Important to see price of Right issue!!! Market is sluggish and good time to invest through Right issue route!!!

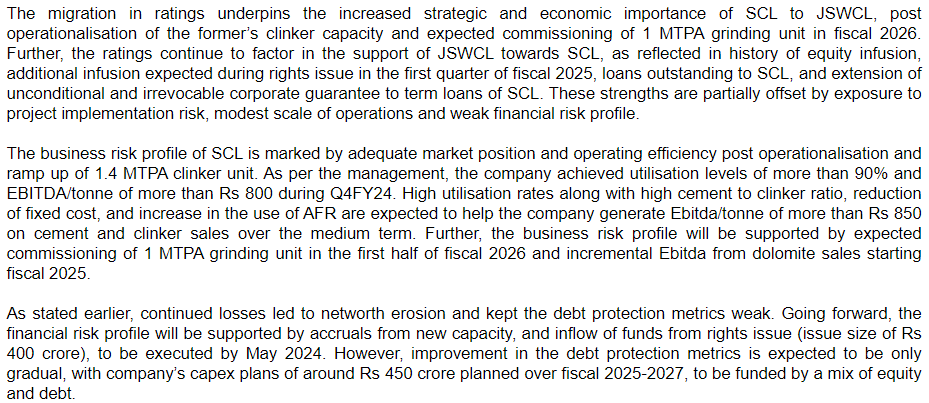

Q4 results + Rating upgrade

Is there any information regarding mngmt plans for reduction of debt?

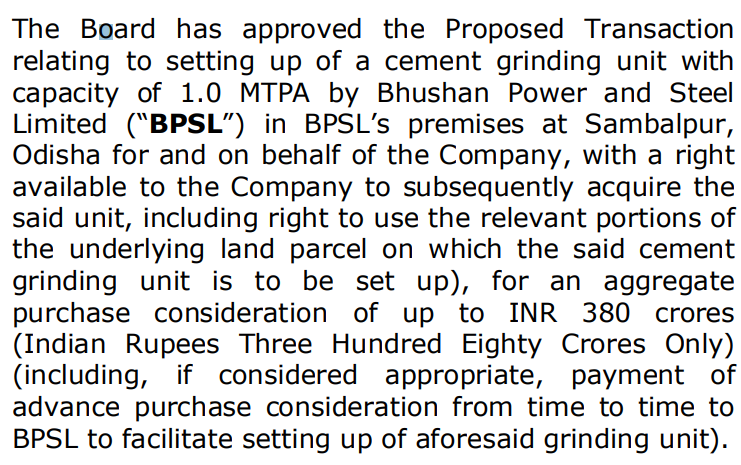

Right Issue of Rs 400 Crores and objective of the issue

Repayment of Debt: RS 345 Cr

GCP: Rs 55 Cr

2 Likes

Turnaround potential Cement pack after 2 Years

- JSW Cement is the parent company and currently company is producing Clinker and sale to JSW Cement. EBITDA ~ 800 MT (Which can be ~ 850 MT)

- In first half of FY26, grinding unit at 1MT will be operationalize.

- Waste Heat recovery plant @ 9 MW

- Crushing plant of Dolomite and Limestone @ 4 MT

- Railway siding inside and outside plant @ 12 KM

- OLBC: transport LS from mines to the plant @ 8 KM

all are coming FY26 and FY27.

Another part to watch carefully,News of JSW Cement IPO!!!

1 Like

So the full year EBITDA potential from clinker at current quarter capacity utilisation (90%) at the rate of 850 Rs is 107 Cr. only.

And after paying 345 cr debt they still have to pay almost 75-80 cr of interest. At full swing operations also the company will make losses on standalone clinker business unless they fully pay the debt. I dont have much info about other products. Please share your thoughts on other business potential of the company.

Disc: having tracking quantity

Near to agree on your calculation!!! and current set up

What we are looking FY26 and FY 27, which I was mentioned from point 2 to 6 and other aspects to retire parent company loan!!!

Credit rating report on Shiva.pdf (415.8 KB)

1 Like

Using some basic math here:

- Co has already done 144 Cr in Q4 FY24 & OPM of 24 Cr

- Current debt on the books is 1423 Cr & on this int cost declared is 101 Crs. If no further debt taken int cost proportionately should come down to 74 Cr.

- If it is able to maintain the Q4 rev & OPM run rate, then for FY25 rev should be 576 Cr & OPM of 96 Crs.

2 Likes

OP level pe to sahi hai. Net profit kitna karegi ye sawal hai. After deducting interest cost (74 cr) and depreciation (30-40 cr) what will left? Market is giving 1250 cr valuation to a company which is making losses and will make losses in the near future also.

If you have information regarding other revenue stream like upcoming new products and how much will it generate revenue and profits then kindly share

There is NO Material change on Business specially in FY25 & H1 FY26 or considered full year!! This is not the case of SHIVA; this is pure contrarian call based on Management and future development on point from 2 to 6!!!

This is Chicken and Egg story and after Right Issue and H1 FY25 result, more clarity is coming.

1 Like

28fbe18d-5981-4e38-859d-a2c2dbd37c3f.pdf (384.1 KB)

Allotment of Right Shares and Increase of Share Capital