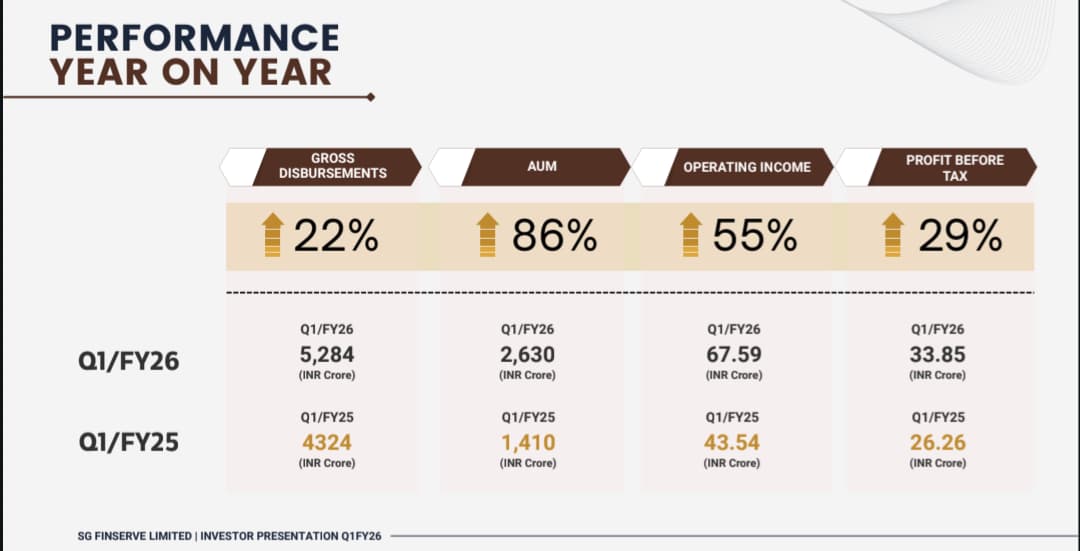

Q1FY26

AUM up 86% YoY

Disbursement ![]() 22%

22%

PAT ![]() 29%

29%

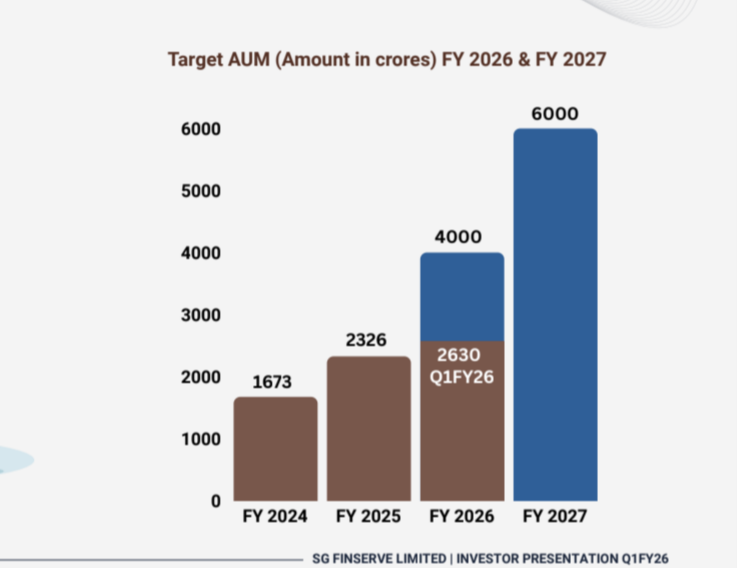

![]() 65% AUM target achieved in Q1 itself

65% AUM target achieved in Q1 itself

I am not able to understand the difference between disbursement, Loan book, average daily loan book and AUM. Can anyone explain in simple words?

