huh! they were launching FMCG products and seem to be taking their eyes off compliance? Rare to get this warning letter amid pandemic and especially when USFDA has been generous in enforcements offlate.

Hi Sumit: It is incorrect to state that they have taken the eye of compliance. This Jadcherla inspection happened around 2nd week of Feb 2020 & they got the 483 issued. From then on , there was no communication from USFDA (even beyond the 90 day import alert deadline). Finally they got this warning letter-almost 7 months after the 483. Shilpa meanwhile had gone back with monthly submissions to see if they could get a VAI. Yes it is a big negative as margin expansion would not happen (Formulations is where margin is) , new approvals would not come through but atleast there is clarity on the issue ( had been festering for too long). It is only because of this pandemic that USFDA outcome was delayed. Lets see how they tackle it , for sure this delays future launches by atleast 6-9 months

They are in the pharma biz for so long so you can’t make it a trivial mistake. If they are really capable, they need to demonstrate regulatory trouble free run of their plants. There are many Indian pharma players who have much cleaner record. Are they not managing it proactively? I am not an expert on this subject so can’t go into the details of the actual impact but an investor can’t not ignore repeated issues with the regulator and keep giving high valuation.

Notes from Shilpa Medicare’s Q1 investor ppt -

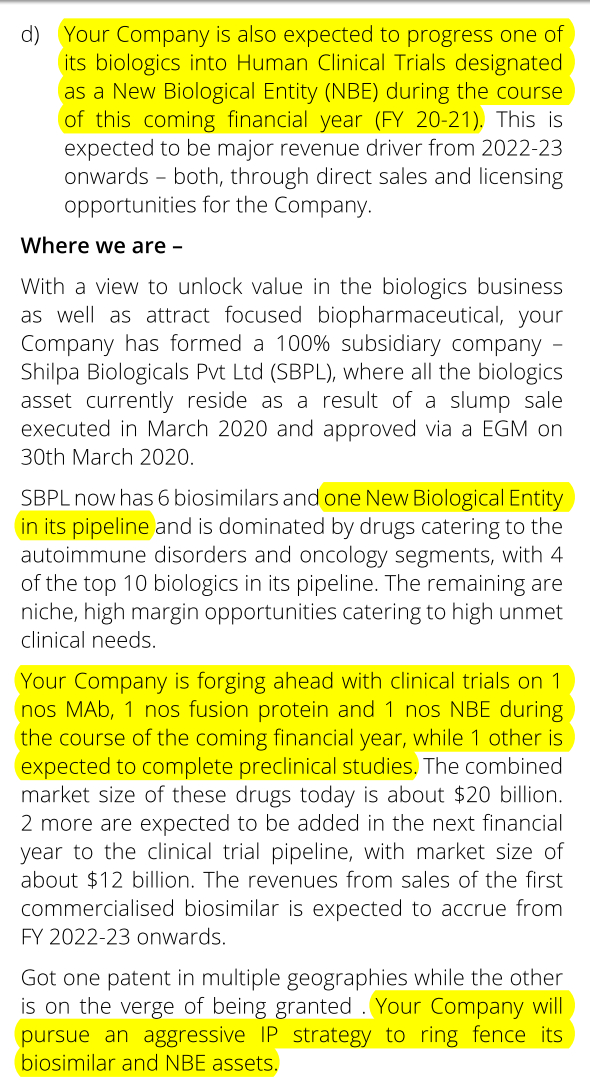

- 06 biologics in pipeline. Strengths in development of continious bio processing has the potential to disrupt the current Mkt Pricing.

A few lines about this process ( an extract from an article ) -

Continuous bioprocessing has been proposed as one future biomanufacturing state because it operates at similar scales for both clinical and commercial production using flexible facilities that can react readily to changing market pressures. Application of flexible infrastructure such as singleuse flow paths and small surge vessels and similar bioreactor sizes will reduce footprint and capital investment while simplifying technology transfer activities and maintaining quality-attribute profiles. Continuous equipment trains can operate over long periods, so this manufacturing approach will need closed processing to manage the risk of microbial contamination. In addition, integration of downstream processes into a single flow path requires synchronization of each unit operation through automated process control.

