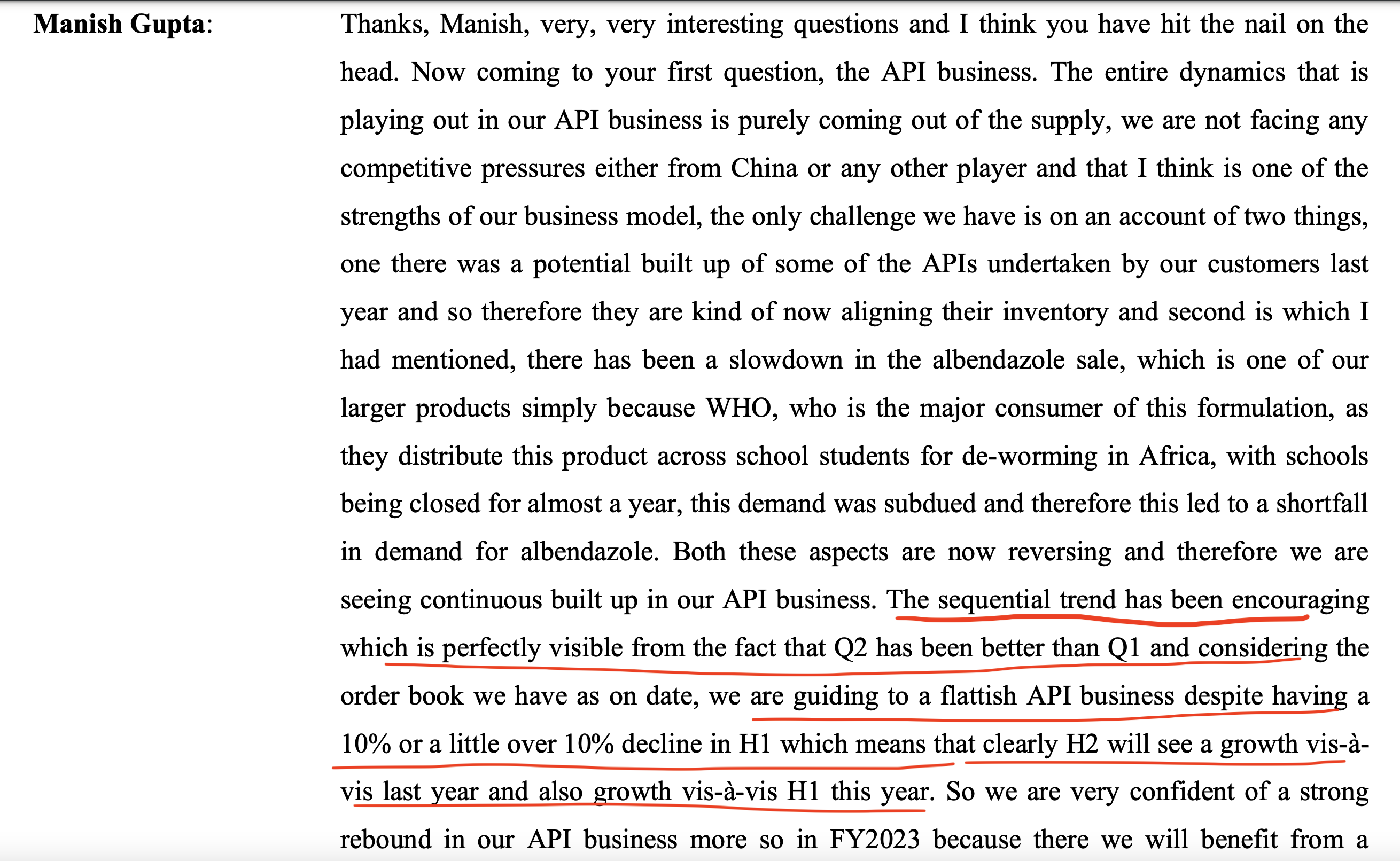

Let me delve into just API number. In Q2 con call, they said YOY API growth will be flat.