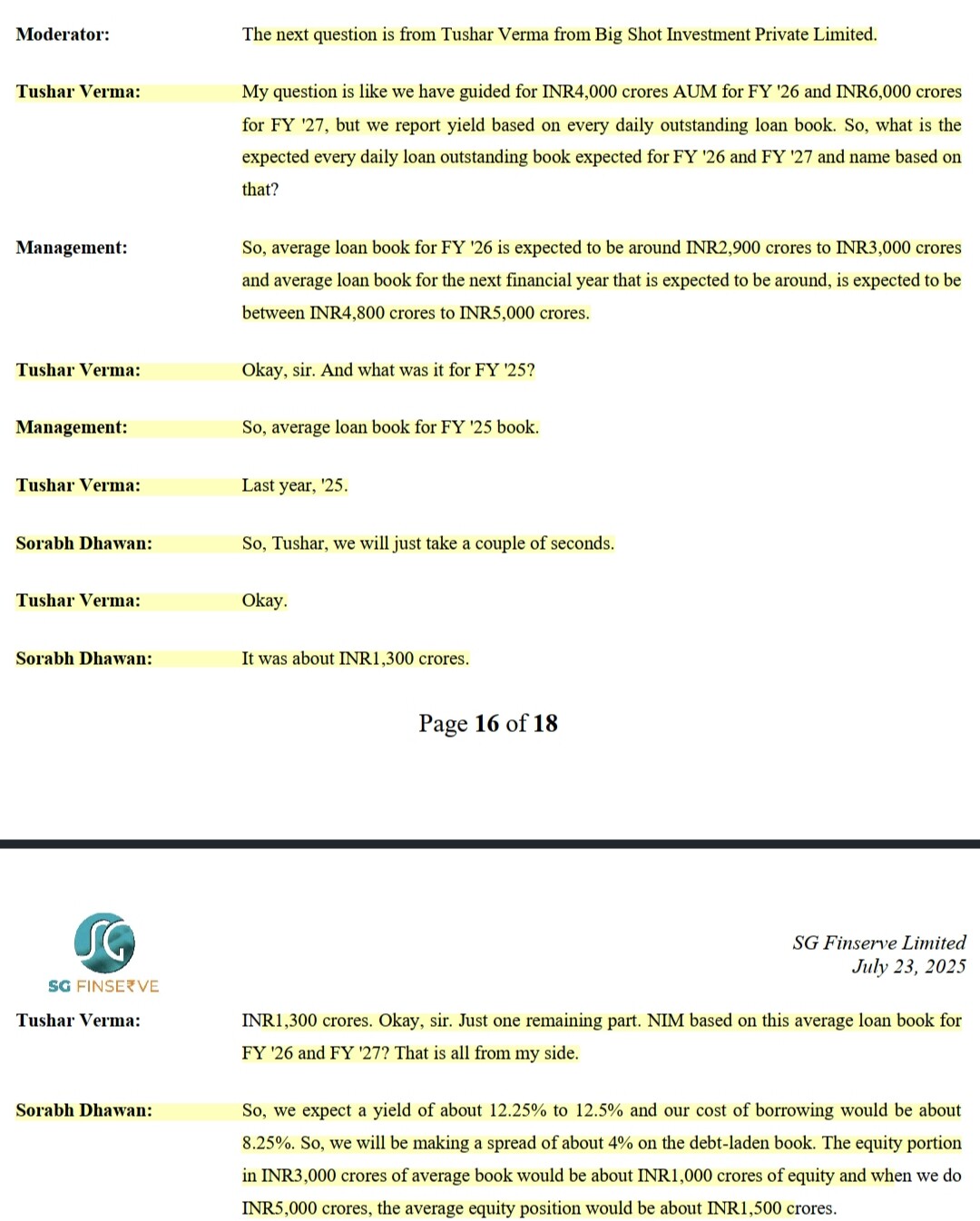

Also after reading the concall Q1 26, i am little bit confused about the loan book. Towards the end of the call, one investor asked about the average daily loan book for year 2025, 2026 & 2027 (both targets), to which the reply was:

-

Average daily loan book of 1300 Cr for 2025 and in the beginning of the same concall management was talking about growing the loan book from 2600 Cr at end of Q1 Fy 26 to 6000 cr at the end of FY 27 ( My guess they must be talking about AUM but mistakenly refered it as loan book or are those both the same thing for SG Finserv as it doesn’t have any off balance sheet loans)? Screenshot attached

-

Average loan book of 2900-3000 Cr at the end of FY 26 that means loan book in Q4 26 will be more than 3000 Cr to give the average 2900-3000?

-

Average loan book of 4800-5000 Cr at the end of FY 27 that means loan book in Q4 27 will be more than 5000 Cr to give the average 4800-5000?