-

Biologics capacities -

Two independent lines -Single use ( 1000 KL bioreactors each ) and one 200 KL single use line for production of MABS ( monoclonal anti bodies ) and other recombinant protiens from mammalian cells. ( Do google the benifits of single use Bio Lines vs Stainless Steel reactors )

MABS are man made protiens that mimic human anti bodies.

Recombinant protiens - Protients made artificially using recombinant technologies ( joining of DNA from two different species for medicinal / agri etc uses ). -

Novel Biologics - Molecular pipeline, patent protected.

Targeting - low regulator barrier cell therapy, high regulatory barrier markets with the potential to disrupt the best in class. Also has the potential to develop targeted chemotherapy drugs.

Capacities in Novel Biologics - 2 lines each of 1000KL fermentation capacity for production of the NBE to cater to clinical trial material and formulation grade material.

- Manufacturing footprint -

Dharwad - Bioglogics manufacturing

Raichur Unit 1 - API - Both Onco and Non Onco

Raichur Unit 2- API - Both Onco and Non Onco

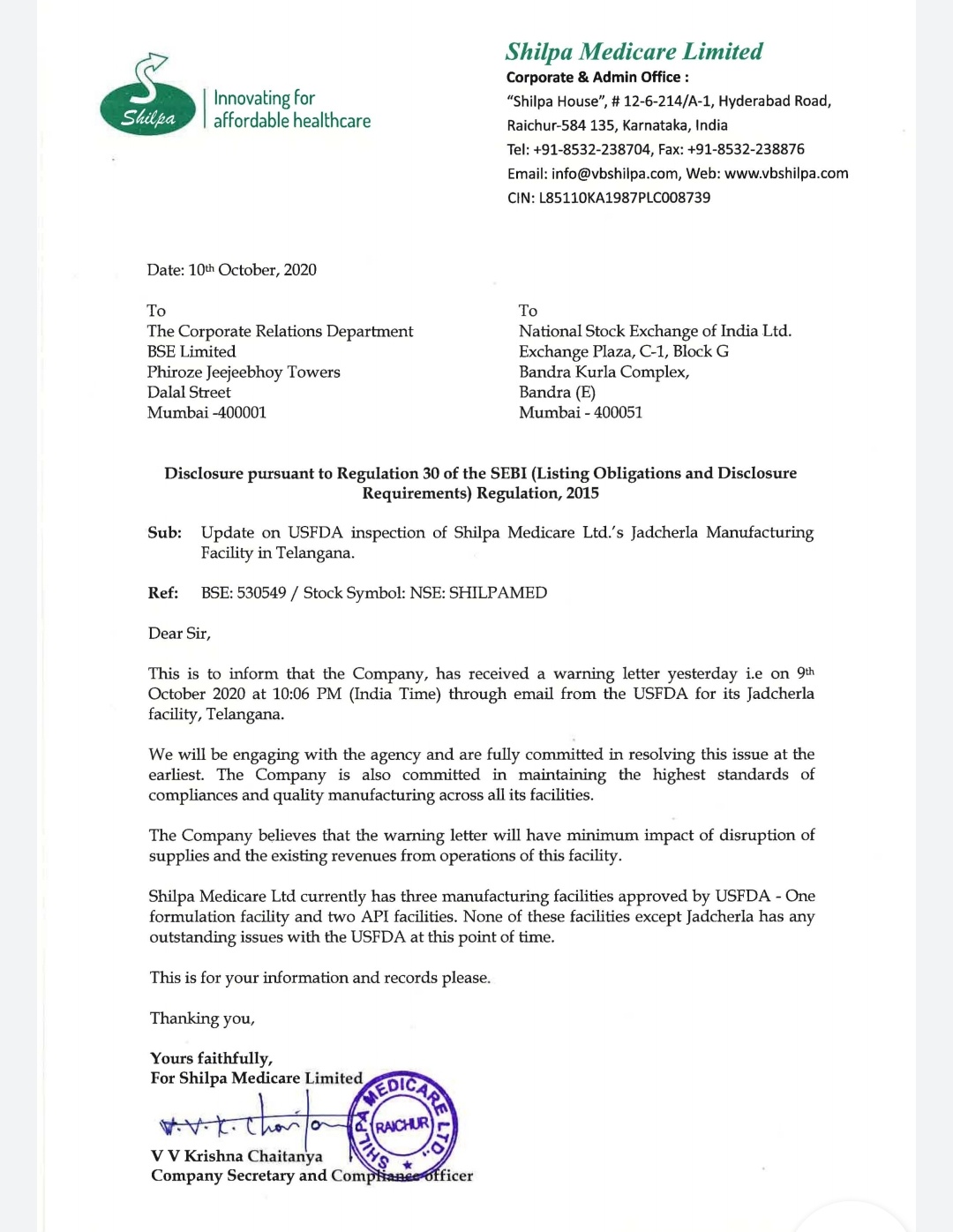

Jhadcherla - Formulations ( Onco and adjuvant therapies - oral and injectables ) - This is the facility that has got the FDA warning letter on 09 Oct . This plant was inspected in Feb 2020, was flagged with 15 observations.

Hyderabad - Oral dissolving films - formulations

Austria - API

-

Consolidated sales - 228 cr, up 40 pc YoY

Consolidated EBITDA - 70 cr, up 127 pc YoY,

Consol - EBITDA margins at 31 pc vs 19 pc YoY

API sales - 147 cr vs 110 cr, Formulation sales -

56 cr vs 31 cr, Others - 7 cr vs 5.5 cr, Service and

Licence fees - 6.2cr vs 7 cr. -

Last three yrs key data -

Formulation sales - 89cr>165cr>191cr

API sales - 365cr>348cr>388cr

Service and License income- 36cr>30cr>89cr

- Company has launched 3 key Onco products in India mkts in last 1 yr at affordable rates -

