I think the marketplace right now is between the Sales force of the company and the potential clients. After the initial relationships are built and then this platform kicks in their SGNA should go down - only for the B2B trading vertical

for the Services vertical - it will be a customised offering so the platform might not help and sales should come from the B2B sales force stationed at or in-around the service center

1 Like

completely agree. the whole game is of Bargaining Power which will come into play once they reach a critical volume. Similar to any SAAS startup, the network effects is the moat.

1 Like

Some people are talking about low EBITDA margins, one should take into account that this is a pass through business where the margins are always low (say your petrol pump business is pass through), if someone wants to calculate the EBITDA margins in real terms , he/she can do it on net revenues(gross profits are net revenues) not on gross revenues. Finally when it comes about moat in trading business, the only moat is the volume, the bigger you become the tougher you make it for others to enter…

8 Likes

In general, i would suggest to our members to read the book " The world for sale", its an engaging read which actually outlines how does trading happens on the metals across economies

5 Likes

Can someone help me with the address of Pune service center. I want to visit it.

1 Like

Please share insights here as well after your visit.

3 Likes

do share the insights

They are neither receiving calls nor responding on mails. Surprising and shocking!!!

1 Like

that’s unexpected. Can you go to their office location and check? Also, which other cities have operational service centers now?

SG Mart -

Q2 FY 25 results and concall highlights -

Q2 financial outcomes -

Revenues - 1820 vs 506 cr, up 259 pc

EBITDA - 15 vs 11 cr, up 33 pc ( margins @ 0.8 vs 2.3 pc YoY, due steep correction in steel prices in Q2 which led to inventory loses to the tune of 17-18 cr )

PAT - 16 vs 9 cr

H1 financial outcomes -

Revenues - 2960 cr, up 350 pc

EBITDA - 40 cr ( margins @ 1.3 vs 2.3 pc )

PAT - 42 vs 10 cr

Cash on books @ 1080 cr

Total active customers at the end of H2 @ 535 vs 315 at the end of Q2 LY

No of active suppliers @ 75 vs 21 YoY

SG Mart offers a wide range of products, now encompassing more than 27 product categories, and more than 2,500 SKUs. These categories include construction steel products like TMT Rebars, HR Sheet, Welding rod, Binding wire, mesh net, tapping screw and barbed wire, among others. Additionally, in response to the increasing demand, the Company has introduced tiles, cement, bath fittings, laminates and paints

Company did volumes of 3.5 lakh tons in Q2. For current FY, company aims to maintain an avg of 1.2 lakh tons / month. Next yr, they aim to take it to 1.6 lakh tons / month followed by 2.5 lakh tons / month for FY 27

Steel price volatility + Weak construction activity in Q2 did hurt company’s business in Q2

Company indulged in steel trading while procuring steel not only from local manufacturers but also the imported steel

Currently, company is operating 3 steel processing service centers @ Ghaziabad, Pune and Raipur. By Q3 ending, 2 more service centers should be live @ Pune and Dubai. These r relatively higher margin businesses

Aim to start making Solar panel frames at their service centers wef Q4. This is an area with strong tailwinds, huge demand and no presence of any organised players

One more service they intend to add at their service center is to start making Purlins ( steel structures used to add strength to roof structures )

Company has identified more places where they will open their service centers over next 1 yr. These are - Chennai, Jaipur, Indore, Siliguri, Hyderabad and Ahemdabad. Similarly for FY 27, they ll identify places and operationalise more service centers across India

Capex lined up in current FY to open new service centers @ 100 cr. Have earmarked 300-400 cr for next FY to open even more number of service centers.

Avg inventory days for Q2 were 8 days. As the service center business ramps up in 1-2 yrs, this is slated to increase

Company maintains its guidance of 17000 - 18000 cr of topline by FY 27 with EBITDA margins of 2.5 pc. Also expect margins to recover to > 2 pc in Q3, Q4 FY 25

A 15 pc crash in steel prices is once in a decade kind of event and still the company could come out with 1 pc kind of margins. This should give some confidence to investors in their guidance of 2.5 pc for the long term

Sticking to their full yr guidance of Rs 6500 cr in revenues

Company does maintain a strong quality control team as company procures from different sources and labelling a lot of products under their own brand name

Company has also started testing waters with Zinc procurement and distribution. Company is going very slow in this segment. They will only scale up once they have sufficient experience and confidence in this relatively new area of operation

By FY 27, company expects 40- 50 pc of their revenues to come from service center businesses. Currently their contribution is around 20 pc

The cash that the company is sitting on ( aprox 1050 cr ) will all be used to finance the Capex ie - Opening new service centers + to service the company’s inventory requirements

Disc: holding, biased, not SEBI registered, not a buy / sell recommendation, looking out for EBITDA margins recovery before adding more

10 Likes

thats wired but you can try few more time

Does anyone have any take? on the shareholding pattern of the company … it seems that there has been some internal family transfer of shares… but summing up that too doesn’t get back to the previous percentage. I think the dilution might be because of the exercising of some warrants.

