With China facing a sluggish economy they may Phase out the EV Subsidies soon. Now the Component manufacturers will look for opportunities elsewhere or just dump it. This Might hamper Shivalik Margins.

US is also planning to Phase out EV Subsidies so demand for EV(Shivay) Components might be Hampered. Positive side, EV sales are skyrocketing and Higher Crude prices are another motivation.

3 Likes

Shivalik Bimetals AGM Questions Sep 2023

Thanks to Collated questions from @spatel @sahil_vi @Dev_S @Donald

Those attending the AGM, let’s try and get all these answers from Management. Hoping the standards set in AGM 2022 will be upheld, and looking forward to another great interaction today.

- Competition/Customers - ambiguity

In the Mumbai Analyst meet, we were informed that

-

Shivalik defined its addressable Market as EBW Automotive Shunts for EV BMS [non EV BMS shunts % is as low as 5% already]. Can you please elaborate on that/confirm for everyone’s understanding.

-

Shivalik saw itself as the 4th or 5th biggest player globally in EBW Automotive Shunts after Vishay, Hella, Continental. Also that Isabellen Huette was NOT a competitor [within that segment], as they are primarily in Shunt Resistors. Can you please again elaborate on the Competitive situation and inform us on specific competition players that we as shareholders could also track - to understand the Market/Industry/Supply Chain/Inventory situation much better.

[IsHu supplies to Merc] -

Need some clarification here. We understand that both Hella and Continental are Tier1 BMS Suppliers to OEMs and both are Shivalik Customers (NOT competitors). Who are the other big Tier1 BMS suppliers to OEMs - Marquardt, Bosch, and Rohm?

-

If that is correct, then after Vishay who are the other Top EBW Shunts suppliers/Tier2 suppliers, and thus effective competitors for Shivalik.

- Global Markets 2022 vs 2023 (Total EV 13.8 Mn in 2022) and Shivalik Positioning

ngths- China accounted for 60% of all new EV registrations in 2023. Now? Is this an addressable market for Shivalik? Some addressal must be happening through Vishay? Is it like 10% ?

-

EU accounted for the next big chunk of 25% of global EV Sales. Early 2023 EV Sales growth of 30%? Has this remain unchanged? Fit for 55 package impetus? Shivalik business model/partners for EU Market?

-

US accounts for 10%? Cumulative post-IRA(Inflation Reduction Act) investments of USD 52 billion in North American EV supply chains, of which 50% is for battery manufacturing, and about 20% each for battery components and EV manufacturing? New Plants will be coming online in 2024. Is it a fair assessment that Shivalik is very well placed here strategically because of Vishay relationship/New capex in New Mexico

- Domestic Customers and Market Update

- Proportion of EBW Shunts sales to 4W/2W and 3W domestically

- Update on Mahindra XUV EV platform (co-design) - where are we, what is the scale visibility we have here?

- Tata Platforms -any co-designs or all built to customer specs? Visibility?

- 2W - how do we see this market scaling? What kind of timeframes are we talking about?

- Inventory/Destocking/Lead Times

-A year back Competition supply lead time ~50 weeks; Shivalik <20 weeks.

Has anything changed here? Why, or why not? Please elaborate

-We have seen volumes tapering off progressively quarter on quarter on Shunt strips?

- Acquisition Prospects/Fund Raising Needs

Shunt and Disconnect Relay both have an important role in smart-meter. Are we seeing integrated Relay-with-Shunt gaining traction in the market? If yes, is Shivalik exploring an option to acquire, build or partner with Disconnect Relay product co and enhance it with its own shunts? Something like Johnson Electric ZRP. Basically, to increase our wallet share in the real boom of smart-meter.

Source: https://www.youtube.com/watch?v=7j_QQAXWmIA

- Market Outlook

China and the EU are seeing a jolting drop in EV sales in 2023 (from EV touching 50% market share to now 15-25%). Consumer enthusiasm for EV is dampened as subsidies are reduced or set to disappear. The road ahead for the EV portion of our shunt business segment looks bumpy just in the near future or a bit longer?

Automakers across the globe have announced huge investments in EV and a relatively rapid transition to an all-electric fleet. Could you throw light on our cumulative Design-ins or Design-wins that could result in sizable sales in years to come?

How does the Opportunity Pipeline look today compared to a year ago? For the Shunt and Bi-metal/tripmetal business segment.

“The third and fourth quarter for us should be much stronger than what it has been in this quarter” was said in Q1FY24 concall. Any new encouraging/ discouraging development or the statement still holds true? Is this statement based on smart-meter deployment push in India and/or based on shunt exports order book visibility?

