Wonderful set of results…

GLP revolutuion is here to stay…Since GLP pen business is high margin …it is bound to bring in lot of competition over the long term.

Short to medium term Shaily is well positioned to reap in the gains.

If shaily can make some meaningful inroads into semiconductor/electronics as well.. over next few years then this multibagger can turn into durable compounder.

I have been following earnings call for last 6-7 years…Overall management is honest and conservative. They have been looking for CEO but that plan seems to have taken backseat.

People invested in Shaily, should listen to Q2 One Source Concall. DRL stuff will happen for sure but will be delayed. Also significant opportunities r coming across the world. OneSource is fully booked and is not taking any fresh booking. Quite interesting FY26 ahead.

Thank u very helpful. But I think in march patent expired. Many Durg makers are involved in drug making. But shaily have advantage but only concern is chain. If pen demand increases then definitely chain deployed in huge amount.

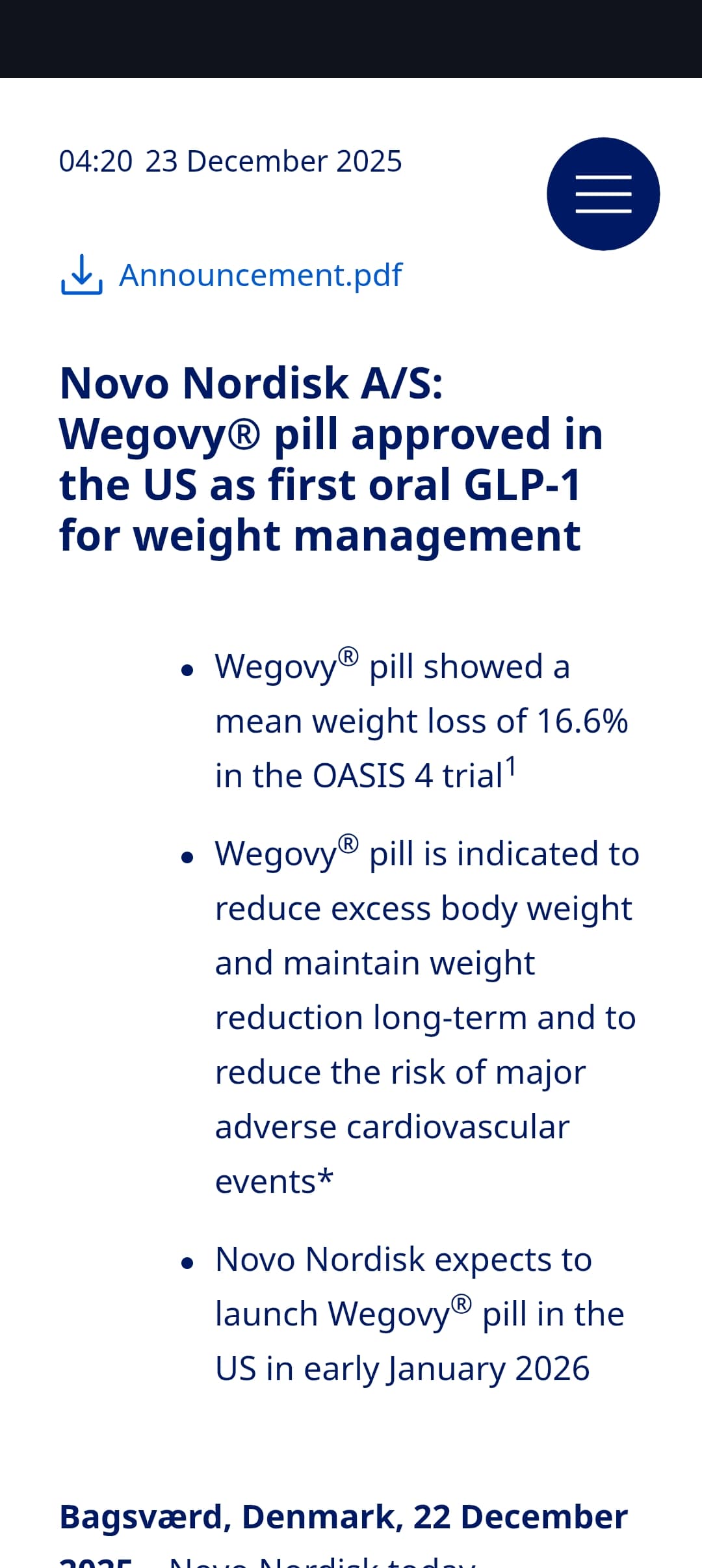

Oral pill is now launched in US. Is this the reason why stock is showing weakness?

