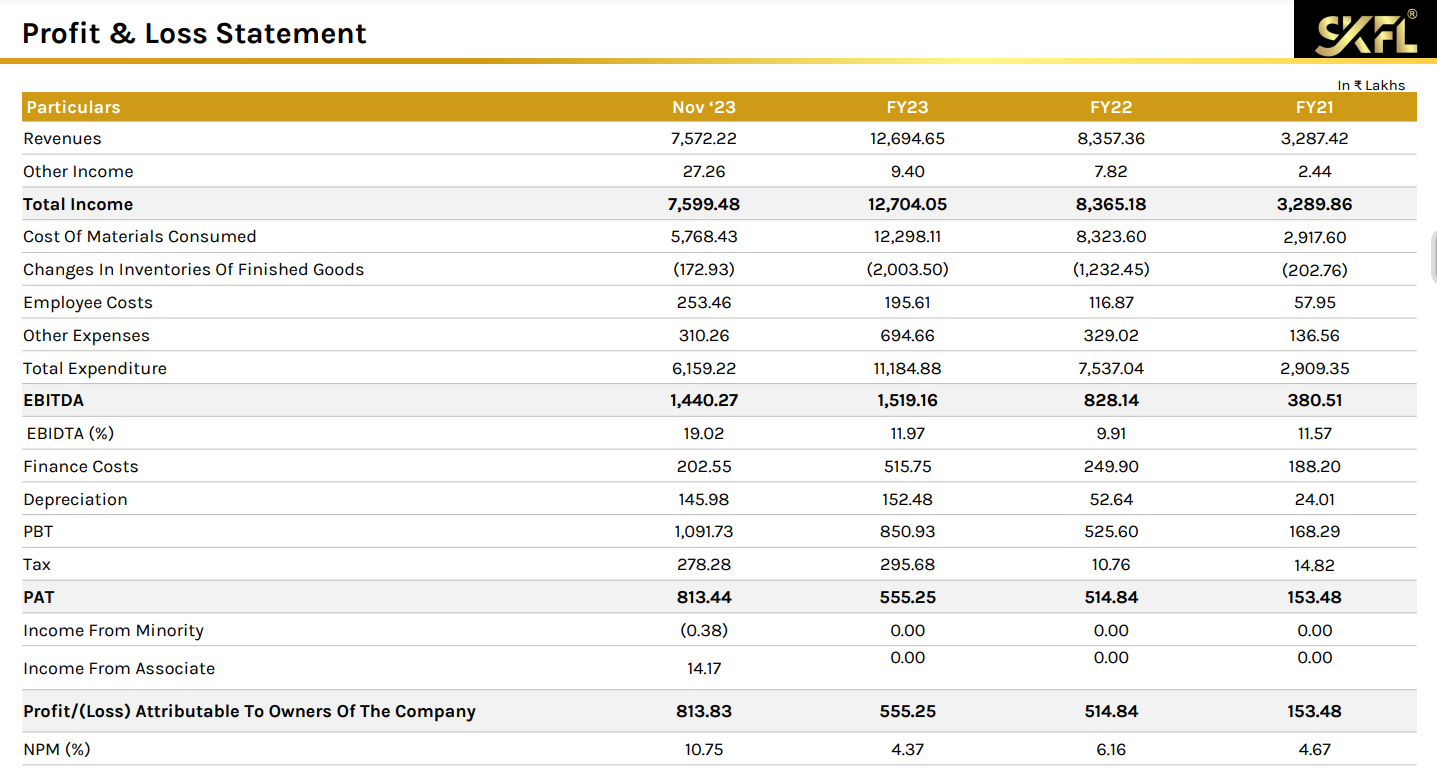

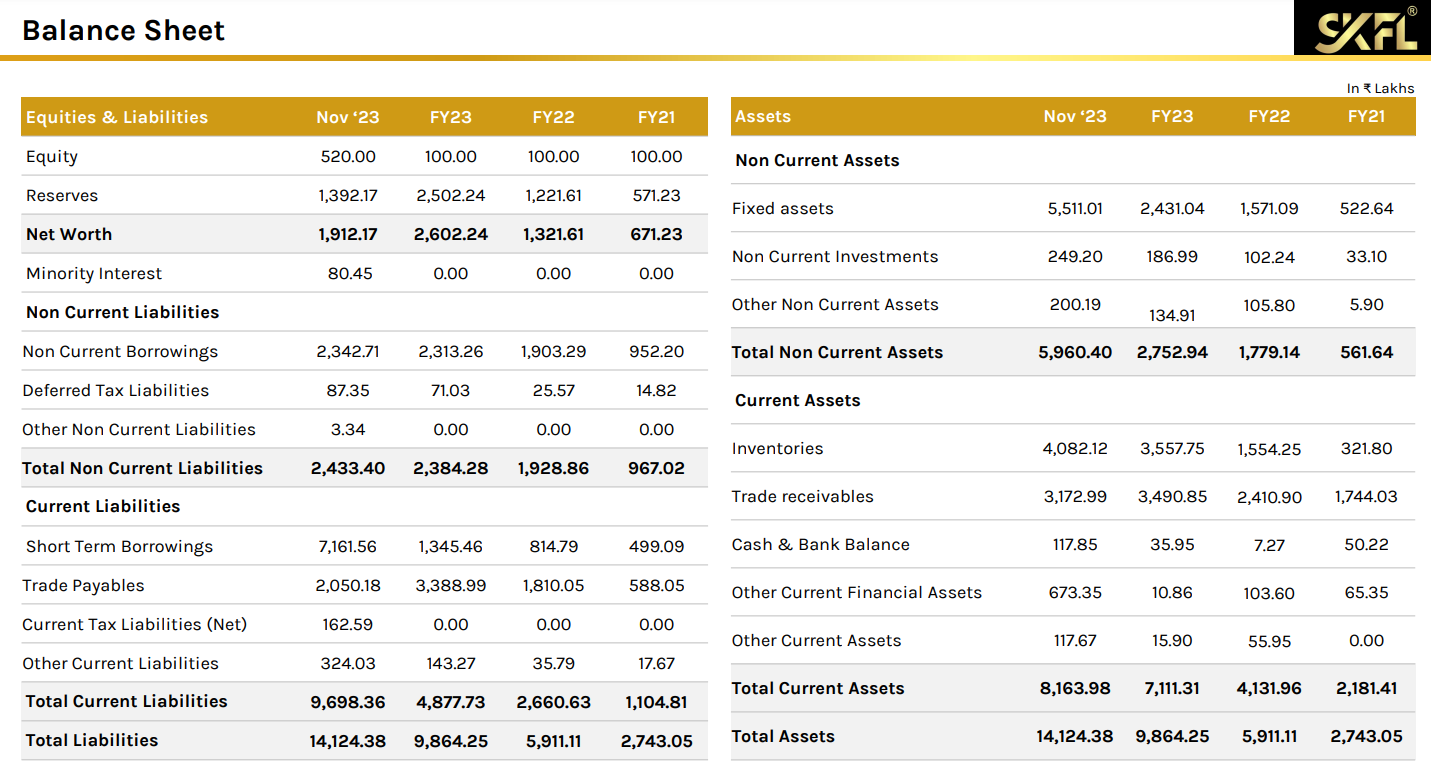

Financials-

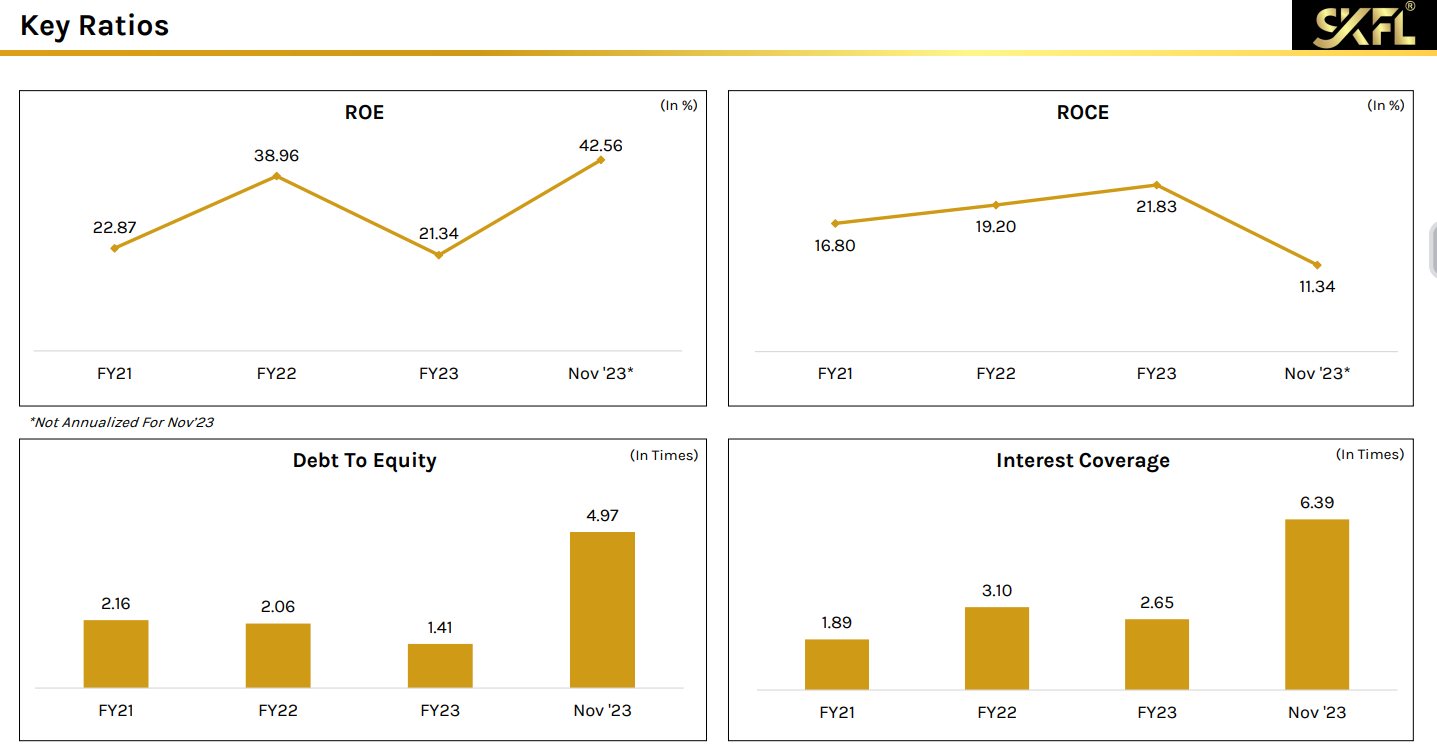

Key Ratios

Red Flags -

