Looking at this year heat wave and massive transformer failures, I am expecting, good units might have been sold. A Wild guess. Let’ see.

1 Like

I think they had some inventory left - so numbers will be better from Q4 and much better from Q1 of last year

Shilchar is not into that kind of transformers. So what works for the bulk transformer manufacturers like Voltamp BBL, etc. won’t work for Shilchar. Most of the margins come from Export to EU and US, and in domestic consumption also the transformers they produce are mostly used in small scale industrial applications. So I think the push factors for them are quite different from other players in the market, and hence the higher margin.

6 Likes

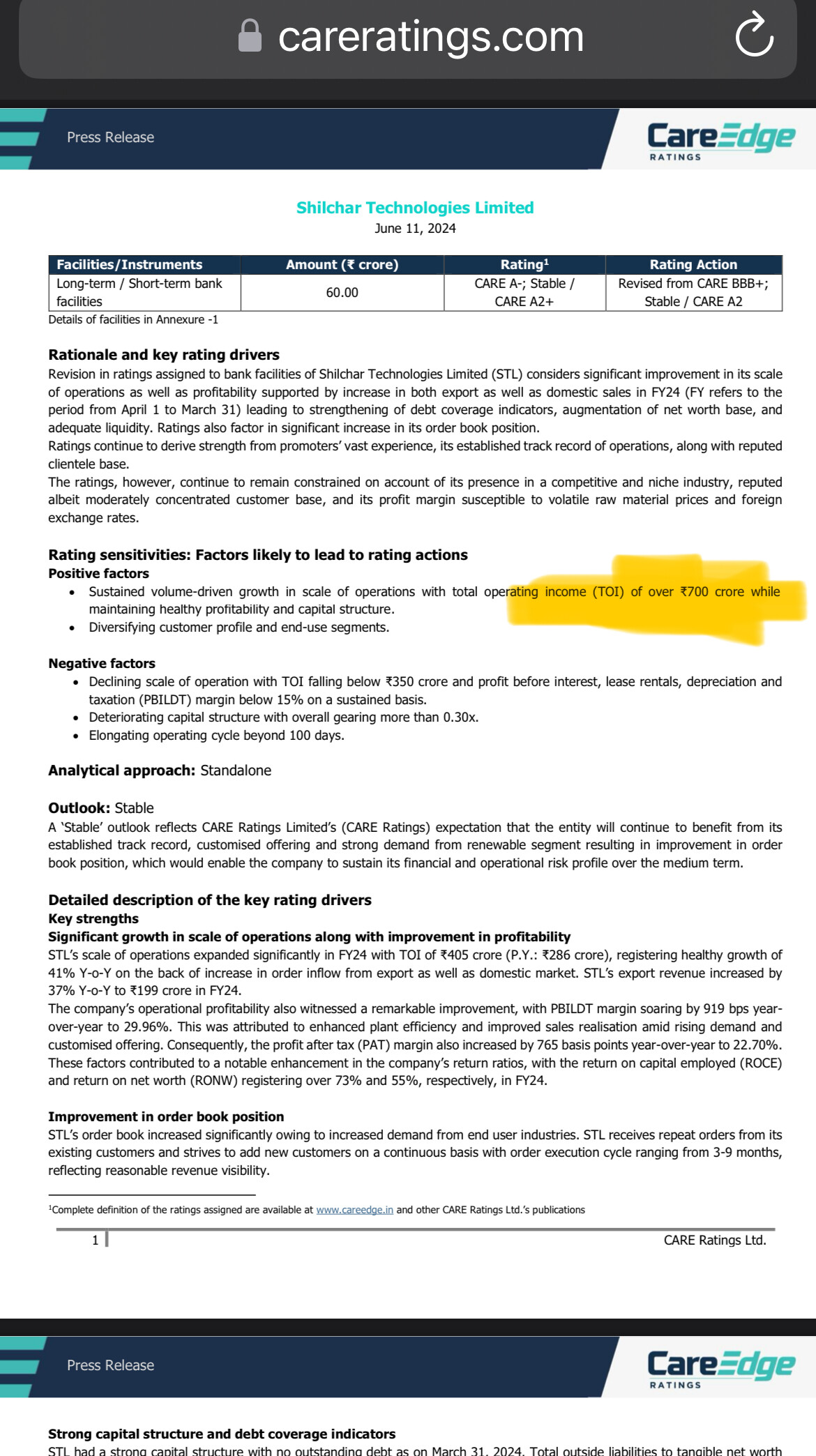

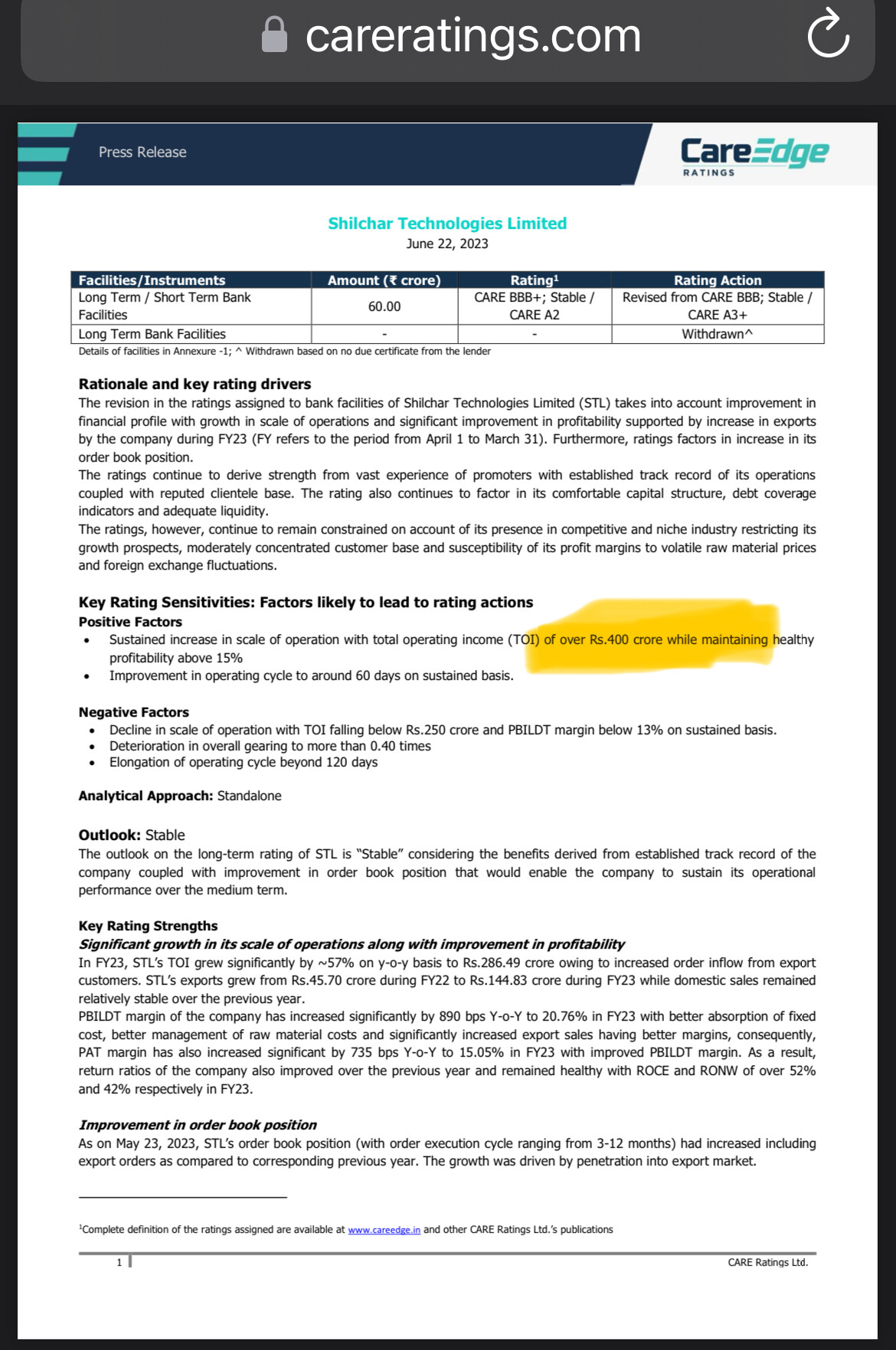

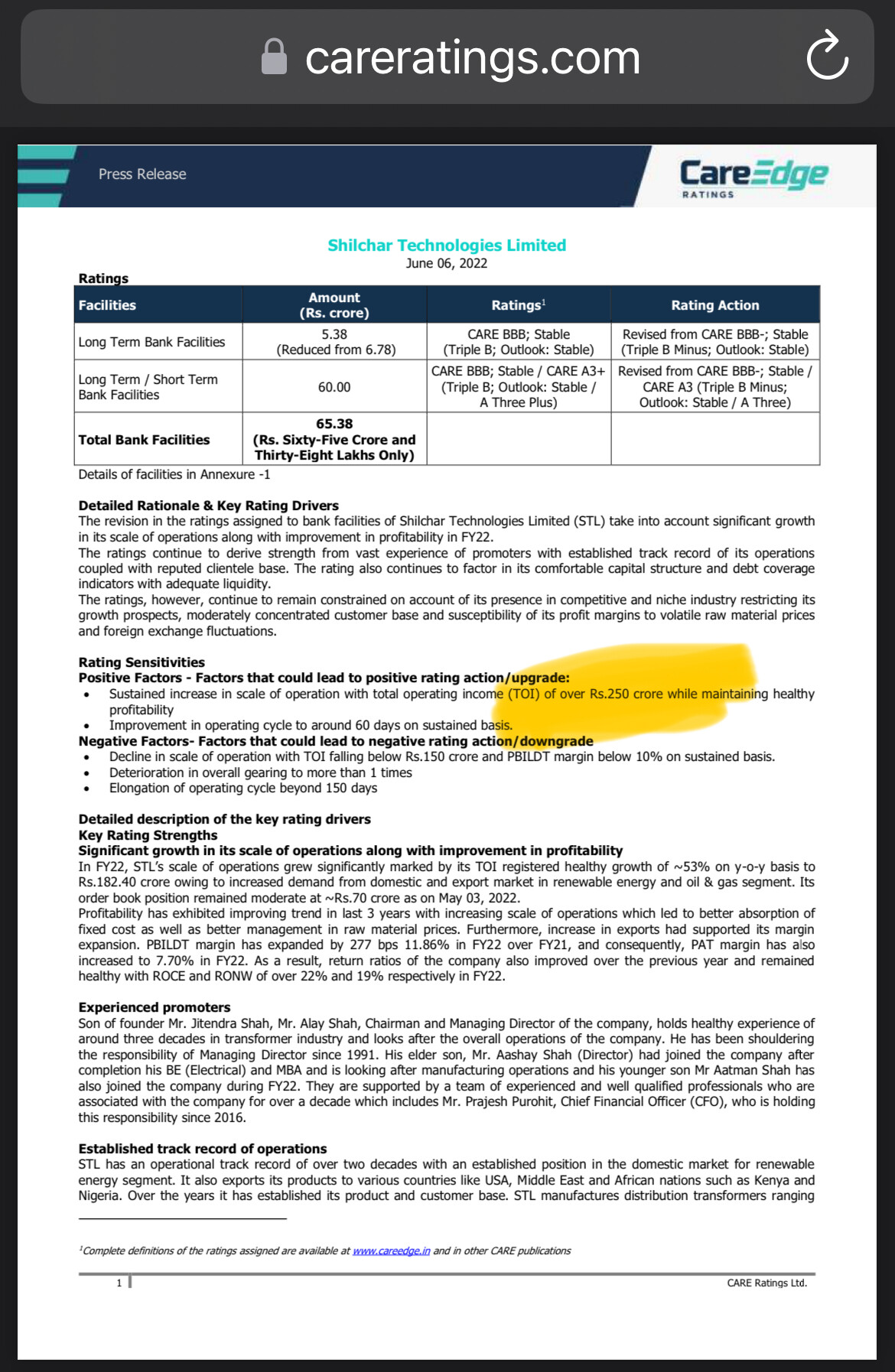

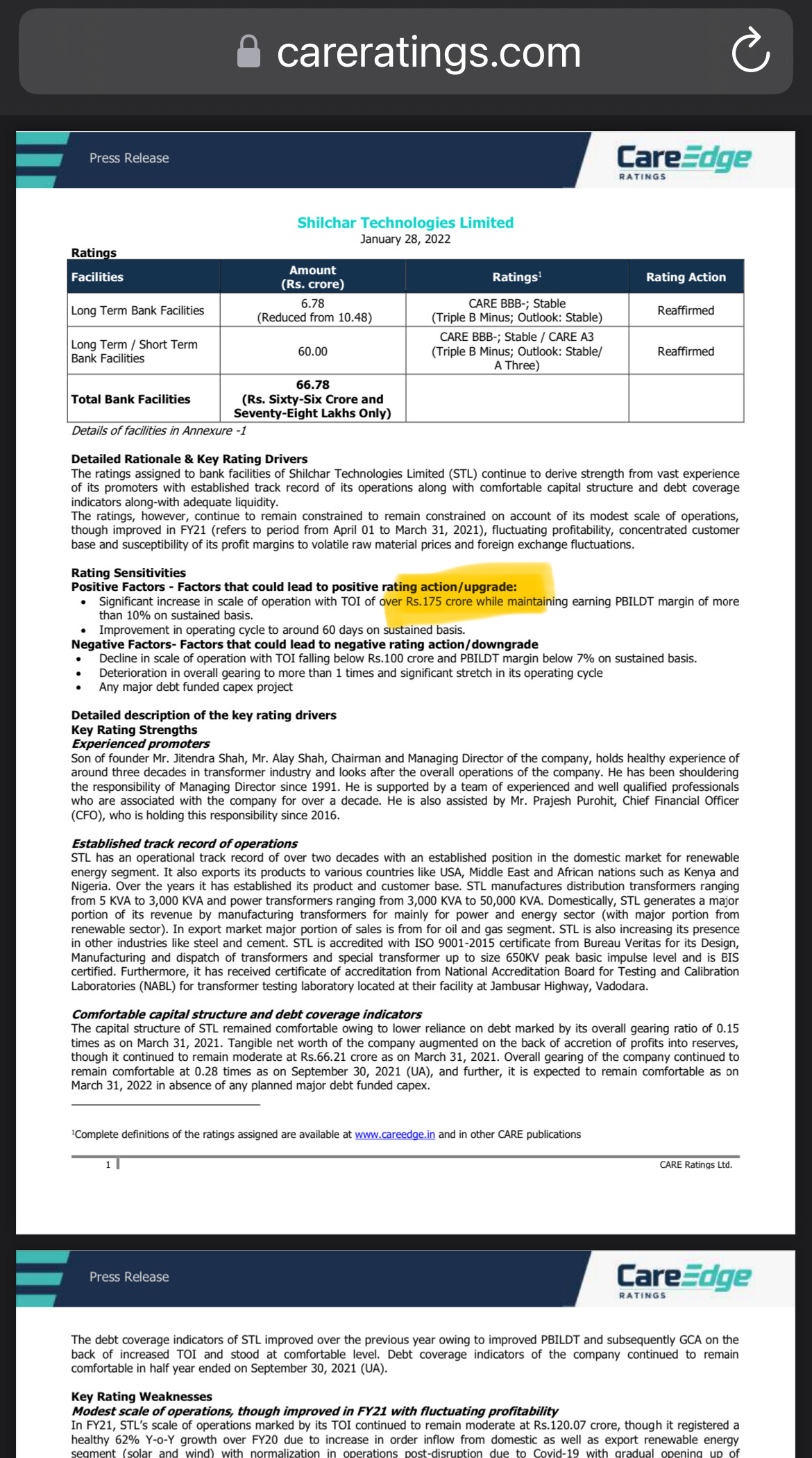

Recently CareEdge has upgraded Credit Ratings of Shilchar on account of improved performance.

One interesting point I found in the ratings report is hidden guidance of 700 revenue by the management.

To dig deeper if we check these credit reports of last 3 years we can clearly see the number given in those reports is matched or exceeded by the company

In 2021-22 they did 180 crores against guidance of 175 crores in credit report. Similarly, in

2022-23 280 crores against guidance of 250 crores and in

2023-24 397 crores against guidance of 400 crores.

