Kirloskar Brothers Limited is the century-old, flagship fluid management company of the Kirloskar Group, recognized as India’s first and largest pump manufacturer.

Company History & Evolution

-

Early Foundations: Established in 1888, the company was incorporated as KBL in 1920. It has a rich history of engineering firsts in India, including the first iron plough, first electric motor, and the first centrifugal pump in 1926.

-

Strategic Divestments: Over the decades, KBL incubated and subsequently divested several major industrial businesses to form independent entities like Kirloskar Oil Engines, Kirloskar Pneumatic, and Kirloskar Electric.

-

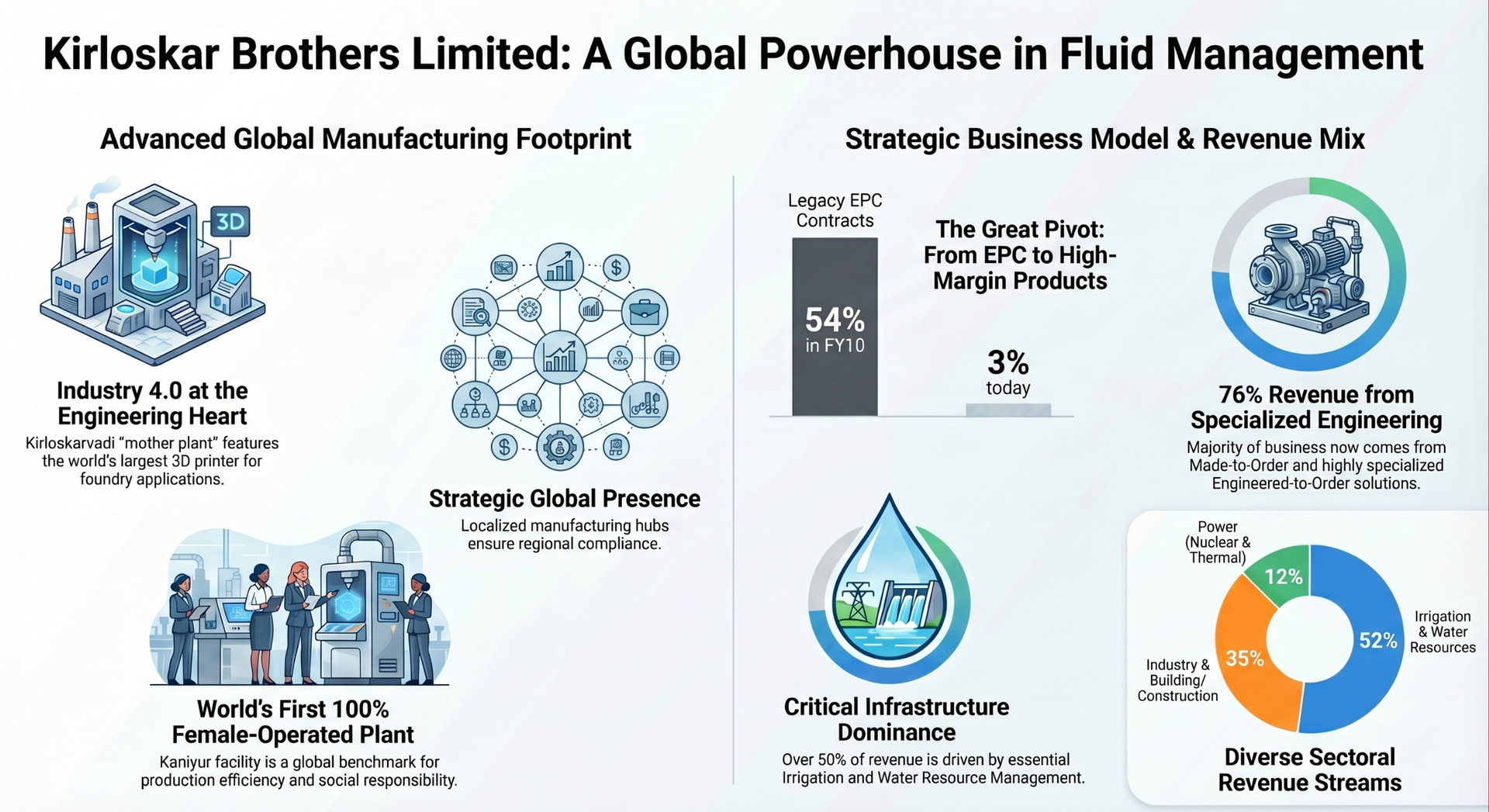

Global Expansion & Acquisitions: The modern era saw KBL transform into a multinational entity through strategic acquisitions and joint ventures. This includes establishing Kirloskar Ebara Pumps Ltd (1988), and acquiring SPP Pumps UK (2003), Kolhapur Steel (2007), Braybar Pumps South Africa (2010), SyncroFlo USA (2014), and Rodelta Pumps Netherlands (2015).

-

Technological Modernization: Today, KBL is heavily investing in Industry 4.0, utilizing remote IoT monitoring (KirloSmart), AR/VR training, and additive manufacturing.

Manufacturing Facilities: Global Footprint and Technological Integration

Kirloskar Brothers Limited operates a highly distributed and specialized manufacturing network designed to optimize localized production, adhere to regional sourcing mandates, and leverage specialized labour pools.

-

Kirloskarvadi, Maharashtra (Established 1910): Serving as the mother plant and the engineering heart of the company, this expansive facility handles end-to-end manufacturing from foundry casting to final testing. It is equipped to produce a massive range of pumps, scaling from small 5 kW units up to customized engineered pumps of 30 MW. The facility integrates advanced Industry 4.0 manufacturing processes, notably housing the world’s largest 3D printer for foundry applications, which significantly reduces the lead time for complex castings.

-

Dewas, Madhya Pradesh (Established 1962): This is the company’s second-largest domestic manufacturing hub. It is strategically focused on high-volume production lines, primarily catering to agricultural, domestic, and standard industrial pump requirements.

