Kenneth Andrade - old bridge capital - exited the stock in July to Sept 2020 quarter

Disclaimer - Never invested in it (educational interest only)

Kenneth Andrade - old bridge capital - exited the stock in July to Sept 2020 quarter

Disclaimer - Never invested in it (educational interest only)

Very good set of numbers by the numbers… As already discussed the Company has now started reaping benefits of KUSUM… I anticipate that this is just the beginning and the growth story is expected to continue for at least next 2 to 3 years…

The management is also hosting a conference call for its investors…

One great thing about the management is that although the Annual sales of the Company is in the range of Rs 360 to 600 Cr , it continues to make conference call with investors. The company has been continuously conducting a Concal for the last many years.

Also another thing is that apparently Promoters are net very conversant in speaking English, however they reply to all queries satisfactorily in Hindi. I have not seen concal in Hindi in any Company…

The promoters seem to be commited to their buisness and they are very well aware of what they are doing…

How does Shakti pumps compare to Kirloskar brothers. I had created a thread with some content on Kirloskar brothers. People who has done industry analysis can share their views.

Disc: I own Kirloskar brothers.

Shakti Pumps Q3 Conf Call

Huge Opportunity getting created in Solar Pumps through PM-KUSUM scheme for farmers

Shakti Pumps will be major beneficiary of the same

The revenue to reach 5000Cr by 2025

Operating Leverage to kick in with new orders

Disc: No Investment… started tracking recently

Transcript_Q3_2020_21 (2).pdf (126.7 KB)

Shakti record profits, PAT 30.5 Cr, compared to prev qtr. 26.5 Cr, best ever, as expected! 75% of TTM PAT.

YoY comparison here:

Disc: invested

Comparison of FY 2020-21 vis a vis FY 2019-20.

Sales have increased considerably from Rs 386.91 Cr to Rs 929.66 Cr i.e growth of 240% on YOY basis.

EBIDTA has increased from Rs 16.33 Cr to Rs 145.81 i.e growth of 792% YOY basis.

Net profit increased to Rs 74.94 Cr as against loss of Rs 14.30 Cr.

In spite of increase in revenue, financial cost has reduced from Rs 20.79 Cr to Rs 16.79 Cr

Long term borrowing is only Rs 19.91 Cr which has come down from Rs 26.11 Cr a year ago.

Short term borrowing has also decreased substantially from Rs 158.38 Cr to Rs 69.70 Cr.

Recievables increased from Rs 125.26 Cr to Rs 264.56 Cr. i.e as against revenue growth of 240% receivables have increased by 111% only , in days term it has come down from 118 days to 104 days i.e improvement of 14 days.

In spite of increase in revenue inventory levels have come down from Rs 144.55 Cr to Rs 133.40 Cr i.e inventory turnover ratio has improved from 2.67 to 6.96.

So over all there is improvement in all parameters from i.e Sales, EBIDTA, EBIDTA margin, Net Profit, Financial cost, decrease in borrowings, improvement in receivables holding period, inventory turnover ratio. The Company has major orders from Government however the Company is cautious of its working Capital cycle which is evident from improvement in receivable days and inventory turnover ratio.

The Company had advised during last Concall that it is presently operating with 60 to 70 % capacity utilization so with operational leverage coming in play we can see further improvement in operating and profit Margins. Even at the current run rate, the Company sales growth will be more then 35% in FY 21-22 in comparison to FY 20-21.

Apart from this the Company has also declared dividend of Rs 8.

With the KUSUM scheme these figures seems to be benchmark figures for future. The Company is also finding good traction in EXPORT market with more than Rs 250 Cr export orders in hand.

Management seems to be committed and do frequent interactions with investors through Concall.

Overall a very good set of numbers for FY 20-21 and in my opinion the stock is probable candidate for re-rating.

Disclosure : Invested since 2018 and 10% of my portfolio.

I very much respect the outstanding financial performance of the company and I am invested too. Although, I have few doubts if someone could clarify or even ask the management, if possible.

The increase in receivables could be easily understood since they are working with state governments. However, in the Q3 call, they said we would only take orders considering cash flow in mind. So, this substantial increase should not be a long-term trend right?

Since there is an insane opportunity available with the company currently, why are they not at all focussed on Capex instead of giving out dividends and paying out loans (this is fine, but considering the opportunity, they should be focussing on growth)?

