I am still not convinced to buy sheela foam at current price. I donot understand why such companies got such high valuation with very little growth.

Anybody can explain, what I am not looking or where I am wrong.

I am still not convinced to buy sheela foam at current price. I donot understand why such companies got such high valuation with very little growth.

Anybody can explain, what I am not looking or where I am wrong.

I agree on little to no growth. Only reason for me to track this is two positive triggers which have happened in last few months/year -

This wasn’t delivered by mgmt. Does anyone know if there is commentary by mgmt on this?

SFL will continue to trade at premium valuations given its market share and low public holding. For generating wealth, we need to identify good companies during their bad times. Companies like Sheela Foam (SFL), Hindware, Acrysil, TTK Prestige, etc. are cyclical stocks (home building and home improvement) and hence not doing well at the moment. During the upcycle, each of these will skyrocket.

No…u have not told about demography of Sheela foam and Kurlon in your posts…I was referring to some details in public domain about Sheela foam is strong in North and west, where as Kurlon is strong in south and eastern parts…So was looking for your opinion about this spread of business and festive season sales

None of these are undervalued now though. Fairly valued with decent upside potential, maybe, if one assumes a robust consumption recovery in the near term. There are still no signs of that though. I am interested in Sheela Foam, but yet to be convinced that it’s time to get into it in a meaningful way right now.

Shraddha kapoor( 2nd most followers after Virat Kohli) just posted instagram ad on sleepwell (Shraddha ✶ on Instagram: "My recent sleep upgrade @officialsleepwell’s Pro FitRest mattress! 💤✨ I value quality sleep just as much as I value fitness and my work, and the Pro FitRest mattress has been an absolute game changer. My recommendation if you care about your sleep and muscle recovery as much as I do. And don’t forget to ask your loved ones every morning, “Did you Sleepwell?” #ProFitRestMattress #Mattress #DidyouSleepwell? #Sleepwell #collab")

Stock is in support zone of 2017

Acquisition synergy may start playing out now

PS: Took some position, no reco

Been studying this a bit, and came across this interview. Quite enjoyed it, so sharing.

Very disappointing result. Management committing but not delivering.

Drastically reduction in EPS.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8eaeb75a-9aa6-49c1-97f7-b02261b72555.pdf

Anyone attended earning call? Please share your views

-----------------------------------------------------------

Not attended any such call however providing summary of what has been provided over legitimate screeners.

-----------------------------------------------------------

1. Acquisition of Kurlon

2. Financial Performance

3. Growth Strategies

4. Operational Highlights

5. Challenges

Overall Outlook

There’s nothing wrong here. They have interest expenses from their acquisition and, on the other hand, depreciation—which was paid upfront but is recorded monthly in the books to leverage tax benefits. This isn’t exactly a deduction.

India / Asia is a growth market, but large US/ European firms will be setting up manufacturing bases here. Its going to be interesting how Sheela Foam competes at one end with the startups and at the other with these established much larger global firms…

I think branded mattress manufactures from world in India will increase overall healthy awareness among consumers and it will help to translate business from non-organizing sector to organized sector… Sheela has good cost controlled manufacturing capability will take benefits of this market share from non-organized sector to organized sector

Good to hear from mgmt that they don’t see slow down in mattress demand. Hoping that the next couple of quarters shows good pickup in sales due to wedding season.

