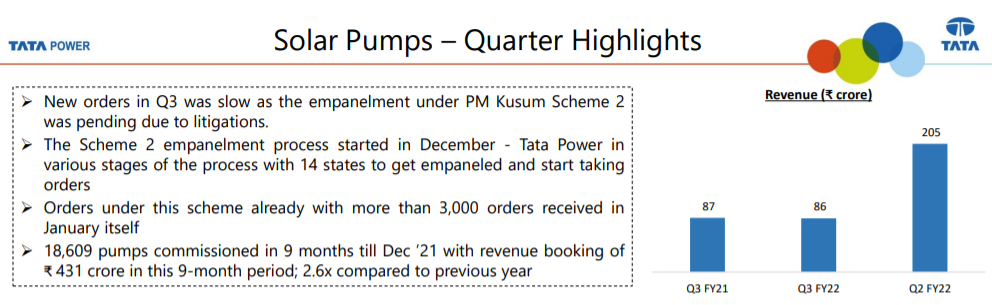

A point to note is that in Q2, the management has claimed that they will do 2000 cr revenue, where as in Q3 they did less than half that amount!

Does this mean that the management’s word can’t be trusted?

Disc - Planning to invest

A point to note is that in Q2, the management has claimed that they will do 2000 cr revenue, where as in Q3 they did less than half that amount!

Does this mean that the management’s word can’t be trusted?

Disc - Planning to invest

For sure, management word cant be trusted

they have been silent/not been upfront in communication on many issues

including

stuck of tender in courts and outcome

not sharing that Kusum 2 is under suspension and not started ( while we all in dark expecting 400 -500 cr revenue or more this quarter )

Disc. Invested based on opportunity size and management talk

Exited now based on management only --opportunity size still remains huge —execution is big challenge --they have lost the first mover advantage

Is it planned by some other player !! I am just pondering

Can you share the source for this that its extended run of Kusum1 and not kusum2

this shows that supply will start from 1st week of september

So definitely management has been silent or not forthcoming proactively on the status

Stock is violently moving in hands of operators ( else retail can not drive that price movements alone --that too without any news on some of observed days)

Any update on concall

Maybe I am not upto date with the developments or confused myself!

This below shows govt chose to delay the sanction for KUSUM 2. (it mentions centralized tenders 1 and 2)

Shakti quite optimistically (mis)guided for process to normalize by September.

disc: invested, was biggest position, have been reducing as story is slow to realize

You can find the concall audio on researchbytes website. Here is the link Researchbytes.com (If this doesn’t work, you can login to researchbytes website). Management said KUSUM 2 orders have finally started to come in January first week.

As mentioned earlier, i dont think Management’s word can be trusted!

In yesterday’s call, management has guided for 30-35% topline growth with 12-13% EBITDA margin. They were honest to say that they have committed higher numbers in the past and would not like to do that same mistake again. (But did same mistake of laying out goal of Rs 5000 Cr topline by 25-26 :-  ) Since they don’t control many things like govt tendering timeline, size of the tender, legal hurdles etc, I feel we need to discount any number and timeline thrown by the management.

) Since they don’t control many things like govt tendering timeline, size of the tender, legal hurdles etc, I feel we need to discount any number and timeline thrown by the management.

My first impression about the management is that they are bit raw(and ambitious more than they can deliver) and hence get into trouble by giving hope to the investor community .But I did not feel like they are fraudulent and doing it on purpose. My investment thesis is based on their capabilities (exporting to so many countries) and tremendous growth potential of the solar pump business globally. Their EV motor venture , if successful, can be cherry on the cake (but I doubt!)

Disclosure - invested after listening to the concall yesterday

Do you guys feel EV is Deworsefication and takes away management bandwidth in highly competitive segment

i have so big pie available 5000cr --and i want to change my focus to new pie

why not rather i focus on optimizing my existing pie to full and focus to kill out competition ( assuming i am the biggest manufacturer and others take it from me)

I still need to go through concall though

May you please explain in a little detail what made you invest in the company?

Thanks

• Shakti Pumps conducted the conference call for Q2: FY22 "With KUSUM mgmt guides to grow at 30-35% YoY in coming year Here are the conference call highlights.

• Business Updates: • KUSUM 2 sales has been started and will be seen in Q4. • Received order book of 100cr in Jan first week. • With increase in EPC product mix, margins impacted a bit. • Mgmt expect the Raw Material prices to reduce further. • Capacity Utilization: 40%

• KUSUM: • Total Market of KUSUM 2: 3,17,000 - Addressable Market: 1,50,000 • Shakti Pump is already present in 22 states, being leader in states such as Haryana, Rajashthan, MP, Maharashtra • Price Hike done in KUSUM 2: 3-4%. • Bank Guarantee of 3% has to be given.

• Export: • Co. will explore other country prior to having experience in delivering the pumps in the current market covered.

• Margins: • Mgmt expects margins to increase in coming quarter. Guidance for margin - OPM: 12% - PAT: 8-9% • From last year, margins got reduce because of initiative in entering KUSUM business. Now RM prices are increased but not prices, hence due to competition margin reduced.

• Expansion in EV: • Opened new co. name Shakti EV pvt ltd. (EV Controller, EV Motor, DC charger- In focus to manufacture). • Business will be started with manufacturing of Motor & Controller. Competition: Mainly in Valsad. • Co. will 250cr in coming 5 years in this subsidiary.

• Raw Material: • For Solar pump, mgmt don’t thinks any raw material supply issue from Adani side. Competition: • Adani is also entering for solar pumps. However mgmt feels market size is big and addition of 2-3 players will not impact the industry much.

• Other: • For EV business co. has applied for PLI scheme where new facility is created. • Pumps price is for 2,50,000 for size of 5-10HP pumps (Key focus area of Shakti Pumps) • Took step for digitizing in pumps selling by starting an app and website for it.

Concall for Q3 FY22:

Due to the promoter’s extra optimism, sometimes it makes me question if they are really saying the truth or not. However, Tata Power has made the same arguments in their IP. They have also started to receive orders from January and were stuck due to litigation. This sort of makes me feel comfortable in owning Shakti Pumps.

Does anyone know the export profile of this company? I see the stock price has been falling very steeply with the start of the Russia - Ukraine conflict. The fall has been quite steep compared to other companies (even with exposure to these countries e.g. Dr Reddy’s has fallen <10% with ~10% export market to Russia) or overall market fall. Does it have any heavy export orientation with any of these countries. Sorry this info may be there in annual reports/other reports/mention in concalls but i could not get time to look at those, hence asking here.

it is falling in its natural course of correction

Margins of the Company were already under pressure in Q3due to increase in Steel prices. During Q4 steel prices have further increased which will further impact the margins.

Yes, the margins will surely be impacted. However, I feel tracking revenue might be a better option right now. Since KUSUM 2 program was supposed to start in January, its impact should surely come in the form of increased revenue. We would have to look into margins in further quarters.

The Company will have to rethink on its existing export orders as well as Kusum tender as Commodity prices have gone out of roof…

The Company seems to be very weak on technical charts also and is likely to test its support level at Rs 400.

Disclosure : Exited all my positions after Q2 results Concal