This news was not reported to the exchanges and upon seeking clarification the company has apologized!

Apparently this is their first successful patent and there are 28 more in the pipeline.

The problem of course is tender price vs commodity cost squeeze, and the fact that KUSUM scheme does not seem to have targets but is end-user/farmer demand driven. Though diesel pump-sets will be really expensive to run in comparison.

DC motors are the most efficient variety, using magnets instead of dual-windings (stator+rotor), hence their auto traction motors may start to sell if they work as good as their pumps.

Today AAP govt declared free 300 units of power to all in Punjab from 1st July. If this experiment (they have done it in Delhi but Punjab will be their first real test) succeeds, it will potentially impact sale of solar pumps negatively.

As per management commentary margins will be range bound as KUSUM 2.0 is fixed contract project. As KUSUM 3 will launched in next calendar year we can expect similar margins in next 3 quarters also.

Sales have improved however inventory and receivables have also increased significantly.

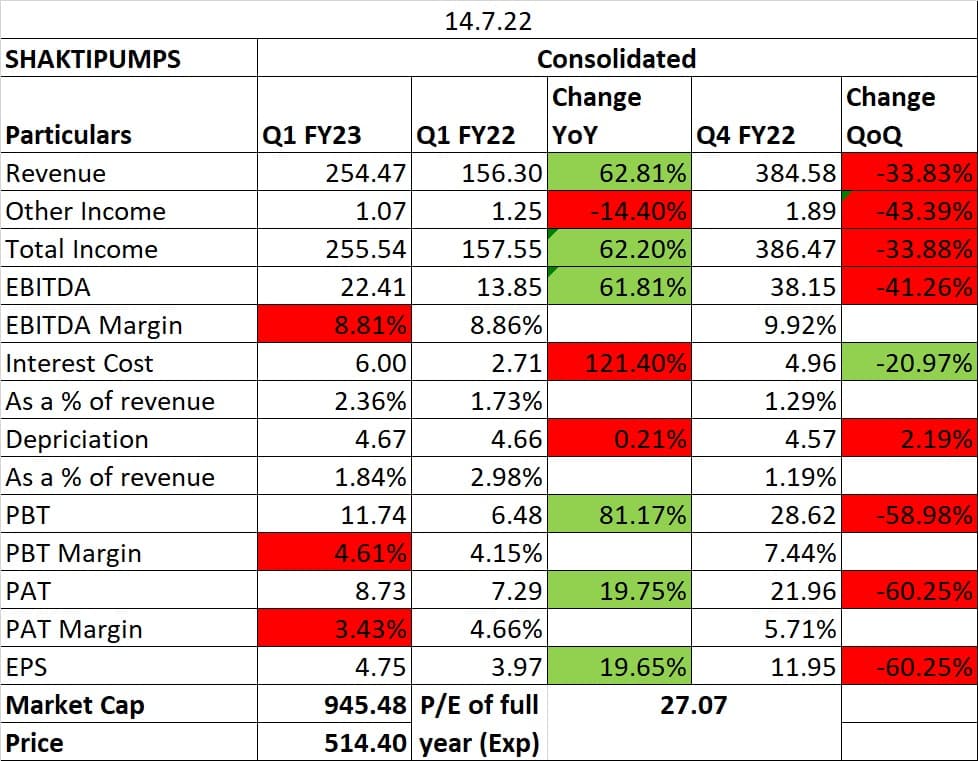

Results are below expectation… Margins have come down to 8.39% and guidance is 10% for the full year which is below earlier guidance of 15%.

Kusum scheme is yet to pick up across the state…

Shakti Pumps currently for revenue is completely dependent on Kusum Scheme. Which should get over by 2024-25. Exports and retail is still not a very huge part of revenues. Sustainability of revenues is still a question.

The Risks are known and reflected in the valuation. However If one does take the risks (Govt Business tends to be Lumpy and high working capital oriented, but Large volume and predictable!) then the story has just begun to unfold as the KUSUM scheme has large Ambitions and interestingly very willing stakeholders too!

The Co. has demonstrated 45% share in the Pilot project through farmer demand which is commendable.

Just noticed their other Investor Presentations and observed that the company has never given Management Commentary in their Presentations. Giving it this time is a testimony of the fact that the company realizes the panic these dismissal set of numbers can create and as such the company has tried to make its shareholders’ informed about the reason for the same. These is good practice and protects the investors from misrepresentations.

