Shivalik Bimetal Controls -

Q3 FY 26 results and Concall highlights -

Shivalik Bimetal Controls Limited (SBCL) is India’s only fully integrated manufacturer of precision thermostatic bimetals, low‑ohmic shunt resistors and silver contacts, critical components that enable accurate sensing, switching and thermal control across electric vehicles, smart meters, switchgear and energy‑storage systems

Headquartered in Himachal Pradesh with three manufacturing campuses and sales nodes in the US, EU and Asia, SBCL partners with 300+ OEMs/Tier‑1s in 38 countries

Details of company’s product portfolio -

Shunt Resistors - ultra low ohmic current sensing components. One can think of them as electrical traffic cops - precisely measuring the flow of current in a circuit. Company makes these components using Electronic beam welding - a difficult technology to master. These shunt resistors find applications in - BMS, Smart meters, Industrial drives, Gas metering, Charging Infra, Power modules

Thermostatic Bimetals - these r metal alloy strips that bend predictably with heat - causing opening / closing of circuits. Used as essential components for protection against overheating, for temperature control in various devices. Primarily used in - swithgears, geysers, irons, automotive thermostats and other Industrial applications

Electrical Contacts - they facilitate the on/off switching of circuits, regulating the flow of electrical power. Used in lighting and wire accessories, circuit breakers, smart meter latching relays, auto and electrical appliances. Company offers end solutions to market by providing ready to use sub-assemblies, combining the manufacturing of electrical contacts and joining them onto complex sheet metal stampings