-

Kaniyur, Tamil Nadu (Established 2011): Dedicated exclusively to the production of domestic pumps, this plant holds a unique global distinction: it is the world’s first and only pump manufacturing facility operated entirely by a 100% female workforce. This facility is a benchmark for both production efficiency and corporate social responsibility.

-

Sanand, Gujarat (Established 2012): This modernized plant focuses exclusively on the manufacturing of borewell submersible pumps, serving critical groundwater extraction needs for agriculture and rural water supply.

-

Shirwal, Maharashtra (Established 2014): Serving as the assembly and technology integration hub, Shirwal focuses on advanced fluid dynamics solutions. It primarily produces Hydro-pneumatic (HYPN) systems and manufactures the IoT (Internet of Things) control panels (KirloSmart) used for real-time predictive maintenance of KBL’s pump installations worldwide.

-

International Manufacturing & Assembly Centers: To comply with regional preference policies—such as the “Buy American” provisions in the United States and the Broad-Based Black Economic Empowerment (BBBEE) program in South Africa—KBL maintains active, localized facilities in Atlanta (USA), Coleford (UK), Almelo (Netherlands), and Johannesburg (South Africa).

HERE

Business Segments, Products, and Financial Contributions

KBL has systematically transformed its business model over the past decade, consciously pivoting away from capital-intensive, lumpy projects toward specialized engineering and high-margin product sales.

1. Product Portfolio & Execution Models

The company manufactures a comprehensive suite of over 75 distinct types of pumps, more than 30 types of valves, and localized hydro turbines. The business is currently structured around three primary execution models:

-

Made-to-Order (MTO - 51%): The dominant segment, providing customized pumping solutions tailored to specific industrial or municipal requirements.

-

Engineered-to-Order (ETO - 25%): Highly specialized, mission-critical pumps built from the ground up for specific applications, such as nuclear power cooling or massive flood control projects.

-

Made-to-Stock (MTS - 20%): Standardized, fast-moving retail pumps (domestic and agricultural) distributed through an extensive dealer network.

-

EPC (Engineering, Procurement, and Construction - 3%): Once the majority of the business (representing 54% of revenue in FY10), legacy EPC contracts have been deliberately minimized to free up working capital and eliminate execution risk.

2. Sectoral Revenue Mix

KBL’s revenue stream is well-diversified across critical infrastructure sectors:

-

Irrigation (28%) & Water Resource Management (24%): Together forming the largest revenue block, this segment is driven by large-scale government lift irrigation projects and national water supply schemes like the Jal Jeevan Mission.

-

Industry (20%) & Building & Construction (15%): Driven by specialized pumps for chemical processing, oil & gas, HVAC, commercial building pressure management, and FM/UL-approved fire-fighting systems.

-

Power (12%): A highly specialized segment where KBL holds a dominant engineering position, including the manufacturing of primary and secondary sodium pumps for India’s nuclear fast breeder reactors and massive circulating water pumps for thermal power plants.

3. Financial Performance and Segment Profitability

The financial breakdown highlights the specific contributions of domestic and international operations:

-

Domestic Standalone (KBL): Continues to be the primary profit engine, generating Rs. 1,919 Crores in revenue and delivering strong EBITDA margins of 14.3%.

-

Karad Projects and Motors (KPML - Subsidiary): Contributed Rs. 460 Crores to the top line, yielding an EBITDA of Rs. 47.9 Crores.

-

International Operations (KBIBV Group): The overseas subsidiaries collectively delivered Rs. 1,149 Crores in revenue with an aggregate EBITDA of Rs. 131 Crores, showcasing successful turnaround and localized execution strategies across different geographies:

-

SPP Pumps (USA): Demonstrated excellent operational leverage, reporting Rs. 415 Crores in revenue with an impressive 13.6% EBITDA margin.

-

SPP Pumps (UK): The largest single international revenue contributor at Rs. 507 Crores, maintaining stable profitability with an 8.8% EBITDA margin.

-

South African Entities: Though smaller in scale (Rs. 51 Crores in revenue), this segment achieved exceptional profitability with EBITDA margins reaching 21%, benefiting from localized manufacturing advantages and high-margin demand from the regional mining sector.

----------------------------------------------------------------------------------------------------

Promoters & Leadership Profile

Background & Technocrat Status

The promoters of Kirloskar Brothers Limited (KBL) are highly educated technocrats, a characteristic that deeply influences the company’s engineering-first culture.

-

Mr. Sanjay Kirloskar (Chairman & Managing Director): He holds a Bachelor of Science degree in Mechanical Engineering from the Illinois Institute of Technology, USA. Under his leadership, KBL has transformed from a domestic manufacturer into a global fluid management multinational.

-

Ms. Rama Kirloskar (Joint Managing Director): She brings a blend of technical and financial expertise, holding a double major in Mathematics and Biology from Bryn Mawr College, USA, and possessing prior experience in venture capital in Boston.

-

Mr. Alok Kirloskar (Director): He holds a Bachelor of Science in Business Administration with a concentration in Finance from Carnegie Mellon University, USA, and drives the international operations and strategic acquisitions.

Shareholding

- Promoter Holding: As of the quarter ending December 2025, the promoter and promoter group hold a commanding 65.95% stake in the company. The holding is distributed directly among the family (e.g., Sanjay Kirloskar ~22.48%, Pratima Kirloskar ~17.44%) and through group entities like Kirloskar Industries Ltd (~23.91%).

Marquee Investors & Institutional Shareholding (As of Dec 2025)

KBL has attracted significant institutional backing, reflecting confidence in its turnaround and capital allocation strategy.

-

FII/FPI Holding: Foreign Institutional Investors hold 6.05%. A notable marquee investor in this category is the Long Term India Fund, holding roughly 1.13%.

-

DII / Mutual Fund Holding: Domestic Institutions hold 7.99% (up from 7.63% in the previous quarter).

-

Nippon India Small Cap Fund: This marquee mutual fund is the largest institutional shareholder, holding a significant 5.68% stake.