-

Raw Material - Margins stability: Is it correct to say that in the Vishay relationship, Shivalik is insulated from RM sourcing volatility thereby providing predictable and sustainable margins. A fantastic business relationship and long-term secured relationship

-

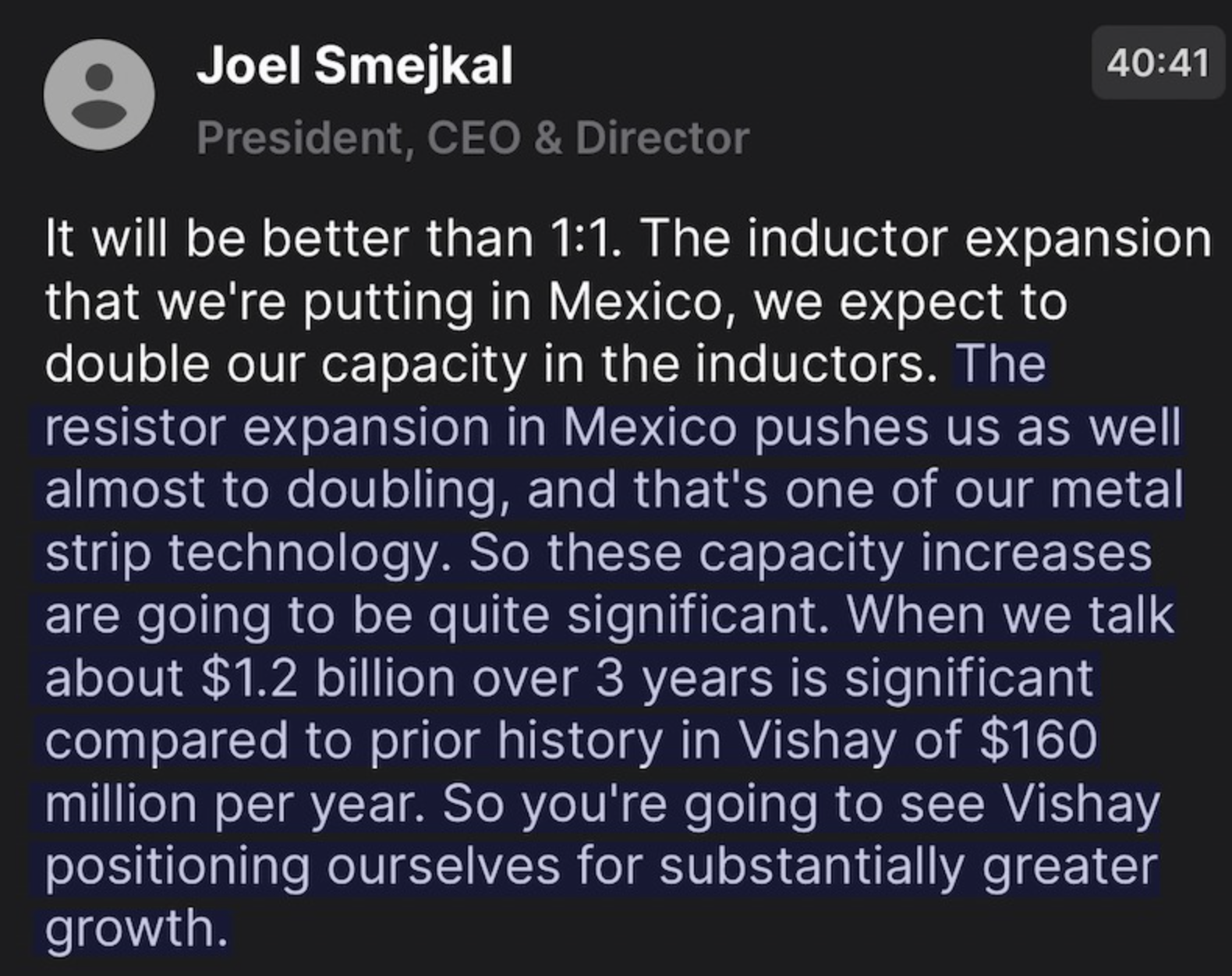

Vishay has new CEO Joel Smejkal starting early 2023. A Power Metal Strip (Shunt Resistor) specialist with many patents in this area Google Patents. Joel has been an old timer at Vishay. How has Shivalik’s relationship with Joel evolved over the years? Any change after wearing the CEO hat?

- In Vishay Q4 '22 concall, Joel new CEO talks about capacity expansion in their Power Metal Strip business segment. Any revised expectations by Vishay from us to support this growth, from capacity and/or capabilities expansion perspective?

-

Could you share new customer contributions in FY 23 and Fy 24 in exports for shunt and bimetal - how should this trajectory play out over 1-2 years?

-

How is the global supply situation when it comes to shunt resistors? EV subsidies going away/reducing in many geographies - would this have a further setback on demand for the short term? Can bimetal compensate for any temp demand setback on global demand front for us?

-

Quarterly communications by our top client vishay talks about inventory position of their customers normalizing (inventory destocking) in post covid world. Do we have any visibility from Vishay & other clients on when we expect inventory destocking to end in the value chain & for normalized sales momentum of 20-25% growth to pick up?

