But, kurlon as a brand has a pretty strong recall and customer instantly identify it with mattress.

In mattresses space, 3 most popular brands are -

Sleepwell

Kurlon

Century

Now with both brands (Sleepwell and kurlon) under the belt, sheela foam can make new strategic planning.

They might position kurlon as mid segment and Sleepwell being premium segment brand.

I recently visited HGH 2022 Mumbai Fair and sheela foam has largest presence.

They have 4 different booth, spread all over, each catering to different segment.

I never seen Sheela foam putting so much presence in any other HGH or other events.

Things definitely seems interesting over a long run.

–Last couple of weeks the demand has increased and the direction is upwards and its getting better

–Closely linked to TDI RM prices as of Q3 it stood at INR 243/KG which is lower than Q2 , where is it ? --The prices are down and its oscillating and its currently at INR 220/KG so there is a drop from Q3.

–Margins will improve and our products in B2B where selling prices are linked to RM prices there is +ve. The wedding side of the Biz , the contribution of TDI to cost of goods is much lower & therefore it will be a mixed bag and there is a lag between the impact of these prices on margins.

–Inorganic growth ? --co is looking to complete decision making for @FURLENCO acquisition in next 2 months which is a furniture rental co.

–Balance Sheet status ? --Reasonably healthy & we have some 750/800Cr cash on books and debt is relatively negligible but in some places it is there i.e Australia/Europe subsidiaries. Size for Acquisition is dependent on Acquisition but we dont need to borrow from anywhere. The acquisition will be much lesser than 500Cr. The said co is profitable on operating level but loss is there on the financial side. Revenues are 200Cr/year & it can go to 400Cr/Yr once we get involved

–Feather foam / starlight --these brands are primarily supplying to MBOs and all our sleepwell products are completely with the EBOs and there are large no. of MBOs which we have to address and its growing on a steady basis and its dependent on geos and MBOs we go after & it has higher growth as the base is small and universe is much larger.

–FY23 we will be single digit , what’s the outlook for FY24 ? --As of now growth will be 12/13/14% & Margins will be similar 13/14% EBITDA

the brand sees value in its physical presence: The “store is the best representation of our brand. It’s the best way to show all of our products. It’s the experience we can control in a physical way,” Arel said, pointing to the fact that almost 80% of mattress purchases are bought in a place where you can test them out.

Offline / physical retail can never get out fashion and most of the online only brands have to go offline in long run.

Here are some key takeaways from the Q2 FY24 earnings concall transcript of Sheela Foam mattresses:

Revenue growth: The company reported a 22% year-on-year growth in revenue, driven by strong demand for mattresses and other comfort products. The company also gained market share in both organized and unorganized segments.

Margin expansion: The company improved its EBITDA margin by 240 basis points year-on-year, mainly due to better product mix, operational efficiency, and cost optimization. The company also benefited from lower raw material prices and stable forex rates.

New product launches: The company launched several new products in the quarter, such as Sleepwell Signature, Sleepwell Cocoon, Sleepwell Spinetech Air, and Sleepwell Feather Foam. The company also introduced a new brand, SleepX, to cater to the online and value segments.

Outlook and guidance: The company is optimistic about the future prospects, as it expects the demand for mattresses and other comfort products to remain robust, driven by increasing awareness, urbanization, and disposable income. The company also expects to benefit from its strong distribution network, brand recall, and innovation capabilities. The company has guided for a 15% to 20% revenue growth and a 20% to 25% EBITDA growth for FY24.

Kurl-on acquisition: The company has acquired 94.66% stake in Kurl-on Enterprises Ltd. at an equity valuation of Rs. 2,150 crore. The deal is expected to be completed by December 2023. The management expects significant synergies from the acquisition in terms of product portfolio, distribution network, manufacturing capacity, and cost savings. The combined entity will have a market share of more than 50% in India’s organised mattress space2.