-

Mahindra Manulife Value Fund: Holds 1.05%.

-

The New India Assurance Company: Holds 1.06%.

Q3 Earnings Quality & Line Items

1. Quality of Earnings

While Revenue dipped slightly (-2.45% YoY) and PBT dropped (-23.84% YoY), the quality of the earnings is robust.

-

The Tax Anomaly: The YoY drop in PBT was exacerbated by a ₹15.60 Crore exceptional charge relating to newly notified Labour Codes. However, Net Profit actually grew 5.82% YoY. This was due to the NCLT-approved merger of KBL’s step-down subsidiary, The Kolhapur Steel Limited (TKSL), into Karad Projects and Motors Limited (KPML). This strategic merger allowed KBL to utilize ₹126.1 Crores in brought-forward losses, generating a unique tax credit of ₹7.50 Crores for the quarter.

-

Management Discipline: The slight revenue dip is actually a sign of management quality. Rather than “channel stuffing” (pushing inventory to dealers to artificially meet quarterly targets), management deliberately held back ₹50 to ₹100 Crores in domestic dispatches because state-level funding for the Jal Jeevan Mission was delayed. This protects dealer cash flows and ensures the reported earnings reflect genuine, cash-backed demand.

2. Other Income

Other Income stood at ₹19.10 Crores for Q3 FY26. An analysis of the cash flows reveals that the bulk of this is high-quality treasury income—specifically interest income and profits from the sale of mutual funds. This indicates effective deployment of surplus cash rather than one-off asset liquidations.

3. Depreciation & Interest

-

Depreciation: Remained steady at ₹25.20 Crores for Q3 FY26 (₹71.90 Crores for 9M FY26). The company is not artificially altering depreciation schedules to boost short-term profits.

-

Interest (Finance Costs): Extremely nominal at just ₹8.60 Crores for Q3 FY26. KBL operates with a near-zero net debt profile. Total consolidated borrowings (current + non-current) stand at a mere ₹75.2 Crores, which is vastly outweighed by a massive cash and current investment reserve of ₹605 Crores.

Capital Allocation & Return Ratios

KBL’s capital allocation has undergone a disciplined, structural shift. The management systematically shrunk the capital-intensive Engineering, Procurement, and Construction (EPC) business from 54% of revenue in FY10 down to just 3% today. Capital is now strictly directed toward high-margin, fast-turnover Made-to-Order and Engineered-to-Order products. The immense surplus cash generated from this asset-light pivot is continually parked in safe, liquid mutual funds (e.g., holding ₹286.3 Crores in current investments as of September 2025).

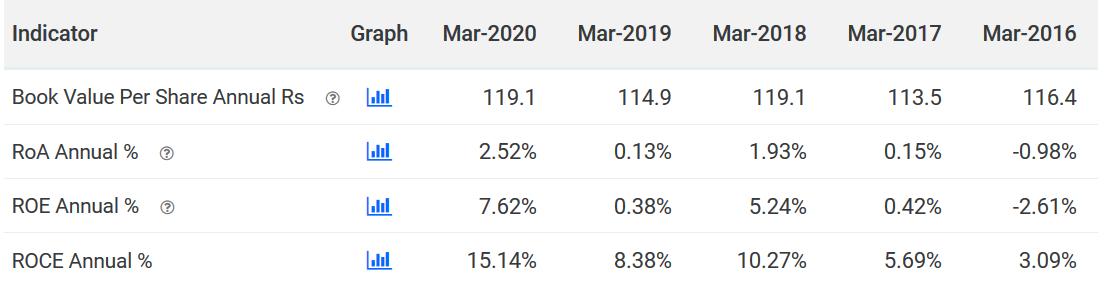

Return Ratios (ROE & ROCE)

This aggressive defense of working capital and low debt profile dramatically boosts the company’s return ratios.

-

Return on Equity (ROE): With a consolidated Equity base (Net Worth) of ₹2,217.6 Crores as of September 2025 and an annualized PAT trajectory running above ₹350 Crores, KBL generates a robust ROE in the 15% to 16% range.

-

Return on Capital Employed (ROCE): Because the company utilizes practically zero long-term debt to fund its operations, the ROCE naturally trends significantly higher than the ROE, signalling that the core manufacturing engine is highly efficient at compounding capital.

Working Capital & Cash Conversion Cycle

1. Receivables Management

KBL has demonstrated exceptional discipline in collecting cash, slashing its consolidated trade receivables by a massive ₹136.5 Crores in just six months (dropping from ₹580 Cr to ₹443.5 Cr).

- The Strategy: The improvement in receivable days (down to ~40 days) is the direct result of a stringent internal policy framework. The company refuses to book or dispatch large project orders until cash advances are formally secured in the bank. This ensures that revenue growth is strictly cash-backed, entirely eliminating the risk of bad debts from aggressive “top-line chasing.”

2. Inventory Management

Inventory is the sole factor widening the Cash Conversion Cycle. Total inventory expanded from ₹853.7 Crores in March 2025 to ₹972.7 Crores by September 2025.

3. Trade Payables

Trade payables reduced slightly from ₹612.0 Crores to ₹581.9 Crores. The company continues to pay its suppliers promptly, ensuring a stable and reliable supply chain without overly stretching its vendors to artificially pad its own operating cash flows.

