Shiv Texchem

- Shiv Texchem is engaged in the business of import and distribution of hydrocarbon-based chemicals.

- No manufacturing, no further processing. Just import and distribution.

- Products include Acetyls, Alcohol, Aromatics, Nitriles, Monomers, Glycols Phenolic, Ketones, and Isocyanates, are critical raw materials and inputs and have applications across a wide spectrum of industries like paints and coatings, printing inks, agro-chemical products, specialty polymers, pharmaceuticals products and specialty industrial chemicals.

- The company is engaged in secondary and tertiary derivatives of bulk chemicals which are in turn used as raw material for different industries.

- Sourcing from multiple countries that include China, Taiwan, South Korea, Kuwait, Qatar, USA, Netherlands, Belgium, Italy etc

- Also provides storage solution, with storage and handling agreements at Kandla, Mundra, JNPT, Mumbai, and Hazira ports

- Have worked for multiple large corporations such as Gujarat Flourochem, Apcotex, Reliance etc.

The Business and Strategy

- The company is primarily an importer and distributor of chemicals for domestic manufacturing companies

- The rationale- Most of the petrochem manufactured in India is for fuel-based applications. Hence supplying and handling procurement needs for manufacturers’ petrochem imports.

- The company is trying to leverage its offerings as an import-handling arm for the petrochem needs of customers.

- This is backed by their domain expertise, relationships, and supply chain solutions.

- Capabilities to store both critical as well as bulk chemicals.

- Currently, the customs duties on these products are approximately 7.5%—complete pass-through to customers.

- Highly diversified business - Top customer contributed to 4.5% of the topline in FY 24, Top 10 - 16.43%

Top Supplier - 57.76% of purchases for FY24, Top 10% - 19.29%

- In an interview, when asked about concentration on geographies and sectors, management responded that it depends on the business needs. When a particular sector does well or a certain chemical from a supplier concentration shifts.

- Order backed Inventory (~70%) along with no product accounting for more than 10-15% reduces concentration risk. (-Credit Rating)

Industry

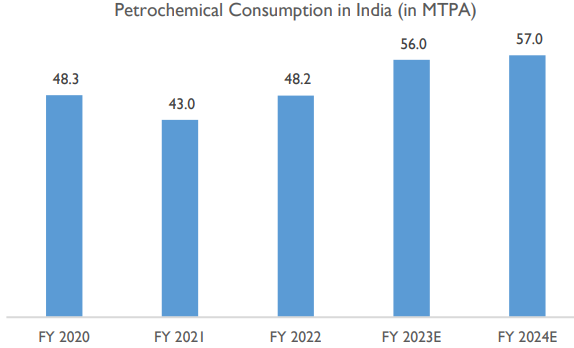

Petrochem consumption is estimated to be around 61 MTPA in 2025 and reach 80 MTPA by 2030.

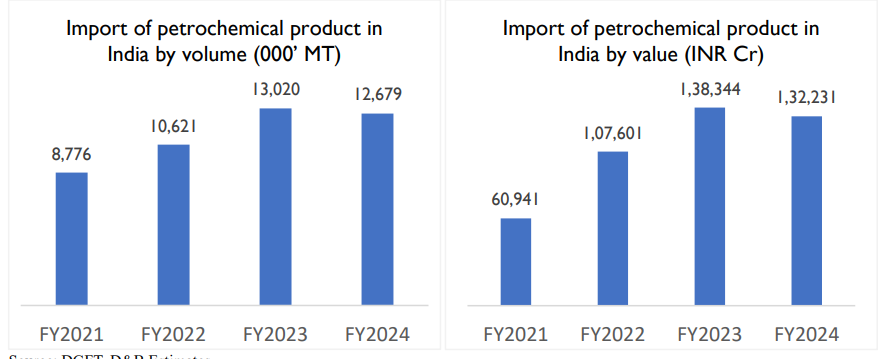

Major consumers of petrochem products include dyes, inks, Paints, AGrochem, Pharma, consumer etc. Tailwinds in these sectors directly impact petrochem consumption and imports.

Management

Mr.ShyamSundar Chokhani, Mechanical Engineer from IIT Bombay, started the business 19 years ago, where he supplied caustic soda from Aditya Birla Group to local manufacturers and distributors.

Hemanshu Chokhani, son of Mr.Shyamsundar Chokhani, is a rank holder CA, IIM Ahmedabad graduate, brings 14 years of experience, is the CFO.

Vikas Pavankumar (Hemanshu’s Friend) obtained a bachelor’s degree in Industrial Engineering from Purdue University and completed his graduation programme in Management from ISB, is the MD. 14 years of Exp.

Girdhari Lal Kundalwal is an independent director, who is also a director at Ganesh Benzoplast.

| FY 22 | FY 23 | FY 24 | Jun 24 | |

|---|---|---|---|---|

| Sales | 858.65 | 1117.59 | 1534.9 | 566.04 |

| COGS | 803.42 | 1033.65 | 1397.85 | 523.89 |

| GPM% | 6.43% | 7.51% | 8.93% | 7.45% |

| EBE | 0.99 | 3.33 | 2.68 | 2.06 |

| Other Expenses | 37.24 | 45.19 | 75.58 | 23.33 |

| EBITDA | 17 | 35.42 | 58.79 | 16.76 |

| EBITDA% | 2% | 3% | 4% | 3% |

| Depericiation | 0.09 | 0.2 | 0.19 | 0.05 |

| OI | 6.81 | 1.07 | 1.78 | 1.02 |

| Interest | 3.96 | 15.35 | 18.87 | 5.22 |

| PAT | 13.86 | 16.02 | 30.11 | 10.05 |

| PAT% | 1.60% | 1.43% | 1.96% | 1.77% |

| Other Expense | 37.24 | 45.19 | 75.58 | 23.33 |

| Import duty | 10.98 | 10.76 | 18.32 | 7.72 |

| Storage Handling | - | 18.86 | 36.15 | 10.09 |

| Freight and Forwarding | 23.46 | 9.8 | 7.65 | 1.25 |

| FY 22 | FY 23 | FY 24 | Jun 24 | |

| Share Capital | 1.6 | 1.6 | 2.13 | 2.13 |

| Reserves | 105.13 | 121.16 | 190.74 | 200.8 |

| Long Term Borrowings | 60.23 | 60.05 | 66.82 | 62.51 |

| Short Term Borrowings | 60.1 | 269.09 | 229.83 | 208.34 |

| Finance Cost | 3.29% | 6.83% | 6.03% | 1.84% |

| Trade Payables | 193.77 | 115.666 | 277.64 | 338.68 |

| Inventories | 129.71 | 315.67 | 396.55 | 405.54 |

| Trade Receivables | 178.36 | 125.21 | 182.3 | 214.18 |

| Cash | 103.62 | 133.79 | 180.67 | 194.09 |

Rationale -

- Solving a clear business need

- Experienced promote group

- Chemical price upticks to support topline

- Valuations comfort (PE < 20)

- Storage solutions to be key

- Network effects as vendors concentrate and clients increase.

Insights-

- Rationale business catering to a clear need. (Were suggested by clients to solve this pertrochem issue during traditional caustic soda operations)

- Highly diversified supply and demand side

- Experience promoter group

- High Short-term borrowings, but that is part of business as there is no value creation as such, just a channel for import needs.

- Working capital days look moderate for a trading business

- Ratings upgrade along with bank limit.

- Low Float (~74% Promoters, ~11% Institutions)

- Things to look/Track

Inventory management strategy

Storage solutions economics

Guidance