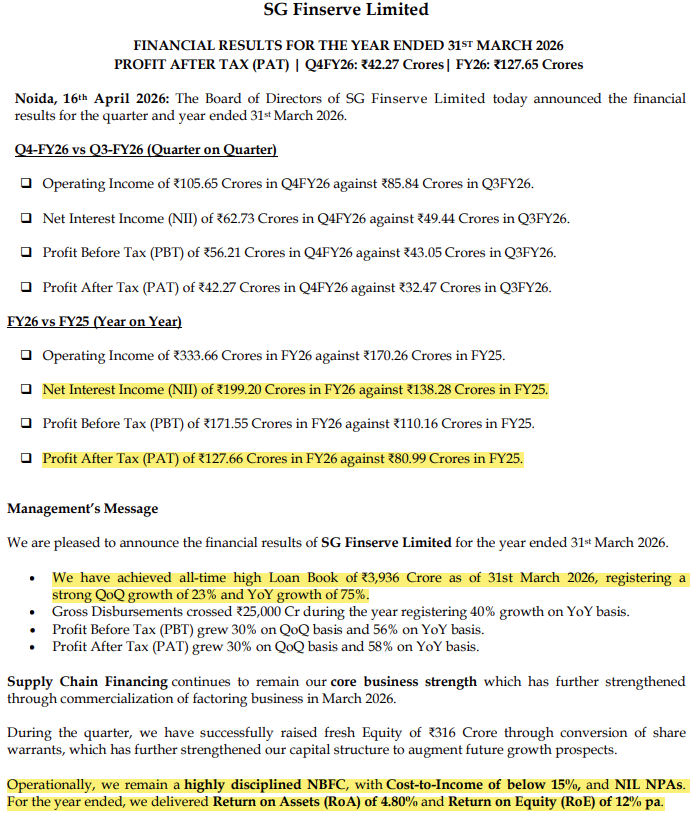

Doubles YoY loan book in Q3

8 Likes

Excellent result :