Cash Flow Deconstruction:

-

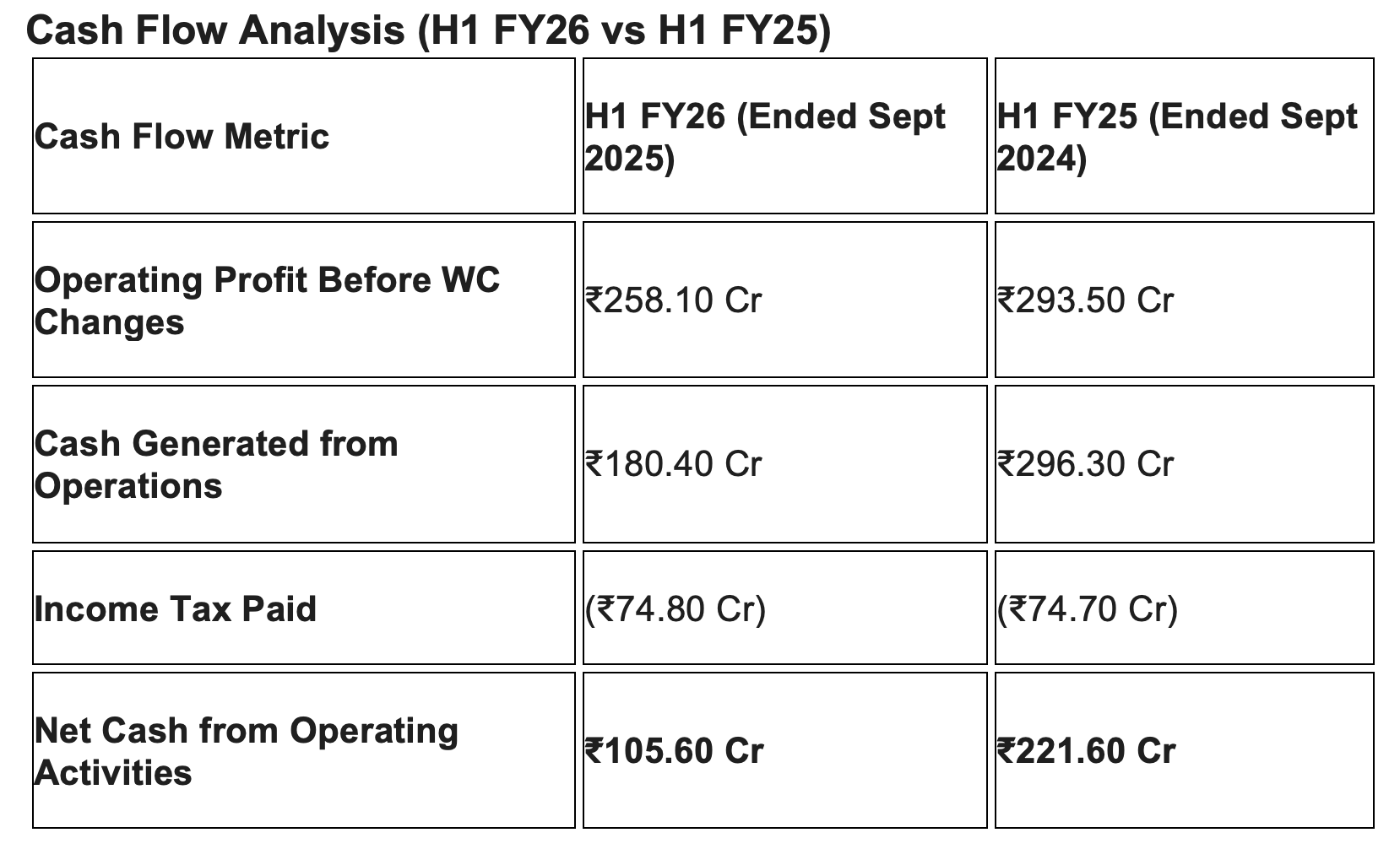

Operating Cash Flow (OCF) Moderation: Net Cash from Operating Activities dipped to ₹105.60 Crores in the first half of FY26, compared to a stronger ₹221.60 Crores in the same period last year.

-

The Working Capital Drag: The reconciliation clearly shows that the ₹119 Crore buildup in inventory was the primary drain on operating cash flows. However, this was significantly buffered by the ₹129.3 Crore release of cash from the rapid collection of trade receivables.

-

Robust Liquidity: Despite the temporary dip in OCF, KBL’s balance sheet remains exceptionally liquid. The company continues to maintain a massive war chest of ₹605 Crores parked in current investments (mutual funds), cash, and bank balances. The deployment of this cash is generating high-quality treasury returns, yielding ₹24.4 Crores in interest income and ₹5.3 Crores in mutual fund profits during this half-year alone.

1. Major Acquisitions & Their Synergies

A. SPP Pumps Limited (United Kingdom) – Acquired 2003

-

The Profile: KBL’s flagship international acquisition. SPP Pumps is a leader in engineered pumping solutions, particularly dominant in the global fire-fighting, offshore, and water supply markets.

-

The Synergies:

-

Market Leadership: SPP enjoys an immense market share (historically ~80% in specific UK niches) and provides KBL with a dominant foothold in the Middle Eastern oil, gas, and water sectors.

-

R&D and Digital Hub: SPP acts as the innovation engine for the broader KBL group, spearheading digital initiatives like the “KirloSmart” IoT condition monitoring system.

-

Financial Engine: It is the largest international revenue contributor (generating over ₹500 Crores in a 9-month period) and maintains stable profitability.

B. SyncroFlo Inc. (United States) – Acquired 2014 (via SPP)

-

The Profile: An Atlanta-based pioneer and manufacturer of pre-assembled, packaged pumping systems, primarily catering to HVAC, fire protection, and municipal water pressure management.

-

The Synergies:

-

“Buy American” Compliance: SyncroFlo gave KBL localized manufacturing and assembly capabilities on US soil, which is an absolute necessity for winning municipal and government infrastructure contracts under strict US domestic sourcing laws.