-

Smart meter opportunities have been around for > 15 years now with lots of back & forth over floating & cancellation of tenders. What has changed now & why is it a large opportunity that will result in real cashflows? Genus power now has 8300 cr orderbook. Genus sources 60-65% of components locally. Since genus is largest player in industry, taking Genus as industry benchmark, what percentage of Relays going into smart meter orders which are being executed currently are being sourced locally versus imported into country?

-

What is our current market share in the relays which go into smart meters ? OEMs like schneider electric are investing 3200 cr capex including significant investment over next 3-4 years for smart meters. Are we already working with all smart meter & relays OEMs & what is the strength & longevity of these partnerships? By when can we expect significant indigenization for our components (contacts, shunts) in the country? What are the drivers for it? Are we cost competitive in smart meter shunts & contacts or would indigenisation be driven primarily by government policy requirements?

-

We have talked about both Tata & Mahindra being our customers in the EV BMS space. Currently what % of the EV BMS shunts being used in their EV are imported and what % are manufactured by us? If large commercial volumes have not yet started, when can we expect them to start?

-

We have seen supply to US in terms of shipments/ per shipment qty in recent times normalising - is this new normal with annual growth aligned to industry growth at single digits or we have levers to grow faster - at least high teens? Is there a strategy to counter this global demand context via inorganic route/ product or category expansion?

43 Likes

Shivalik AGM Highlights ( v high level for now )

Understanding of Shivalik Edge (right to win) is deeper this year. Conviction has soared with more granular grip on how/why Competitive Position has got stronger.

Tier 1 approval /coverage for all OEMs is now complete consequently new business/platform share will keep going incrementally higher (even where presence is marginal today).

Competition Mapping by us is now complete. Isa Huette (not expanding), Vishay (expanding big but wedded to Shivalik’s Bimetal edge unreplicable by them) Wieland ( otherwise big but in its infancy in EBW 1 mc), Syntec, Taiwan (was a customer before expanding from 1 EBW), Smart, Korea (similar scale), 2 in China (probably servicing Chinese market, not seen so far in non China)

PS: will try to update details later tonight or tomorrow. On brief vacay from 28th

And as technology demands become more stringent (1% Specs error tolerance set by OEMS shifted now to 0.05% tolerance specific to EV BMS) competition unable to match up will have to fall back to source from Shivalik!

Big Smart Meter calculations shoring up near term slowdown should be discounted (totally is my feel). Supplier infra is nowhere ready. 25 Cr meters might take decade(s) to implement. Currently only about 10% is tendered - even that will be hard to fill. Component makers are slowly adding capacity.

Tempering down near term expectations is a good idea, though Mgmt confirmed that current destocking should normalise by Jan 2024

41 Likes

I met Shivalik in Electronica India last week in Bangalore. Spoke to Kanav and also a sales manager. Please ignore if some of it is basic:

Bimetals – risk of technology – yes, we are also hearing about electronic relay which will give better control and efficiency – for example – in bimetal, if the MCB is tripped, you will have to switch it on manually but in case of electrical relay technology, you can control it or set logic for it. Electronic relays are expensive, so the transition will take a long time. Even otherwise, high volume products will continue to use bimetallic relays.

EBW Resistor – no one can make these in India – one electron beam welding machine can cost 15 to 20 crs, we initially bought 1 each from different OEMs - UK, Europe and US. We have some 10 EBW Mcs now. The last few we made it in-house with base components. You just cant buy a machine and start making shunt resistors. It will take 10 years for a new competitor to get to the scale where we are. If not, anyone would be making it now.

Almost all PCBs which measure/convert/switch current will have standalone shunt resistor mounted on the PCB. Based on application, the value of resistor can vary from 10 Rs to few 100s. Most EMS players buy resistors from us.

Permanent Magnets – very long and good relationship – I am their account manager - the resistors we sell to them start from 10 Rs to 90 Rs – they will not get into what we are doing, we will not get into what they are doing – we are good in EBM which we acquired through our legacy business – they are good in magnetics.

Vishay – they make their own resistors but also buy from us. They will not put up capacity in India unless they see enough volumes. India is small for them. They would rather buy from us as shunt is a not a standard product. It has to be customised for application. More than 50% of our capacity is customised for specific clients.

Reason for guidance of 1600 Crs topline – immediate 12 months, we get framework agreements from clients so that we can buy raw material but companies also give projections for next 2 – 3 years. So our guidance is based on inputs from clients.

All global players are sitting on inventory and hence ordering has slowed down. We expect things to normalise only towards middle of next year April onwards. (Many casting and forging players also said in AGM that inventory will normalise only from January 2024)

Growth will be low for FY24. But FY25 and FY26 will be good.