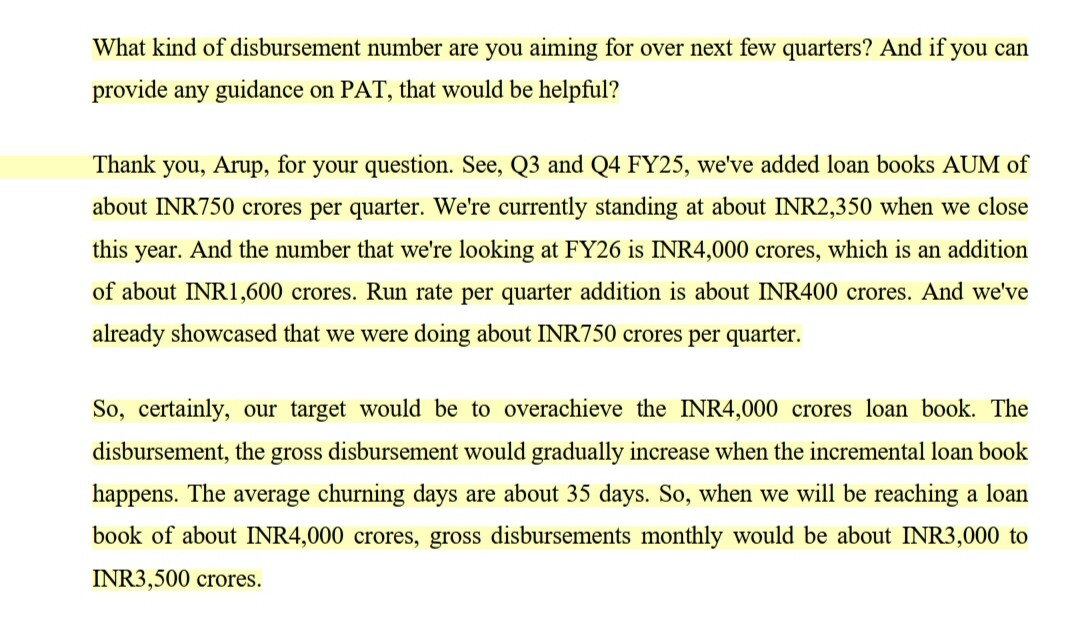

Can anyone explain the relationship between loan book/AUM with disbursements and churn days as shown in the screenshot (Q1 26 CC)

Are the bad debts written off shown in other expenses or impairment of financial assets or they are not shown in P&L statement altogether? Is it the right practice to not shown them in P&L if that done by the company in this case?

Sorry for so many queries.

Dis. : invested but doubting investment.