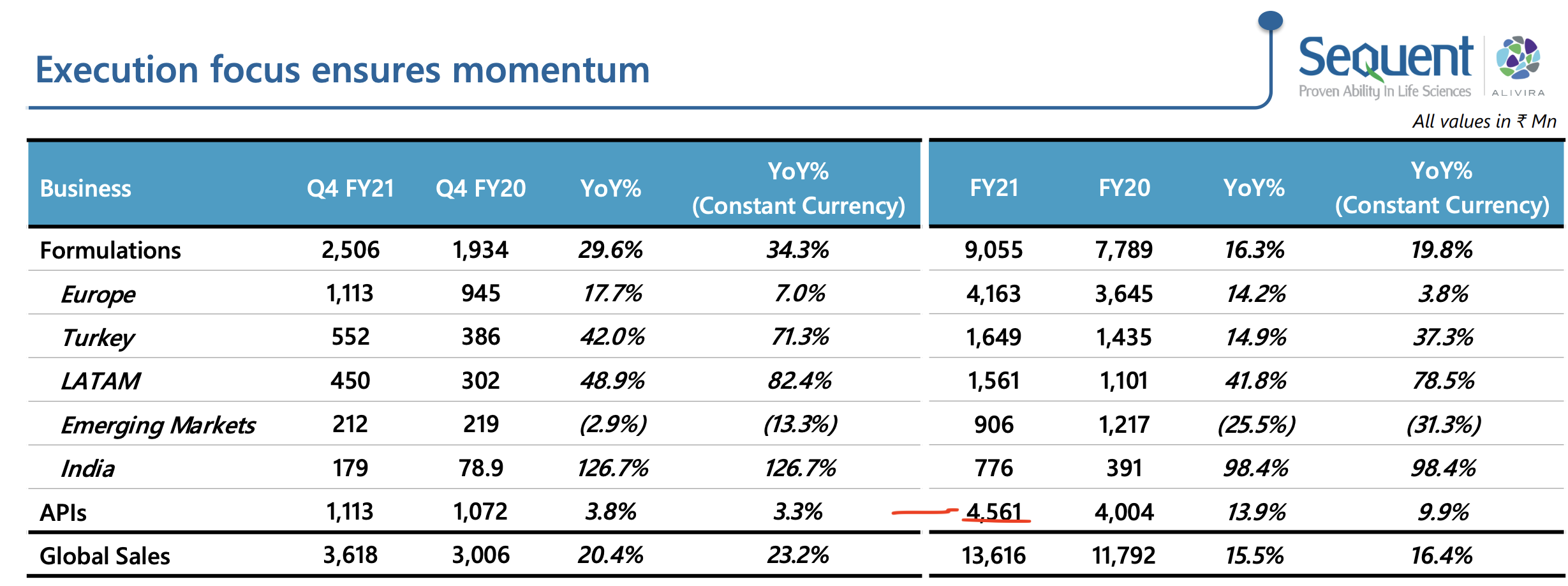

In FY21, API sales were 456 cr.

