In the name of value investing , lot of noise is being made . As per Benjamin Graham in his book : Intelligent Investor - the first tenet of value investing is to look for any share quoting less than its net current assets per share ( Current Asset - Current liabilities/total number of shares). His wisdom was that when a share quotes less than its current assets, you are literally getting their fixed assets free of cost.I wondered whether such situation practically would exists. But surprisingly yes ! I was holding the shares of MPS . At one point of time ( prior to take over by the current management) , shares were quoting less than net current asset per share . But I did not have the conviction to buy more . Rest is now history . From low of Rs. 50 , it touched more than Rs.1000.

I tried to check any such share quoting less than current assets per share in the screener.in link but unable to extract. Seeking help from the members on how to extract this info i.e. shares quoting less than their net current assets.

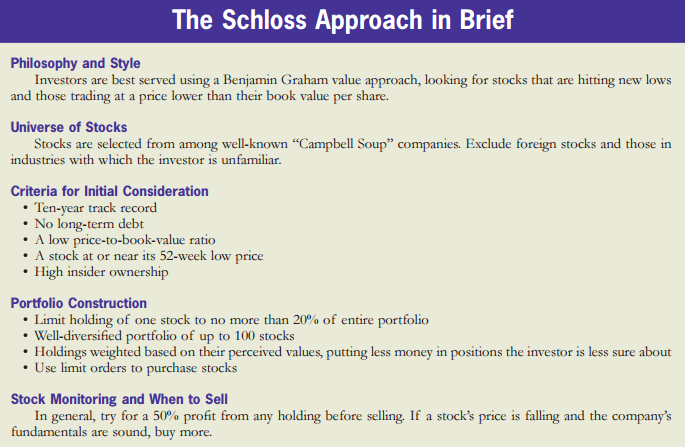

While this is a great start, let me also tell you a few more things which you should be aware of.

Graham operated in the US where shutting down a company and liquidating the assets takes about a week or so. In India it doesn’t happen at all. The laws are not favorable and workers will not let any plant shut down, period. So while the current assets are more than the entire firm, the value unlocking doesn’t happen at all. So following Graham’s formula requires some more work in India.

Contingent liabilities can suck up all the current assets and then some

A malicious promoter can clean up all the current assets and then some (example: where did the cash in Treehouse go?)

If the co is a micro cap (say below 50Cr in value) you run a risk of the co being undervalued for a long long long time. Why/how this happens I can’t explain but it does happen in Indian markets. (This mystery is on par with dramatic undervaluation of DVR shares in India)

Having said that, don’t let this discourage you. I’ve made a decent chunk buying cos which were significantly undervalued in relation to their current assets (e.g. Indian Toners, Divyashakti Granites, Trigyn, Madhav Marbles, Prima Plastics, Virinchi and so on). So yes, it’s possible, but the big caveat is that you should not skip reading the last few annual reports cover to cover and if there is any doubt then just pass.

Disc: Long some of the stocks mentioned above at a significantly lower valuation

Do agree . I have already posted a thread on Tata motor DVR quoting far less than Tata motors for a very long time. This paradox proves once again against EMH ( Efficient Market Hypothesis) theory . Well, one day , market will recognize this difference and DVR may quote very near to the main share ! . Trust we should accumulate till such time.

As regards your portfolio on shares quoting less than net current assets, keen to know details on how you picked them and how they are faring .

Price / Sales is ridiculously low (compared to rest of the industry)

EV/EBITDA is very low

Very bad news but it’s clear that there are no long term effects (e.g. Eros)

Stock has dropped 30 or 50% below 52w high for no apparent reason, the fundamental business model is intact (buy on dips strategy) (e.g. CARE rating)

Regardless of all these, you must remember that

Never buy when market is expensive (e.g. now, PE > 24). Patience is a must.

Never ‘reach’, i.e. never settle for something that does not meet your criteria simply because other opportunities don’t exist

Book profits at every X% rise in stock price or at certain targets. This is necessary because most of these cheap companies have some flaw (hence they are cheap) or have no moat as such. Even Graham said that you should exit at fair value. I part-exit at 40% rise from my buy price but that’s not set in stone. But also see next point …

Let the winners run. Leave some room for a ‘positive black swan’ event. Maybe one of the real bad stocks of today turns out to be a 100 bagger tomorrow.

I don’t put all my money in at once. I start with 1% of my portfolio and will average down every 30% fall. This is of course if the facts do not change, if they do, I’m glad to book a loss and move out. At the max I’ll only have 5% of my pf in one of these statistically cheap stocks and I don’t go beyond 20% of my pf including all statistically cheap stocks. Remember value traps are real, you will end up with a few losses and the worst enemy is you. At some point, you need to realize that throwing good money after bad is a waste.

No company ever went bankrupt if it had no debt. I strictly avoid cos with lots of debt. Strictly.

Keep an eye on diversification. You’ll find periods when for example all metal stocks look cheap. No need to buy them all.

You’ll still miss quite a few stocks. The mistakes of omission will always be more than mistakes of commission. (At least this has been my experience)

Here’s the history of all my cheapskate trades (including ongoing ones). Notice how buys happen in bursts and exits also happen in bursts. Haven’t made a buy in a while now but hoping to exit some more…

As the Byrds sang: There is a season, turn, turn, turn

I have checked few of your stocks and found that they are not selected on basis of " less than net current assets per share ". Is my understanding correct ?

Yes I just go for statistically cheap cos, not necessarily net nets. For reasons I mentioned above, I believe that the lure of net nets is not applicable to Indian scenario.

I was going through this thread and just wondering do you have an updated spreadsheet list which you shared in August 2016?

In fact, I found the list useful and if you could share the most updated one that would be greatly appreciated? Additionally, I have one qn on Voith which I will ask separately.

Haha yes, it has been a phenomenal ride indeed. I haven’t sold any of the holdings after booking part profits so they have continued to give me very handsome profits over the last few years. My ‘active’ holdings have reduced to a trickle now, which is to be expected at such high valuations, and I’m sitting on a fair amount of cash.

Haven’t maintained an xls but I diligently maintain a portfolio online. I’ll see if there are significant changes but I doubt if there are major ones. I haven’t added much because things are not very cheap nowadays (d’uh stating the obvious). Of the top of my head a few trades have been - added to my Tata Motors DVR below 220, bought Ashok Alco Chem around 80, Cochin shipyard bought IPO (BTW it’s very rare I invest in IPO) and part profits booked at 40% upside. I’m also invested in Selan Explorations around 182. Of my current active holdings I think Tata Motors DVR and Selan are highest conviction bets (time frame 3-5yrs or more). Yes I’m aware that Tata Motors has a higher d/e ratio than that I normally prefer but I’m ok to make this compromise for a Tata Co.

Broadly speaking I’m extremely comfortable with the Schloss method and I think my biggest win in this bull run hasn’t been just the money but the discovery of a method that suits me well and gives me handsome profits as well and which I can stick to for years.