Ibrushil - Ibruninib

Dasashil- Dasatinib

Axishil- Axitinib

Disc - invested, small portion of portfolio.

Yes I agree, they should demonstrate trouble free run complying all regulatory requirements. But in case of USFDA, many things are always unexpected. This Jadcherla plant was inspected in November 19 by USFDA and cleared smoothly. Immediately after it was inspected again by USFDA in February 20 and got many 483s. This all probably depends on inspector too. Aarti Drugs is still struggling after 5 years. Good thing is that Shilpa story is not fully dependent on Jadcherla, there are many feathers in hat. Yes, metamorhing into formulation is delayed again, this has been continuing for 4 years.

Regarding Shilpa’s recent USFDA warning letter,

I cannot find it on the USFDA website:

https://www.fda.gov/drugs/warning-letters-and-notice-violation-letters-pharmaceutical-companies/warning-letters-2020

The website says that “Content current as of: 10/13/2020”. Would anyone happen to know why this might happen?

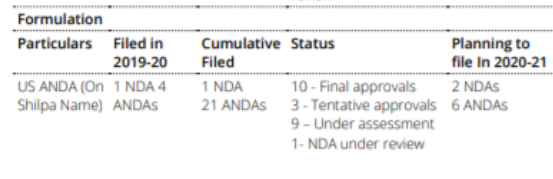

As per my understanding NDA’s are either filed by Innovators or CDMO’s (for innovator). How come Shilpa, a generic drug company file NDA?

Disclosure: Not holding.

Shilpa indeed has a New Biological Entity. It is not a pure generics player.

Source: Page 43 AR 2019-20

Are you sure about this timeline ? I’ve been doing some reading up on Shilpa’s usfda troubles and it seems that they received the 483s based on inspection in August 2019 (not in 2020). See this :

https://www.google.com/url?sa=t&source=web&rct=j&url=https://www.fda.gov/media/130236/download&ved=2ahUKEwjwufHDmb7sAhWhoekKHfDiAWMQFjAAegQIFxAC&usg=AOvVaw2vkE0Chjl5CnnyLyX2N5Wm

Key learnings for me from the 483:

- Shilpa does not use the equipment which they promised usfda they would use. They also did not inform about change in the production process and did not update the production flowchart.