1 Like

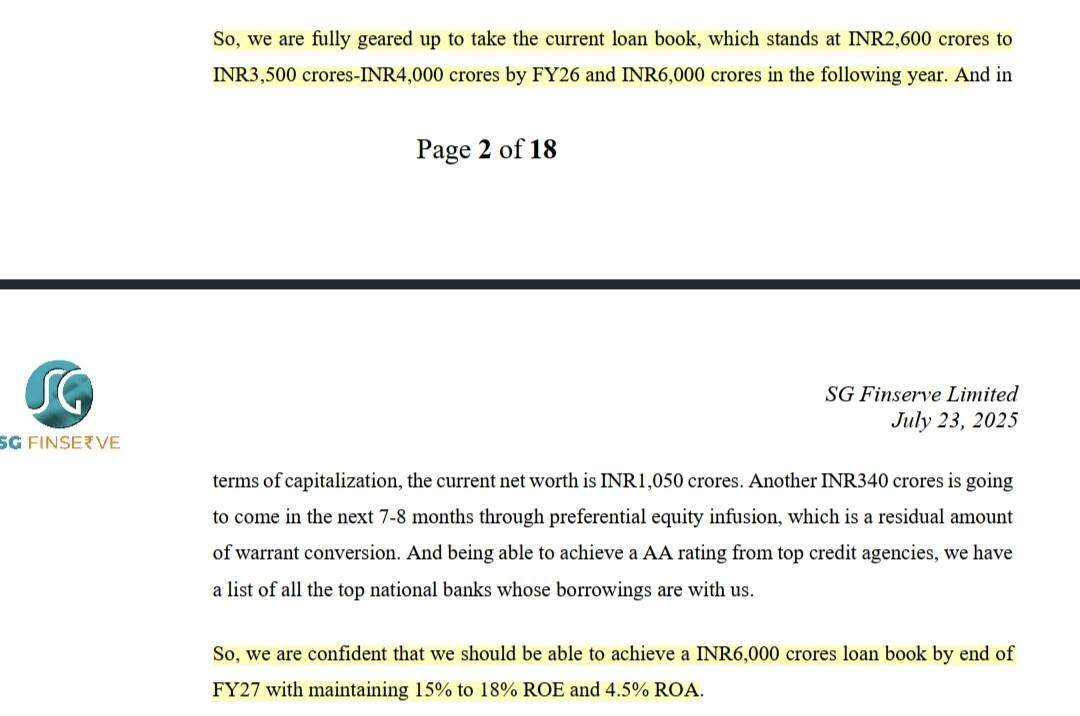

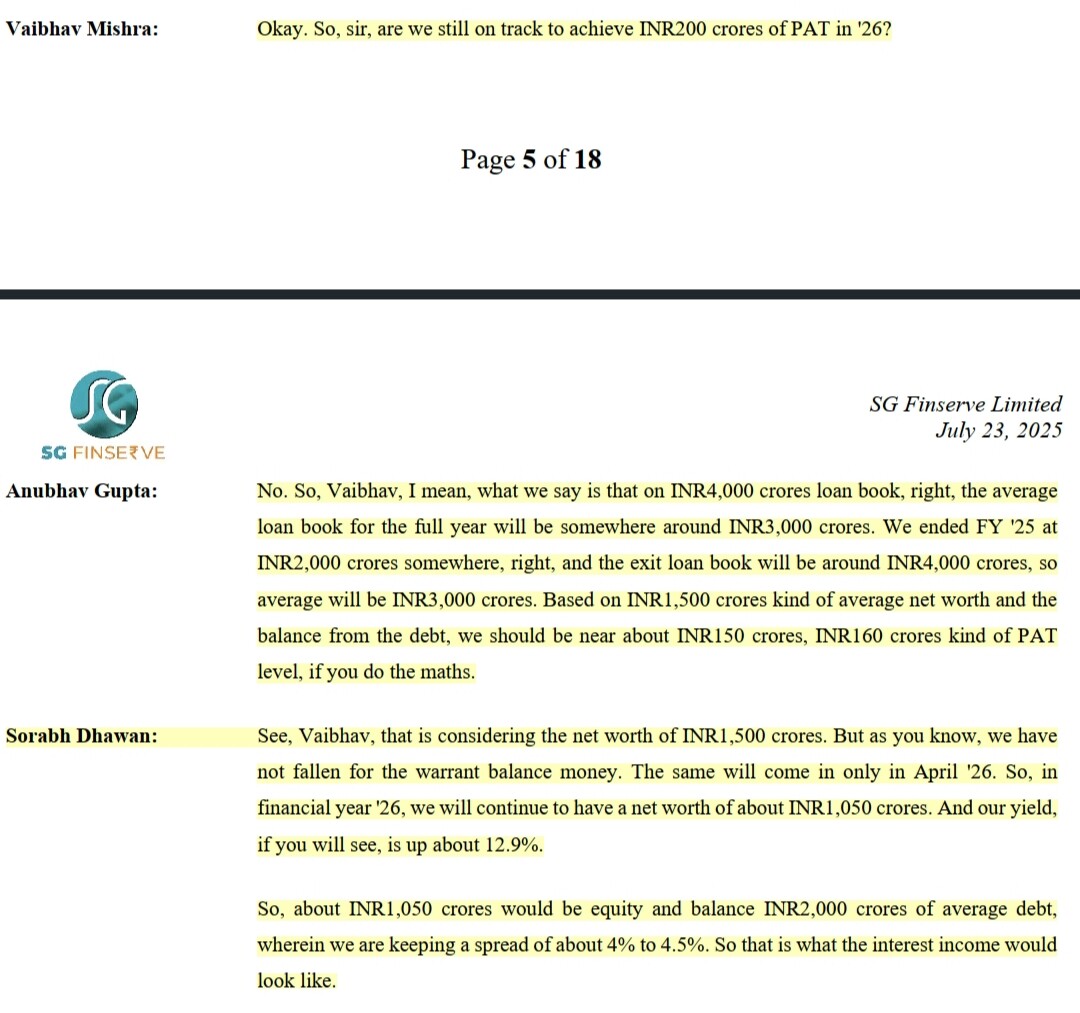

On asked about Management guidance for 200 Cr profit in FY 26.

Mr Gupta mistakenly count the 340 Cr warrants in the equity capital in Fy 26 and taken in 1500 Cr from the current 1050 Cr levels. However the warrants can only be converted in April 26 i.e FY 27. On this basis he projected 150-160 Cr profit for FY 26. However, Mr Dhawan corrected him sooner.