The first GLP-1 pill is available in the US. Commencing a new era for weight loss treatment, Novo Nordisk said yesterday that it had begun rolling out its Wegovy pill—the first and, currently, the only GLP-1 pill for weight loss approved for sale in the US. Its price ranges from $149 to $299 per month, depending on the dose, making it less expensive than the injectables on the market (plus, no needles). Regulators signed off on the prescription drug last month, and it is now available at CVS, Costco, and through some telehealth providers. The company said it’s making enough to avoid the shortages its injectables suffered. Novo’s biggest competitor in the weight loss space, Eli Lilly, is working to bring out its own GLP-1 pill soon.

The primary driver of the “High-quality growth” mentioned is Shaily’s entry into the healthcare vertical, specifically for injector pens used for GLP-1 drugs (like generic versions of Ozempic/Semaglutide).

The Opportunity: The patent for Semaglutide is set to expire in 2026 in markets like India, Canada, and Brazil. Shaily has already partnered with 23-24 global pharma companies to be their device supplier.

Growth Projections: The report notes that healthcare revenue is expected to grow at a staggering 96% CAGR between FY25 and FY28.

Market Share: Shaily is positioned to capture 50-60% market share of the generic GLP-1 device market in these targeted geographies.

2. Business Segments & Optionality

Healthcare (The Star): Expected to rise from 21% of total revenue to over 55% by FY28. This segment has higher margins and higher entry barriers (patented technology).

Consumer & Industrials: This is the “steady” part of the business, supplying components to global giants like IKEA, P&G, and GE Appliances. It is expected to grow at an 18% CAGR.

The “Optionality”: The report highlights potential new growth from the consumer electronics and semiconductor space, which isn’t fully baked into the current price yet.

3. The “Limited Valuation Cushion” (The Warning)

This is the part of the title that relates to your previous questions about P/E multiples.

Sky-High Multiples: Shaily is currently trading at a P/E of ~68x to 70x.

Priced to Perfection: The market has already factored in the 75% EPS CAGR projected for the next three years. If there is any delay in generic drug launches or a shift in the market, the stock has no “cushion” to fall back on.

Multiple Compression Risk: Even if the company performs well, if the growth slows down to “normal” levels (say 20-25%), the P/E multiple could contract from 70x to 30x, which would lead to a significant drop in stock price even if earnings are growing.

4. Key Risks Highlighted

The “Oral Pill” Threat: Novo Nordisk recently launched an oral weight-loss pill (Wegovy pill) in the US. If patients prefer pills over needles, the demand for Shaily’s injector pens could be lower than estimated.

Regulatory Hurdles: Any delay in FDA or local regulatory approvals for the generic drug manufacturers (Shaily’s clients) would push back the revenue timeline.

Promoter Selling: The report likely notes recent block deals where promoters or early investors (like Ashish Kacholia) may have trimmed stakes to take profits at these high valuations.