- They had 3 power failures in a duration of 15 minutes and the back up generators did not kick in. The investigator noted that several times there are 8-9 hour power cuts and it is not documented how this affects the quality of the produce and no attempts were made by shilpa to study how the power cuts affect the in process products.

- There was a lose bolt under a machine and no documentation for what this bolt was for.

- A particular machine used in qc was decommissioned and no replacements were put in place until the second day of the inspection.

Overall, it appears that the culture of compliance simply does not exist (or it would be more accurate to say, did not exist when the 483s were given). The fact that the 483s resulted in a warning letter means that shilpa did not manage to adequately address USFDA concerns in the period between the inspection and the awarding of the 483. I’ve tried to contact the company secretary about this but haven’t received any responses. Had a tracking position until last week. Planning to liquidate next week and not invest.

It is most likely that their NBE and biosimilars pipeline is being built for india and emerging countries, where the price they can fetch are much lower, so are volumes. As per my understanding, it takes 30-40 million dollars per biosimilar filing with USFDA and shilpa is simply not doing that kind of capex. The core work of the company is definitely very interesting. Their USFDA compliance would be a key monitorable for me.

These obswrvations are for Raichur plant. You can check post by Monk88888 in Aug19 regarding this. This is for API plant and it was cleared in Dec19. It is also available in this thread.

Present USFDA issue is for Jadcherla formulation facility. This USFDA is most important to transform into formulation player.

https://www.fda.gov/inspections-compliance-enforcement-and-criminal-investigations/warning-letters/shilpa-medicare-limited-607877-10092020

Not gone though it as yet not a pretty picture on a quick read basis

this is related to a particular batch for which there seems to be contamination and customer complaints. the FDA letter says that

- investigation on why the contamination occured was not carried out properly and the explanation is not sufficient to explain the contamination

- handling of customer complaint and the response did not follow the standard procedure…

they have recommended hiring of consultant and recheck thier processes. till such time they clear all the observations new products from this plant will not be approved.

Credit Rating update from India Ratings

Strong Business Profile; Experienced Promoter: –

- SML is a niche player in the oncology space (oncology accounts for over 70% of the total revenue), with a presence in active pharmaceutical ingredients (API) (FY20: sales of INR5,544 million; 61% of total revenue) and formulations (FY20: INR1,943 million; 21%) segments.

- SML supplies more than 30 oncology APIs and over 10 formulation products to various regulated and semi-regulated markets, including the US, Europe, Japan, South Korea, India, Russia etc. through a B2B business model.

- SML has a strong vintage of supply relationships with global generic companies. Domestic sales contributed about 32% to the revenue FY20, while exports accounted for about 68% of the same.

- Its facilities are approved by United States Food and Drug Administration (USFDA), United Kingdom Medicines and Healthcare products Regulatory Agency, European Directorate for the Quality of Medicines & HealthCare, Therapeutic Goods Administration - Australia, Pharmaceuticals and Medical Devices Agency-Japan, Korea Food and Drug Administration-Korea, and Therapeutic Products Directorate-Canada.

- Furthermore, SML’s promoter, Vishnukant C Bhutada, has over 35 years of experience in the pharmaceutical industry.

Medium Scale of Operations:

- SML’s revenue rose to INR9,079 million in FY20 (FY19: INR7,334 million) due to the continued pick-up reported by the formulations segment. The API segment’s revenues declined by 15% over FY17-FY20, primarily due to the reduction of contract research and manufacturing services (CRAMS)

revenue, while the formulations segment witnessed a strong CAGR of 31% over the same period. - SML has modest customer concentration, with the top ten customers (ex-sales to CRAMS JV partner) accounting for about 50% of its revenues in FY20.

- SML’s product concentration is stabilising, with its top 10 products accounting for only about 45% of the total sales in FY20 (FY19: 45%, FY18: 49%).

- According to the management, SML is amongst the top three players by market share in oncology formulation products such as capecitabine, docetaxel, tarceva, gemcitabine hydrochloride and irinotecan in the US market.