Can such a mistake from senior management in CC normal or can be ignored?

1 Like

Hi Mannu, let me try to answer what I can and if you still have doubts I can take another stab at it.

Let’s say i start an NBFC today with 100 crs cash

- On day 0, as i have not lent money to anyone, my loan book is zero

- On day 1, I make my first loan of 20 Crs - this is disbursement

- As soon as i disburse first loan, my loan book becomes 20 crs

- On last day of the month, day 30, i disburse another 80 crs. My loan book is now 100 Crs (20 + 80). This is also end of period, or closing loan book

- However, my average daily loan book will be the average of loans outstanding over this 30 day period - which will come out to 22.6 crs only - as the biggest chunk of 80 crs was only disbursed on the last day

- For AUM, i’m guessing the company might be reporting Loan Book + Investments. That is, in addition to giving out loans which is the main business, the company could also be parking some surplus funds in FD/Bonds/Govt Securities etc.

- You are right in assuming that for average loan book at end of FY26/FY27, Q4 will have to be higher as typically the loan book size will be increasing quarter on quarter

- Churn days here means in what period does the borrower actually payback its loan. As SG provides short term working capital loans, its churn days are lower at 35 days. If it were providing Term Loans, these would have longer churn days of lets say 1-2 years or more

- For bad debts, company would create an impairment in P&L. This would then get added to provisions in the balance sheet. Any bad debts that occur will be set-off against this provision already made. As SG doesnt have any stressed assets, it is only making provisions for Standard Loans (which are not overdue) as required as per accounting standards.

15 Likes

That was perfectly explained Aditya, thanks a lot.

I usually stay away from investing in banks and NBFC because of my inability to analyze them, this is my first thoughtful investment in it, still finding somethings a bit confusing.

For SG Finserv the AUM and loan book is equal as the management is clearly using them interchangeably in the CC.

In the fifth bullet point, how did you arrive at 22.6 cr value?

In fourth bullet point, the 100 cr is my total disbursement and will be equal to the loan book if there aren’t any loan paybacks right?

But suppose out of the 20 Cr initially loaned, 7 Cr was paid back on 20th day of the month then the loan book at the end of the month should be 20-7+80= 93 Cr, right? Disbursement remaining equal to 100 Cr irrespective of the payback, right? Am i getting it right?

In that respect, now the average daily loan book would be (20-7+80) /30= some kind of averaging which i couldn’t get?

Also the bad debt provision would be provided for both in P&L under expenses and the same would be reflected in balance sheet under liability side right?

But as soon the bad debt is written off, where it would be accounted for in P&L? In other expenses or the impairment of financial assets?

Hi Aditya, thanks for the wonderful explanation. Could you please explain to me how you arrived at the 22.6 Cr value? Didn’t understand that part

- For the 22.6 crs value, i took average over a 30 day period. For Day 1 to Day 29, loan book o/s is 20 crs. For Day 30, o/s is 100 crs (original 20 crs + fresh 80 crs disbursed). Effectively, Average daily loan book o/s = ((20*29)+(100))/30

1 Like

- See above point for average

- You are right, for 4th bullet point => Total disbursement is 20 Crs + 80 Crs i.e 100 crs, and is also my loan book o/s as no repayments took place

- In your example, you are right both about loan book at 93 crs and disbursement at 100 Crs. Disbursement is not linked to repayment.

- For average daily loan book, think of 30 days again. For 1st 19 days, loan book o/s is 20 crs. For day 20 to day 29, loan book o/s is 13 crs (as 7 crs was repaid back on day 20). And for day 30, loan book o/s is 93 crs (13 crs o/s + 80 crs fresh disbursement). Now take average of these 30 numbers and you get daily average loan book o/s

- You are again correct w.r.t to both expensing bad debt in P&L (called impairment charge here) and provision in balance sheet under liability.

- as you have already taken the expense of bad debt in P&L once, even when you write off the bad debt at a later date you dont need to charge it again to P&L. it will directly knock off from the provision that you had created earlier.

Think of it like this, from an accounting perspective, i am required to look ahead and make provisions for expected bad debts in the future. I keep expensing a reasonable amount every year in P&L and keep building my provisions. My P&L keeps taking the hit over the years by this small amount. The day an actual bad debt is occurs, i knock it off from the provisions i had created earlier without impacting my P&L directly.