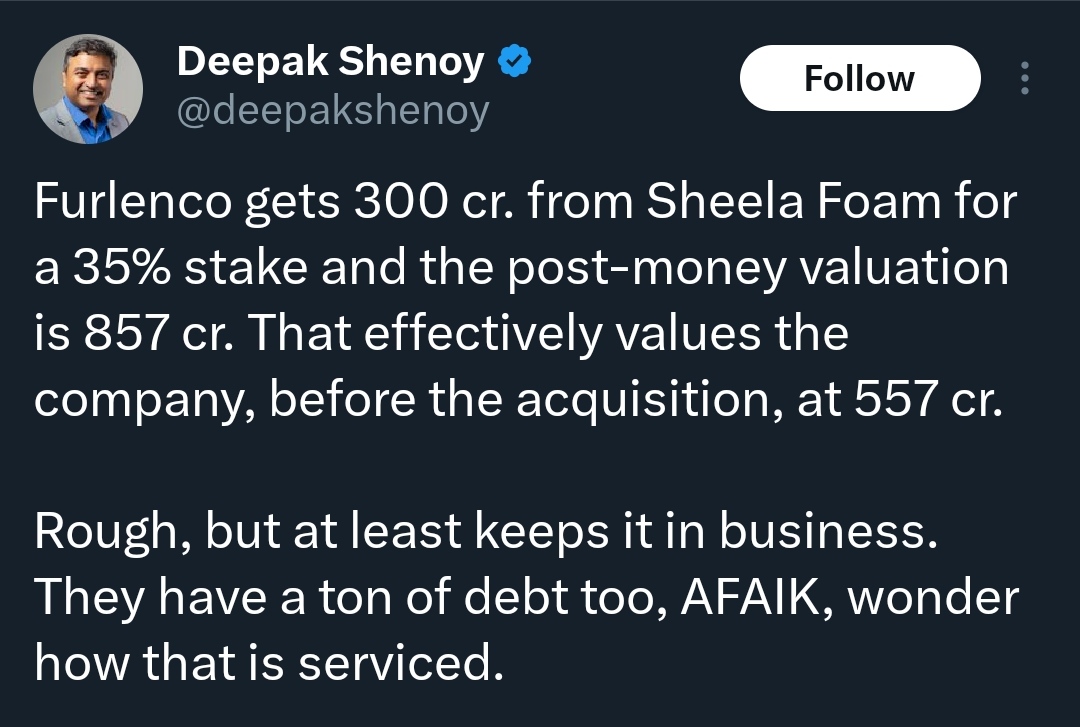

Furlenco acquisition: The company has acquired 35% stake in Furlenco, a furniture rental company, for Rs. 300 crore. The deal is expected to be completed by March 2024. The management believes that Furlenco is a disruptive player in the furniture industry, with a strong brand, loyal customer base, and scalable business model. [The company aims to leverage Furlenco’s online presence, data analytics, and design capabilities to expand its own product offerings and reach new customer segments]

sleepwell strong in north n west, kurl-on on east and south.

kurlon acquisition ramping up.

furlenco not yet PAT level profitable, will be by feb 24.

There are efficiencies or expertise of their respective companies.

Kurlon has a high level of expertise in rubberised coir, making those coir, which we used to buy from outside.

We manufacture foam much more efficiently than Kurlon. Approximately our yield is 10% higher to them.

We are able to service our customers from the nearest distance possible. So our freight cost is going down. So these are the things which definitely yield – would yield tangible benefits to the bottom line.

Sheela Foam has undergone a major transformation with the acquisition and integration of Kurlon Enterprise Limited (KEL), a leading mattress brand in India.

The management is confident that the fundamental business remains strong, and the disruptions caused by the integration process will be temporary.

The company is focusing on realizing synergies and cost savings from the integration, which are expected to enhance profitability in the coming quarters.

Strategic Initiatives:

Sheela Foam has undertaken a comprehensive integration of the Kurlon business, including manufacturing operations, sales and distribution, IT systems, and corporate functions.