-

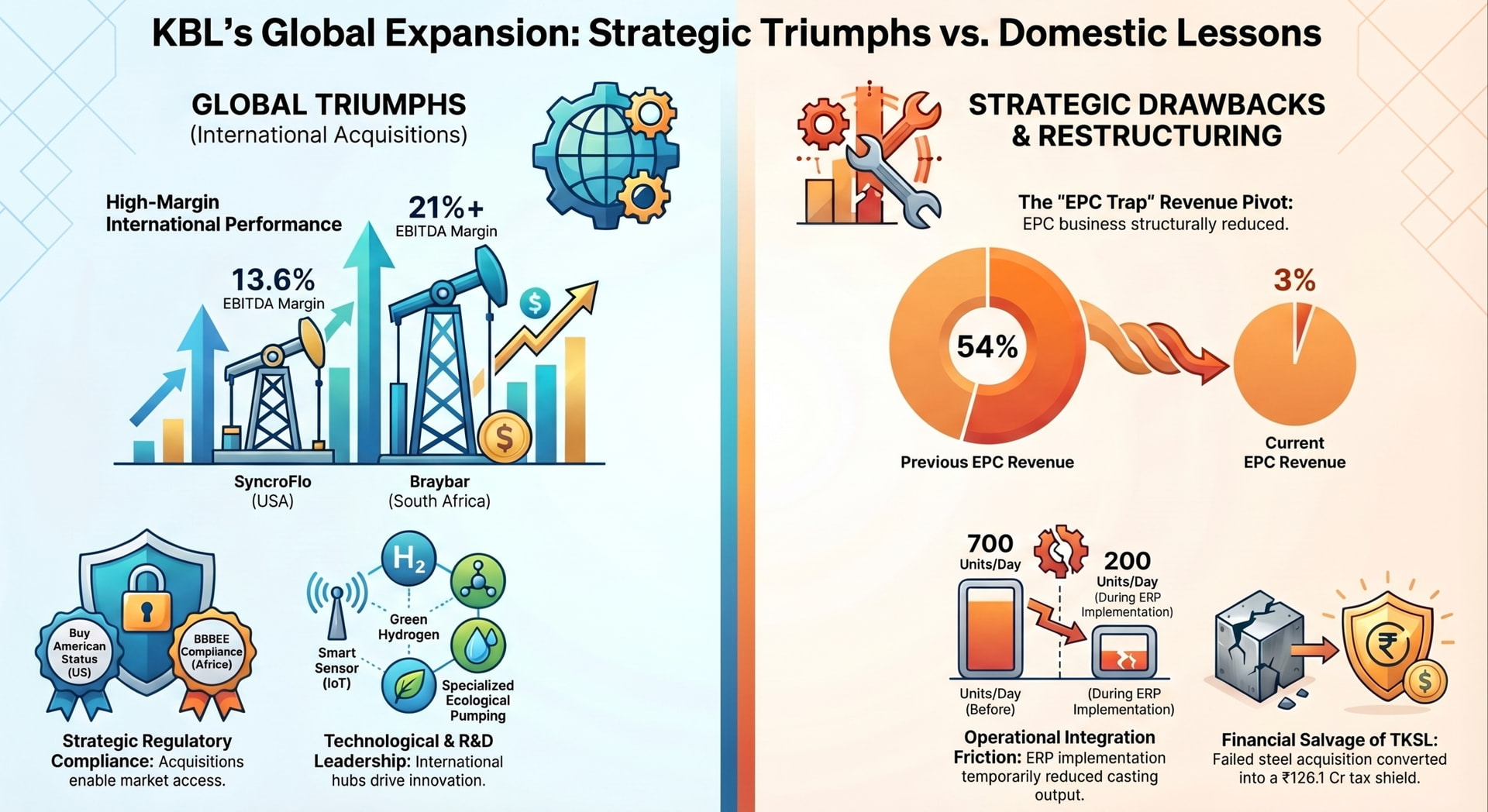

High-Margin Execution: SyncroFlo has proven to be highly lucrative, currently boasting excellent execution leverage with strong EBITDA margins of around 13.6%.

C. Rodelta Pumps International B.V. (The Netherlands) – Acquired 2015

D. Braybar Pumps (South Africa) – Acquired 2010

2. The Drawbacks, Challenges, and “Misses”

A. The Kolhapur Steel Limited (TKSL) – A Strategic Failure Turned Tax Shield

-

The Acquisition (2007): KBL acquired TKSL to secure a captive supply of high-grade alloy steel castings for its massive engineered-to-order pumps, aiming to control supply chain bottlenecks.

-

The Drawback: TKSL turned out to be a severe financial drag. It failed to achieve operational efficiency, accumulated massive debt, and continuously bled cash, forcing KBL to fully impair its investment in the subsidiary.

-

The Resolution (2025/2026): To salvage the situation, KBL orchestrated an NCLT-approved merger, folding the struggling TKSL into another subsidiary, Karad Projects and Motors Limited (KPML). The only “synergy” ultimately derived from this failure was an accounting one: the merger allowed KBL to utilize ₹126.1 Crores of TKSL’s brought-forward losses, generating a sudden ₹7.5 Crore tax credit in Q3 FY26.

B. Aban Constructions & The EPC Trap

-

The Acquisition (2006): KBL acquired Chennai-based Aban Constructions to transform itself from a mere pump manufacturer into an end-to-end Engineering, Procurement, and Construction (EPC) turnkey contractor for massive pipeline and water projects.

-

The Drawback: The EPC business proved to be disastrous for KBL’s balance sheet. It was highly lumpy, politically sensitive, and brutally working-capital intensive. Projects frequently stalled, trapping KBL’s cash in receivables and elongated inventory cycles.

-

The Pivot: Realizing the synergy was an illusion that destroyed shareholder value, KBL management had to spend the entire last decade structurally shrinking the EPC business from a massive 54% of total revenue in FY10 down to a mere 3% today, pivoting back to high-margin product sales.

C. Cross-Cultural Integration and ERP Friction

Acquiring companies across different continents brings immense operational friction. Harmonizing diverse IT architectures and manufacturing cultures into a single global entity is challenging. A recent example is the integration of a unified SAP ERP system across KBL’s foundry operations. While necessary for long-term global tracking, the immediate integration severely throttled short-term production (dropping casting output from 700 to 200 per day temporarily), leading to a ₹50 Crore revenue deferral in recent quarters.