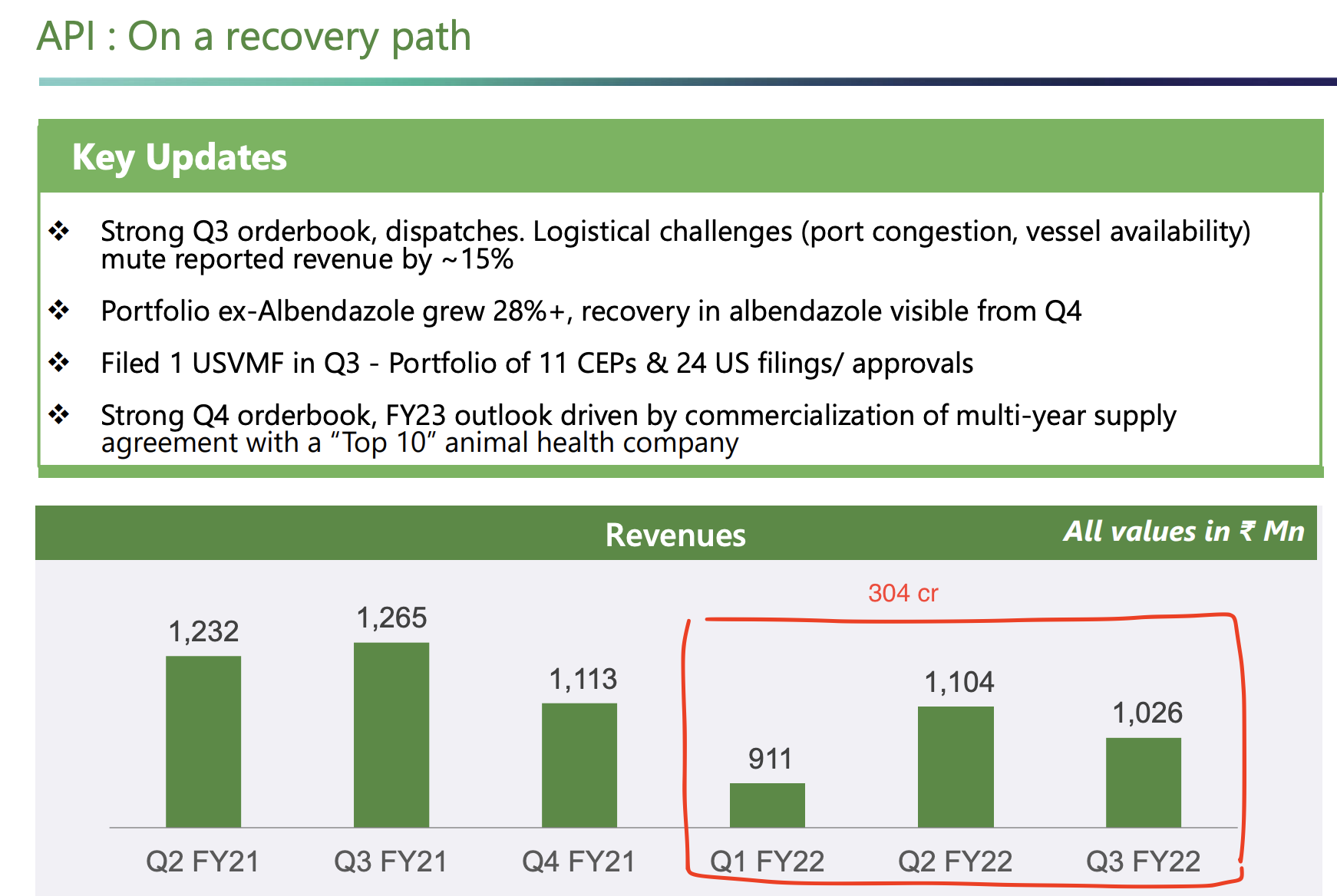

So far TYD, sequent has done API sales of 304cr.

If we go by words of management, they need to do API sales of 150 cr in Q4, which is 50% of YTD (Q1+Q2+Q3) of API sales, with higher prices as management (price escalation happens at the start of new calendar year starting Jan).

…and API is a better margin business

So just based on API, additional 50 cr of sales (150 cr - 100 cr of Q3) shall result in decent PAT. I think they can report one of the best quarterly profit (keeping everything else same) in Q4, hence I said above that worst seems to be over.

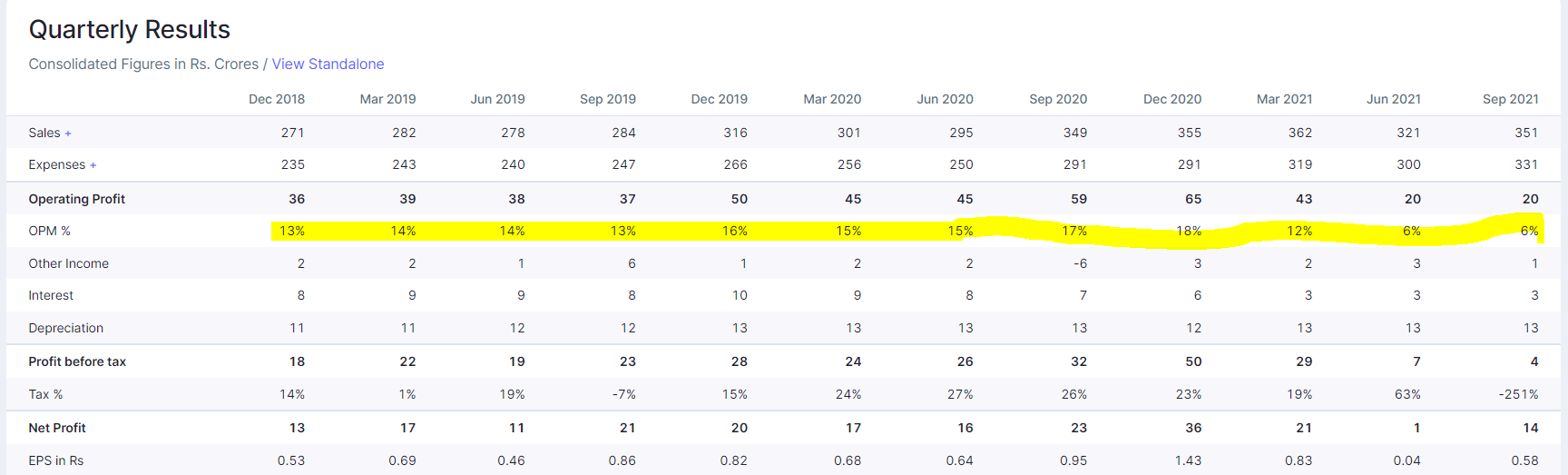

Additionally, their OPM shall improve (regression to the mean) to mid teens (13%+). It may take few more quarters, but it is likely to be on upwards trajectory going forward.