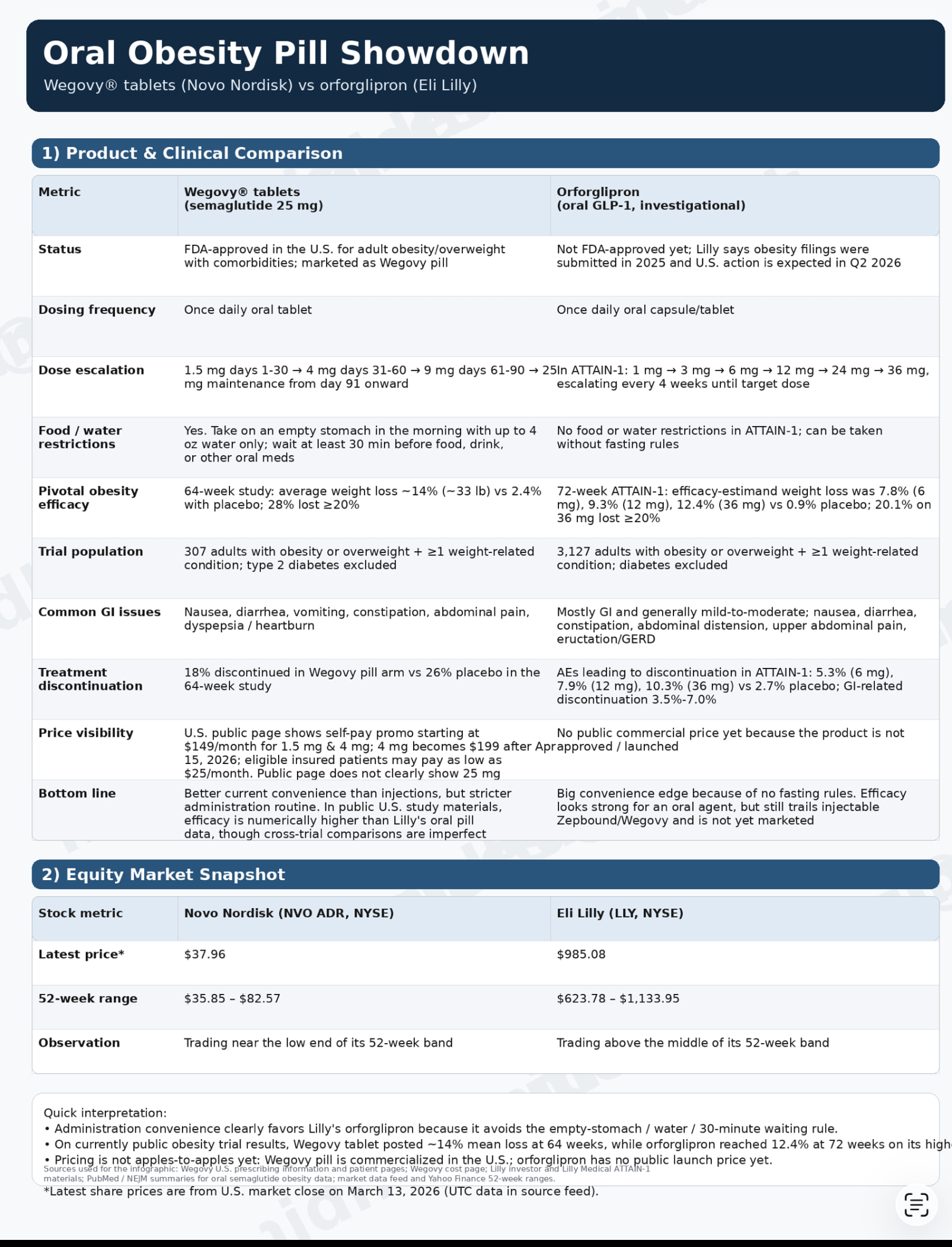

Been studying the impact of Oral GLP1 on injectibles. It seems to boil down to

Convenience

Price

Efficacy

And the relative importance of these might differ for different type of user.

Is it possible that injectibles remain much cheaper than Branded (patent protected pills) in markets like India, Brazil, China and most other large ermerging markets for a long time?

Current pricing suggest a big gap in favour of injectables:

1. 27% YoY revenue growth in Q3; 32% increase on 9M basis. 43% improvement in EBITDA YoY

2. Setting up a facility in Abu Dhabi for manufacturing medical devices.

Approx. 300 crore investment

Capacity: ~75 million pen injectors p.a.

Operational timeline: Q4 FY28

Looking at high speed lines, each line should be capable of producing 25 million pens/ devices p.a.

Will increase pen injector capacity from 80 million to 150 million

3. Rationale of Abu dhabi – Importing equipment, hiring some manpower from Asia regions. Hiring expats from Asia regions where tax rates lower. Higher expenses with expats working in India. Difficult to justify the cost of bringing in their capabilities.

4. Capacity expansion

1st pen assembly line (25 mn pens) to be completed next week and commercial production likely by April; 2nd line likely to be completed by July end

Expansions are backed by commercial contracts. 50 million almost fully backed by commitment and likely to be fully utilized in 18 to 24 months

Abu Dhabi unit also supported by 60% capacity commitment

At higher scale, fully automated operations would result in operational efficiencies, resulting in improved margins.

5. Segment wise deep dive

Healthcare

139% growth YoY

2 new customers were onboarded in the fast growing GLP-1 segment

Signed 2 new contracts with global companies for the manufacture and supply of pen injectors

Guidance of 30 million pens at the start of the year broadly remains.

India launch: Customers using both Harmony and Neo platform. Harmony platform to go live in March and Neo 1-2 months later.

Margins to improve in Q4, but full impact of the high-speed lines will be seen Q1 onwards, resulting in further increase in margins.

Can expect Sequential improvement in margins for next 2-3 quarters.

Industrial

87% growth YoY

Supply of Power Tool components from a new customer

Consumer business degrowth of 13% YoY

Demand slowdown in Europe, US. Once economy improves should see a rebound.

With 18% tariff, India likely to have advantage in terms of exports to US

Consumer electronics business– See it as a Very scalable opportunity, margins likely to be better than home furnishings; aim is to participate in high precision, high complexity products (with entry barriers) – combinations of metal & plastic.

Semi conductors– Chip manufacturing cos not fully operational yet, two large customers likely to start commercial operations next year. Supplies to start next FY. Small quantity likely in near future

6. Exports contributed 71% of total revenue

Canada – Have 65%+ share. Anyone who receives approval very likely to use Shaily devices

UK – Pipeline looks strong (7 new projects) to grow substantially over next 2-3 years

Turkey , Brazil – Likely to start contributing by Q1 – Q2 next FY .