Summary

KBL’s acquisition strategy is a tale of two halves. Its international acquisitions (SPP, SyncroFlo, Rodelta) have been brilliant strategic manoeuvres, providing geographic moats, regulatory compliance, and access to premium global margins. Conversely, its historical domestic acquisitions (TKSL, Aban) were strategic missteps that tied up capital and required years of painful unwinding and restructuring to fix. Today, the clean balance sheet indicates that the company has successfully digested these historical drawbacks.

–——————————————————————————————————————–

Capex & Timelines

Kirloskar Brothers Limited (KBL) maintains a highly disciplined approach to capital expenditure. Rather than engaging in massive debt-funded capacity expansions, KBL directs its Capex toward technological modernization, operational efficiency, and ESG (Environmental, Social, and Governance) compliance. The company operates with a near-zero net debt profile, fully funding its capital outlays through robust internal cash accruals.

Historical & Projected Capex Trend:

Nature and Timeline of Capital Investments:

-

Technological Upgrades & Industry 4.0 (Completed/Ongoing): A significant portion of recent Capex was directed toward the installation of advanced 3D printers in the Kirloskarvadi foundry. This drastically reduced the turnaround time for complex, customized Engineered-to-Order (ETO) castings. Furthermore, the company recently invested heavily in a unified SAP ERP system across its foundry operations. While the integration temporarily slowed production in recent quarters, the system is now stabilized and is yielding real-time visibility into material waste and supply chain bottlenecks.

-

Renewable Energy Augmentation (FY25/FY26): To hedge against fluctuating industrial power tariffs and meet sustainability goals, KBL is actively deploying Capex to enhance its captive renewable energy capacity. The company is scaling its infrastructure to an aggregate 13.5 MWp, adding to its existing 4 MW wind and 4.74 MW solar rooftop installations.

-

High-Tech Tool Rooms (Forward-Looking): Aligning with recent domestic manufacturing incentives, future capital outlays will likely focus on precision tooling capabilities to further indigenize high-tech pump manufacturing and reduce reliance on imported components.

Future Growth Prospects

KBL is well-positioned for medium-term revenue visibility, supported by a consolidated order book that swelled to ₹3,727 Crores as of December 2025 (a 20% growth from the previous year). The growth runway is supported by several distinct macroeconomic tailwinds:

-

Thermal Power Resurgence: Reversing a decade-long lull, India is actively adding thermal power capacity. KBL is a direct beneficiary, underscored by its recent ₹214 Crore order from Adani Power for massive Concrete Volute Circulating Water Pumps, slated for execution across multiple states over the next 18 to 24 months.

-

Nuclear Power Expansion: The Indian Union Budget 2026 extended the basic customs duty exemption on goods required for nuclear power projects until 2035. KBL is a dominant supplier of highly complex primary and secondary sodium pumps for India’s fast breeder reactors. This policy stability guarantees a long-term, high-margin pipeline for the company’s ETO segment.

-

Water Resource Management & Irrigation: The government’s continued push to develop urban infrastructure in Tier-2 and Tier-3 cities, alongside rural initiatives like the Jal Jeevan Mission and the development of ‘Amrit Sarovars’ (reservoirs), provides sustained demand for KBL’s standard and mid-sized fluid management systems.

Optionality (Non-Linear Growth Vectors)

“Optionality” refers to emerging, high-potential business avenues that currently contribute minimally to the bottom line but possess the capability to scale exponentially, offering non-linear upside to the stock.

1. Data Center Liquid Cooling Systems

The explosive global growth of Artificial Intelligence is driving a massive build-out of hyper-scale Data Centers. These facilities generate immense heat, transitioning the industry from traditional air cooling to highly complex liquid cooling infrastructure. Management has explicitly stated they are actively targeting the Data Center market. If KBL successfully positions its specialized pumps and HVAC fluid management systems within this ecosystem, it will unlock a high-growth, technology-agnostic revenue stream.

2. Green Hydrogen & Carbon Capture Value Chains

Through its European subsidiary, Rodelta Pumps International (acquired in 2015), KBL possesses advanced intellectual property in niche fluid dynamics. This includes specialized OH5 pumps, which are highly suitable for the emerging Green Hydrogen production and transportation sector. As global capital—and domestic incentives, such as the ₹20,000 Crore allocation for carbon capture tech—flow into clean energy transition, KBL’s European technology portfolio could see outsized demand.

3. Predictive Maintenance as a Service (PaaS)

KBL has developed “KirloSmart,” an IoT-based condition monitoring system that tracks pump health, vibration, and temperature in real-time. Currently, this acts as a value-add to equipment sales. However, the optionality lies in transforming KirloSmart into a standalone, subscription-based Software/Service model. Transitioning from selling industrial hardware to earning recurring software and maintenance revenues would fundamentally re-rate the company’s valuation multiples.

KBL’s competitive dynamics:

1. Competition with Chinese Manufacturers

The Challenge:

Chinese pump manufacturers (such as Kaiquan Pump, PowerChina, and various regional fabricators) operate heavily in the high-volume, standardized pump market. They aggressively target developing regions—particularly Africa, the Middle East, and Southeast Asia—often undercutting global bids by leveraging low raw material costs and state-backed project financing. This creates severe pricing pressure, especially in municipal water and sewage pump tenders where public bidding often prioritizes upfront cost over lifecycle efficiency.

KBL’s Counter-Strategy:

KBL actively avoids engaging in a “race to the bottom” on price. Instead, it is capitalizing on the global “China+1” supply chain realignment.

- The NABL Moat: To separate itself from cheap imports, KBL recently became the only pump manufacturer globally to secure the rigorous NABL (National Accreditation Board for Testing and Calibration Laboratories) accreditation for its Hydraulic Research Centre. This provides independently validated, internationally recognized testing data. As global buyers increasingly demand certified quality and risk mitigation over pure low-cost sourcing, this accreditation acts as a massive differentiator for KBL in international export markets.

2. Local Competition

In the domestic market, competition is strictly divided based on the type of pump and the end-user application.

