@desaidhwanil

Shemaroo Entertainment: AGM Meeting on September 26 2016 in Mumbai

Disclaimer: I hold share in the company and no change in my position in last one month. Please note that there might some misunderstanding while taking down notes in AGM and hence reader shall aware about same. Also, all investor are advised to do their own independent due diligence as my views might be biased due to my interest in the company.

I have attended AGM of Shemaroo. Find enclosed key discussion points in the AGM from Chairman speech followed with Q&A with management by the shareholders:

1) Likely completion of Investment mode of the company

Currently, the acquisition of the new content is higher than the monetisation of the content as the company is in investment phase. The company is in process to build up content titles. During last 5 years, the title ownership has increased around 2000 to more than 3,400 titles now.

2) Economic Value and Accounting value of Perpetual Rights:

The accounting policy of perpetual right in provided in presentation. As per industry norm, transaction cycle for traditional media is 5 years. For films where the company has more than 10 years rights, the company have would write off the cost over two cycles. In management experience, with increase in ad spent, the overall content price has increased by 12% p.a. over long term. Hence, Economic value of content is high. Accounting value of perpetual right would be written off over 10 years. However, the company would continue to sell the rights of broadcaster till the expiry of copyrights and that shall drive the revenue (rather PBT) from year 11, as there is no cost being charged for same. Hence, Economic value and Accounting Value of perpetual rights has some variation.

3) Free Cash Flow and Debt position

The company expect debt position to increase to highest level in 2018 and Free cash flow to increase significantly post 2018 for the following two reasons:

a) Even after 2018, the company would continue to acquire the new content, however, there would be benefit of higher margin of old perpetual content (after two cycle, nil cost of perpetual rights) and also the company has sufficient large library which would reduce the per centage growth. For instance, 100 movies on 2,000 would be 5% of size which shall be only 2.5% when the company has library of 4,000 titles. Further, of old 1,000 rights, many would be having completed 10 years (the company started acquisition of title in 2005). So acquisition cycle (investment mode) would reach maturity by 2018 while monetisation phase would have just begun for the company.

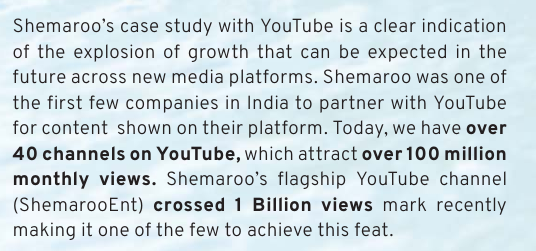

b) Higher Broadband penetration (with increased use of lower cost Smart phone) coupled with superior data speed (with all players moving to 4G). All these factors are likely to drive content demand through various platforms from DTH/YouTube/Netflix/Jio. The company would be gaining business at least from the one the platform which shall drive the Free cashflow growth going forward. Industry growth for Digital content for next five years is expected to be around 35% p.a. and for traditional media is expected to be 12-15%. In past the company has grown at higher than industry rate which it expect to continue for next 3-5 years. Even working capital cycle for digital media is lower than traditional media. So the company would be able to get more free cash flow with higher share of digital content in revenue.

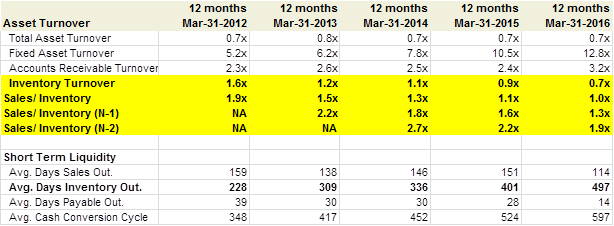

4) Inventory valuation of perpetual and Aggregate right:

The management said that the company is acquiring aggregate right on on-going basis. On a given day, the value of inventory may be affected to new acquisition or sale of aggregate rights. Hence, the valuation of volatile on a particular day and hence the company does not share that number, as a particular day inventory value would be not give true picture of inventory value.