Smart Meter – shunt might cost Rs. 50- 100 and silver contact might cost Rs. 50 to 100. So overall Rs. 150 per meter. If 2 Cr meters will be installed every year, it gives us 300 Cr revenue opportunity. We will be supplying to players who make the relays like Gruner. No one makes all the components needed for a smart meter in India. Most of it is being imported by Genus and others currently. Some components like chip, India doesn’t have the capabilities. Govt mandate to make everything in India in few years. They have given timeline. While orders have been received by the likes of Genus, we think the delivery will take at least 12-18 months (the manager wasn’t very bullish for the short term) as we are still in prototype stage. Ecosystem is not ready. But big opportunity once it starts.

No one makes the copper grade we need in India. So we import almost all of our copper.

Kanav had to catch a flight and I had to leave too. I couldn’t ask abt EV applications. Will try talking to the Key Account Manager for PML.

65 Likes

I work in Automotive. During work from home we need systems to be triggered remotely.

e.g Ignition Key or any other power key . We use USB based Relays which cost Rs

500-2000.

Cheaper one last less. demand for Relays are Increasing. Most of them are imported from China or US. Manufacturing of Relays in India being setup.

will find and put up more data and application areas in this field later.

Relays are used to protect the electrical system and to minimize the damage to the equipment connected in the system due to over currents/voltages. The relay is used for the purpose of protection of the equipment connected with it.

These are used to control the high voltage circuit with low voltage signal in applications audio amplifiers and some types of modems.

These are used to control a high current circuit by a low current signal in the applications like starter solenoid in automobile. These can detect and isolate the faults that occurred in power transmission and distribution system. Typical application areas of the relays include

- Lighting control systems

- Telecommunication

- Industrial process controllers

- Traffic control

- Motor drives control

- Protection systems of electrical power system

- Computer interfaces

- Automotive

- Home appliances

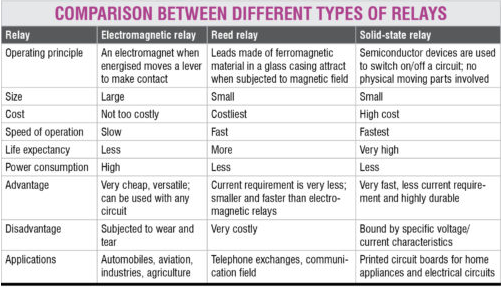

What is Relay? How a Relay Works? Types of Relays, Testing, Applications

8 Likes

Shivalik Bimetal AGM 2023 26 Sep

(2nd Order details added - compiled on flight - will refine tomorrow and add 3rd order details from Notes. Please excuse typos)

2023-24 OUTLOOK

Will be little slow. Post the semiconductor shortage, everyone stocked up like crazy extrapolating. This was seen at Customer end, Distributor end, and even at our end.

This is not specific to our industry, but a phenomena seen across industries. Ours has NOT been that severe. New Orders have started coming in, and destocking will end soon, normalised levels could start by Jan 2024

2025-26 outlook is more exciting!

EATON CORP AWARD

out of 12000 vendors globally, shortlisted 10.

6 were given Higher Excellence Awards

SBCL only Indian vendor among the 6

Has led to higher visibility globally, but more importantly within Eaton Corp entities - many didn’t even know SBCL makes shunts

EBW BMS Shunts

60% of all Automotive

Competitive Positioning is almost unchallengeable (my words)

Lot of changes are coming. We can see where it is moving (e.g. 1% error at shunt level specs will move to 0.05% error tolerance OEM specs for shunts). It’s NOT measurable by the OEMs but they want proof to be shown by vendors like Shivalik that they are able to move there. Done.!!

Quality of test jigs, strip bimetal/EBW quality (acknowledged by Vishay as better than theirs), 100 % process automation for 15 pre-EBW, 15 post-EBW processes, when coupled with 100% test sampling data - goes a long way in reaching there. Zero PPM defects is the new goal!!

Lot of competition will drop out. Already instances of competitors becoming customers for newer products happening. Especially heartening is a German instance !!

At all Auto OEMs Shivalik Shunts and Strips are now approved with their Tier1s(Bosch, Hella, Continental, others) directly or via embedded Tier2s like Vishay. Some Tier1 relationships are at advanced stages (after 5-6 years of engagement). New Competition will take at least as many years. Many are at initial stages of engagement. BYD engagement has moved from Development customer to Commercial!

MARGINS SUSTAINABILITY

Business model allows complete pass-through now

a) manufacturing margins are always protected

b) metal price index volatility is calculated separately - and is also passed on to customer

c) however Tier1s negotiate hard on productivity/scale benefits - which is a challenge we have to face - so far it’s been win win

d) 2-3% additional margins available for customers where SBCL also provides value engineering services - takes original design and suggests improvements

e) some customers ask us to source RM - only from say Hitachi (don’t care what price) that works better for SBCL

f) metal price varies from 6-7% of shunt costs to 50% for some of the heavy/ bulky products

OTHER EV (non BMS Shunts)

Much more competitive space

a) Off the shelf - more SKUs to be maintained

b) Customisation Shunts - all process optimisations are finished; more in control now

REALISATIONS

Fy23 Shunts volumes grew by only 3%, but top line moved by 23%, so realisations have moved up by 20%? Led by ??