Surprisingly, management is guiding for 700 crores revenue despite delay in capex by four months for phase-1 and one month for phase-2. But again, the company has so far over delivered on every front and have been quite no-nonsense and that gives confidence.

In my opinion if they achieve this 700 crores, in ideal world this could be approximately 100 crores, 150 crores, 200 crores and 250 crores for Q1, Q2, Q3 and Q4 respectively with some hits and misses.

55 Likes

Amazing observation!

Looks like company underpromises, overperforms! Great observation!

3 Likes

1 Like

I think Company expects the turnover of around Rs. 800 to Rs. 900 crores in two years, NOT For the FY25.Please correct me if I miss any …

2 Likes

Might be I will be worng with these hypothetical Earnings ![]()

Q1FY25 +93(40% YOY)//PAT 20(21%)

Q2FY25 +148(40% YOY)//PAT 31(21%)

Q3FY25 +165(40% YOY)//PAT 34(21%)

Q4FY25 +147(40% YOY)//PAT 31(21%)

FY25 +553(39.29%)//PAT +116(21%)

3 Likes

Shilchar AGM was conducted today. Key takeaways:

→ Demand and outlook continue to be strong both in India and exports. Current order book is 480 cr. Little delay in commissioning of new capacity mainly due to monsoons.

→ Will start utilizing new capacity mostly in H2 and expect 100% utilization in H2 itself. FY25 revenues expected to be 550 cr+ and expecting ~750 cr type of revenues in FY26.

→ Plan to manufacture transformers in same range as now since it’s a stronghold for the co. No plans to cater to higher kVA range.

→ Domestic & export demand both continue to be strong. Have successfully entered the EU market and like all markets it will take 1-1.5 years for significant revs to accrue. Expect this to be a strong market though can’t guide what percentage of revenue will come from here. Have already received first order. Mostly catering to the renewable sector in EU.

→ Though mgt didn’t answer it directly they seemed to suggest current profitability will sustain.

→ Call on next round of capex will be taken in Nov-Dec this CY(if I caught this correctly)

Q1 nos came few hrs post AGM. Probably for the first time Q1 revenues were same as Q4. This clearly underlines the strength in demand. If not for lack of capacity,revenues could’ve been higher than Q4 as well. Profitability continues to be strong and I sensed higher confidence on the same in the concluded AGM vs earlier years.

Disc.: Invested. Views are biased.