2 Likes

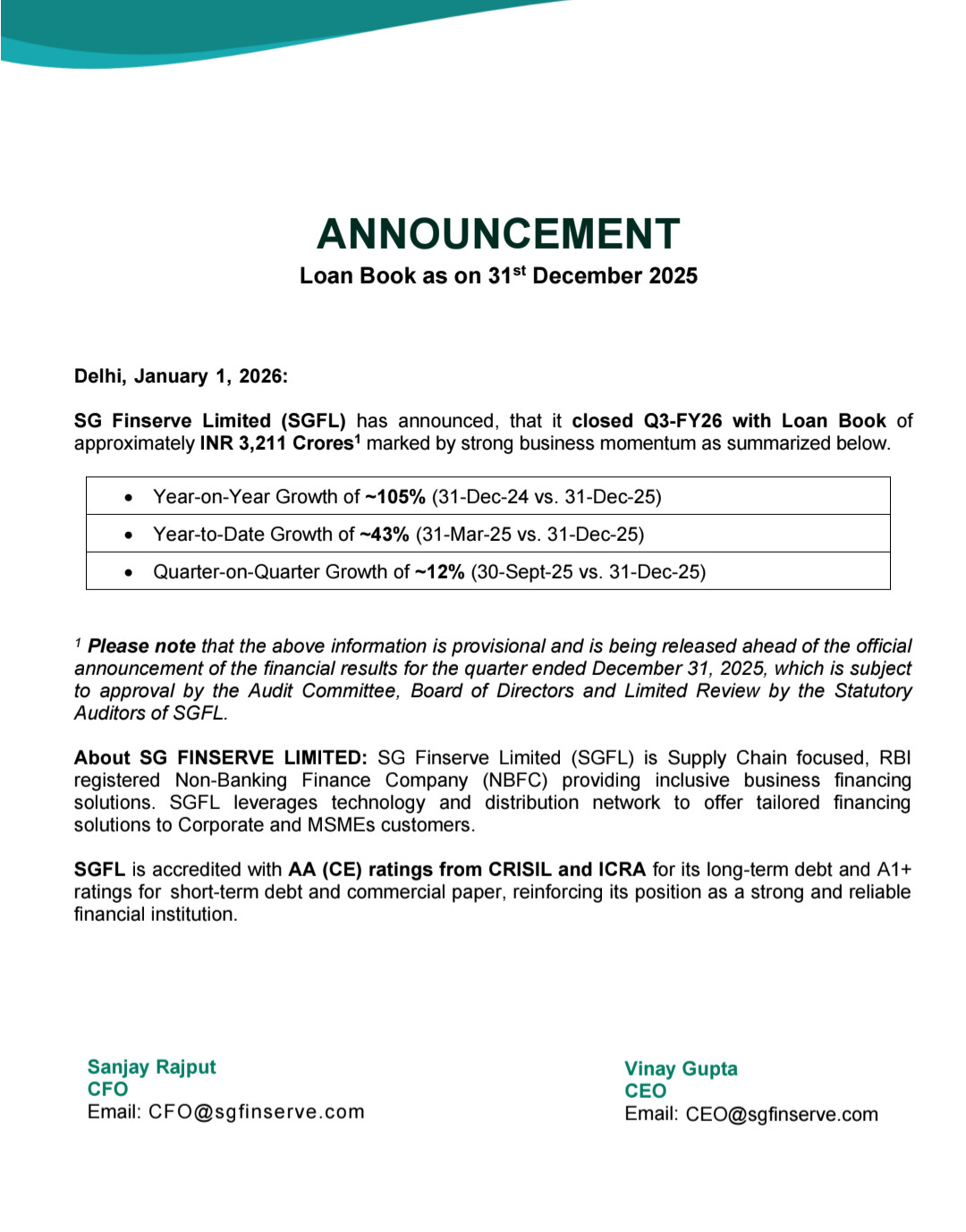

Based on these projections - SG fin results are one quarter behind on PAT number and interest income number

Also the prefrence share hasnt been converted yet - so that part is also delayed a bit for book value accrual.