- SML has a record of growing its research capabilities through the acquisition of stake in entities like Sravathi Advanced Processes Technologies Private Limited, INM Technologies Private Limited etc.

- SML recently acquired FTF Pharma Private Limited for INR750 million,; the acquisition will aid SML in under the Food and Drug Administration’s section 505 (b)(2) new drug application fillings.

Investments into Newer Therapy Areas:

- SML has made significant investments via research and development (R&D) and capex to enhance its current capacities into newer areas such as biosimilars, transdermals and films, apart from expanding its API and formulations facilities.

- Its R&D investment increased to INR1,288 million in FY20 (14.6% of sales) from INR341million in FY16 (4.8% of sales).

- SML has been able to monetise its R&D spends via product development and license revenue (FY20: INR1358 million); the management expects this segment to clock annual revenue of INR800 million-1,000 million over the medium term.

- SML is also in the midst of a capex cycle of about INR 10 billion for capacity enhancements and for future initiatives (about 35% of this amount was spent on the biologicals facility in Dharwad and almost 20% was transdermals-related capex).

- SML had a substantial number of products lined up even in the newer therapy areas such as films, topicals and transdermals (Filed – 48, Granted – 2) and Biologicals (Filed – 8, Granted – 2) as of September 2020.

- SML has set up a R&D and manufacturing facility in Belur, Dharwad, for its foray into the biosimilars segment, under a carved-out entity, Shilpa Biologicals Limited, for an initial investment of INR3.6 billion.

- The biologicals business is likely to generate revenue from the end of FY22, and according to the management, it will add 15%-20% to the top-line post the ramp-up, primarily driving the consolidated revenue growth.

Disclosure: Invested; No transactions in the last 6 months

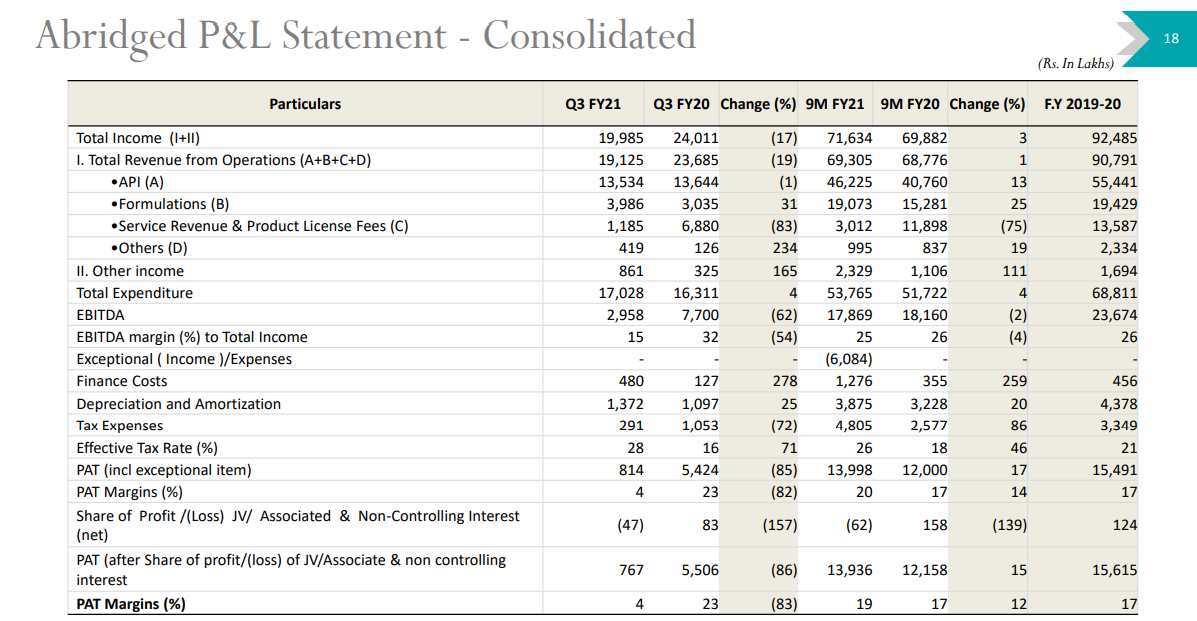

Company came out with very poor set of results in Q3FY21 with most of the damage led by USFDA warning letter issued in October 2020. Detailed investor presentation here

As per the update, remediation measures are in full swing, and committed supplies to resume from Q4FY21 - so numbers might see some sanity in the next quarter.