- The company availed Interest Free loan from the promoters - 2378.76 Lakhs

(couldn’t understand what the company is planning on - It means their PAT would have been much lower if they would charge interest on this loan amount)

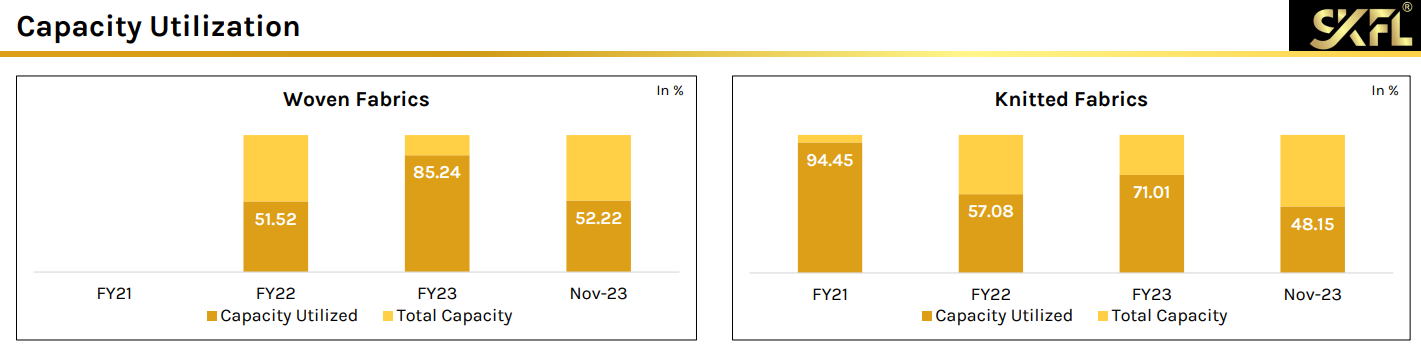

2.The capacity utilisation is very low.

