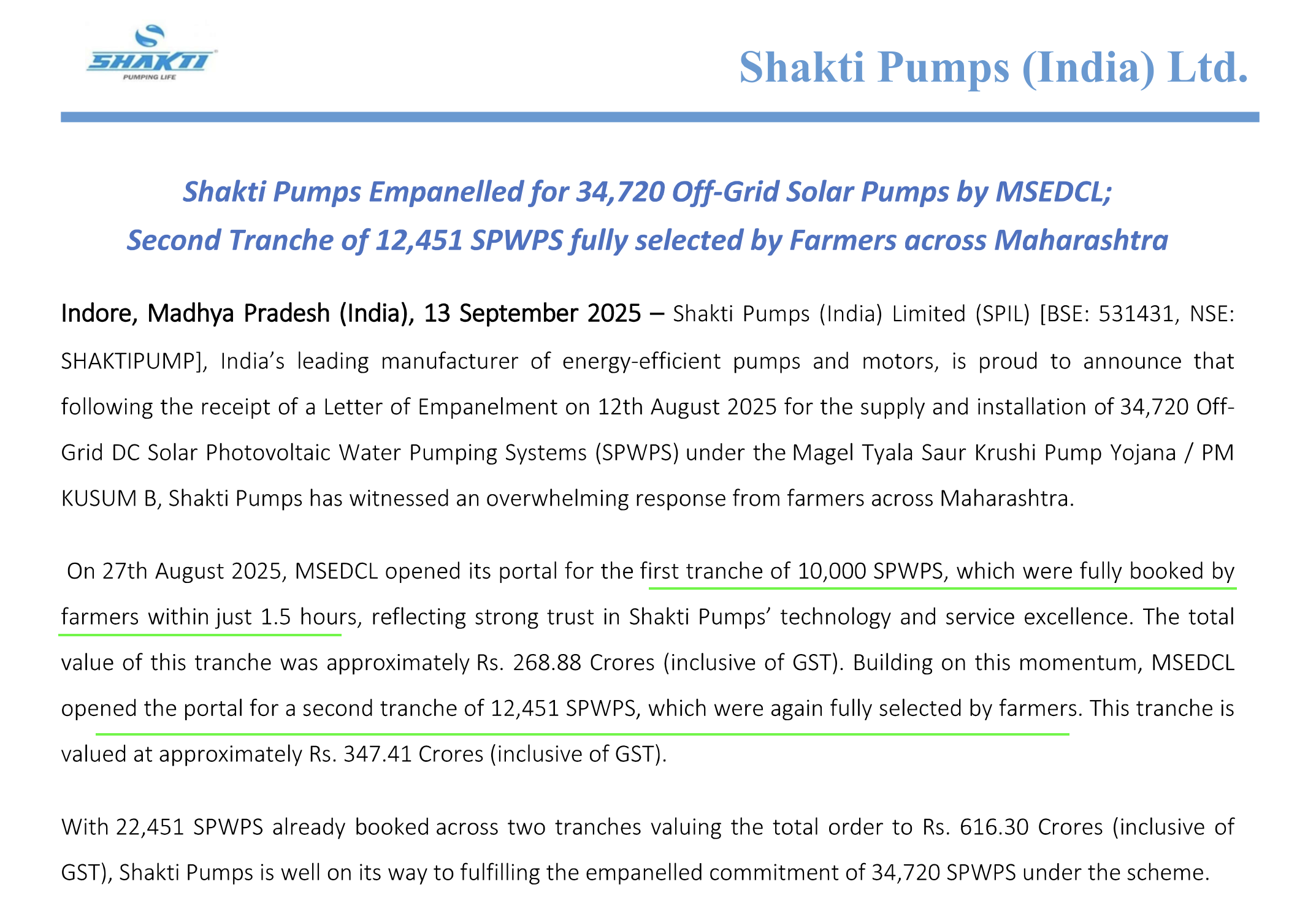

The second tranche on the MSEDCL was opened recently . Press release by the company for Rs 347 Cr selected by the farmers. The total number of pumps preferred by the farmers is 22451 , amounting to Rs 616 Cr.

S Pump.pdf (756.5 KB)

4 Likes

The speed of booking entire tranche of Solar Pumps in just 1.5 Hours shows the high demand of solar pumps in the market.