What happens if the bad debt that occurs is larger than the provisions i hold? Eg. bad debt 100, provisions held 80. In that case, i take a hit in my P&L for the remaining amount of 20 crs in that particular year. I still call it impairment charge, again build a provision for 20 crs extra, and then knock off the bad debt from that provision (80 crs earlier plus 20 crs new).

3 Likes

Excellent answer, thanks again Aditya, for clearing the concepts.

1 Like

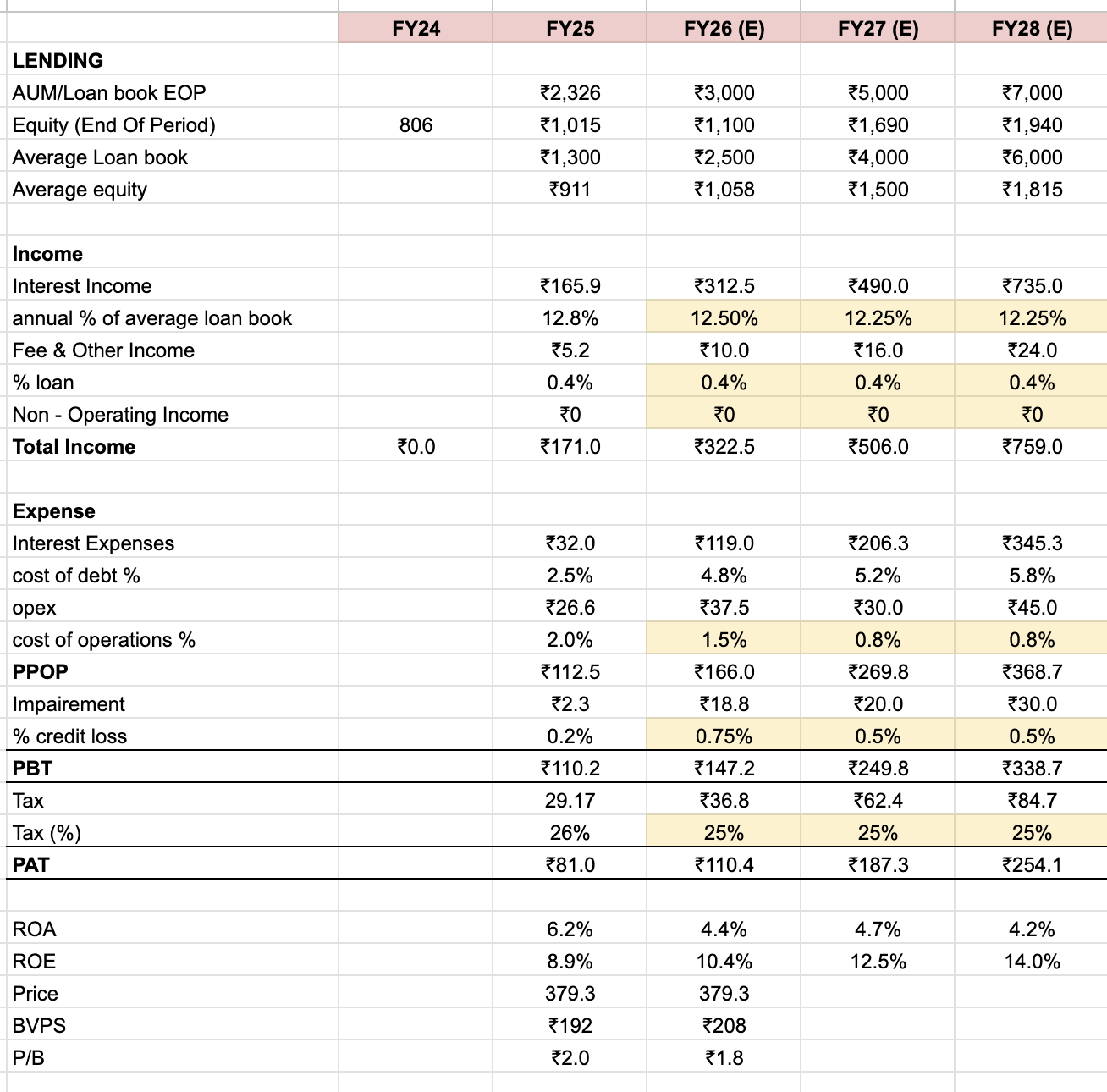

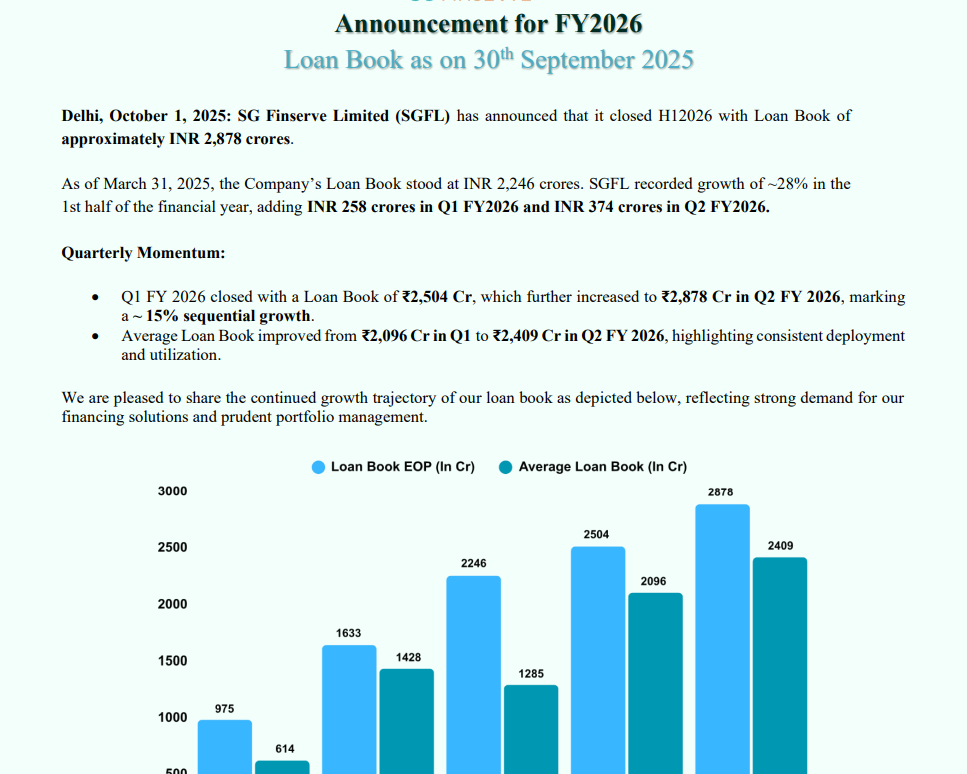

@Vineet_Bhatia I modelled for 2026. Made it more conservative based on management guidance of FY26-28 and actual Q1 performance.

- FY26 average loan book guidance 2900 Cr, Q1 actual average 2100 Cr, assumed 2500 Cr

- 1% GNPA and 40% provision for that (credit cost higher)

PAT growth is healthy even with conservative assumptions. P/B (forward) at 1.8 also seems reasonable

At 6000 Cr orderbook ROE will reach 14% and there will perhaps another year before next fund raise will be needed.

There are many assumptions, so please consider this directional.

Disclaimer: Small investment. Evaluating whether to increase.

2 Likes

Just a quick update to this. AR FY25 is out.

- Mgmt took an impairment on financial instruments of 2.29 crs - this is like a provision for standard assets

- Hidden in other expenses, there is a Bad Debt write off of 5.37 crs. Mgmt could have used existing provisions to write off this amount, but chose to take separate hit on P&L

- As all bad debts have been written off in FY25, gross NPA are Nil

3 Likes

5.37 Cr write off on 1300 cr (average AUM 2025, shared in Q1 Earnings call) is 0.4%

As the loan book grows, I think credit loss could be in the 0.5% to 1% range.