5) Impact of Jio and Netflix

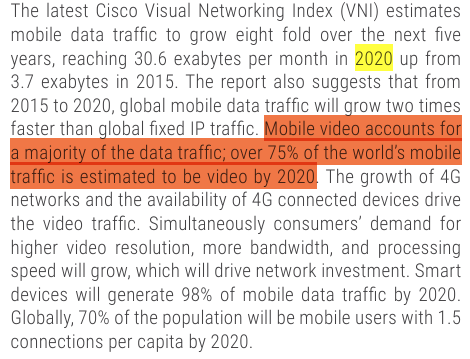

Netlfix launch in near term has increased the competition. It has package starting from Rs 500 p.m. to Rs 850 p.m. While it has yet to penetrate in big way in Indian market, due to current APRU of around Rs 200 per month, over a medium term, it is expected to change Indian Media from advertisement paid to consumer paid Eco system. The current system is more driven by advertisement revenue for the broadcaster which would soon shift to consumption driven. The revenue share for content provider in advertisement system is around 1-5 cents vis around 10 cents under paid Eco system. In the developed market, it has been observed that when the market move from advertisement base to customer base, content owner benefit due to ability to charge higher price. Hence, Shemaroo is optimistic to get benefit of content in long term.

Jio, on other hand, change the price and penetration of board band along with superior speed. Increase in broad band speed offer option to the end-user. One may choose to watch movie on YouTube/Hotstar or on Reliance Jio OTT. The end results would be all these would lead to higher consumption. Most of email and other basic usage of data can work on 3G as well. Once the consumer is used to 4G experience, it would be habituated to higher data usage which would be difficult to downgrade after 3-6 months of fixed price offer.

As per US Media Industry analysis, Top 5 Video and Movie service provider account for almost 2/3 of bandwidth consumption in USA. Same trend is expected to be observing in India.

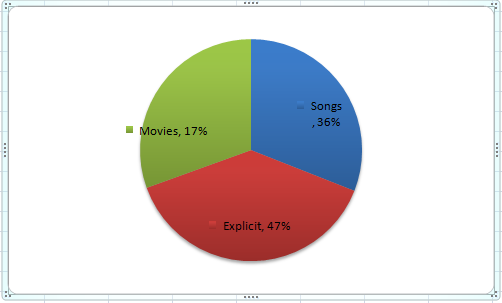

Further the increase in viewership, while not have material impact of CPM (YouTube advertisement rate), but would definitely drive higher CPM in medium term. So increase, in broadband and user with higher speed, drive higher demand for content which in turn increase Revenue by way of higher CPM, would result in higher margin.

Advertisement follows eyeballs. There would be positive impact on advertisement. In short term, it would drive in more shift from print media advertisement (not much from TV advertisement in first phase), which shall benefit the industry. The CPM growth rate would be increasing in long term.

6) Impact of Digitalisation of TV/Broadcasting

Current APRU for TV under Cable/DTH is around Rs 250 (USD 4) per month vis USD 35-40 per month. So India is spending is almost 1/10 of US. With various players now coming to market, the prices are unlikely to increase in short term, however, as market stabilise, we shall expect higher growth in APRU as well.

Pricing of Digital OTT offer have wider range with basic offer of 100 per month to Netflix with international content in range of 500-800 per month. Till current APRU is around Rs 250 per month, the Digital media would be restricted to only to elite audience.

7) Competition

In Second and subsequent cycle of film, there is no organised players. There are some unorganised and semi organised player. But none would be comparable to Shemaroo.

8) Other points

a) Net addition in inventory was around Rs 95 Cr in FY16. Gross addition can be calculated from balance sheet but figures were not readily available.

b) Rate of interest on borrowing is 11.5-12% pa.

c) Subsidiaries are for multiple reasons. For US and UK region expansion. Other is for parallel markets not related to main business, but related to content utilisation like Airline distribution. Couple of subsidiary for film business. There is no activity on film production, no release in last 18 months. There is no film on production as of now. subsidiaries are in investment mode and Shemaroo would continue to support them. The management expect most of subsidiaries to turn around in 1-2 years.

d) There is no dead inventory in the titles. The company write off acquired aggregate right which are not sold within 18 months is written off. However, that does not mean that the company cannot generate any revenue from such content. At time a single song or scene has generated more than expected revenue on Digital front for the company as against total acquisition of film price.

Request other members present also to give there view in case I have missed any point or misunderstood any points.