3 Likes

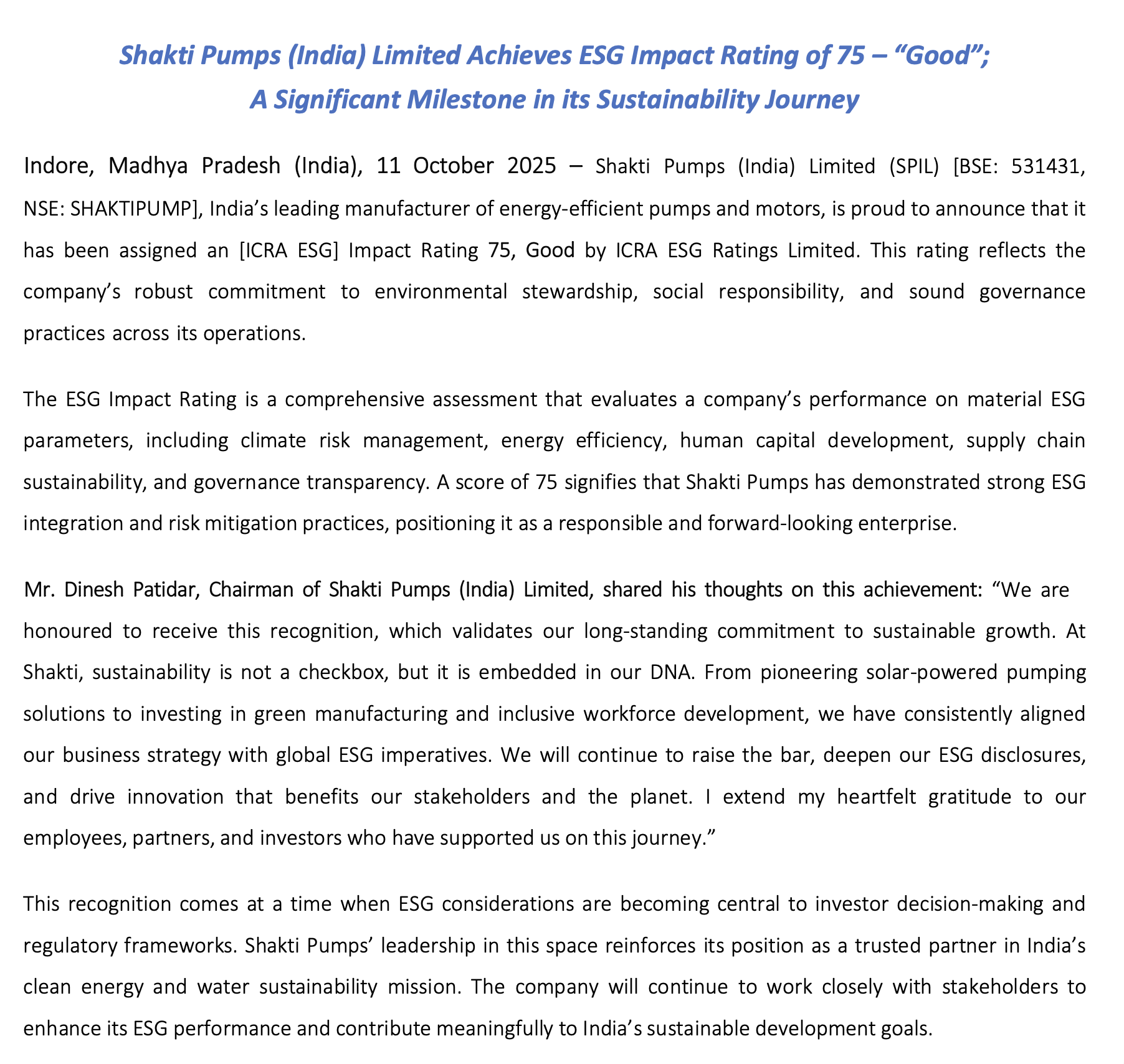

Shakti Pumps (India) Limited received a “Good” ESG Impact Rating of 75 from ICRA, highlighting its commitment to environmental, social, and governance best practices. This recognizes their strong focus on sustainability, clean energy, and responsible business operations.