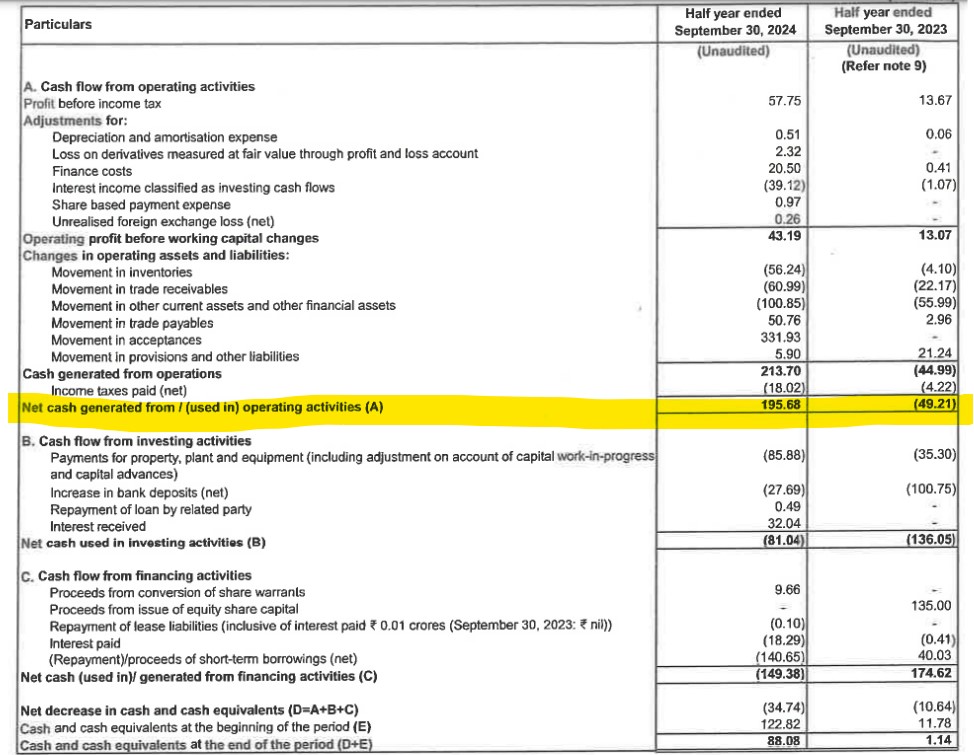

Any idea on Cashflow from Operations?

I do not have the cashflow numbers for the last Quarter, but the one I have is from March and it shows negative cash flow from operations. Looking further this looks like a situation of high trade receivables and inventory.

I think this has been address but if someone has more information on this, I would like to know more.

1 Like

Read the Q2 note

https://www.bseindia.com/xml-data/corpfiling/AttachHis/fecb7c9e-79d1-4876-b185-67f04e0273f6.pdf

1 Like

Can they maintain sustainable EBITDA of 2.5% going forward?

Or become an cyclical business like steel producer ?

What will be PE ratio after some scale?

Honest opinions from experts ???

Can SG mart fall under new age business , i mean is it a disrupter ? and a very high growth business taking market share from peers and is it profitable ? All these qns have positive answer. Last qtr they have booked inventory losses still bottom line was positive shows the power of business model.when all tech backed new businesses burning cash , they are making profit from inception even in this situation{ steel price crashed more than 10% in a month, management says once in a decade event}.What happens if they book inventory profit in coming qtrs ? second point is management said they were in negative wc cycle 2nd qtr.this is hugely positive to me{ may not be the case going forward as they scale up}. so business wise everything is in place, can management scale up the business is KEY thing to watch.

INVESTED AND BIASED.

Pardon me for my poor english.