- Product Mix changes

CURRENT SENSING MODULES Dev Status

Lot of changes happening in requirements/designs. This is still under evaluation. Strong possibility of joining hands with a Customer

5G UPDATE

Europe 5G rollouts had stopped. Now they have restarted. India - some Telco roll out design includes us, some don’t

RIL 5G rollout SBCL will play a role

SLOWDOWN - blessing in disguise

Good use of slowdown times this year

Valuable time and space for v important stuff that keeps us ahead in the game

a) Process Automation

taken to another level. Batch level random sampling is now replaced by 100% sampling data. So huge granular data available to analyse Error for Performance variations and identification of root cause for particular batch/sample (minute wise variations) is thus hugely more granular (unlike earlier random sample data where guesswork and trials sufficed)

b) New Innovation

3 layer adjacent Magnetic-Non-Magnetic-Magnetic Metal Strip for stabilising Camera in Smartphones. Moved to bulk trials. Exciting development certainly, but will take 5-6 years for Commercial (Japanese customer)

RAINS/FLOODS

Solan is on rocky terrain (not soft). Roads were vulnerable due to design issues, wrong road cutting issues. Even during the worst flooding/landslides situation road transportation did NOT see a single day of disruption. This NH5 is an important Defence Road - has to be kept clear at all times.

VISIBILITY

-3x Sales in 2-3 years targets - 50% is visible today

LEAD TIMES

Competitors 52 weeks, SBCL <20 weeks for complex products, normal 4-8 weeks - stays unchanged. Even before EBW process there are 14-15 processes (all competencies in-house for SBCL as opposed to many outsourced for competitors.and 14-15 post-EBW processes

SBCL commands even shorter lead times from its supply chain vendors

(to be continued)

63 Likes

This is most likely pointing towards Permanent Magnet ?

Frankly no idea.

Knowing them my sense though is, it would probably be one of their bigger global scale Tier1 or Tier2 partner

3 Likes

Thanks @Donald for putting together such a detailed notes of AGM. Just need one clarification on following:

VISIBILITY

-3x Sales in 2-3 years targets - 50% is visible today

Does this mean that company is targeting for 3 x of the current revenue in next 2-3 years. Is it only for Shunts division or overall?

Shivalik Bimetal AGM 26 September 2023 at Solan, HP

FY23, volume growth in Shut and Bimetal was in lower single digit. However, improved product mix assisted the company to improve realization and relatively higher growth in revenue and stable net profits. Generally, higher thickness materialize would result in relatively higher volume of sales as compared with lower thickness material. However, Value addition and margin in generally superior in lower thickness products as compared with Higher thickness product. This was main reason for higher sales value and profit growth, despite muted volume growth in FY23,

Q1FY24 was demand was adversely impacted due to Destocking. The COVID related uncertainties resulted in overstocking of goods across the channels, from the company to distributors to end customers. This was particularly true for US/EU market. The management expect same to be normalize as indicated by receipt of new orders. During last 6-9 months, slowdown in demand given necessary free time to company to focus on process improvement and new product development. While working on many initiatives, the company developed carrier of mobile phone camera. This carrier is expected to reduce the vibration while taking phots and may work as superior quality as compared with current technology usage. The product still under development and experimentation with the potential customer.

The company pro-actively, expecting good demand from Domestic and export market, invested in building up new capacity and process optimization. Advance Meter Infrastructure (AMI-Smart meter orders) for power sector provided very good and large opportunity to the company. The company is confident about its ability to supply required volume to customers (Smart Meter Manufacturer). However, given that scope of work involved, manufacturing, installation and service of smart meter for next 8 years (2 years’ time for manufacturing and installation), it would practically very difficult to implementation on scale of 25 Cr meters as reported in Media/Industry sources. Despite all optimism, considering the on-ground situation, only 2.5 Cr order under AMI are tendered. Hence, company expect expected timeline to install 25 Cr Smart meter higher than expectation from regulators. Given the current interactions with customers in export market and development in domestic market, the management is optimistic for demand growth in FY2025.

Major customers interactions give good visibility of business long term. At least 50% of increased capacity is likely to be utilized based on current interactions in medium to long term (5-7 years). Shunt share is likely to increase 65-70% while Bimetal would be remaining. The company likely to use Bimetal inhouse to manufacture Shunt/ other new products developed which would have superior margins.

Process improvement with support of AI and machine learning:

The company has implemented Fully automatic optical inspection to check surface imperfection. It has also installed resistance inspection machine. Further, it uses now online system in Automatic rolling mills which continuously monitor input and output width. As against previous approach of sample-based inspection, now the company has data about all products manufactured real time and analyses data with machine learning and use learning in developing logic for various production process. This process is continuous and assist substantial improvement in quality and process optimization.