- Top ten Clients cater to 74.23 % of the revenue (as of latest data in Nov’23) - Needs to diversify its clientele.

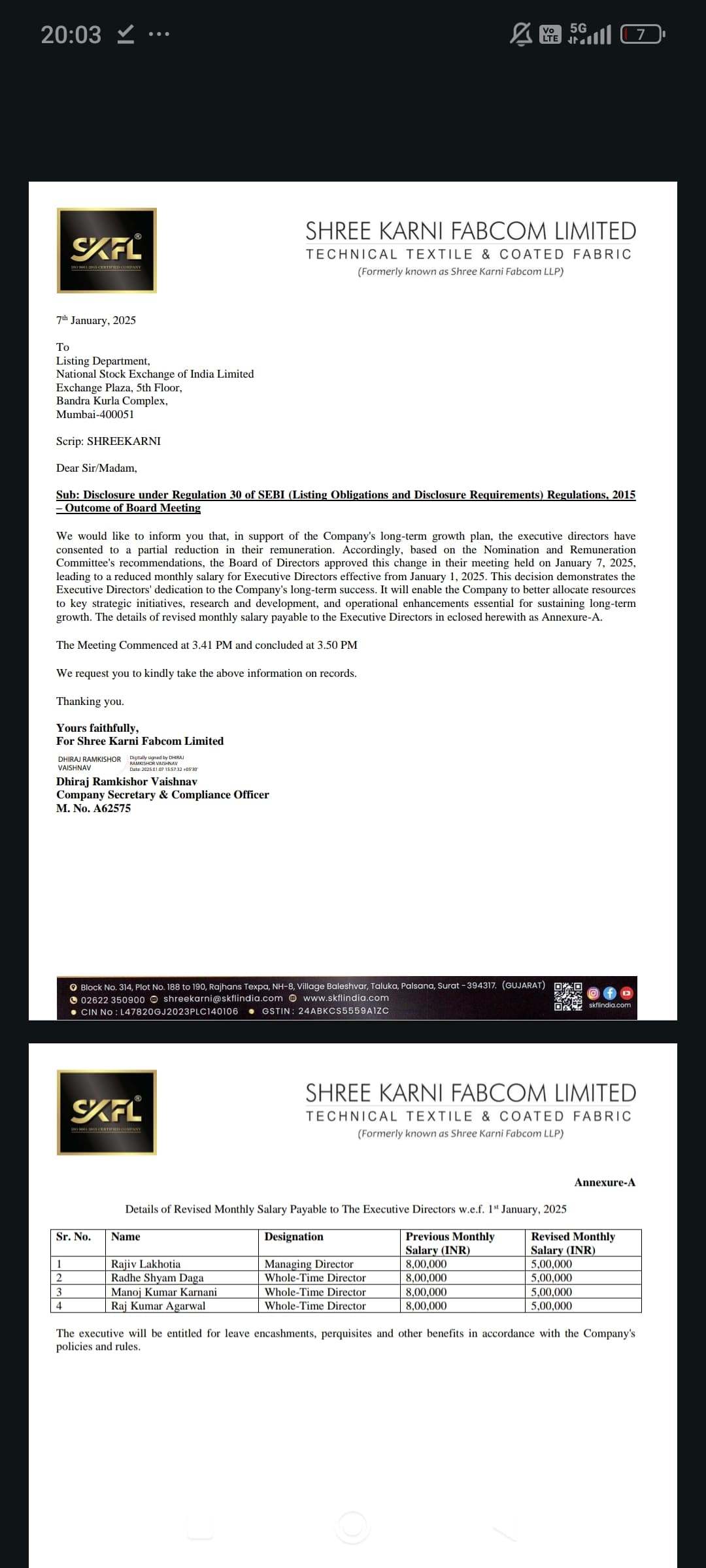

Disclosure:

Invested