Capex for what? Working capital?

This is a mystery. The capacity is said to be 5 lakh pumps but they have previously done a qio to increase capacity as well as mentioned in concalls about capacity constraints, debottlenecking etc.

It might be a sku issue.

1 Like

Short Squeez coming in Shakti Pump, watch out. Many shorters are going to lose big.

Bro it’s a non FNO stock, and if you want to short it you don’t get any margin benefit because it is in Long Term ASM. I don’t think anyone is shorting this ticker. What’s your rationale behind this Short Squeeze prediction?

2 Likes

Already out of ASM last week and stock does not have to be in FnO to be shorted.

1 Like

Anyone know the rational behind sudden spike in prices?

It seems to be purely technical. The whole market is on the run since last few days and many old names that were not moving suddenly felt left out and start moving north with good volumes. Clearly FOMO amongst many late comers. Another possibility which can always exist is some kind of information that insiders know about the company that would be out soon. But one can only guess.

3 Likes

I think Oswal pumps IPO is round the corner and Market participants generally check current company and closer competitors valuation planned during IPO to see any arbitrage

Disc : Had Positions and exited recently due to around 20-25% growth prospects this FY26 year

3 Likes

Solar Cell is a unrequired backward integration in my opinion.

Disclosure: Exited long back.

2 Likes

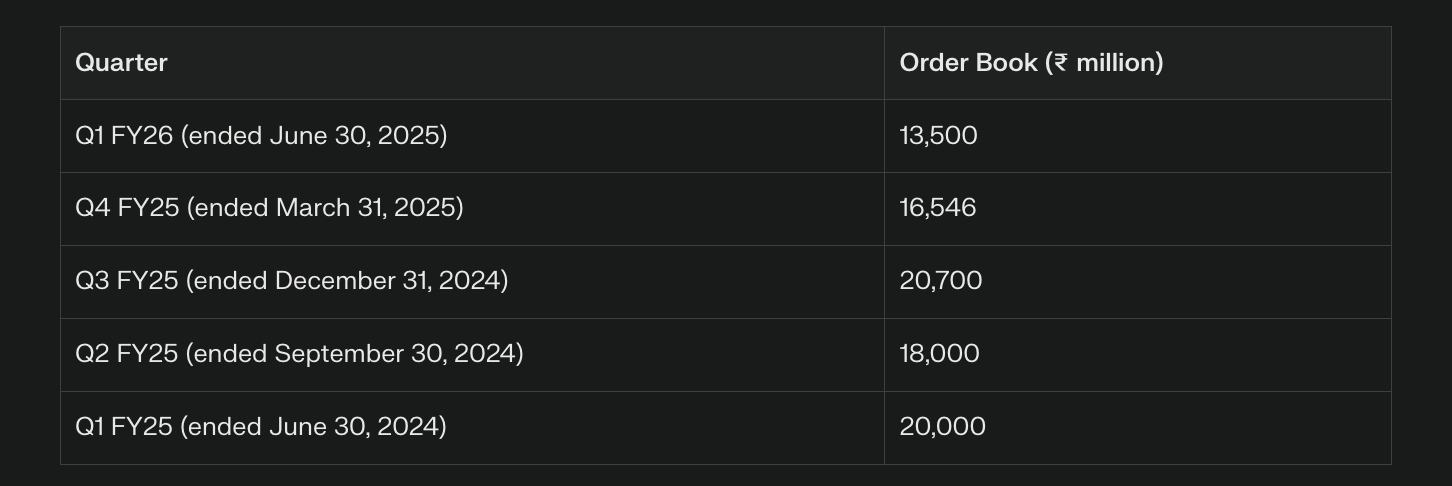

Orderbook at end of every quarter for last 5 quarters. Currently at 1350 cr. Roughly 2.2 times of quarterly revenue