1 Like

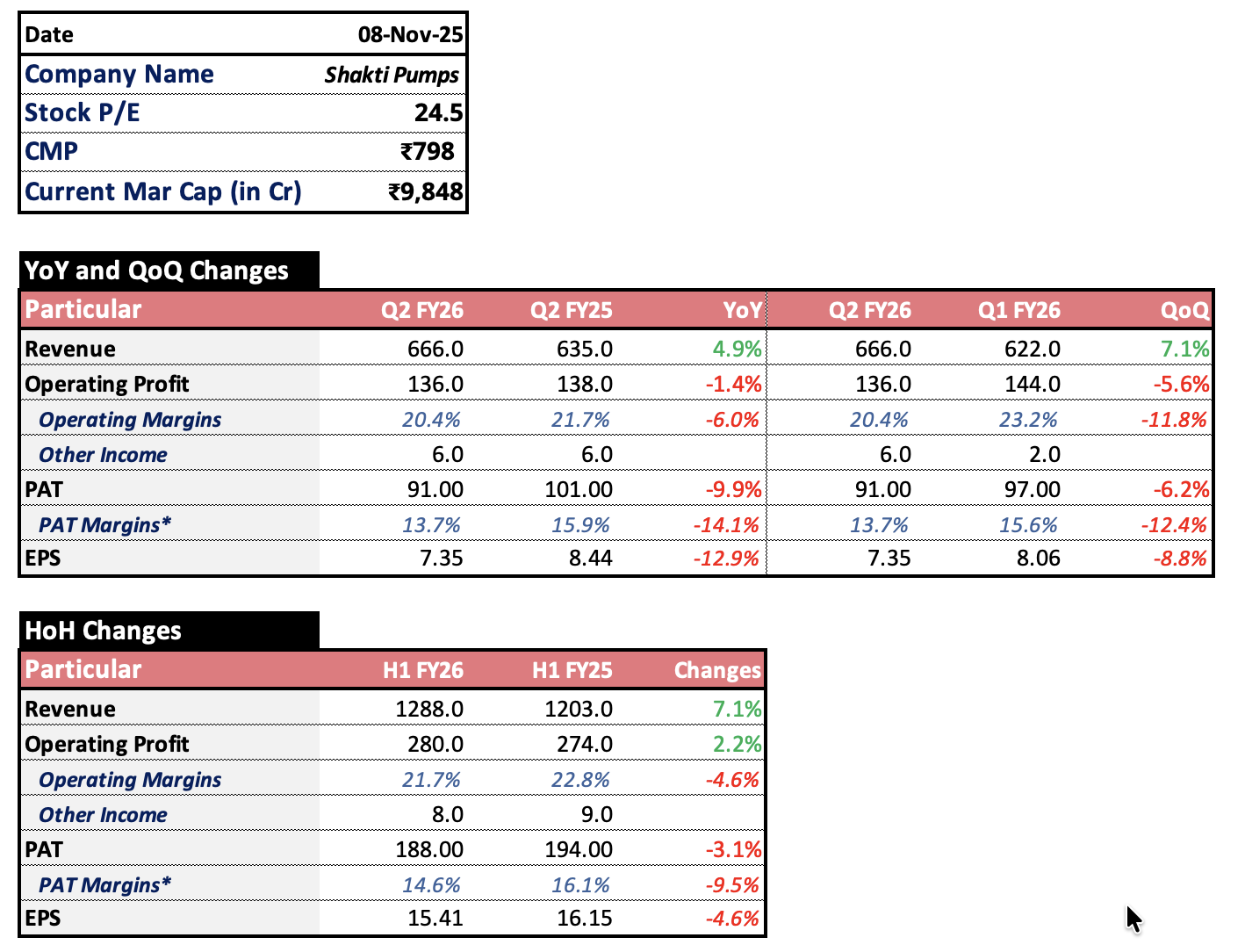

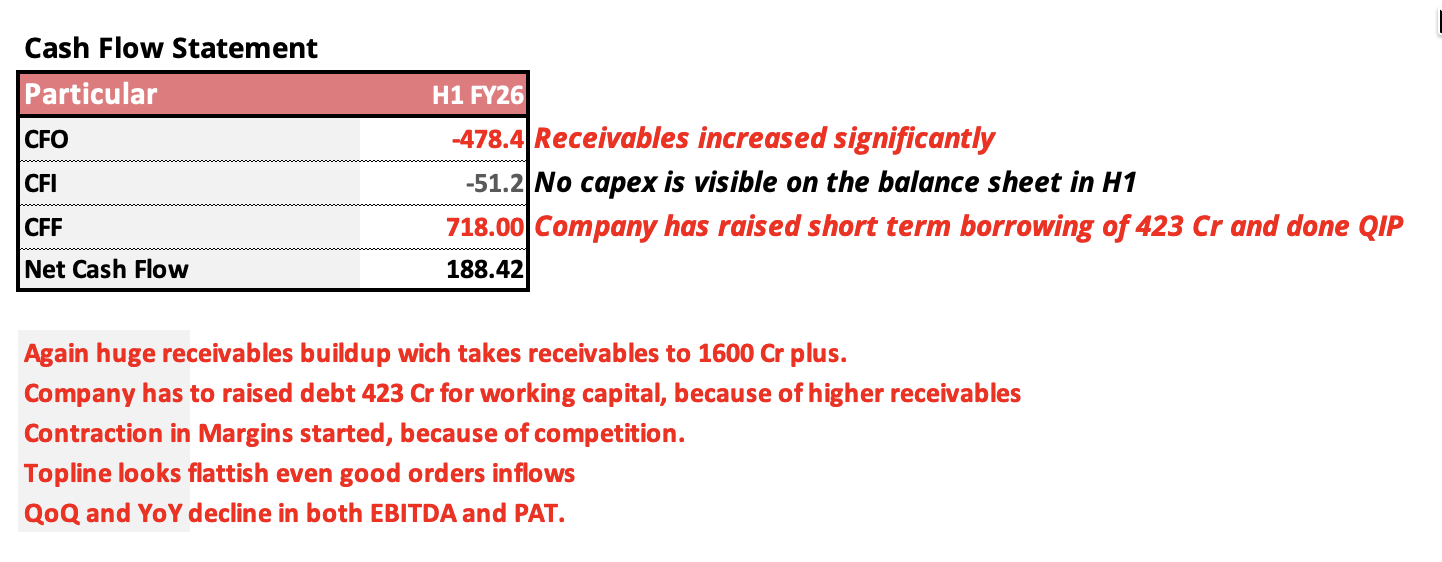

Flattish to Negative Numbers in Q2 FY26

Land Purchase and Development

- The company planned to buy 45.66 acres of land and develop it, costing around ₹20 crore (₹16 crore for land + ₹4 crore for development).

- The ₹16 crore land cost assumes a concession (discount) from the Madhya Pradesh Industrial Development Corporation (MPIDC).

- Without concession, the land would cost ₹32 crore.

- The company has asked the Madhya Pradesh Government to approve this concession.

- If the concession is not approved, the company will cover the extra ₹160 crore using its own funds (internal accruals).

So far, the company has:

• Received an allotment letter from MPIDC for 23.35 acres (no concession on this portion).

• Paid ₹15.36 crore (after adjusting TDS and advance payment).

• The company says this 23.35 acres is enough to start work on the project.

• The remaining 22.31 acres acquisition is still in process.

200 Cr raised last year for this capex which is needed to completed by FY26 end but there is much delay in this.

2 Likes

The management was riding high on government subsidies and now seems to have hit the wall for further growth. Their guidance for the FY seems to be beyond reach by a big margin. Oswal pumps better execution is also eating market share.

PS: invested

2 Likes

Hoping H2 will be good for solar pumps players. Big Kusum 2.0 announcement is also awaited, which will further give road map to the players.

Kusum 2.0 is less likely to happen in this cycle of contracting Govt Capex and even if it comes, it will be not be as big in scope.

Margins for the company peaked right before it did a QIP of 292cr in July! That doesn’t look like a coincidence

2 Likes

Impressive and consistent YOY growth from 125 Cr in 2020 to 1665 Cr as on Sept 25

2020 2021 2022 2023 2024 2025 2026

125 265 383 244 667 1,049 1,665

but unfortunately the growth is in Receivables.