Also, it’s commendable and a bit fearful that their entire CFO would have been near to zero if they didn’t have such an increase in payables (commendable because in the last call they said they have increased creditor days because of increased volume of orders)

Who are the other major players in Solar Pump and why other pump manufacturers (Kirloskar,KSB, ROTO WPIL etc) are not so gung ho about KUSUM. Is the company having any edge or moat for KUSUM.

I guess you are ending your post with a question? Maybe you should know answer since invested with big allocation for sufficiently long?

My guess is that, Roto and WPIL are not in the category of energy efficient submersibles. Kirloskar and KSB have more diversified product portfolio, but can provide competition. Shakti openly claims to get 50% of KUSUM orders, so far and even in forecast, and that they work on advising govt how to make the tendering better (some political leanings?). They even claim to refuse orders from ‘bad’ state govts. Though KUSUM has upfront payment from time the work is approved. They acknowledge MSME quota in tendering but claim these cos struggle to fulfil the tenders. MSME will anyway only work as assemblers since pumps will be sourced from one of the main manufacturers.

Mystery is indeed the capex plans.

Disc: invested

Thanks for the answer!!

Yeah, I forgot to see receivables in terms of days instead of absolute terms (since there has been a big jump in sales too)

I do know that utilization has been around 60%, but since the management told in the call that “This is sort of a pilot project for us,” shouldn’t they be spending more on developing capacities for the upcoming bigger growth for them. If they don’t do it, others will, and they won’t be able to meet demand. (They are spending 14 crores on dividends, while spending 12 crores on PPE)

As @vikas_sinha said, “Mystery is indeed the Capex plans.”

Yeah, the cashflow needs to be monitored as growth comes along.

The company said in its call that the biggest advantage they have is the experience of efficiently completing the tenders, so they get a preference in that terms.

Also, you guys are not considering one of the biggest competitors in the listed space, Tata Power. Shakti Pumps installed around 13000 solar pumps in first 9 months, while Tata Power is behind with around 13000 solar pumps in FY20-21.

Regarding points raised:

#2 they might have plans for incremental capex from what I may recall, so not big bang, but addition of capacities within a year or so, of about 20-30%. They said max run-rate is ~350 Cr per qtr, so they will touch 100% this year looks like as expected by mgmt also. They may have visibility of tendering and see capex requirement sufficiently in advance.

#5 Tata power solar is good, but they focus on all things solar, pumps is only a part and I am almost sure they would be not be manufacturing pumps inhouse.

Shakti does most manufacturing in-house, except solar panels, which is partially done only. They make control panels to pump, the whole package and do the installation work. So almost 100% package for solar.

Disc: invested

Shakti Pumps plans expansion, pins hopes on PM-KUSUM scheme - The Economic Times.

@Rushil_Shah : Tata Power is a big player however they do not have any pump manufacturing capacity.You are right that for grabbing such big opportunity the Company needs to focus on CAPEX and investors would be rather happy even if they do not distribute dividend provided they are prudent in Capital allocation.

Any body attending Concal should definitely ask question to the management regarding their future Capex plan and also that present Capacity can scale the sales to what levels. Quantum of Capex required for doubling the sales from this level.

@vikas_sinha : I couldn’t find the answer as submersible pumps are generally used for Solar Pumps and all the Pump Companies manufacture Submersible pumps.

May be Shakti has focused its entire bandwidth towards solar pump. Some where I had read that the Company even manufactures solar structure for mounting Solar Panels under its subsidiary Shakti Energy.

Shakti Pumps had also launched first Indigenous Universal Drive “Simha" in 2018.

The opportunity size is so large that every one can get a reasonable share.

