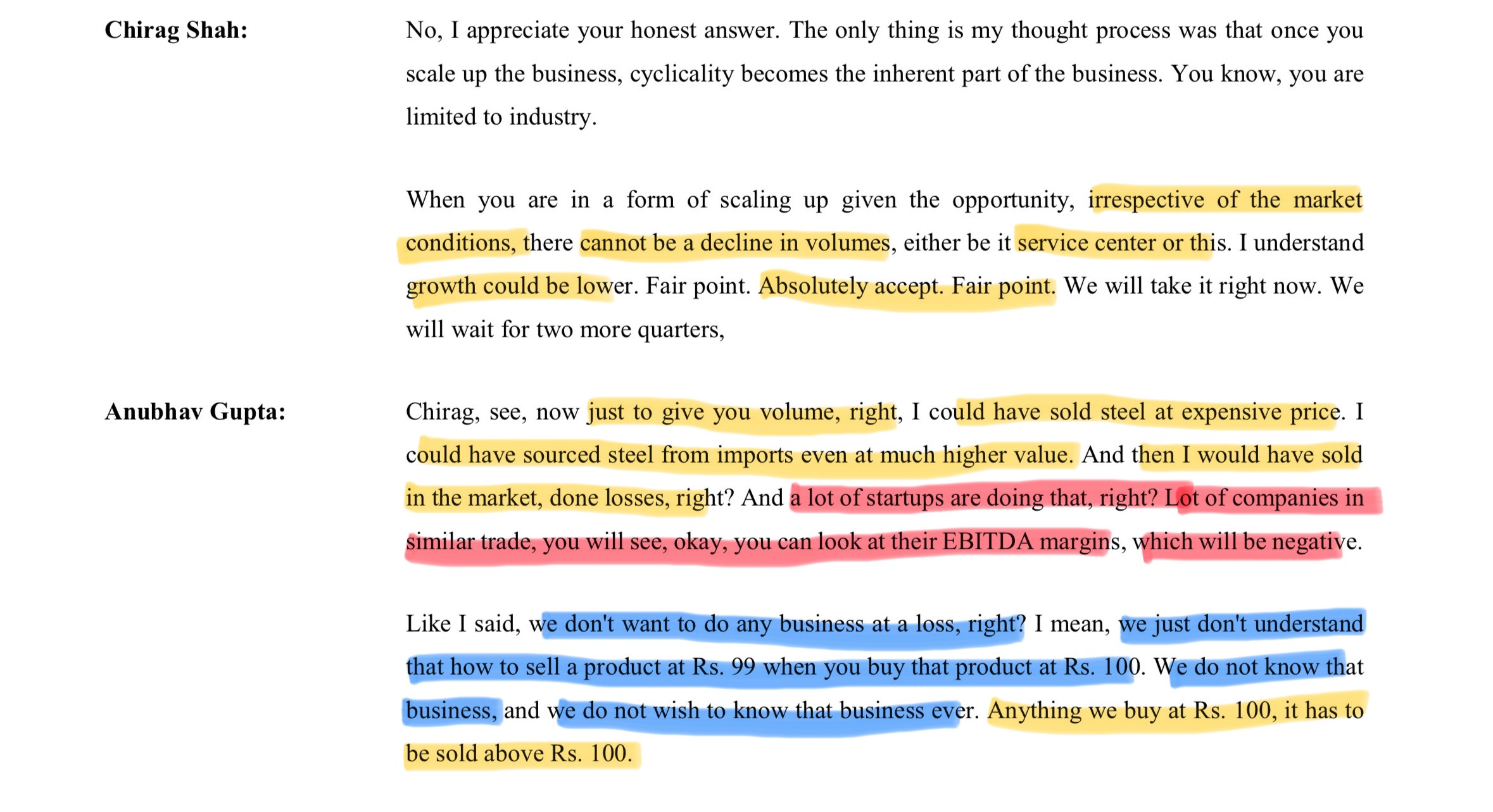

Yes the B2B segment was 50% down because of unavailability of domestic steel. Management is confident that domestic steel production will ramp up in H2 and will be enough to meet the demand.

2 Likes

How come they are facing unavailability of domestic steel when production is up 11% along with an 8% uptick in demand. Source - India's April-June finished steel imports fall nearly 30% as China, Japan shipments slow | Reuters

And how come their peers are not facing these strong headwinds? Looks to me like their claim of becoming the preferred buyer of steel due to their large purchasing power is in the mud.

See JSW One’s GMV growth rate

3 Likes

To me it seems like the exports have fallen by a greater percentage (-28.8%) compared to the rise in domestic steel production (11%).

Also JSW One has advantage of inhouse steel production so the impact of above things may have been minimal.

See, the pie is large and JSW One may get the bigger pie than SG Mart but in the end, what matters is the incremental growth rate of revenues and its flow into EBITDA and PAT. As along as that is positively achieved, I am happy with my investment.