-

Engineered & Municipal Pumps (Direct Rivals: WPIL Limited, Jyoti Ltd): WPIL is one of KBL’s most direct comparables in the large-scale municipal, irrigation, and power segments. Both companies fiercely contest high-value government tenders, such as state-level river-lift irrigation schemes and thermal power cooling pumps. While WPIL is highly aggressive in project execution, KBL leverages its century-old institutional references, sheer scale (capable of manufacturing pumps up to 30 MW), and superior balance sheet liquidity to win large-scale orders.

-

Retail, Domestic & Agricultural Pumps (Direct Rivals: Shakti Pumps, CRI, Texmo): In the “Made-to-Stock” segment (borewell submersibles, small agricultural pumps), KBL faces intense pressure. Competitors like CRI and Shakti Pumps dominate the retail channels with incredibly deep, aggressively incentivized dealer networks. While KBL maintains a strong presence here, it is strategically pivoting a larger portion of its capital away from this commoditized, low-margin segment toward high-margin industrial products.

-

The EPC Shift (L&T, MEIL, NCC): Historically, when KBL operated a massive turnkey EPC (Engineering, Procurement, and Construction) division, it competed directly with prime contractors like Larsen & Toubro (L&T) and Megha Engineering (MEIL). Today, because KBL has structurally shrunk its EPC exposure down to 3%, it no longer competes with these giants. Instead, KBL now acts as a specialized equipment supplier to these prime contractors, effectively turning former rivals into bulk customers.

3. International Competition (Global Multinationals)

In the high-end industrial, chemical processing, and nuclear power sectors, KBL’s international subsidiaries (SPP Pumps, SyncroFlo, Rodelta) go head-to-head with some of the world’s largest fluid-handling conglomerates.

-

High-Spec Industrial & Power (Direct Rivals: Flowserve, KSB, Sulzer): These MNCs possess legacy technology and deep R&D pockets, often setting the benchmark in nuclear, oil & gas, and complex chemical tenders. KBL competes against them by combining the niche European intellectual property it acquired (e.g., Rodelta’s specialized OH5 pumps for green hydrogen) with the cost-arbitrage of manufacturing major components at its Kirloskarvadi mother plant in India.

-

Water Management & Smart Pumping (Direct Rivals: Grundfos, Xylem, Wilo): Players like Grundfos and Xylem are aggressively pushing digital monitoring, energy-efficient lines, and lifecycle maintenance contracts. To prevent losing market share to these technological shifts, KBL has developed “KirloSmart”—its proprietary IoT condition-monitoring system that offers real-time predictive maintenance, matching the digital offerings of its European competitors.

Summary of KBL’s Competitive Advantages

-

Regulatory and Regional Compliance: Global competitors often struggle with localized protectionist policies. KBL bypasses this via its subsidiaries. For example, its SyncroFlo plant in Atlanta allows it to win US municipal contracts under strict “Buy American” infrastructure laws, while its Braybar facility ensures compliance with South Africa’s BBBEE (Black Economic Empowerment) mandates, effectively locking out non-localized MNCs.

-

Diverse Execution Models: By maintaining a balanced mix of Engineered-to-Order (25%), Made-to-Order (51%), and Made-to-Stock (20%), KBL insulates itself from the cyclical downturns that routinely hurt competitors heavily over-indexed to a single sector (like retail agriculture or pure-play EPC).

-

Cash-Backed Bidding: Unlike highly leveraged competitors who bid aggressively on government tenders just to maintain cash flow, KBL’s massive cash reserves and zero-pledge promoter holding allow it to walk away from low-margin, high-risk contracts, ensuring the order book remains highly profitable.