3 Likes

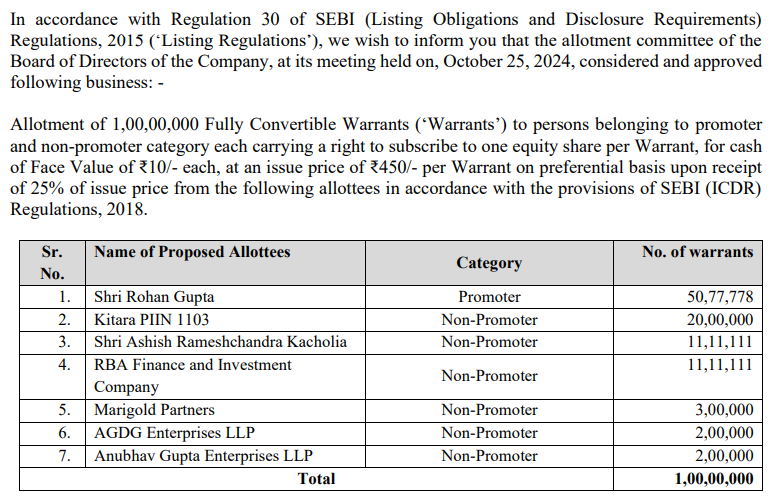

Share count assumed is not inclusive of the 1 Cr warrants issued on 25th October 2024, which can get converted into equity shares anytime between the allotment date and 18 months from the warrants allotment date i.e. till 25th June 2026. Total outstanding shares will increase from current ~5.6 Crs to 6.6 Crs post warrants conversion, which would make the BVPS as per your equity calculation to be ~Rs. 250 in Mar-27 quarter.

5 Likes

You should have a BVPS projection as well,

Will look into it, thanks for pointing out

1 Like

i would not keep these as peers of SG Fin. because SGFin is pure play invoice financing

4 Likes

| Year | Net Profit (₹ Cr) | Equity (Cap + Reserves) | Avg Equity (₹ Cr) | Total Assets (₹ Cr) | Avg Assets (₹ Cr) | ROE (%) | ROA (%) | Forward B/V |

|---|---|---|---|---|---|---|---|---|

| FY23 | 18 | 41 + 532 = 573 | — | 1,079 | — | — | — | |

| FY24 | 79 | 55 + 751 = 806 | (573 + 806)/2 = 689.5 | 1,779 | (1,079 + 1,779)/2 = 1,429 | 11.46% | 5.53% | |

| FY25 | 81 | 56 + 959 = 1,015 | (806 + 1,015)/2 = 910.5 | 2,416 | (1,779 + 2,416)/2 = 2,097.5 | 8.89% | 3.86% | |

| FY26 | 100 | 1215 | 1115 | 4000 | 3048.5 | 8.97% | 3.28% | 2.30 |

| FY27 | 200 | 1515 | 1365 | 6000 | 5000 | 14.65% | 4.00% | 1.84 |

| Mcap | 2791 | |||||||

| 450 CR warrants Conversion Funds will Come OCT 2025 | @450 |

4 Likes

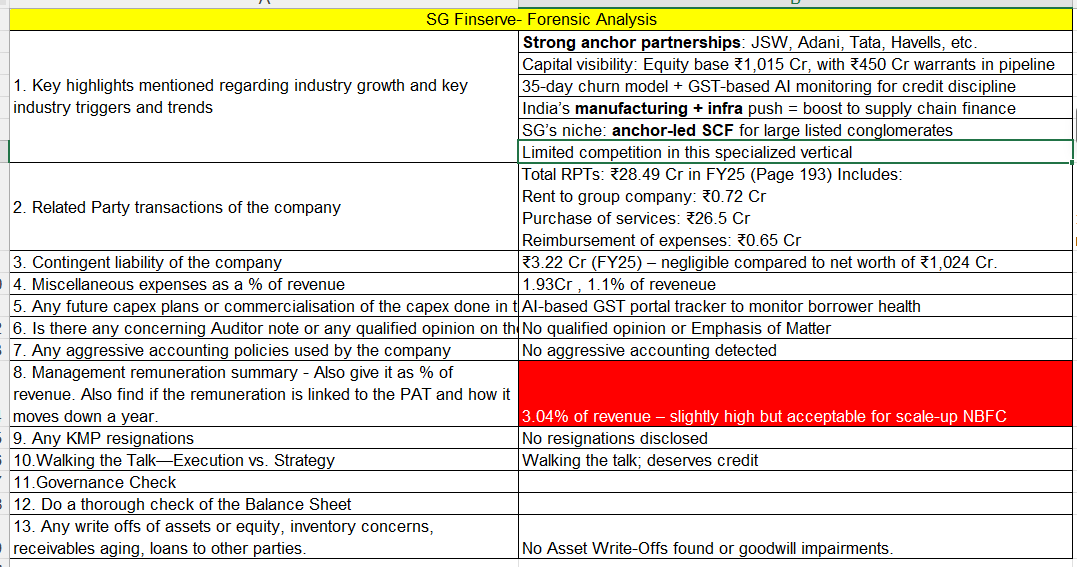

Both CEO and CFO resigned ..something to be worried of?