With the all the cash it has and management background/ guidance, i would give it a year or two to perform before taking a decision.

Dis: invested and may be baised.

2 Likes

The above question is answered in the Concall by management:

At the end of the day it’s a commodity business. They simply cannot escape/ insulate from market conditions, they can only manage and minimize losses.

They are trying to achieve economies of scale and become bigger middle player in the industry.

6 Likes

For record keeping purpose:

Rohan Gupta, acquired 35 Lakhs share from open market. His share increased to 17.70 from 14.92.

Disc: Invested.

2 Likes

How is Shankara Building products different from SG Mart?

Shankara can be a customer of SG mart. Check the previous threads it was answered by management last year I think

Disc: invested

Following based on Copilot -

Infra.Market vs SG Mart Limited comparison

What each has been doing to grow

Infra.Market

- Category breadth and private labels: Building a house-of-brands across core construction materials to lift attach rates and margins (qualitative).

- M&A integration: Strengthening presence in paints/panels/RMC to deepen project coverage (qualitative).

- Tech-led procurement and logistics: Data-driven sourcing, pricing, and route optimization to reduce cost-to-serve (qualitative).

SG Mart Limited

- Topline ramp-up: TTM/FY25 revenue reported around ₹59,475 million vs ~₹27,145 million in FY24, showing very rapid growth prints on the portal feed.

- Profit scaling with low margins: Net income up to ~₹1,095 million TTM while operating margins stay ~1.84–1.89%, pointing to volume-led expansion rather than margin expansion.

- Balance sheet strain: Negative free cash flow in FY24 and TTM FY25 despite profits, suggesting WC absorption or growth capex; check AR for specifics.

Business model explained simply

- Infra.Market: One-stop supplier for builders. It buys or makes materials (often under its own brands), aggregates demand, and delivers fast and predictably. Money is made on spreads and better margins from private labels, plus efficiency in logistics and procurement (qualitative).

- SG Mart Limited: Public filings show a fast-scaling revenue base with thin margins and notable financing dynamics. Given portal classifications and variability, ground truth for the model, segments, and revenue sources should be taken from the FY24 Annual Report and MD&A.

Red flags and caution points

- Infra.Market (qualitative):

- Working capital/receivables risk: B2B materials with SME credit can stretch DSOs.

- Integration complexity: Multi-category M&A needs tight controls, QA, and warranty metrics.

- Margin sensitivity: Thin contribution can be whipsawed by input/freight inflation.

- SG Mart Limited:

- Negative FCF despite profit: FY24 and TTM FY25 show negative FCF, implying WC intensity or capex/funding needs—probe cash conversion cycle, borrowings, and interest costs.

- Very low margins: Operating/EBITDA margins ~2% leave little buffer for shocks; pricing power may be limited.

- Data inconsistencies across portals: Industry classification and abrupt share count changes warrant deeper verification in AR and notes; rely on audited FY24 report for segment reality and related-party checks.

Management commentary and focus (recent)

- Infra.Market: Emphasis on margin quality, private-label mix, and category/geographic scaling ahead of listing (qualitative).

- SG Mart Limited: Use FY24 Annual Report for management discussion and outlook; cross-check stated strategy, risk factors, and financing plans against the sharp growth and cash flow profile shown in the data feed.

Market share changes

- Infra.Market: Likely expanded in India’s organized construction-materials B2B through category breadth and network scale (qualitative).

- SG Mart Limited: Market share isn’t disclosed in the portal data; infer from segments in the AR and compare to peer set within the same industry classification to establish share trends.

Stock performance outlook

- Infra.Market: Pre-IPO. Post-listing, watch gross margin trajectory, private-label attach rate, DSOs, and cash conversion. Execution quality will drive valuation multiple (qualitative).

- SG Mart Limited:

- Positives: Revenue momentum, rising net income.

- Risks: Negative FCF, wafer-thin margins, interest expense trends, and any reliance on non-operating income items.

- Call: Favor caution until AR confirms segment economics and cash discipline; monitor whether margins and FCF inflect positively without over-leverage.

SG Mart quantitative data

The figures below are from a public financial data portal. Validate against the audited FY24 Annual Report for investment decisions.

| Metric | FY23 | FY24 | FY25 TTM |

|---|---|---|---|

| Revenue (₹ million) | 26,829 | 27,145 | 59,475 |

| Gross profit (₹ million) | 739 | 1,725 | 1,860 |

| Operating income (₹ million) | 613 | 1,080 | 1,107 |

| Net income (₹ million) | 609 | 1,034 | 1,095 |

| Gross margin (%) | 2.75 | 2.94 | 3.17 |

| Operating margin (%) | 2.28 | 1.84 | 1.89 |

| Profit margin (%) | 2.27 | 1.77 | 1.87 |

| EBITDA margin (%) | 2.30 | 1.88 | 1.93 |

| Free cash flow (₹ million) | -752 | -5,485 | - |

| Shares outstanding (diluted, million) | 82 | 117 | 118 |

Sources:

Notes on segments, capacities, and volumes

- SG Mart Limited: The public portal does not reliably break down product segments, capacities, or volumes. Use the FY24 Annual Report’s MD&A, segment reporting, and plant disclosures for capacities and volumes, if applicable.

