Lately I have read a lot about solar players and realised that solar pumps is a commodity product… Shakti had first mover advantage but the competition is there… ecozen, alpex, premier, and many more… there is 4-5 components to it. 50% is solar panel and then rest pump, motors etc.

Let’s see how many orders Shakti can fetch but surely has to be vary of competition.

Truth is everything about solar EPC, Cells , Modules or Pumps is a commodity product. Yet all are thriving and may continue to do so for some time due to huge TAM and tailwinds.

I went by the first line in the same paragraph where they say modules are manufactured by us while pumps are sourced from external vendors. I am assuming the later use of manufacturing that you have highlighted, means assembly.

We should clarify in either Shakti Pumps or Premier Energies concall.

If they do anything under 550-575 cr a quarter, that would be a worry as last 3 quarters, their average quarterly revenues have been 558 cr.

So even with 550 cr a quarter, their revenues will be declining.

this is cyclical stock and only seem to works around election year with gov trying to please farmers. I have exited this at 4000 after their big orders hit the news.

But the results and stock prices don’t show any short term cyclical pattern, although the execution and order flow would be influenced to some extent due to elections but I guess the major impact we’ll only see when there is a change in the current government.

But, the solar & Renewable theme is a long term theme - Related to energy security (even highlighted in this years budget). So, I guess the theme is good.

The pace, Valuations, companies to invest can change based on metrics and timing etc.

remember that mejority of the orders only come from gov as subsidises pumps… India’s farmer land holding it too low for farmers to afford a 3 lakh solar pump… as they also get free electricity so organic demand is almost non existent apart from few large farmers…

their RM prices have collapses ie steel and solar modules… that also helped them expand margin…so their margin is unsustainable…

this is clearly a cyclical stock…

any where gov is involved sector becomes cyclical …

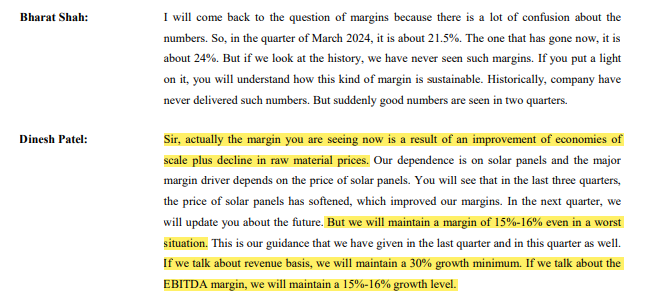

Dinesh Patel (CFO Shakti Pumps) has said that they will maintain a margin of 15-16% even in a worst-case scenario, and will continue to grow their revenue at a rate of 30% year over year

does the CEO know where steel price will go in next 6 months… or where the solar cell prices be ? If BJP gov collapses post maharastra haryana elections the orders will be canceled. For thouse who dont know the past this company dint even take the gov orders from some states because the prices offered by gov were too low.

So dont believe the CEOs and use your own logic.

This stock is not cheap alredy trading at peak of price to book value range that it got to in last election up cycle. So caution is adviced who are thinking to enter this now.

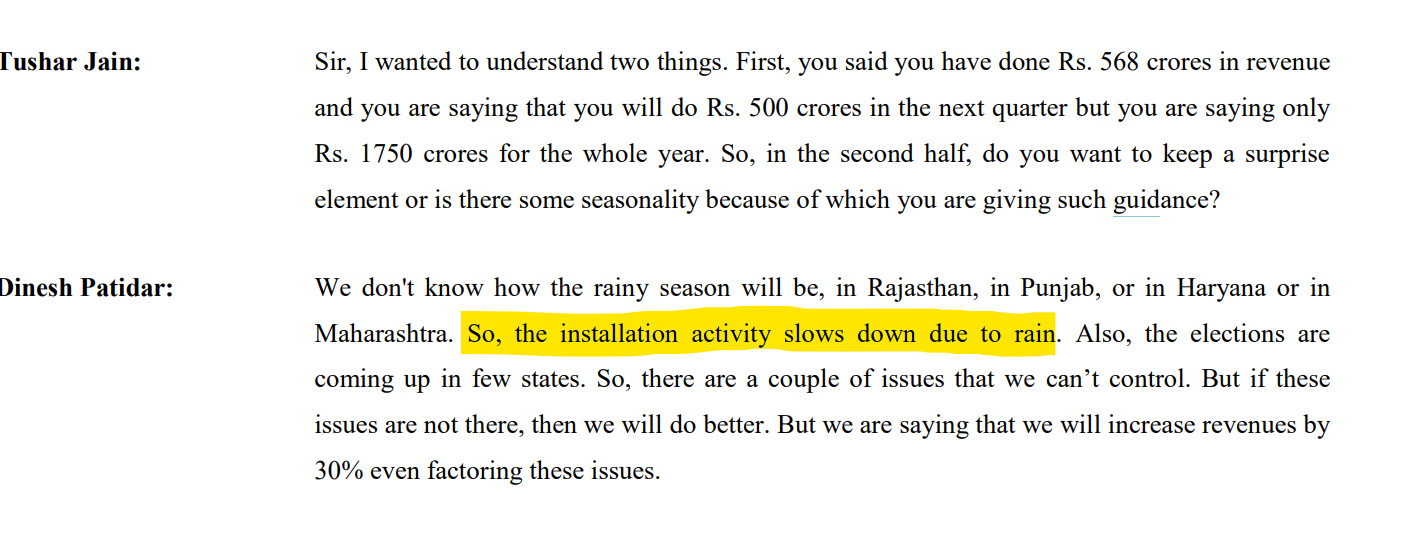

Due to monsoons, it is normal that execution is slower. Beating qoq should not be an expectation in any case. Management guided for 500cr quarter and 30% growth for the FY. So if one starts expecting more than that, then it is your own fault.

Monsoon definitely + sometimes numbers are updated with lag as state govt takes times to share data. But certainly yes, we should lower our expectation and go by 30% growth in this year

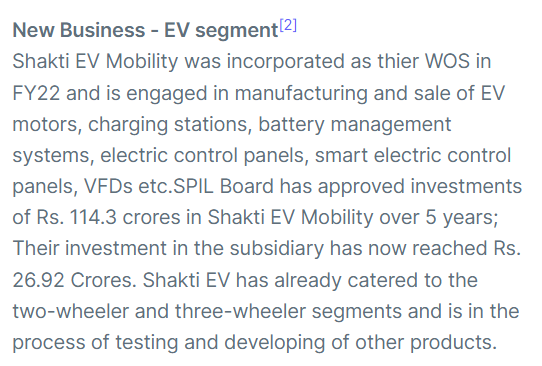

When I read the latest concall, I understood that Shakti Pump Management has been also moving into “EV Mobility” with investment of 114.3 crores.

My question is, aren’t they moving away from their core business (talking of solar pumps only), which still has huge untapped market to capture in India and at the same time much more in Europe and/or Americas. I feel like management is diversifying its focus, which might be detrimental to the innovation and brand in medium term.

Maybe someone can comment, am I right in thinking like this?

very basic understanding is missing. and fact check is very important.

farmer gets subsidy- cost is not 3-5 lacs. it is anywhere between 20% to 50%.

concept of non existent organic demand is incorrect. the organic demand is already there.

there are 4.5 cr diesel pumps already operating in India. operating a diesel pump is not free. replacement of these with solar pumps is automatic.

on the RM cost- 50% is solar modules not steel. solar module prices have declined and not set to increase even with duties in India.

the comment on margin again incorrect. revenue per pump is fixed, solar module prices have declined, even if they remain stable. margins will stay or expand.