The company has closed down two factories and optimized the distribution network, resulting in estimated savings of INR250 crores annually.

Sheela Foam is also strengthening its presence in the online and small-town India markets through new product launches and targeted distribution strategies.

Trends and Themes:

The Indian mattress industry is evolving, with rising consumer awareness and increasing demand for branded, high-quality products.

The company is focusing on premiumization and expanding its presence in the affordable segment to cater to the growing consumer base.

Industry Tailwinds:

The overall growth in the Indian consumer durables sector, driven by rising disposable incomes and improving living standards.

Increasing urbanization and the emergence of the middle-class consumer segment in small towns and rural areas.

Industry Headwinds:

The temporary disruptions caused by the integration process, which have impacted the company’s sales and profitability in the short term.

Competitive intensity in the mattress industry, with new players offering aggressive discounts to gain market share.

Analyst Concerns and Management Response:

Analysts are concerned about the significant drop in Sheela Foam’s Q1 FY’25 revenues and profitability, which they believe is not in line with the company’s earlier guidance and market expectations.

The management has attributed the decline to temporary disruptions caused by the integration process and assured that the situation will normalize in the coming quarters as the integration is nearly 85-90% complete.

Competitive Landscape:

Sheela Foam is the market leader in the organized mattress segment, with its flagship brand “Sleepwell” enjoying a strong brand equity.

The company faces competition from other organized players like Kurlon, Nilkamal, and several regional and unorganized players.

Guidance and Outlook:

The management has provided a guidance of double-digit revenue growth and EBITDA margins of 14-15% in the next 3 years, driven by synergies from the Kurlon integration and expansion in the small-town and online markets.

Capital Allocation Strategy:

Sheela Foam has been conservative in its dividend policy, preferring to retain earnings for growth initiatives and acquisitions.

The management is evaluating the possibility of increasing its stake in the recently acquired Furlenco, a furniture rental platform.

Opportunities and Risks:

Opportunities: Expansion in the affordable mattress segment, growth in the small-town and rural markets, and further consolidation in the fragmented industry.

Risks: Sustained disruptions from the integration process, continued competitive intensity, and any adverse changes in the regulatory environment.

Regulatory Environment:

The mattress industry is subject to standard consumer protection regulations, and there are no significant changes in the regulatory landscape that could impact Sheela Foam’s operations.

Customer Sentiment:

The company’s flagship brand “Sleepwell” enjoys a strong brand loyalty and customer preference in the organized mattress segment.

The management is focused on addressing the concerns of the traditional cotton mattress users in small towns and rural areas through innovative product offerings.

Top 3 Takeaways:

Sheela Foam’s strategic focus on integrating and realizing synergies from the Kurlon acquisition, which is expected to enhance profitability in the medium term.

The company’s efforts to expand its presence in the affordable and small-town India markets through new product launches and distribution strategies.

The management’s confidence in the fundamental strength of the business and their guidance of double-digit revenue growth and improved EBITDA margins in the next 3 years.

@nikhildoshi please throw some light on how you see seasonality in this business, especially Kurlon and sleepwell is catering mainly in opposite geography. As Sheelafoam roamed here and there after listing few years back and coming back to almost same level makes this good opportunity to invest.

Although from entirely different product segment, Symphony which is air cooler market leader also struggled with sales from 2016-17 till last summer which was blockbuster and resulted in mojo back.

Disc: invested couple of days back expecting good festive season

[quote=“PraveenKG, post:123, topic:8456, full:true”] @nikhildoshi please throw some light on how you see seasonality in this business, especially Kurlon and sleepwell is catering mainly in opposite geography.[/quote]

I don’t remember when I said that. Can you please point that out? I will try to find the any specific context for that

Yes, I am adding Sheela foam regularly.

Sorry, not tracking symphony.

But, they have started big on commercial air coolers (used in marriage hall or large places) and they have good products. I bought 4 of those commercial coolers