47 Likes

Thanks for the AGM insights. Highly appreciated

Anything on holding concall. They didnt held it in the previous quarter as well

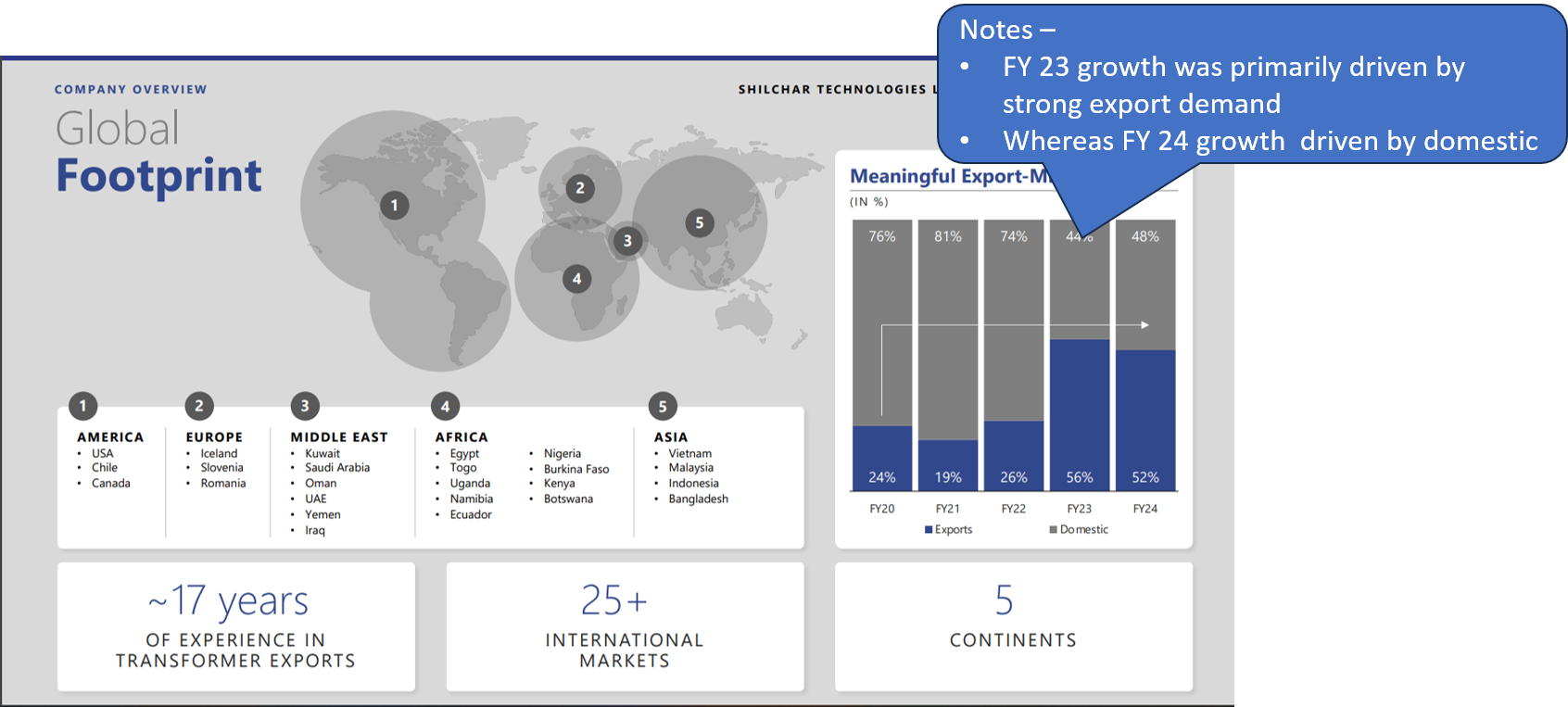

Shilchar has finally hired an IR team and come up with an interesting and detailed investor presentation. Gives a holistic overview of their capabilities, new plant, business model positioning, ability to scale up quickly through internal accruals, etc.

Few key slides which are worth highlighting –

Exports have seen a sizable jump from 24% to 52% , aided by strong design & engineering capabilities and ability to deliver customized solutions at scale.

Strong presence in Middle East & America

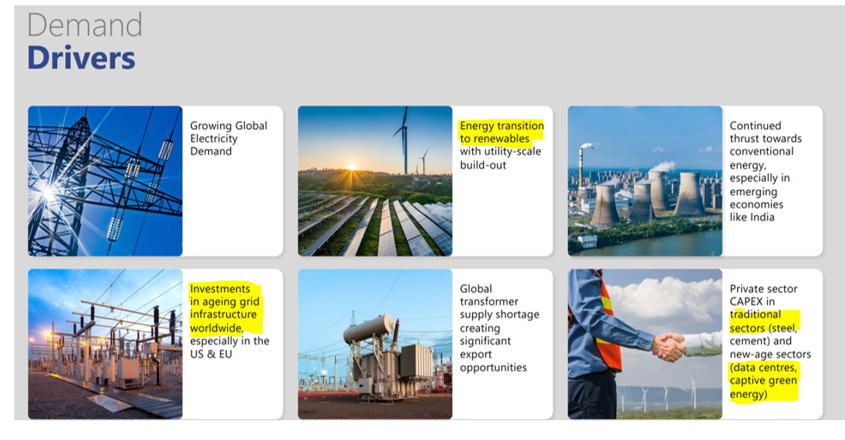

Demand drivers

- Good mix of drivers from conventional sectors like Renewables, steel, Oil & gas, and export opportunities rising from grid infra replacement and transformer supply shortage