Company’s Manufacturing facilities -

Plant 1 Solan - EB welded shunt resistors - peak revenue potential of 700 cr

Plant 2 Solan - Thermostatic Bimetals - peak revenue potential of 600 cr

Plant 3 Solan - Electrical contacts - peak revenue potential of 300 cr

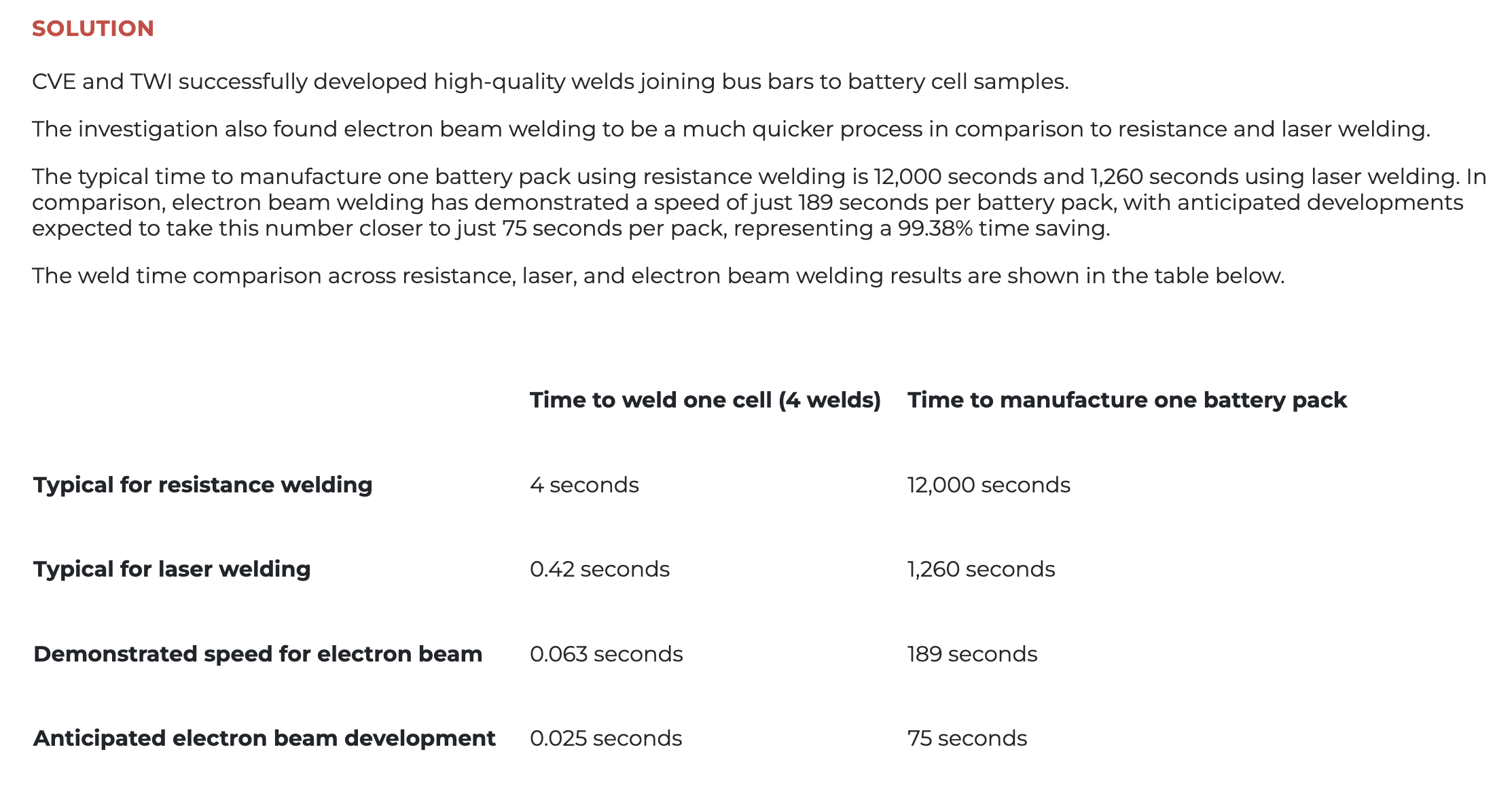

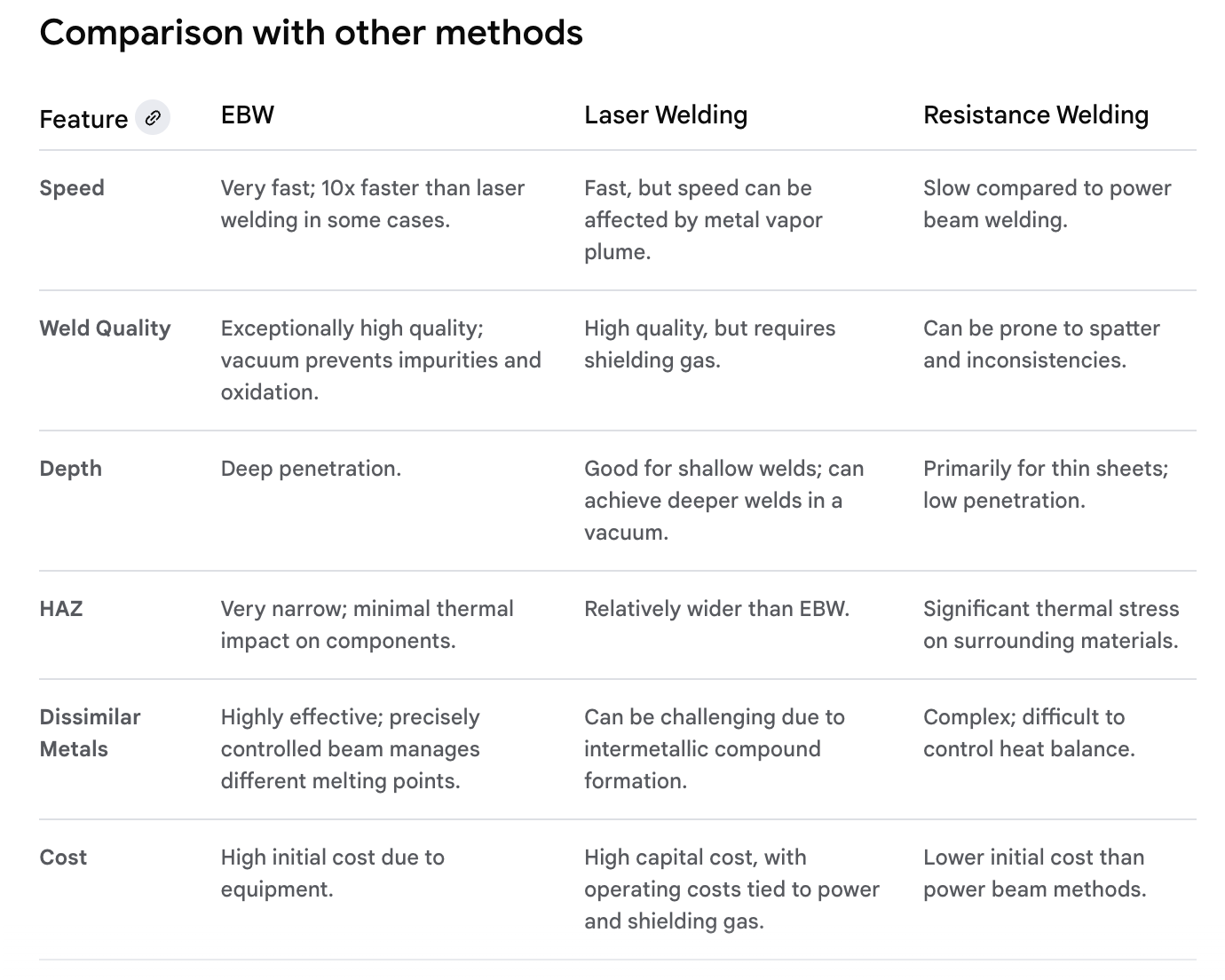

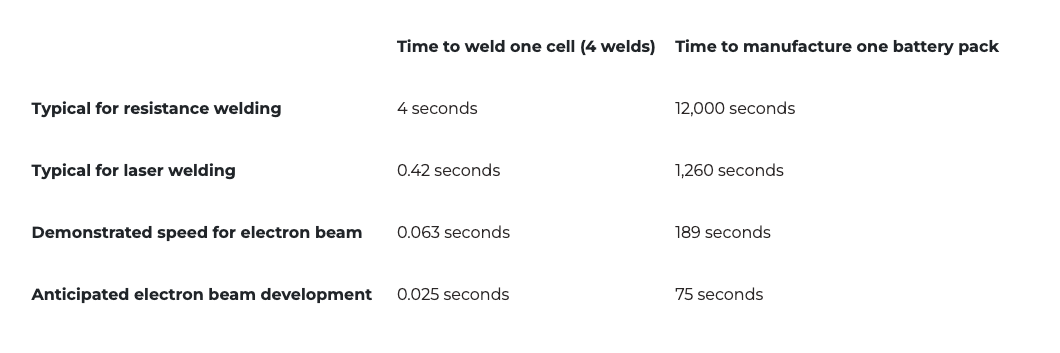

Company’s expertise in Electronic beam welding -

Imagine using a super-focused, high-speed beam of tinyparticles (electrons) to melt and fuse metals like copper and manganese together with incredible accuracy

Think of it like a very precise beam welder, but instead oflight, it uses electrons in a vacuum to create strong and clean joints

Shivalik can build these specialised welding machines themselves for about half the cost of buying them from overseas

This allows us to make industry-leading shunt resistors that can measure electrical current with very high precision. Only a few companies have this expertise & SBCL stands as a leading EBW welder globally with large capacity

Company’s expertise in Diffusion Bonding -

Picture pressing different metals together very tightly under high heat and pressure for a specific time. Over time, the atoms from each metal mingle and create a strong, seamless bond, almost like they’ve become one, without disturbing the original properties of the alloys joined

It’s like slowly merging two pieces of dough together by pressing them, they become a single piece