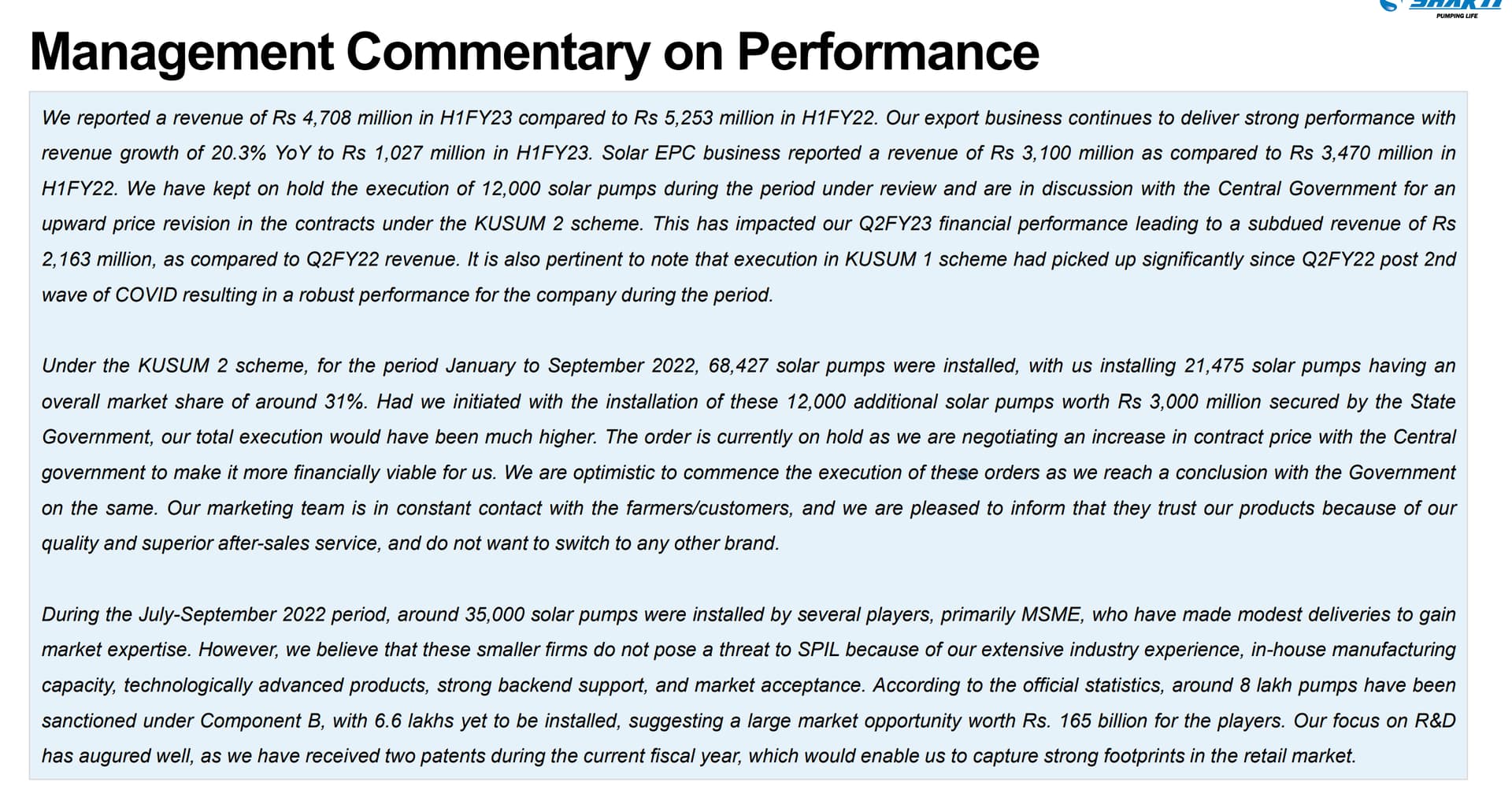

As per the commentary, the execution of 12000 pumps would have added a magnitude of Rs. 300 Cr to the revenue. So, once the order is executed we can see a good quarter hereafter.

Q3 is also going to be a wash out… The promoters did not have any answers for their performance in Q3 as they are not undertaking KUSUM project and secondly there is no clarity on Uganda order due to price escalation clause. Q3 is expected to be worse then Q2. So next trigger will be in Q4 only whose results will come in April. Till that time the stock will consolidate at this level or even fall further.