on loan book and debt on books, the numbers are all tying with september number

so ill fairly assume - they are one quarter behind

2 Likes

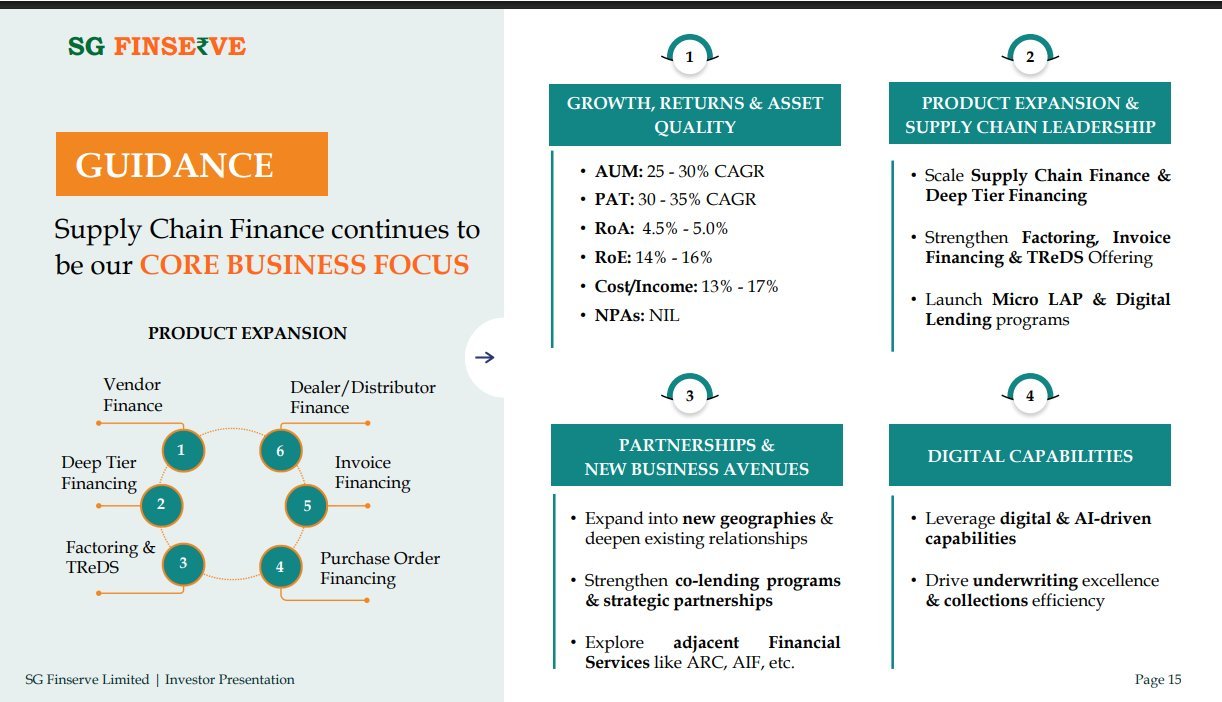

In my view, management has materially deviated from their previous guidance. They previously guided for 6000cr of AUM by FY27. Now they are saying 7500cr by FY30 and 20% CAGR growth from current levels which means 3500cr AUM by FY26 (vs 4000cr guided previously) and 4200-4500cr by FY27 (vs 6000cr guided previously)

And also announcing new initiatives (AIF etc) while they are going slow has spooked markets! They kept clarifying these are all future initiatives and nothing is planned now - If not then why announce them?

Results were decent but they have now reset expectations much lower.

2 Likes

They should provide guidance only for one year ahead, not beyond that. Although the results are strong, investors are unhappy again due to unclear and inconsistent guidance.

4 Likes

i totally agree and this changes all the numbers in projection. hence growth guidance is now much softer and definitily needs to be re-looked for investment for next 5 years

2 Likes

INR 337.5 is the breakeven price below which not subscribing to warrants is better than subscribing to warrants at 450Rs and paying 75% of balance amount.

Believe any price below INR 340 is attractive for long term (notwithstanding the drastic drop in future estimates)

2 Likes

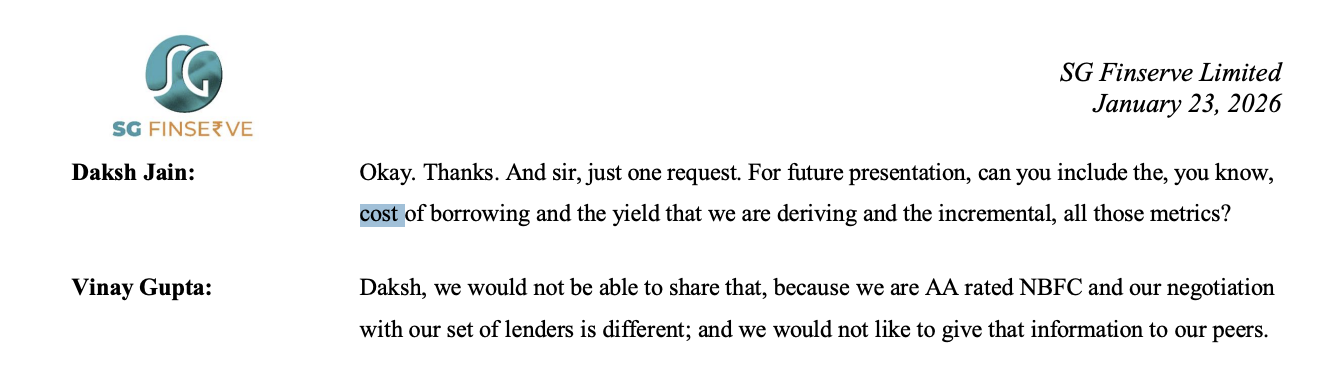

Does anyone know the cost of borrowing for SG Finserve?

I don’t think so they made it as public information. Just to add more I think this is not cool. What difference would it make! Every NBFC does release this information

2 Likes

its easy to decipher - they pay around 8.5%

2 Likes

Thanks for that. But could you please explain how you deciphered it?

Divide this quarters interest(which is on higher side because they have higher ending debt balance for december) with last quarters ending debt balance…you will reach around 8% annual rate…for the sake of safety I said 8.5%.

Why I am doing like this - because I am assuming they will have to pay interest on atleast last quarter outstanding as it will remain unpaid throughout quarter ( please note , they get repayments within 45 days and they do disbursals too, so taking this quarter ending balance will be futile unless we we know daily balance)

1 Like

When NBFC raise money from promoters by issuing warrants and converting it to equity at premium prices, it shows first sign that promoters are confident in future business. With zero NPA and premium price paid by promoters, i think good days ahead for investors in SG Fin

8 Likes

Strong Q4 results.

Seems the grinding by investors in Q3 concall on core business deviation and growth has worked well.![]()

1 Like