This process allows Shivalik to quickly develop new combinations of metals (bimetals) with specific properties, which are essential for customers in industries like switchgear, HVAC, and electrical appliances

This can lock customers into using Shivalik’s designs for many years. Shivalik manufactures grades of bimetals using this method as a critical component with high-switching costs for global marquee clientele

In the same way, cold pressure bonding is also part of

Shivalik’s machinery capabilities, following the same process of diffusion bonding without heat

Q3 outcomes -

Revenues - 134 vs 123 cr, up 9 pc

Gross margins - 47 vs 44 pc

EBITDA - 32 vs 25 cr, up 30 pc ( margins @ 24 vs 20 pc )

PAT - 22 vs 18 cr, up 22 pc ( includes one time impact of aprox 1 cr towards implementation of new labour codes )

Sales breakup - Shunts : Bimetals @ 55:55 cr vs 51:55 cr

9M FY 26 outcomes -

Revenues - 408 vs 375 cr, up 8 pc

GMs @ 46 vs 43 pc

EBITDA - 95 vs 75 cr, up 27 pc ( margins @ 23 vs 20 pc )

PAT - 70 vs 55 cr, up 25 pc

Sales breakup - Shunts : Bimetals @ 171:174 cr vs 157:166 cr

Export : Domestic sales mix @ 56:44

For 9Ms FY 26 - GM expansion led by cost controls, favourable product mix, better operating leverage. EBITDA margin expansion led by operating leverage

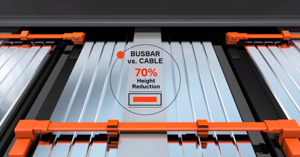

Board has approved to set up an automotive busbars and assembly facility near Pune. Should go live by Q1 FY 27. Capex required for this facility should be around 20 cr - to be funded via internal accruals

US business for both Shunts and Bimetals should see substantial improvement wef Q4 as the tariffs stand reduced. Seeing that play out in real time

Company already has orders in hand for BusBars. Company was already supplying these in smaller Qty. As the order build up is picking up, they r obliged to expand their capacities in Pune ( near OEMs )