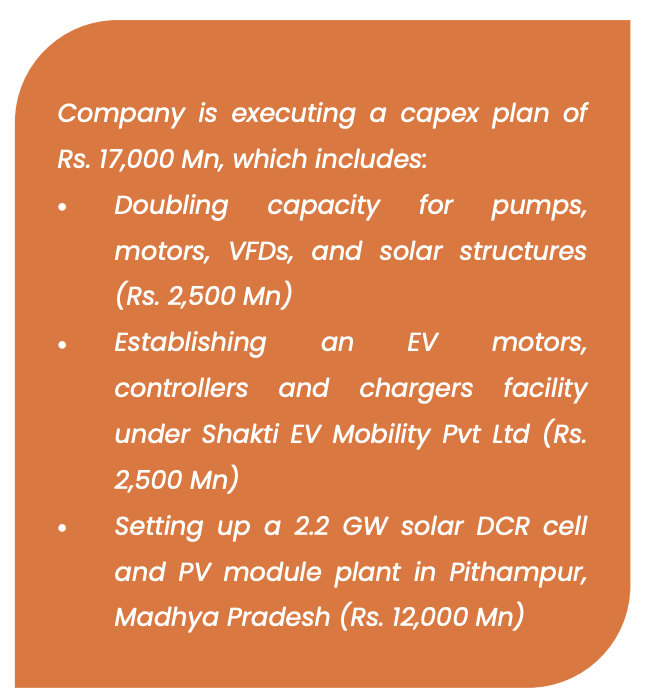

Also capex announced to double capacity for pumps, motors, EV motors and solar DCR cell and PV module plant.

not sure about diversification in EV Motors and DCR cell and PV module. will see how it plays out

4 Likes

This Shakti Pump guy is an expert is decoding the government scheme and most importantly guides the customer like they did with Farmers. They have set of team which knows how to deal with the government and actively clears the O/s.

Now this Surya Kiran Yojana, they are entering here seems to be a good diversification. Because here again government is same, team is same, just the new customer where they can effectively manage as they did earlier.

I don’t know why but i find this guy very resilient and hard working.