Unit IV (Plant 2) Manufacturing unit in installed with Cold Bonding mills, Automatic thickness control and gauging tolerance of production. Reversible Cold Rolling Machine Control (ABS) is also installed. Data collection mechanism, which check batchwise performance.

Geographical diversification of production facility: Despite heavy rain in HP, the company did not even have logistic issue for a single day. Solan region has relatively strong rock. Hence, the company does not intend to diversify manufacturing to new location.

Capital allocation and Dividend payout:

Since the future capex requirement for growth are not very high as per current situation, with growth in sales and net profit, the company would look utilize excess free cashflow at increasing dividend payout/buyback in medium to long term.

The company has incurred the majority of capex to meet capacity for next 5-7 years. Going forward expect nominal maintenance capex and debottlenecking. It expects capacity (or volume) to increase over 17-18% CAGR over 7-8 years.

Lead time:

Shivalik continue to enjoy lowest lead time to manufacture product to meet customer demand. Captive manufacturing expertise, process equipment understanding, long experience of production team and relatively small supply chain results in the best lead time for Shivalik, even when compared with Global peers.

Competitive land-scape:

EBW, There are couple of players in China, one in Taiwan (name Sen tech, may be linked company but not sure, https://www.sen-tech.com/). Currently, Chinese players are not supplying in global market. Further, the EU/US players also have reservation to source supply from China. New player like Wieland in Germany has just one machine installed while Shivalik will soon get its 8th machine installed. Wieland and Sentech were customer of Shivalik for certain materials. Sentech has one machine which is also not using of continuous beam welding. The manufacturing by Sentech is mainly for captive consumption and very limited is available for outside sale.

Vishay has acknowledged that material supplied by Shivalik is superior in quality compared with their inhouse supply. Given the wide range of product, ability to provide customize product to meet requirement of customer, lower lead time and constant innovation and improvement in cost competitiveness (improving product quality and process optimization) Shivalik Bimetal is well placed in global markets for Bimetal as well as Shunts.

Further, Customer of Shivalik, majority of which are very well known large MNCs, consider Shivalik as PARTNER and Not VENDOR. One of Japanese company (not sure), honored Shivalik as one of six excellent vendors (selected from 12,000 global vendors). Other 5 vendors were EU/US companies.

While company is sole vendor to many of its customers, still prices are negotiated and also productivity gain discount is offered.

Contact business

While contact business has relatively lower margin, the scale of opportunity is huge. Shivalik understand same and intend to replicate model Similar to Shivalik Bimetal in high margin/unique value-added products even in contact business. As compared with normal margin of 8-10%, Shivalik Subsidiary intend to achieve 15% margin on large scale. While it might lower than parent, but still would give scale and better operating leverage/ROCE to consolidated level.

The company expect better prospects for Contact business from US. Previously, JV partner was from US and hence JV was not supplying to US market. With JV partner out, the company is now confident to get more demand from large US market.

End-use application/sectors:

Shunts-55-60% Automobile, 25-30% Smart Meter, 8-10% Miscellaneous

Bimetal: 70% Switchgear, 15-20% Automobile, 8-10% Miscellaneous

PLI Scheme:

Shivalik was looking to incur capex to meet expected growth in future demand. However, during the time, coincidently, second list of products eligible for PLI announced by GOI has products which are likely to be manufacture from new capacity. Shivalik has already been approved in first stage by the Private party appointed by GOI as approver for PLI scheme. In order to get benefit of PLI, further stages are need to completed and Shivalik in process to complete all stages approval.

Managing Transformation:

Shivalik was small company started its operation in Mid-eighties. It took almost 40 years to reach from nil turnover to 400 Cr. Now for Next level of growth say, revenue milestone Rs 2,000 cr, second phase of journey, management realize that they need to take support from External professionals, develop team of excellent managers, and continue to evaluating gap in capabilities. The gap once identified are filled with inhouse talent with training support or engage outside professional/consultant.

Research and innovation:

Given the innovative approach and product development knowledge involved in production process and increased involvement on non-promoter family members in research, the company is looking at protecting its IP by way of patent. They have full time R&D time now and developing R&D Patent Kit (like collecting Trial data, putting it in proper arrangement and give end results to experiments).

IP protection is getting categorized in three broad areas, Manual, process and equipment. Each category is getting properly organized to get patents on knowledge.

Disclosure: Shivalik Bimetal is my second largest holding. My view may be positively biased due to holding. I am not SEBI registered advisor. I am not recommending any investment action. I may buy/sell above mentioned stocks without informing forum. There might be communication gap from my side due to my limited understanding of business. Investor shall do their own due diligence before making any investment decision.

55 Likes

It is for Consolidated entity in my understanding. My understanding may be wrong.