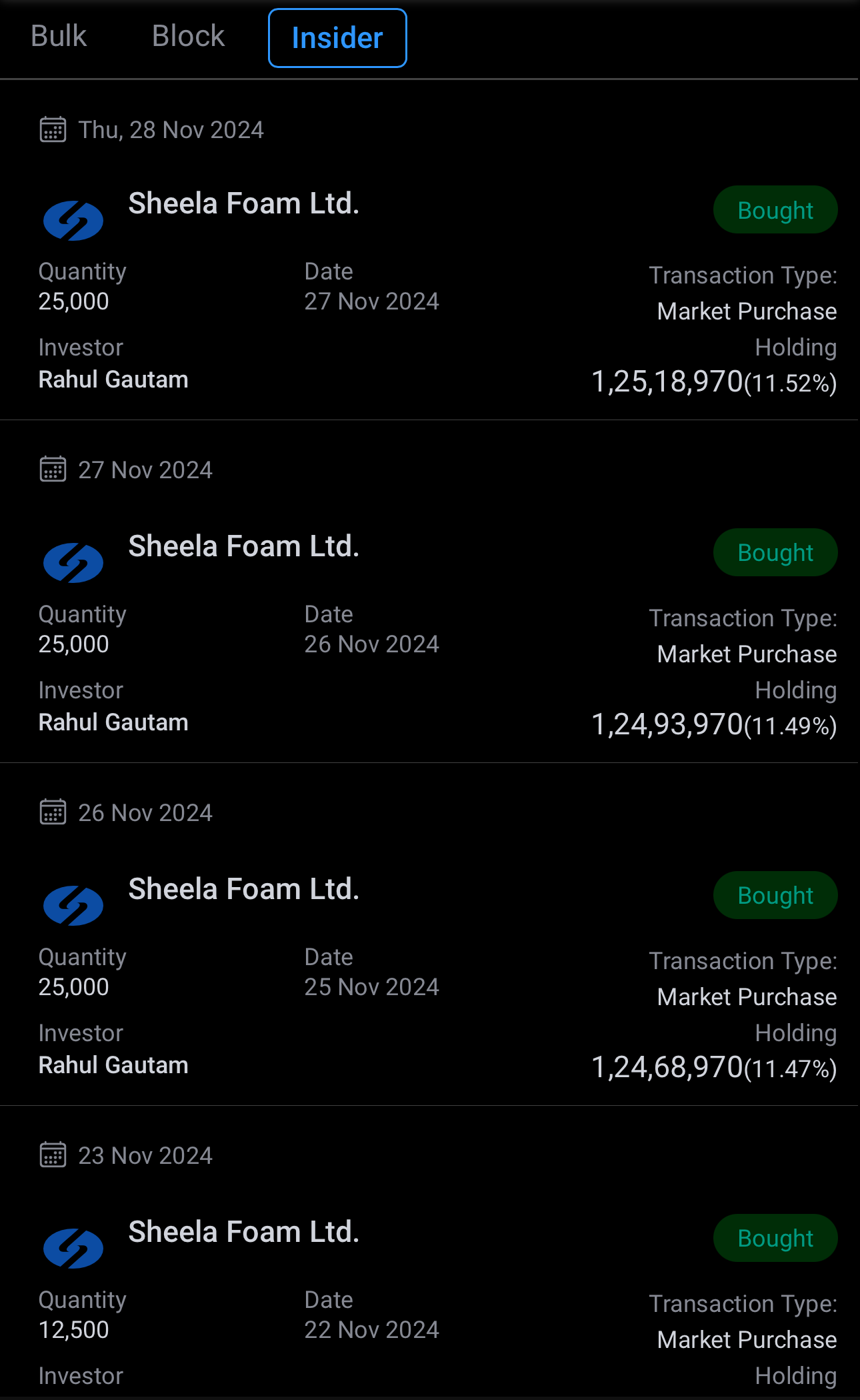

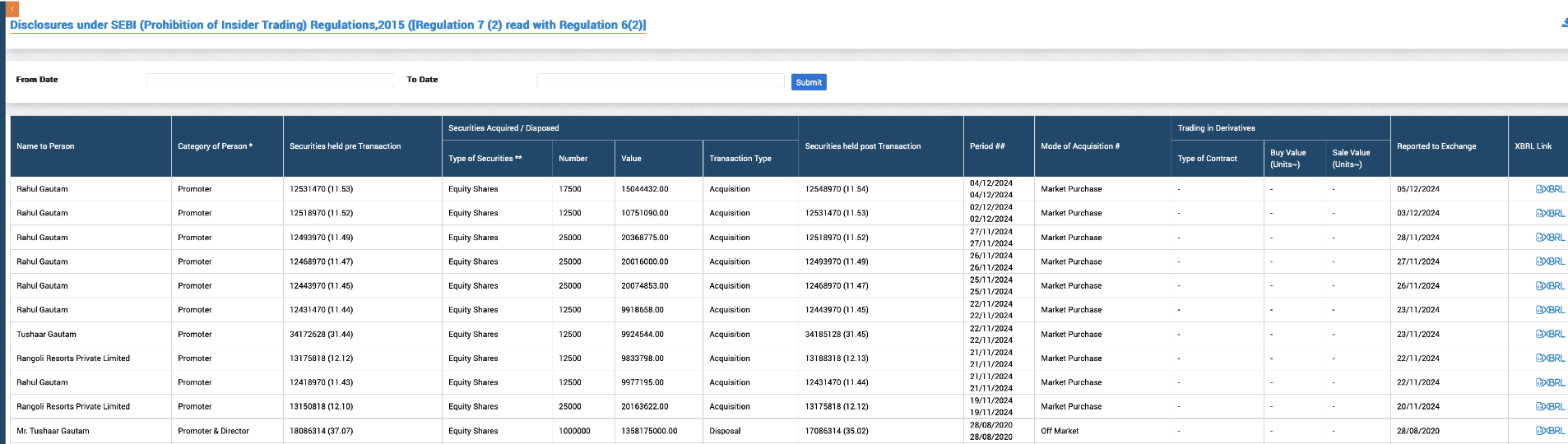

Sheela Foam’s promoters seem to be actively acquiring equity shares in the company, as per SEBI disclosures. Interestingly, the last major acquisition in 2020 was followed by a rally to an all-time high within a month.

Could this be a sign of bullish confidence from the insiders, or is it just a coincidence?

This post is purely for learning purposes and should not be considered financial advice.

Could you provide source link of this information

there you go:

Good read about Sheela form

Which app is this? @BejgamNishanth