Disc : Have small position and Holding

3 Likes

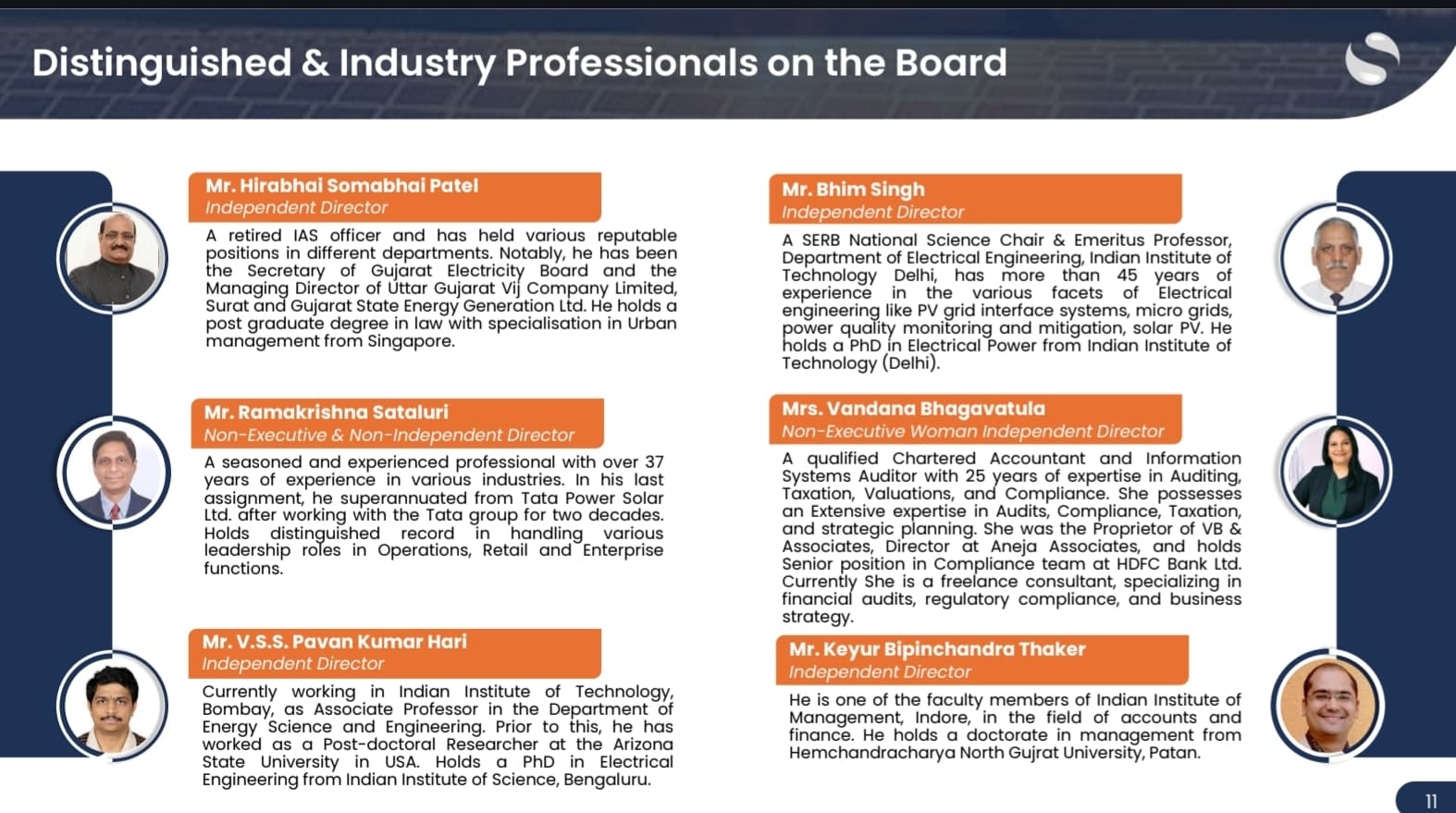

And when companies finding difficulty in appointing talent in ths board of directors this fellow has distinguished illumanries from IIT Mumbai,IIT Delhi,IIM Indore as an independent directors…not a small feat…

Again dewatering projects in Dubai and fountain projects worlwide is something new for me…very informative investor presentation this time…though orderbook soft this time, management are confident of 25 to 30% growth.Also presentation mentions only Maharashtra CM announced 3.5 million solar pump u der magel tyala saur urja pump scheme…so the potential huge going ahead…just a small hiatus in long journey…

Presentation linkx

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3331a845-d377-4145-a612-a27e56accf96.pdf

2 Likes

Shakti Pumps Q1 FY26 Concall Notes

- Company has a capex plan of double the capacity of Pumps and motors and setting up greenfield Solar Cell and modules manufacturing capacity of 2.2 GW which will be start producing by March 2027.

- Company already done capacity expansion for VFDs and Inverter from 2 Lakhs to 4 Lakhs and solar structures from 1 lakh to 2 Lakhs structures annually.

- Company is doing Solar Rooftop business and have a plan to become market leader in this segment by FY30.

- Company has also doing capex in EV business in different phases with a total plan of 250 Cr capex. For 1st phase company announced capex of Rs 114 Crores and out of which 55 Crores already invested. This business is getting good traction in recent time.

- EV business will be 500-700 Crores business when it ramps up.

- This segment is under process as Automobiles OEMs take much time to test and make product on board. Company has already send its product to different companies for testing. We will get the announcement from the company.

- In Q1 EBITDA was sightly lower, that was majorly because or increase in the price of raw material which will be further normalise.

- Company has current order book of 1350 Crores which in enough for 2 quarters and management said there will more order inflows. Company has received new 100 Crores of order in Q1.

- Company has guided for 24% sustainable margins.

- And Revenue growth guidance of 25-30% for next 3-4 Years.

- Company currently working of 60% capacity utilisation.

- Sold 17500 Units of solar pumps in Q1 with 450 Cr Revenue.

- Company done 99 Cr export in Q1 which is 15-16% of total revenue.

- Management has guided for 25% CAGR growth in exports for future and also mentioned Exports has higher margins.

1 Like

Management is having past track of being over bullish. Its a pure commodity business with no moat and fully dependent on government orders.

3 Likes

I disagree!!

First - Commodity businesses never have these kind of margins.

Second - Last year management under commit and over deliver.

Third - Management is trying to get into new business segments like EV Motors doing backward integration (PV Cell Manufacturing) etc.

4 Likes

This can be huge !