3 Likes

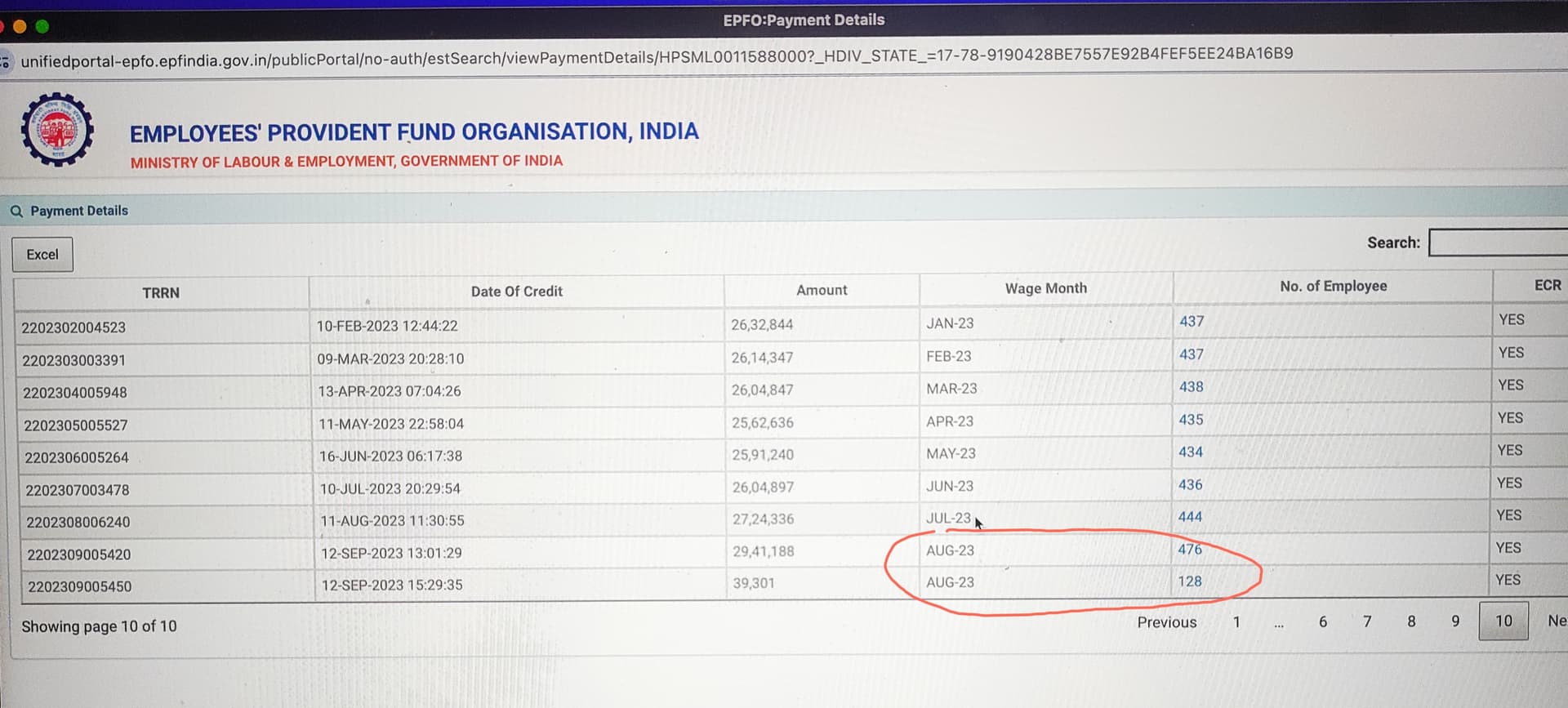

The EPFO data for Aug looks interesting. Big change in employee figures. Correlates to the new plant that got operational in Solan.

25 Likes

Hi Vivek, could you please share the path to access this data?

Thanks

4 Likes

Sir, Could you please tell me how do we find information like this - how exactly do you know where they bought the furnace from? I am new to the world of investing - so trying to figure out how people are able to come up with such granular infromation on micro and small caps

2 Likes

Fresh Edits Oct 7 SBCL AGM 2023 (from my scrambled Notes)

Why/How SBCL will stay ahead of Competition?

PRODUCT MIX (examples)

SHUNTS MIX

- Wider shunts - typically 6000 Kg/shift volumes - drives Topline

- Narrow Shunts - thinner - typically 100 Kg/shift - drives more of the bottomline

We are always moving towards more value-added

BIMETALS MIX

- earlier we were doing 100 % strips (no components/value-adds)

- now 70% value-added; 30% is bare strips

- Bimetal strips can command in a range of 2000-6000-10000 Rs/Kg depending on application requirements

BIMETALS INDUSTRY CONSOLIDATION

Few players. Manufacturing is migrating more and more to low cost destination countries like India. Good size of the global bimetals market is addressable by SBCL, so can SBCL start commanding higher margins?