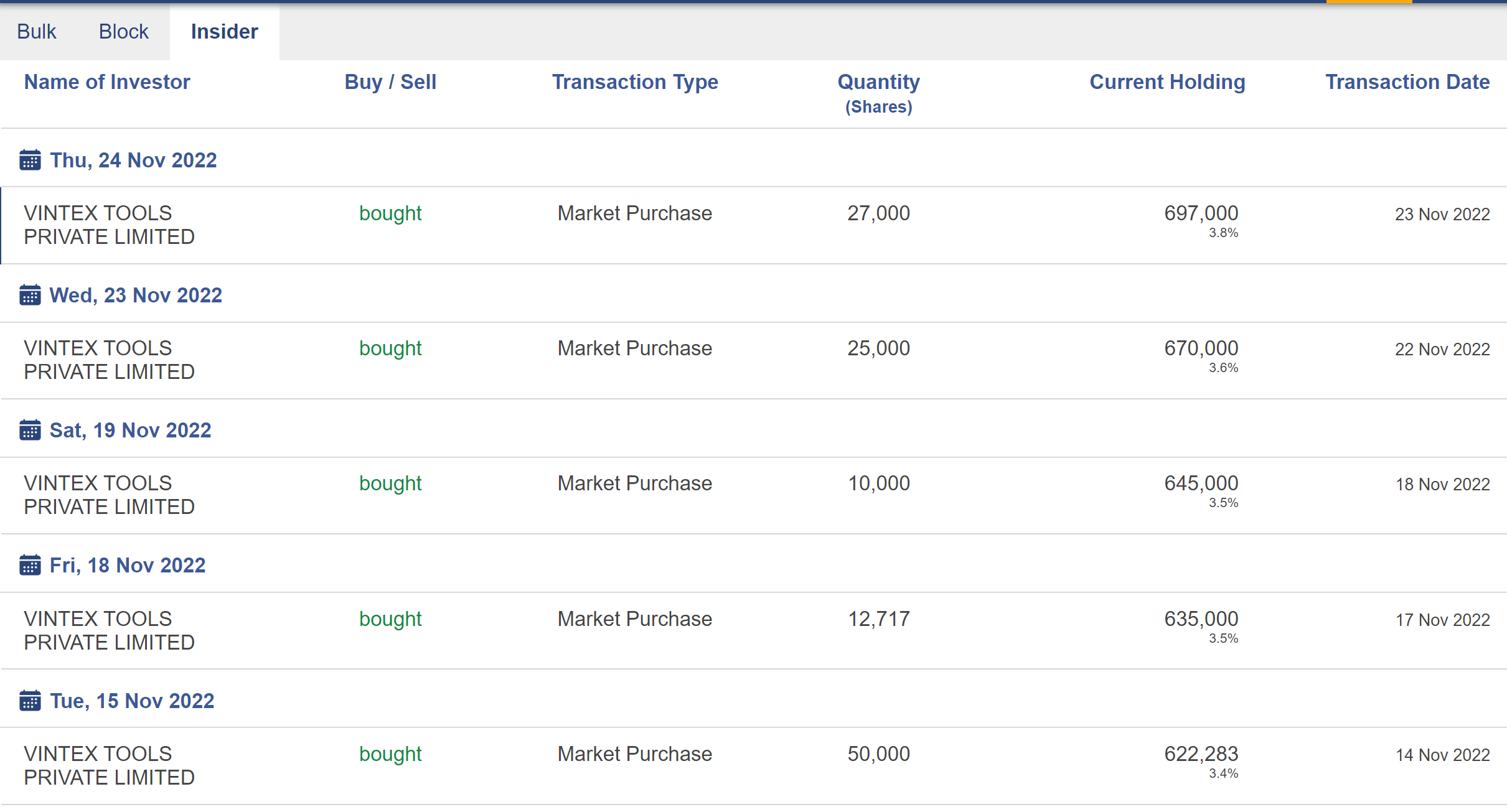

Shakti Pumps Insider Acquisition: From Feb 2022 to 29 Nov, 2022, total acquisition by Directors/Promoters or Promoter Group is of about 214041 shares (approx 9 crores) which is about 1.21% of full market cap and 2.7% of floating market cap.

Shakti Pumps Insider Acquisition: From Feb 2022 to 27th Dec, 2022, total acquisition by Directors/Promoters or Promoter Group is of about 244041 shares (approx 10.15 crores) which is about 1.37% of full market cap and 3.05% of floating market cap.

Strong Growth seen in Solar EPC ad export business. Major contributor in export business is USA. Revenue is up by 24.5%. Main supply in USA is of water supply pumps and have started selling solar pumps. Kusum Business in this quarter is 223 crores.