Similar trend in borrowing:

2023 2024 2025 Sept 20225

75 85 170 617

Disclosure: Exited long back.

1 Like

What indication promoter want to give by buying shares worth Rs 0.56 Cr.

There should be meaningful buying rather then just to create news..

@VALUE2017 Maybe the promoter just wants to buy some shares of his company because he has some cash and has hopes because its his company .Why assume bad when he buys and worse when he sells?

More important question is why are you so obsessed with this company since you have sold long ago ? Many companies go up after one sells it for no good reason .Maybe your decision was wrong or the market is wrong ever since . But crying foul over everything and anything is not very useful to anyone .

Disc, Not invested .

4 Likes

I am just sharing my experience as I had been tracking this Company for last 7 years and had been posting my comments. I had participated in the rally and exited well before it reached peak as valuations were not comfortable to me. It has fallen from peak of 1344 to below levels of 700.

I am not regretting my exit but as I did not find valuations comfortable , I am posting my comments.

When I am bullish on any stock I always look for contra and negative views in this forum and the same has helped a lot to me in bringing down my expectations and valuations.

Any body closely following this forum may further investigate on the negative comments posted by members before making any substantial investment.

4 Likes

I exited the stock around 1250 levels. Reason, it was too hot and expensive. Like any run, one needs to stop, breathe, consolidate and then continue the run. The story with Shakti Pump is far from over. The management proved its mettle long time ago. It is consolidating while management is expanding into Solar Cell manufacturing and there are not many hot triggers for the moment. A similar example is Titagarh which is consolidating since last 1 year and would continue for few more months. I believe once the Solar Cell factory nears completion, the good old Shakti Pump rally would start and many bullish traders would re-enter the stock. Till then, one can buy on dips and accumulate. The management it seems is doing the same. They are buying the stock when it nears 700.

Disclaimer: Not invested but tracking

Pump Company entering high end technology product like Solar Cell which has fast obsolesce. How does it make sense.

They should have focused more in high end pumps, value added pumps and compete with likes of KSB & Kirloskar Brothers.

In my opinion it is not diversification but divorcification..

3 Likes

I have seen a lot of QIPs since past few years. As general rule of thumb I always discount the stock price 30-50% from QIP price nowadays for any company.

Disc: tracking with no position

5 Likes

i have a few queries here..

In FY25 they did 71,572 solar pumps.

First of all is why is the company doubling its capacity from 5L to 10 L?

when it is not even able to achieve 1L solar pumps a year.

how is the company claiming to do 70% capacity utilization?

considering other export segments & OEM sales at max they would be doing 2L pumps.

Secondly, average realization of solar pumps keeps varying every year & every quarter i guess.

is it because of the mix of different power of pumps (3HP, 5HP, 7.5HP.. Higher HP pumps cost more)

And what are the major differences between Shakti and oswal other than the module mfg capacity ?

4 Likes

In my opinion none of them presently have any Solar module manufacturing capacity.

With pump company the play in coming days is going to be not just winning orders of government but also capturing the NON DCR solar pump market.

Reasons :

- If the government order delays remain persistent going ahead your capacities can be under-utilized which can impact your ROE.

- Going ahead sustainability of revenue and margins are in play as we can see the competition is increasing & the EPC players are also aggressively bidding.

- In DCR based solar pump what type of solar pump order you want to bid that you margin sustainability is there.

- If company are bidding for all type of pumps there can be impact on margin. If it wants to maintain margins then topline could be impacted. To cover-up impact of top line, company must push product in NON DCR solar pump market & export market.

- As Shakti pump management spoke that the prices in NON DCR solar pump (off-grid) are lesser than DCR solar pump.

In coming days it close to watch the export market & NON DCR solar pump market how it shapes and how solar company are adding dealers/distributors to push the products.

great amount of government orders received within 30-35 days. PM Kusum orders surged.

Around 1900 crores New orders for Shakti & 680 crores went to Oswal.

Orderbook reached to more than 3000 Crores. (-Q3 execution)

Still, they desperately need to diversify from govt orders.

With China pulling out their export rebates on solar products it might get tough even in the NON DCR solar market.

3 Likes

Significant fall in sales and margin along with increase in financial cost and inventory. This is just reversion to mean.

2 Likes