Don’t forget 95% of our bimetal customers (mainly Switchgear) are mature global customers. Someone like a Schneider will dictate prices; SBCL may be sole vendor to majority of such customers but we have to be price takers. With higher volume off-takes, we are challenged with productivity discounts every year.

SBBCL (EARLIER JV CONVERTED NOW TO 100% SUBSIDIARY

On why it was NOT scaled up earlier

The partners were conservative. Now we are free and we will expand. The new plant is coming up. The biggest opportunity lies in the US market - which is addressable to us now (earlier barred). There are of course lot of other competitors. It will be lower margins than our primary shunts/bimetals segments but with higher asset turns, AND we would like to target as our addressable market ONLY where we can maintain 15% kind of Operating margins, so we should do reasonably well there.

CHINESE COMPANY BATTERY/BMS/SHUNTS ENTERING EU (specifically BYD)

Already supplying. Commercial Supplies to BYD have started for their China requirements !!

(this cannot be tom-tom-ed, for obvious reasons)

PATENTS (ring-fencIng people/knowhow risks crossing over, with Competition trying to enter)

They have at least 3 patentable process/products!

Mgmt acknowledged currently this is an issue and will now be addressed with the setting up of a dedicated R&D cell with folks accountable for outcomes. There is someone who will take these forward and make sure to chase down all requirements/documentation getting filed properly; sometimes these can be very cumbersome and take up to 6 months of consistent follow-ups.

CAPACITY UTILISATION

18-20% kind of annual increase in utilisation is foreseen from existing.

Of course more automated lines for EBW and SMDs will be put up based on order flows

FREE CASH FLOW

On a leading question from an analyst that SBCL is on course to generate 600-800 Cr of Free Cash Flows over next 6-7 years, Management did confirm they have done majority of Capex and are confident of maintaining margins, so yes they are on course for that barring any major geo-political fall outs. Details here

DIVIDENDS

On being asked if therefore they will be looking to return more to shareholders Mgmt confirmed the intent and a dividend policy is likely on the anvil for the Board to consider

23 Likes

Sorry for the late replies (was travelling)

a) of 1600 Cr forecast - 55-60-65% will be from Shunts (thats the visibility today, depending on who in Mgmt was asked the question)

b) they continue to maintain a 25% CAGR in Overall Sales visibility, so doubling within 3 years, you can check some feasible projections here). Goes without saying that they have mentioned FY24 will be slow (destocking related and that normalised levels should/could return by Jan 2024, as new orders have started coming in. FY25 and FY26 probably will see good growth returning (Shunts) as newer models will start getting launched from FY25. That is the time new relationships like Continental and Hella will start kicking in with meaningful numbers?

c) my sense is this is NOT including any sudden explosion in EV happening within the next 3 years

30 Likes

Just wondering…as the company has fair bit of exposure to US markets, and few economists already anticipating a recession in US mid next year, how this is going to impact SBCL’s growth/projections?

Not sure how to interpret this since ASIL certifications are primarily required in EU region. Positive side is since Shivalik posses this “.05%” accuracy it can eat away pie from Isaballe Hutte if they can’t meet the mark.

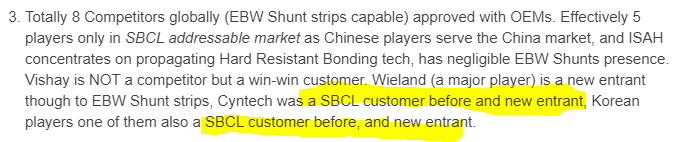

Does this mean Shivalik has overcapacity ? eye opener is China world’s largest EV market ,Who is vendor for their need ? with 2 companies and how mancy EBW Guns ?

Is this the reason behind expansions by Shivalik, readying for the action ? Production lines are getting ready with below evidence

Will Customer becoming competitor impact margins ? or will it be offset by below one

Disclaimer: Invested and Biased.

Views are personal and might be wrong

8 Likes

I had also gone to the AGM this year and it was a wonderful interaction and experience. Having been invested in the company for 5-6 years now it’s a great satisfaction to see how a company has evolved and grown so much and it’s great to interact with management people and see the evolution, leadership and excitement for journey ahead.

Wonderful summaries have already been posted before so I’ll not repeat.

Few takeaways for me were:

- The pictures/sneak peak into the machines and advancements over the years was the most important thing. The machines looked sophisticated and there seemed to have been lot of automation done to have precision and lead. Probably this is the key reason why company could grow even in bimetal segment so rapidly.

- It was good to see the next generation of the management ready, deeply involved and excited for future.

- Strong direct relationships with several leading global OEMs. It seems in many of the cases the co is the sole/customized supplier and is able to offer value addition new solutions.

- Possibilities of new product developments and moving up the value chain.

Overall, it’s impressive what the company has delivered over last 5 years. With such a foundation and tailwind, if they are able to repeat on what they have done, there is opportunity here.

Ayush

Disc : invested in family and client acs. Have done some profit booking over the last few months to protect gains and plant new ideas

60 Likes