1 Like

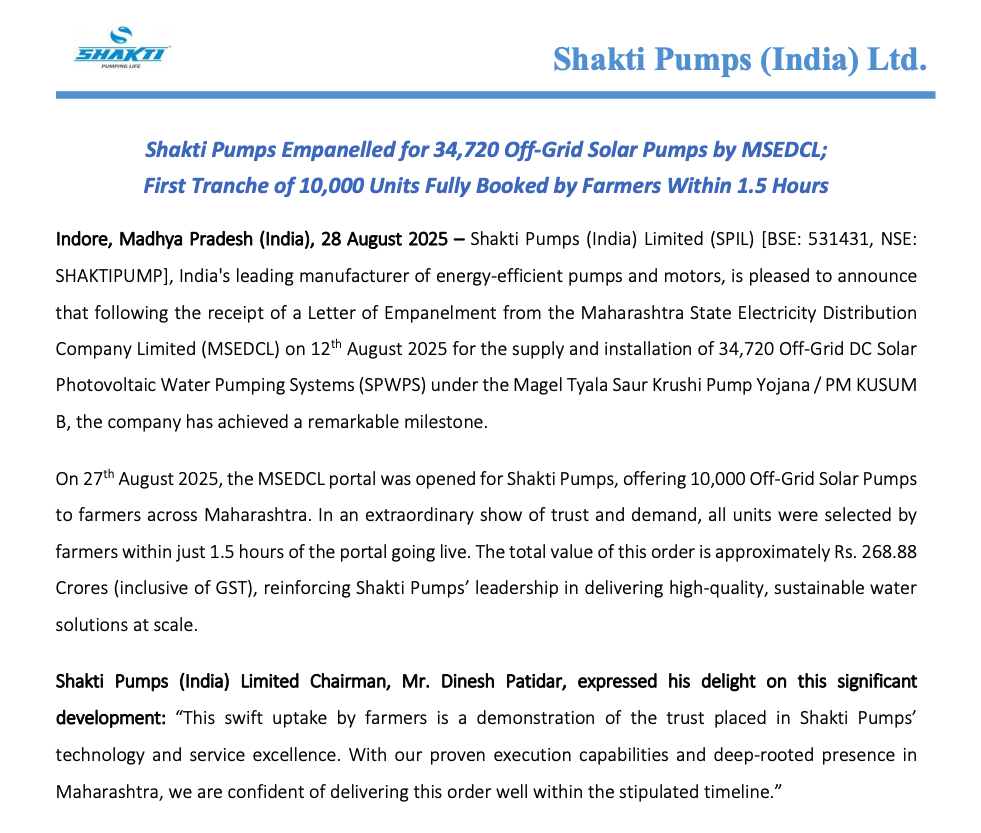

This Letter of Empanelment which means Shakti Pumps can take part in this order of 1037 Cr but not sure how much will be supplied by Shakti only. This gives the visibility for more order inflow by as per the biding system it’s upto Farmers who will select the vendor from whom they want to purchase.

1 Like

Oswal Pumps has also received a similar LoE, but for half the amount. Shakti has a significant dominance in MH market, it should do well. But keep in mind that the 60 days timeline is from the date they receive instructions from govt. to install pump at farmer’s site. This whole 1000+cr amount will not be realised in 60 days, but can take almost 2 quarters or more to be booked as revenue.

2 Likes

Agree with you as Shakti has good dominance in Maharashtra thats why Shakti received large LoE as compares to Oswal. But Oswal already has 8500 pumps order and received 14787 LoE, this makes a good visibility.

In this, regional presence play an important role if you sell Oswal has good presence in Haryana and northern side of India where bas Shakti has its dominance in Maharastra and near states.

1 Like

This LoE is progressing very productively for Shakti Pumps, out of the 34,720 pumps’ LOE that they have received the first work order of 10,000 Pumps has been issued. Now these 10,000 pumps have to be installed within the next 60 days. This gives a nice visibility for the Q3 and Q4. As per the exchange filing, this order was directly influenced by farmer’s choice of Pump provider, and Shakti Pumps managed to sell these 10,000 units within a short time span of 1.5 hours. If true, it further strengthens my confidence in the company’s brand image and after sales service in the MH market.

4 Likes