-

Margins remain subdued due to high input costs. Margins are low as solar pumps prices have increased.

-

With the ongoing challenges, there are few positive developments under the PM-KUSUM Scheme. The Solar Energy Corporation of India Limited (SECI) has issued new tenders for over 6.66 lakh solar pumps in the month of December 2022 and bidding for these new tenders is expected to be completed by March 2023. Orders will start coming in Q1 FY24. (Check order intake of Q1FY24)

-

They have strong presence in states like MP, Rajasthan, Haryana, and Punjab. 5 lakh pumps requirement is only from these states. They will be able to achieve 30-35% Market share.

-

Shakti Pumps and Tatas are only eligible for giving tenders in all states as there’s a requirement of selling 40000 pumps.

-

Will get better rates than KUSUM scheme as eligibility criteria is a little stringent and better for organized players.

-

Varied Range of Applications: Solar, Agriculture, Industrial, Commercial, Domestic, Sewage and Drainage.

-

Capacity utilization is very low only at 30%.

-

R&D setup: For the whole company, we have 150 R&D engineers working. We have done very good job in this power electronic space. We have developed a VFD Solar Controller, Solar Invertor and our motors are very good efficient motors. Worldwide, we are also in good position, as you can compare our motors with any Japanese motors.

-

Haryana Govt order which is on hold will start to get revenues in Q1FY24.

-

Shakti Green Co. will start operations after FY24. Motors are still in testing phase. Planning to launch EV motors and controllers.

-

Order for Uganda will start execution in Q4 or Q1 FY24 as payment is pending from the government.

-

In Q1, they suggested revenues will grow 25-30%. But doesn’t seem to be the case looking at 9M results.

Business is largely dependent on government orders of solar pumps. For the past year and a half because of raw material price increase business was not sustainable. It was not executing the current order book at hand leave alone new order. It was waiting for price increases and new rates have come this quarter.

The current order book of the government for the next two years is 24,000 crore and 8,000 crore is up for grabs for Shakti as per the concall. Business turnarounds Q2 Fy2023 as per concall. But management clearly said they will talk next year what they can achieve. They surely have the capacity for doing 3500-4000 crore a year. Management talks about double digit margins. If you look at past history margins are 14-18 % in the best of times. So you are talking Fy25 with 4000 cr revenues and with a 12.5% margin you are looking at a PAT of 350cr in the best case scenario. Exit PE of about 12. Clearly looks like a 4x opportunity in the bestest case if you know what I mean.

I would highly suggest listening/reading to the latest concall for a clear understanding of the market size and shakti’s share in the same. Here is the link - Concall Q4 FY22-23.

Market is smarter than us …we are focusing on Q4 results and it seems market has started discounting Kusum 3.0.

As per latest Concal ,this time management commentary is a bit conservative and they are not committing on any numbers.

I had exited all my positions in Nov 21, however was tracking the Company and KUSUM scheme.

Kusum 3.0 is very big oppurtunity and it can completely rerate the Company and upward potential is 3x to 4x. However, we need to wait and see the same reflecting in numbers.

One good thing is that Company is conscious of taking project and is not only after topline growth. It undertakes projects where there are better margins and realisation. The Company had forgone the Haryana order of Rs 500 Cr last year as the margins had squeezed due to higher Raw material prices.

As per Q4 investor presentation:

"It gives me great pleasure to announce that the Solar Energy Corporation of India Limited (SECI) has sanctioned the issuance of new tenders for approximately 8.57 lakh solar pumps under the PM-Kusum scheme III, and Shakti Pumps has qualified in 21 states to provide Off Grid Solar Photovoltaic Water Pumping Systems. As the bidding process has concluded, we expect orders to be received from various states in the next 1 month. The major states,

including Maharashtra, Haryana, Rajasthan, Madhya Pradesh, and Punjab, make up 80% of the total requirement mentioned under the current tenders in the KUSUM scheme. As we are one of the largest solar pump manufacturers in India with a market share of around 30-35% in these major tendering states, we are optimistic about securing substantial orders, which will help us in the robust recovery of our Solar EPC business. Our in-house manufacturing, technological capability, experience, and strong product recall give us an advantage over our competitors.

Company and management is good however there is always an element of risk and uncertainty in B2G business.

Initiated tracking position today and will allocate further depending on the developments of Kusum Scheme and number reported by Company.

Technically: There seems to be be a rounding bottom formation and break out with higher volumes.