7. ROCE at 38% ; ROE at 29%

8. Other points

Strengthening Senior Management team - Appointment of Mr. Joe Kam as the Chief Operating Officer (Healthcare)

The oral weight loss drug battle , should have profound implications for players like Shaily. With 17% efficacy this can cannibalize the injectable version . Most of the generic players waiting to launch their versions of Semaglutide injections might also have adverse implications if the pills get faster roll out nod in India

The article also mentioned that the pills attracted new users rather than those switching from the injectables. But I also don’t see why someone on injections would not switch if the efficacy and price are ‘good enough’.

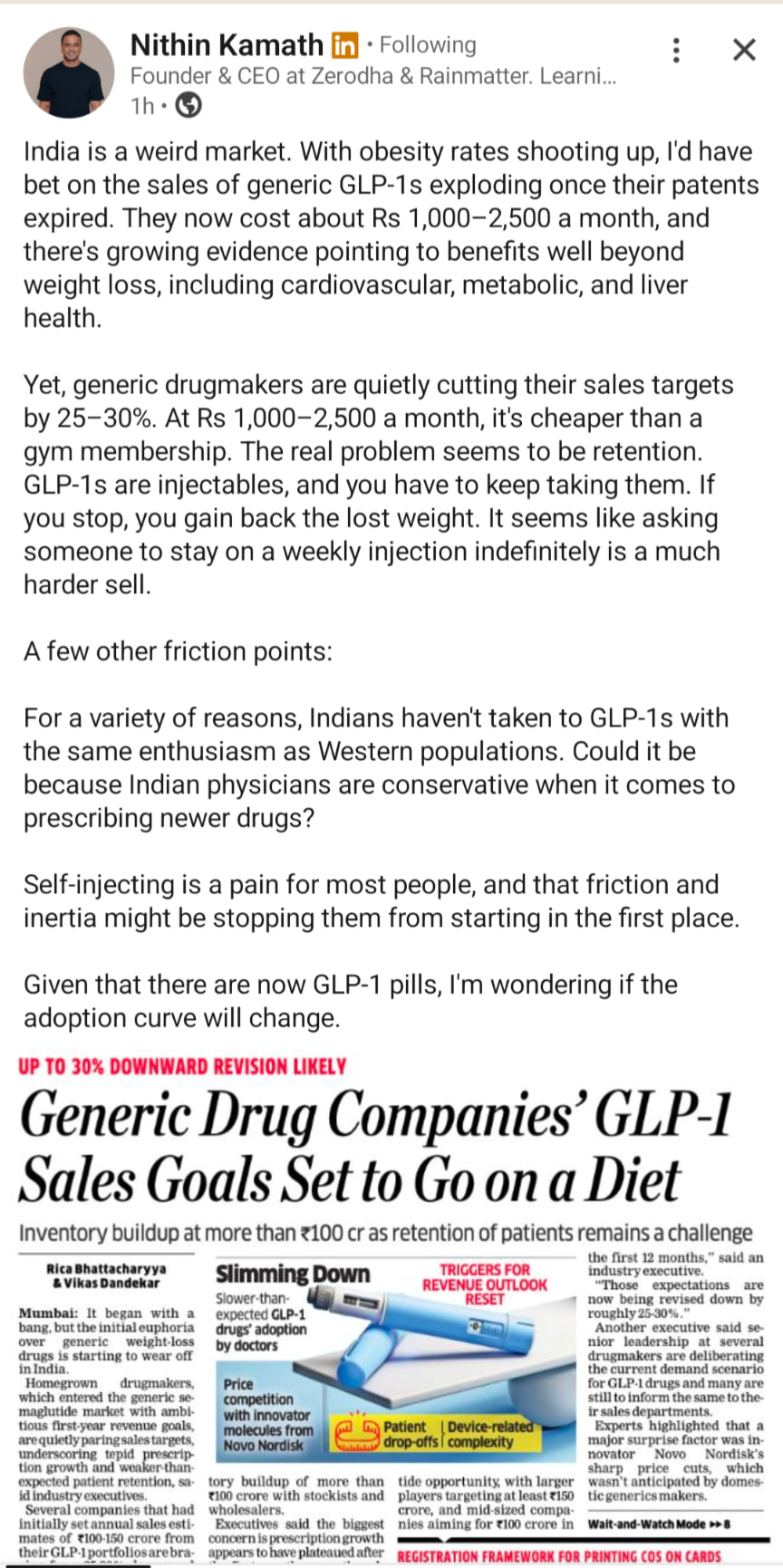

Sales of GLP-1 drugs in India don’t seem to have taken off as expected.

Refer this article and Nithin Kamat’s views:

It kind of strengthens my wariness about Shaily’s prospects since it rides on the willingness of Indian targets to keep injecting themselves (as against taking orals or not taking GLP-1s at all).

While this is true, these medicines are also out of stock in my area. Plus Shaily is also exporting, so me might still see growth. But I am worried about the recent stake sale by the promoter. It might actually not grow as much as anticipated.