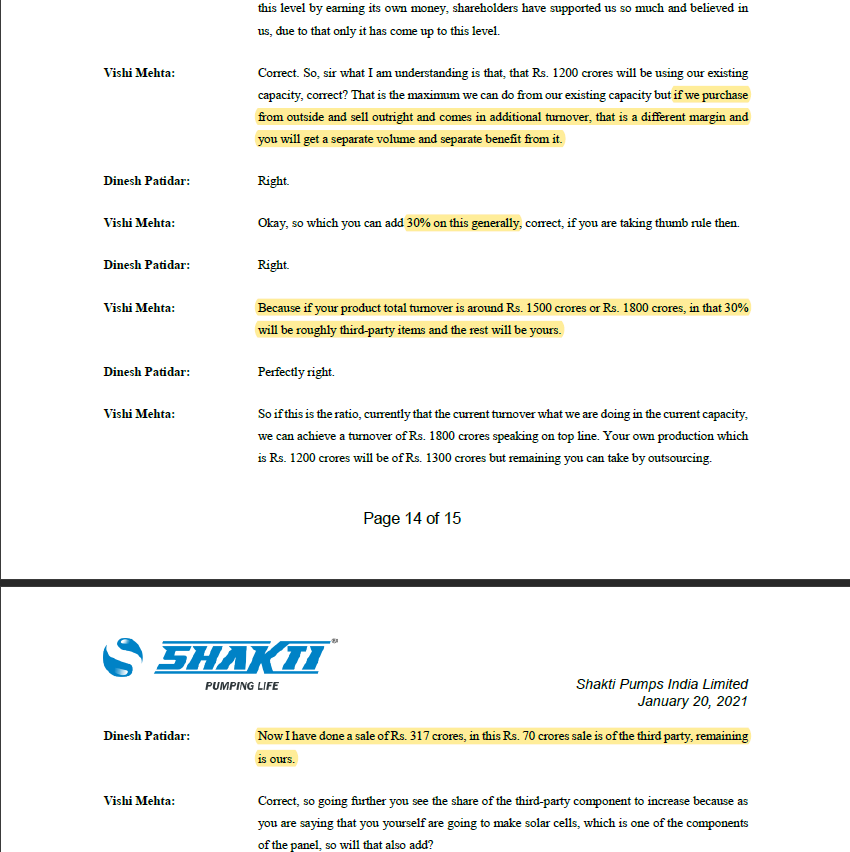

@VALUE2017 @vikas_sinha Yes, Tata Power Solar doesn’t have pump manufacturing, they work with OEMs which mostly work exclusively with them. However, they do have significant brand recognition and impact along with an aim to expand all their verticals. Also, since they don’t directly manufacture, they could easily get on multiple tenders as scaling up is easy for them. Also, Shakti Pump is not a pure manufacturing company. Out of the 300 crore revenue generated in Q3, around 200 crores came through trading. I now realize that this might be the reason behind Shakti Pumps not expanding enough right now, since they could work on the tenders through trading.

From where did you got the figure of Rs 200 Cr as trading sales for Q3 as I couldn’t find single rupee trade revenue in Q3 or Q4 and also no trading revenue for FY 2019-20 or FY 2020-21.

Yes, almost everybody sells submersibles, but definitely not Roto, and WPIL only sells very less large B2B kind of submersibles. Generally pump manufacturers seem to have their individual focus and Kirloskar, KSB do not have submersibles as large part of portfolio. Submersibles being more-energy efficient are needed since they are to be coupled with energy supply from solar-panels which are expensive and low-power efficient.

Shakti quality counts since submersibles are not easy to access for fixing them and installers such as Tata power solar offer 5 yr warranties.

You are right about the opportunity size being huge, with enough to go around. Planned subsidy is ~120k Cr, some 30% contributed by buyer/farmer (with loan option). So, in effect market is ~150k Cr. This is divided over solar plants, solarization of pumps and new solar pumps. Estimating, 60% of this amount for solar pumps, we get spend of ~95k Cr. In past year ‘pilot’, Shakti got 33% of orders, so at that rate they can do sales worth ~30k Cr. So 30 years worth of peak capacity sales opportunity, hence the need for ramping up capacities.

Disc: invested

My bad, I had forgotten the exact numbers (it is 70 crores and not 200 crores), but in the Q3FY21 concall it is mentioned that they do approximately 30% sales through trading

The clarification in the Concal which you have cited is not related to trading income but third party purchase like Solar Panels and Structures. However as earlier said the Company has started making its own structure for mounting of Solar panels. So the third party purchase is mostly solar panels and it will be not recognized as trading income.

From the below file you can guess the size of opportunity the Solar pump represents : 17.5 lac PUMPS BY 2022.

The total present supply under the scheme is less then 1 lac …

Current supply is not even the tip of iceberg…

In my opinion the stock is at inflection point.

Disclosure: Invested and views are biased.

Earnings Call for Q4FY21")