Looking at the Q2 result, the new CEO/CFO seems to following a kitchen sink approach: Reporting losses when they join in clearing up the book and past doing of earlier management. There is a trace of this happening. On the other hand, they would be indicated positive second half, which they did. Management hinted at a slightly better second half, which does not sound very optimistic picture of the future.

In the Q1 call, just a few months back, management said they would recoup all the API sales lost due to fire, but months after the call, the second quarter came much worst. Sequent had 65% of revenue coming from the regulated market, and most of them have a contractual provision to pass on RM prices, and this is likely to happen from Q1 onwards.

They would report better profitability just by passing the RM cost for API. Considering this is a regulated market, this could have been significant. But looking at the management commentary, this looks like a pipe dream, as they have yet to hint at significant improvements in Q4/Q1.

High inflation across the world is impacting farmers’ life. As a result, Sequent cannot pass on higher RM prices in the formulation business. Despite that, they are buying companies in different Geographies. I find it weird that all this formulation business combined is not able to make money if one sees over the last 4 to 8 quarters. Agree; they are making investments for VMF in the US market, but it is small, and the business has little pricing power.

Turkey is another tragedy IMO. Due to currency depreciation, earlier management said that the business is doing locally, and the currency depreciation is making products manufactured within Turkey very competitive in Europe. We have not seen any traces of it yet, and neither the new management mentioned anything about it in Q2. So it seems earlier management was misguiding, or that was just a mirage, and they said for the sake of saying it. I hope this was not the case, but looking at the last 3/4 quarters’ results, it is increasingly looking like the case for me.

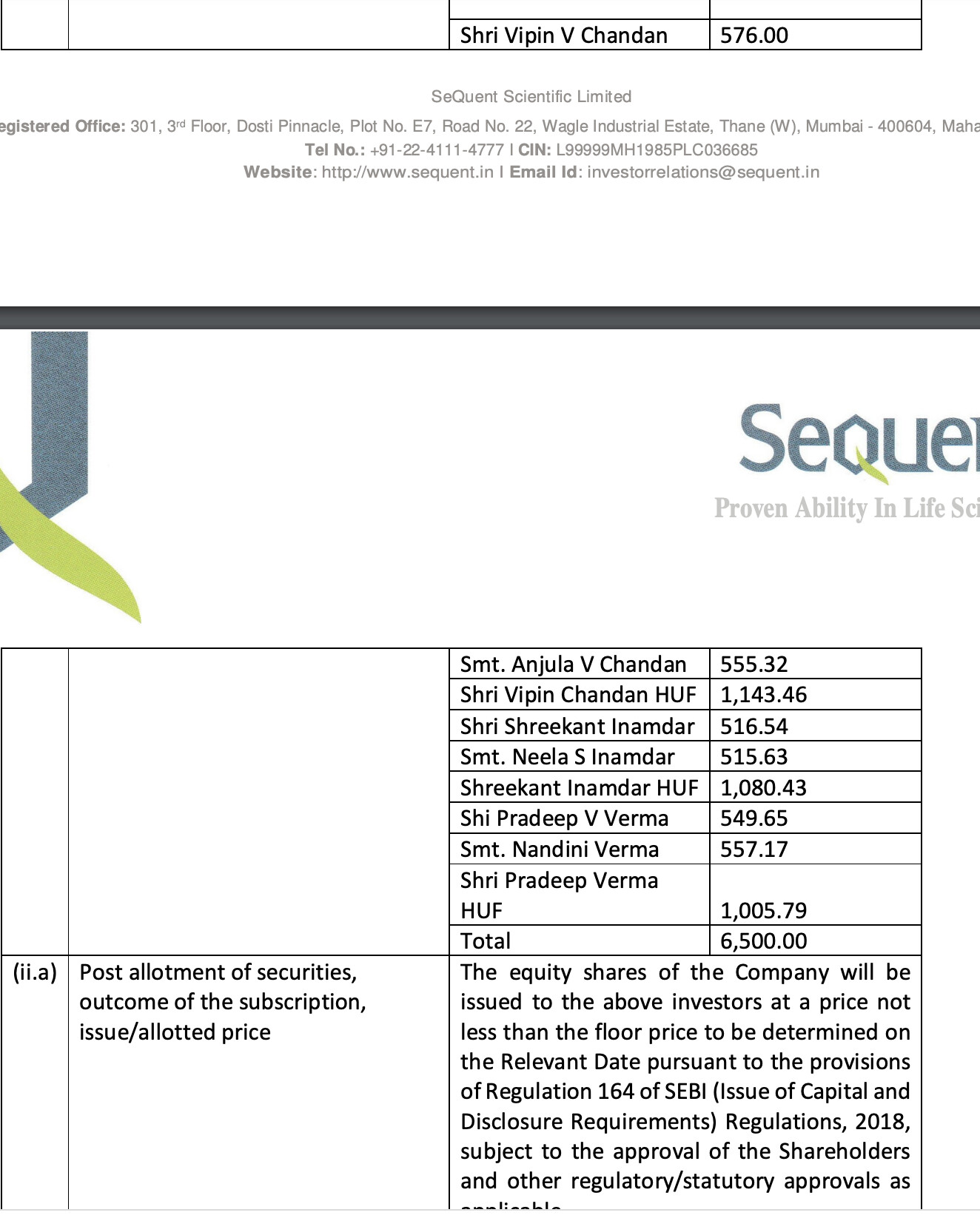

The new India acquisition is funded by preferential allotment for 65 crores. I am keen to see what price new shares are allocated as it will set the new benchmark. If the allotment price is above CMP, then it will be positive for the stock in the short term. However, any discount to the price or allotment of shares around 86, the price at which Carlye bought, will not augur well for the stock. I think the business is nowhere near as sound as I thought it to be, and it is made worst by ESOP costs, which are constant irrespective of the business performance.

Note: Invested and rubbing my nose.