- Infra.Market: As a private company, segment volumes/capacities are typically disclosed in IPO filings; not publicly available yet (qualitative).

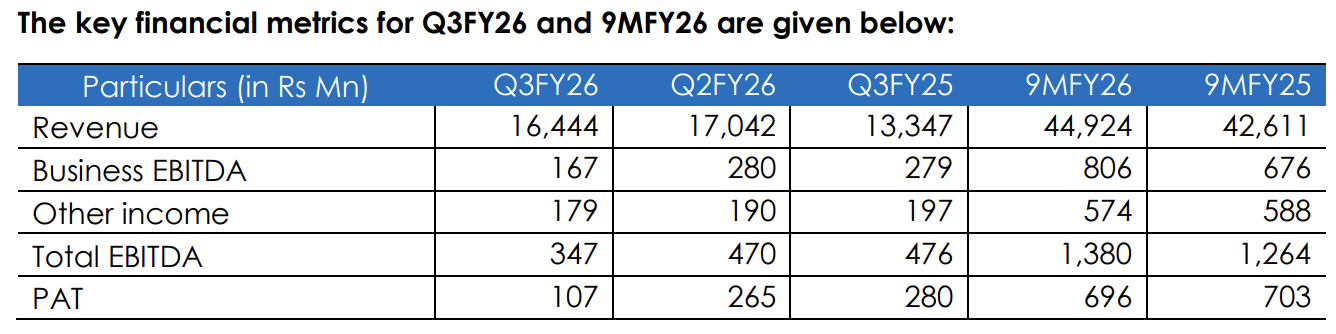

Detailed investor presentation. Though a very subdued result this time.

EBITDA has not followed volume as indicated by anubhav several times…

One more quarter of over promises and under delivery.

4 Likes

Yes starting to become a pattern now. Why do they need to raise expectations so high even though they have all the cash they need for long term survival.

Disc: invested with fading conviction. Will decide on future after investors call.

1 Like

Q2FY26 → Again a disappointing set and Q3 will be similar. I guess the floor for the price will be 300-330 ( the price at which promoter bought 100 crs shares of the company) My thoughts on the concall:

- They openly acknowledged that there was a mistake due to excitement and the guidance in shorter term might be hampered but longer term, they will meet the targets. This is the management whom i am willing to give some slack. Coming into public and accepting mistakes is not easy, they are facing and answering the tough questions(considering their background of being from a big corporate group)

- My sense is management is kitchen sinking all they can in terms of cost in Q2 and Q3 . So, Q4 should see improvement in terms of margin.

- The business is new and not easy ( as the margins are wafer thin and you will be impacted by macro factors), the earlier success and quick scaleup might have given a feeling on invincibility. Sanity seems to be prevailing and hope they will keep their excitement in check and follow practical guidance from now onwards

- What is like is their is constant investment and progress in all the business division. The TAM is humongous, once the positive flywheel starts this can be very big. There is definitely a space in the market for a business like this. The movement is in the right direction, but not with the pace that management set the expectations

Disc: Started Investing from last 3-4 months in the counter. Happy to wait till H1FY27, post that will consider my position based on the execution.

1 Like

Point number 2, what exactly do you mean by kitchen sinking all the costs they can?

I still remember back in 2020-21 this same management promised the moon in Apollo Tricoat volumes and then managed to over deliver !

From that to the current sad state of visibility shown during the concalls of all the smaller listed group cos (Apollo Pipes/SG Finserv/SG Mart) is quite unfortunate.

Across multiple concalls, SG Mart’s management has shared such high sales and volume estimates, even for quarters nearly concluded, only for actual results to fall well short. And to add to the agony, calling inventory and forex gains as service centre pivots or sustainable margin improvements merely stretches credibility further.

6 Likes

In concall they mentioned accounting all expenses like marketing expenditure in Q2 and Q3. Both quarter will be similar in revenue and EBITDA hence they want to account next one year costs now which will make next year better. I would take the word ‘better’ with a pinch of salt. Management is giving once in a lifetime excuses from past 4 quarter now.

Disc: invested and unable to decide whether to add or subtract to the position.

5 Likes

Not a great result by SGMart! Definitely not what I was expecting.. Would like to hear others thoughts as well.

Wondering why the stock is up 5% , even ff the results are bad :(

The results were announced during market hours and the stock moved up?