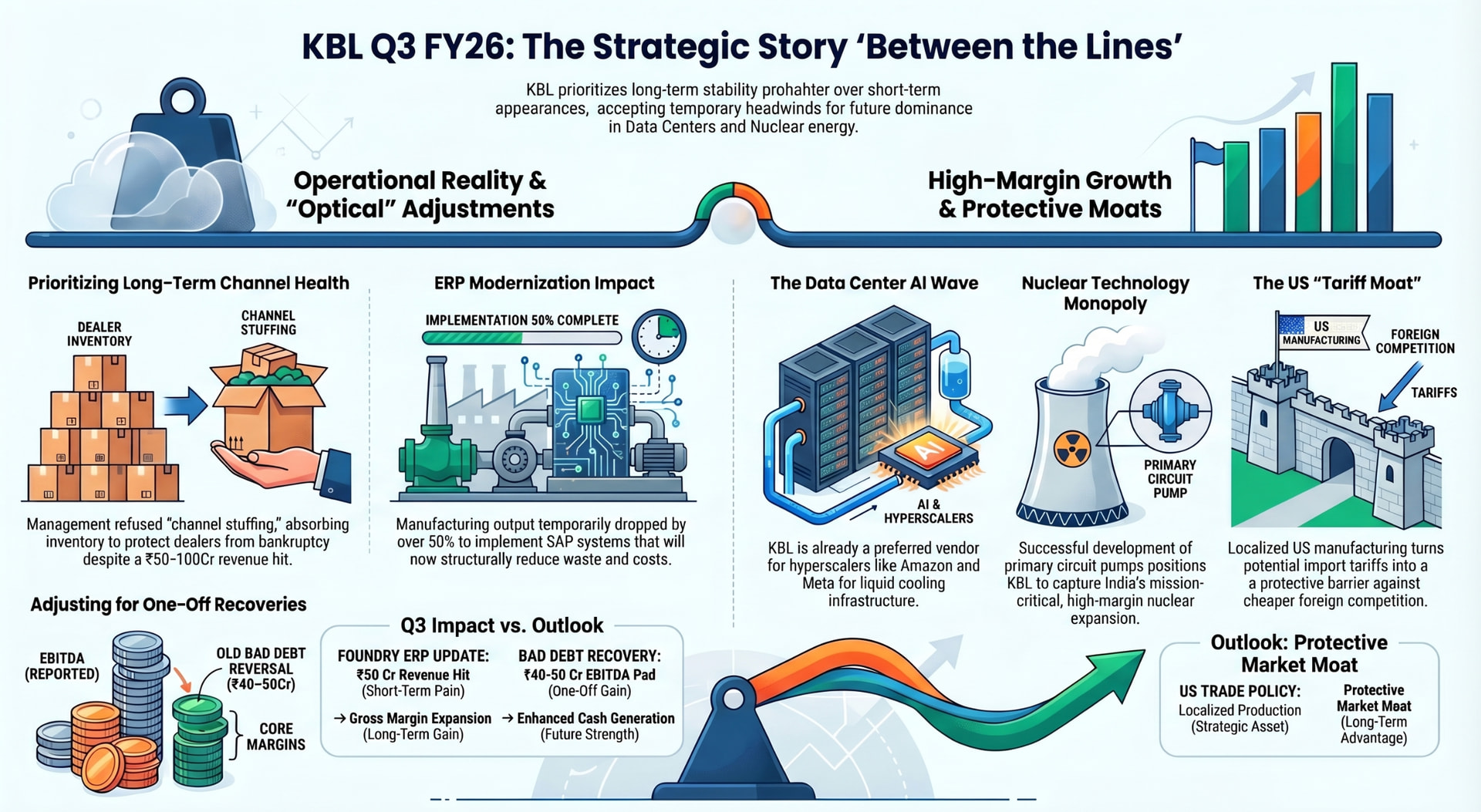

“Read Between the Lines” of the Q3 FY26 Earnings Call:

1. Working Capital Discipline over Optical Revenue Growth

The Commentary: Management noted that standalone performance was temporarily affected due to a slowdown in the Jal Jeevan Mission (JJM), resulting in a revenue reduction of Rs. 50 crores to Rs. 100 crores. The state governments have delayed funding their 20% portion of the scheme, causing a cash crunch.

Reading Between the Lines: KBL is actively refusing to engage in “channel stuffing.” Management explicitly stated they “do not want to just push out equipment and have them have a cash flow situation and destroy their business”. They are absorbing inventory on their own balance sheet to protect their multi-generational dealers from bankruptcy. While this hurts Q3 optical revenue growth, it is a highly ethical, long-term move that preserves the health of their distribution network and prevents the creation of toxic, uncollectible receivables. Furthermore, their policy of not recognizing large orders without confirmed cash advances highlights extremely conservative accounting.

2. The Profitability Boost was Heavily Padded by Bad Debt Recovery

The Commentary: The company reported a significant decline in “Other Expenses” on the standalone entity. Management explained this was due to the successful recovery of old outstandings from customers.

Reading Between the Lines: This is a critical adjustment for modelling core operations. The Chief Financial Officer confirmed that they successfully collected Rs. 40 crores to Rs. 50 crores of old, previously provisioned bad debts. Because this provision was reversed, it artificially deflated “Other Expenses” and padded the EBITDA for the quarter. While this is excellent cash generation and a testament to their collection efforts, one must strip out this Rs. 40-50 crore one-off reversal to arrive at the true, core operating margin for Q3.

3. Short-Term Manufacturing Pain for Long-Term Margin Expansion

The Commentary: The implementation of a new SAP ERP system in the cast iron foundry caused major disruptions, dropping output from a normal run-rate of 700 castings per day down to 200-300 castings. This caused an estimated Rs. 50 crore hit to revenue.

Reading Between the Lines: KBL essentially traded a quarter’s performance to overhaul its legacy manufacturing infrastructure. Management confirmed that the system reverted to target levels by the end of the quarter. More importantly, they noted the new system is now allowing them to “identify waste and also reduce costs”. With this friction now behind them, the ERP system should structurally expand gross margins in the Small and Medium Pump segments by tightening material tracking.

4. International Nuances: The UK Pivot and the “Trump Tariff” Advantage

The Commentary: The UK business faced margin contraction because high energy prices (GBP 283 per megawatt hour) forced major energy-intensive clients (like INEOS) to suspend production, severely hitting KBL’s lucrative service contracts. Conversely, the US business showed 15% growth.

Reading Between the Lines: The UK Restructuring: The UK operation is undergoing a forced structural pivot. Management is aggressively defocusing from energy-intensive industries and replacing that lost revenue with “essential industries” like water utilities (evidenced by the new United Utilities framework contract).

- The US Tariff Moat: A fascinating insight emerged regarding US trade policy. When asked about potential tariffs (up to 60%), Alok Kirloskar stated that a tariff of more than 20% is actually good for their US business. Because KBL has localized manufacturing in the US (SyncroFlo), severe import tariffs essentially build a protective moat around their US operations, locking out cheaper foreign competition and securing their domestic market share.

5. Massive Optionality: Data Centers & Nuclear Monopolies

The Commentary: Management answered questions regarding Data Centers and Nuclear opportunities, highlighting their relationships with global consultants and the successful testing of primary circuit pumps.

Reading Between the Lines: These two segments represent explosive, non-linear growth optionality:

-

Data Centers: KBL is already a preferred vendor for global hyperscalers, having supplied to Amazon, Meta, and Equinox data centers. With 4,000 data centers operational in the US and 2,000 seeking permission , KBL’s integration with prime global consultants like AECOM positions them perfectly to ride the massive wave of AI-driven liquid cooling infrastructure.

-

Nuclear Dominance: KBL has broken a massive technological barrier by successfully developing the prototype primary heat transfer pump for India’s nuclear fleet orders. Management confidently noted the pump performed “far better than expected by NPCIL”. Furthermore, they self-funded R&D to develop two additional primary circuit pumps, both of which have passed NPCIL testing. This places KBL in an effective duopoly (or monopoly) position to capture the highest-margin, mission-critical engineering contracts as India rapidly expands its nuclear power footprint over the next decade.

---------------------------------------------------------------------------------------------------------

Compiled Notes from here & there. No Buy/Sell Recommendation.

---------------------------------------------------------------------------------------------------------

An Enlightening Substack post: HERE

----------------------------------------------------------------------------------------------------------------