Company is trying to make best use of its capacities by participating in the manufacturing of viral vaccines and emerging CDMO opportunities

From the results, what’s concerning is the growing list of subsidiaries. Why would a small cap pharma company need so many subsidiaries needs to be pondered upon.

- Koanaa Healthcare Limited, UK (Wholly owned subsidiary Company)

- Koanaa Healthcare Limited, Austria (Wholly owned subsidiary Company)

- Zatortia Holdings Limited (Wholly Owned Subsidiary Company)

- Shilpa Therapeutics Private Limited (Wholly Owned Subsidiary Company)

- INM Technologies Private Limited (Wholly Owned Subsidiary Company)

- INM Nuvent Paints Private Limited (Step down Subsidiary Company)

- Loba Feinchemie,Gmbh (Step down Subsidiary Company)

- Makindus, Inc (Subsidiary Company)

- MAlA Pharmaceuticals, Inc (Associate Company) r cfo j. Reva Medicare Private Limited (Joint Venture Company) i

- Reva Pharmachem Private Limited (Associate Company)

- Shilpa Pharma Inc (Wholly owned subsidiary Company)

- Sravathi Advance Process Technologies Private Limited (Joint Venture Company)

- Shilpa Biologicals Private Limited (Wholly Owned Subsidiary Company)

- Shilpa Biocare Private Limited (Formerly known as “Shilpa Albumin Private Limited” - Wholly Owned Subsidiary Company)

- Koanaa Healthcare Canada Inc (Wholly owned subsidiary Company)

- Shilpa Corporate Holdings Private Limited (Wholly owned subsidiary Company)

- FTF Pharma Private Limited (Wholly owned Subsidiary Company w.e.f 2nd November, 2020)

- Auxilla Pharmaceuticals and Research LLP (Joint Venture)

- Sravathi AI Technologies Private Limited (joint Venture Company)

- Indo Biotech SDN.BHD (Wholly owned subsidiary Company)

- Koanna International FZ-LLC

The management seems to really lost its focus. Another FDA letter…

This is not another letter but the official letter from USFDA for last year’s audits. The company has issued detailed clarification including the warning letter reproduced in original. LINK

We had received fifteen 483 observations at the closeout of FDA inspection on February 25, 2020. The Warning Letter received on 10 Oct 2020 had specifically mentioned two

citations - (i) inadequate handling of OOS and (ii) inadequate handling of market complaints, including failure to file FAR within stipulated time.We had responded to the Warning Letter on October 30, 2020, followed by three followup responses outlining the CAPA’s and their progress. We have had two tele-meetings with the USFDA on Nov 12, 2020 and 25 Nov, 2020. We have not received any subsequent communication from USFDA since Nov 25, 2020, until yesterday.

This notification of Import Alert does not mention any further reasons/observations

other than nonconformance to cGMP.We have already engaged the services of US based reputed GMP 3rd Party Consultants

to help us with the remediation efforts.We are committed to addressing the concerns raised by the USFDA and will work with

the USFDA to resolve these issues at the earliest. We uphold quality and compliance

with utmost importance and are committed to maintaining cGMP and quality standards

across all Shilpa facilities.The Notification on Import Alert received from the USFDA, is enclosed herewith.

We shall keep you informed on further significant developments, including supply

related information.

I think its a clear scenario of black clouds for Shilpa Medicare. I hope these will pass away soon, but I have 2 points of worry here,

- Will it affect the future approvals from USFDA as in the end approvals are important for future growth,

- And, Will it affect the outlook, retail investors will have towards the company.

Shilpa Medicare Limited enters into Gynecology Segment by launching its First Women Intimate Cleansing Spray in India under the Brand Name “SwatchShil”

SML.pdf (729.3 KB)