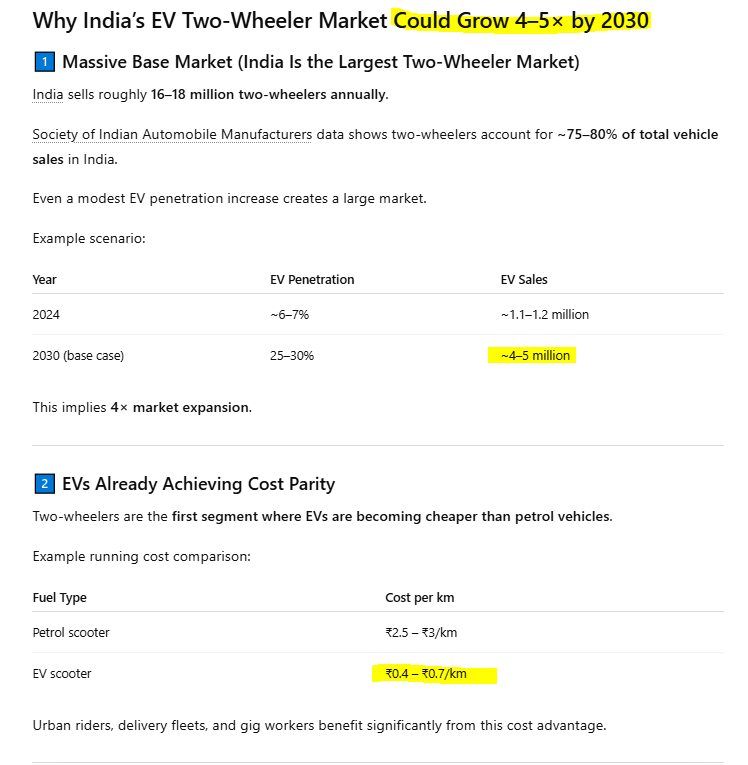

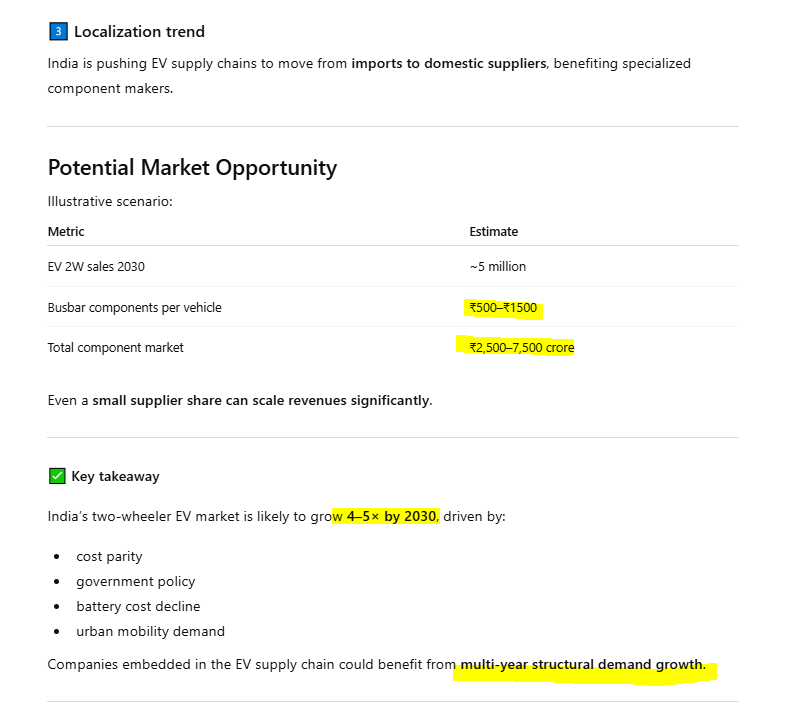

Should be able to clock 70 cr business in FY 27. By FY 29, this should ramp up to Rs 250-300 cr / yr kind of business

Making of BusBar assemblies requires EB welding ( just like shunt resistors ). Hence - it’s a natural extension for the company. At present, shall be making them for E-2W applications. Company is supplying to Bajaj and TVS e-2Ws. At present, no one else makes these BusBar assemblies in India. These BusBars should clock 14-15 pc kind of EBITDA margins

Value per BusBar assembly per vehicle should vary between Rs 1500 - 2500 / vehicle depending on the type of battery / electronics being used

Company’s supplies to Vishay Ltd ( in US ) are expected to be back to their peak levels ( last seen 2-3 yrs back ) - an added positive trigger

There are hardly any switchgear manufacturers in India who are not already company’s customer for Bimetals. Company now intends to gain mkt share in US

Also developing E-4W busbar assemblies in house. Once developed and accepted, can be a future growth engine

Busbar assembly made from EB welding process are inherently better than Busbars made from other techniques. EB welding is the most precise and efficient form of welding and doesn’t affect the flow of current even at the point of joint of 2 different materials

Looking to enter the Automotive Fuses space - used in Power window / Powered tailgates etc. These r high value fuses. The process of making these fuses also involves EB welding. Also looking at Automotive inductors ( used in ADAS, ECU systems )

Since the company already has the EB welding facilities, the incremental capex for the busbar assemblies is only @ 20 cr. This is just the assembly work ( after EB welding ). Hence, they ll be able to start supplies as soon as Apr 26

Topline growth in first 9Ms FY 26 has been @ 8-9 pc. Going forward, it should accelerate

Electrification of economy, demand from EVs, Data centres - all are tail winds for appliances / switchgears that use Shunts and Bimetals

Growth in Shunts business in FY 27 should be strong ie in mid to high teens ( on back of demand from Vishay, Denso and 2 more Japanese players )

Disc: hold a small tracking position, may add if company is able to deliver on its promises, not SEBI registered, not a buy/sell recommendation, posted only for educational purposes