10 Likes

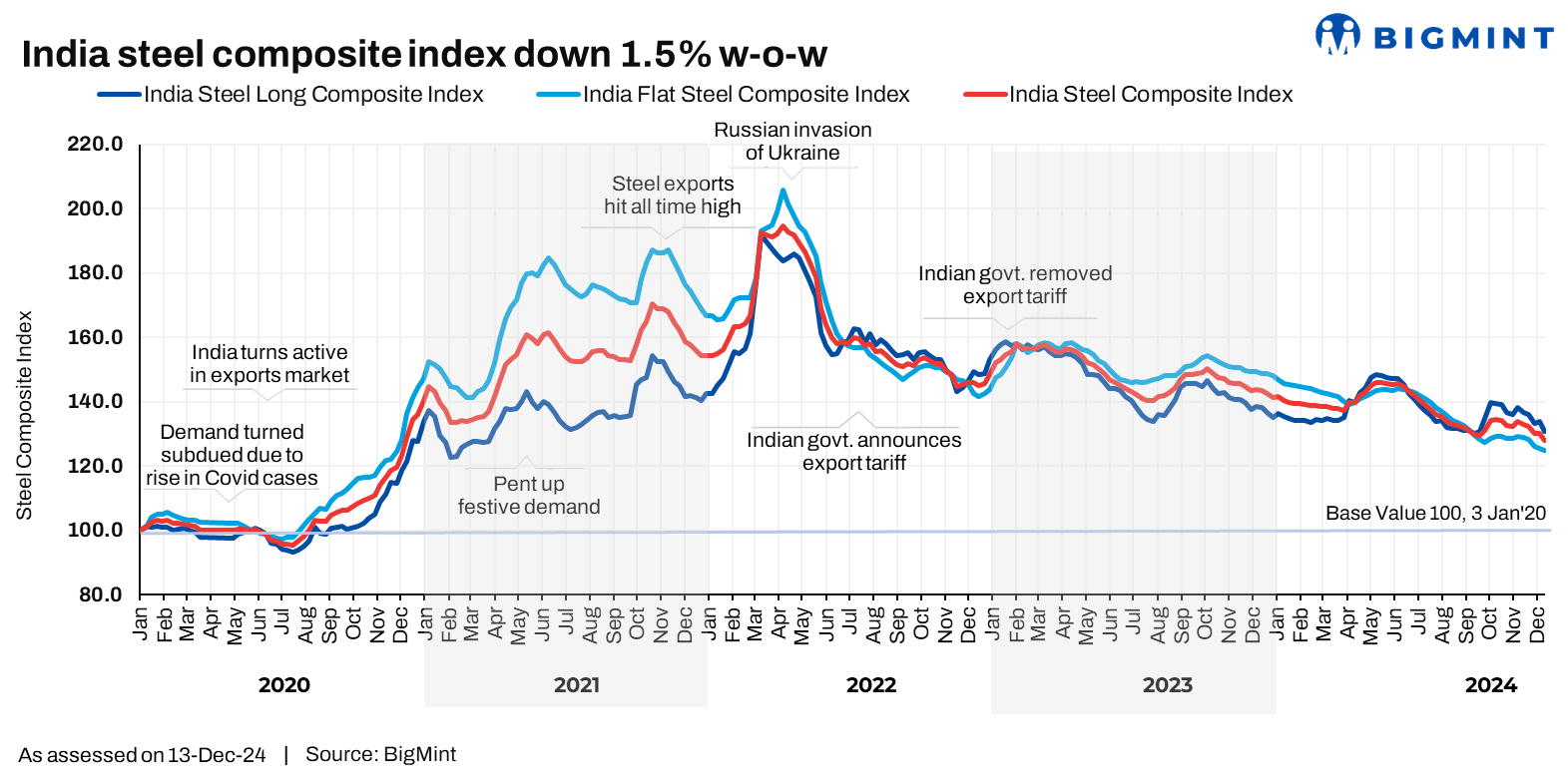

Doesn’t look like any price recovery has happened yet. Looks to be another tough quarter for SG Mart.

Indian steel prices are nursing the blues and how. The India Composite Steel Index dropped 1.5% to 128.1 points at closure on 13 December, 2024. This is a 12-week low but importantly, these levels for the past many months are groveling at four year-lows.

Several factors contributed to this down syndrome.

- The trend of lacklustre demand continued. Longs players are suffering in particular with the government reigning in its infrastructure push.

- The liquidity crunch, as several state elections loom nearer from next year, are adding to the woes. Even as end-buyers feel the liquidity crunch, in a cyclical pattern, little off-take is tightening the funds availability with manufacturers.

- Early December saw a tier-1 mill putting its caster on maintenance which led to a tightness in rebar supplies, which impacted supplies but had no effect on prices though.

6 Likes

Isn’t steel industry cyclical?

How’s SG Mart management able to give 2-3 or 5 year guidance ?

If they are saying 18000cr by FY27, that’s a CAGR of around 85%. Given that the Indian economy as a whole is not doing that well, can we conclude that the guidance is a bit optimistic?

The ambitious guidance should have reflected in the stock price but given that the stock hasn’t moved much in a year indicates there are lot of uncertainties about the execution.

5 Likes

Steady low prices should not affect margins if what they said is true even though it will result in lower revenue . Sudden steep rise and fall in steel prices can affect margins but this chart does not show steepness compared to last quarter .

2 Likes