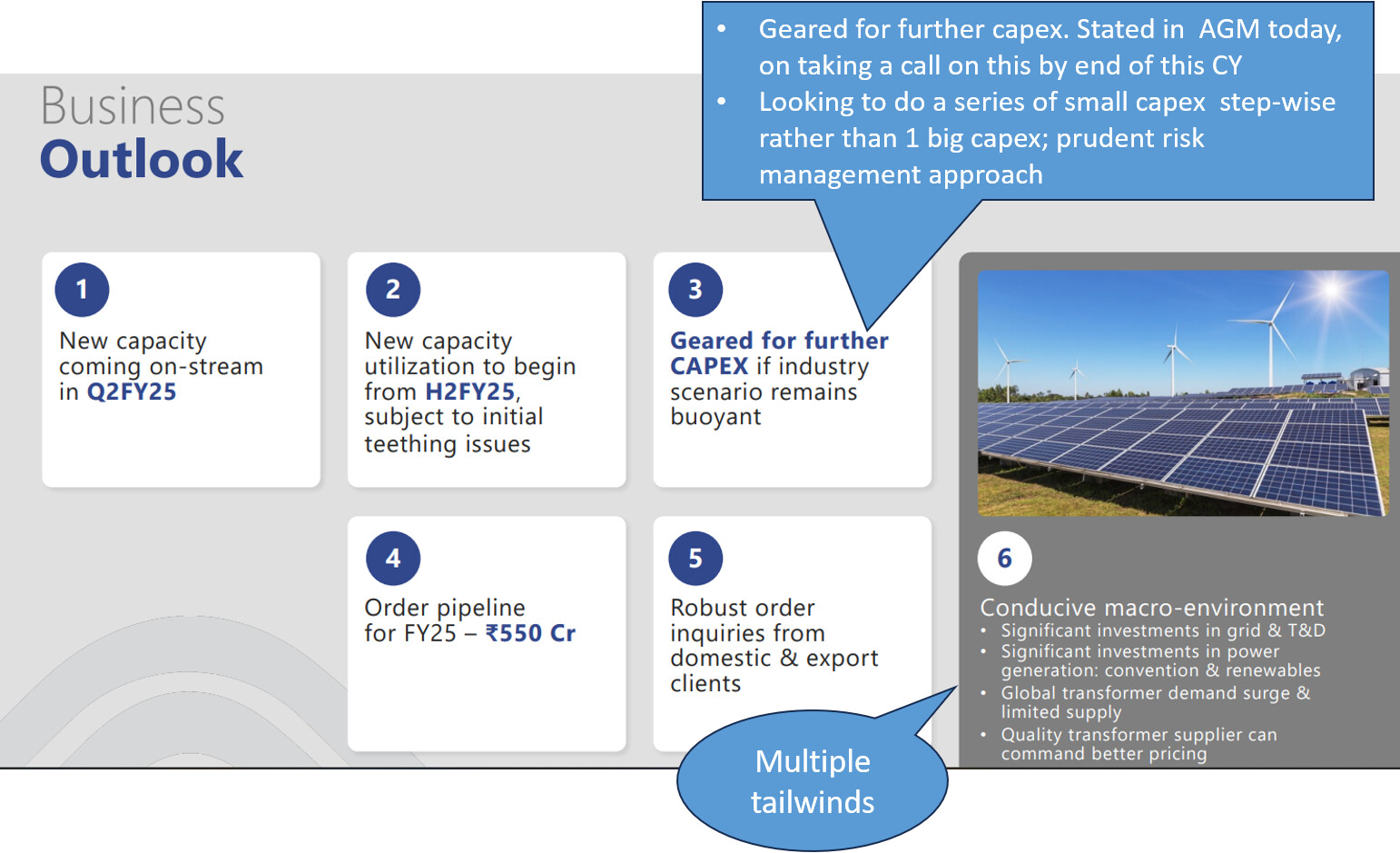

Business Outlook

Disc: Invested from lower levels; views are biased

14 Likes

I heard that there is shortage of Transformers in the world . Am I correct ?

How does that impact Shilchar Tech? Pls explain in layman’s language…

Its not impacting Shilchar in specific… this article just validates from end customers mouth that Transformers have a high demand and a high waiting time.

So new capacity would get consumed fast

10 Likes

The expanded capacity was to be utilised from 16th August. Anyone having an idea if the same has commenced since the capacity expansion had got delayed due to rains.

There hasn’t been any release post commencement of production from the same.

1 Like

I have a stock analysis audio clip of Silchar technologies . How should I share here ?

If it is not a paid one - it should be safe to upload it

audio clip uploading option is not available on Value pickr