Intel:

Last week intel PR mentioned they are looking at “decreasing window of leadership”. What this means is that as soon as intel beats AMD in performance, there is next chip of AMD ready. saphire rapids was competing with milan… but milan-x (3D v-cache) came in in about 2 months with better perf.

Example: Intel Sapphire rapids are delayed. Q4 2022 ramping up and validation. Most likely launch in Q1 2023. Sapphire rapids was supposed to compete with milan/milan-x. Not with genoa that is coming Q1 2023 (launching in H2 2022). So, intel’s upcoming products will compete with AMD products they were never meant to compete with. Intel is giving out good competition. But these delays are hurting them.

Since intel is in rear view mirror for AMD, they are taking steps as a competitor for NVDA. NVDA’s next workstation is with sapphire rapids. My opinion is nvda already sees AMD as competitor and hence they switched to intel. Otherwise I do not see any other reason to not pick a leadership CPU. Another reason can be that intel is only a stop gap until they fully move to Grace (NVDA ARM CPU) CPU.

Some intro into what is make or break for competing with NVDA: → My opinion. Others in the know how of this industry can comment too.

NVDA is the king in AI/HPC space when it comes to accelerators

They have two things

Great hardware - This is a no brainer. Without hardware, you cannot compete here

Great Software platform - This is the real winner. It is called CUDA. It is a platform for parallel computing. CUDA performance is tightly coupled with their hardware → Think of this strategy as what apple does with its software. They also put in a lot of effort to give libraries for scientific computing/AI/ML. Their libraries (as expected) always perform better with their own hardware. Their GPUs come at a premium because of this.

I have myself programmed a bit in opencl and I have browsed through CUDA programmer’s manual some 9 years ago. Even in those days I felt CUDA was more approachable with better manuals and controls. From the way I see it, AMD screwed up from the software side all along. Even though they had decent hardware, I feel they never really had the focus on software like nvda had. NVDA’s hardware is part of the CUDA platform. Not the other way around.

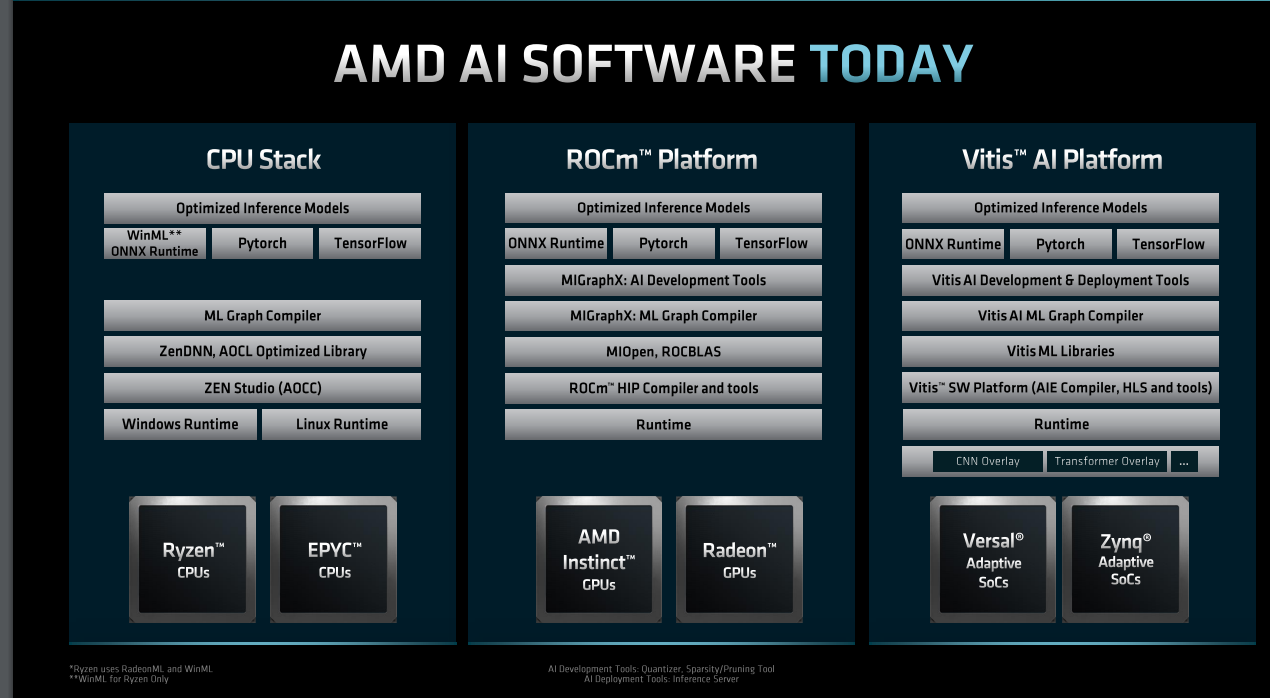

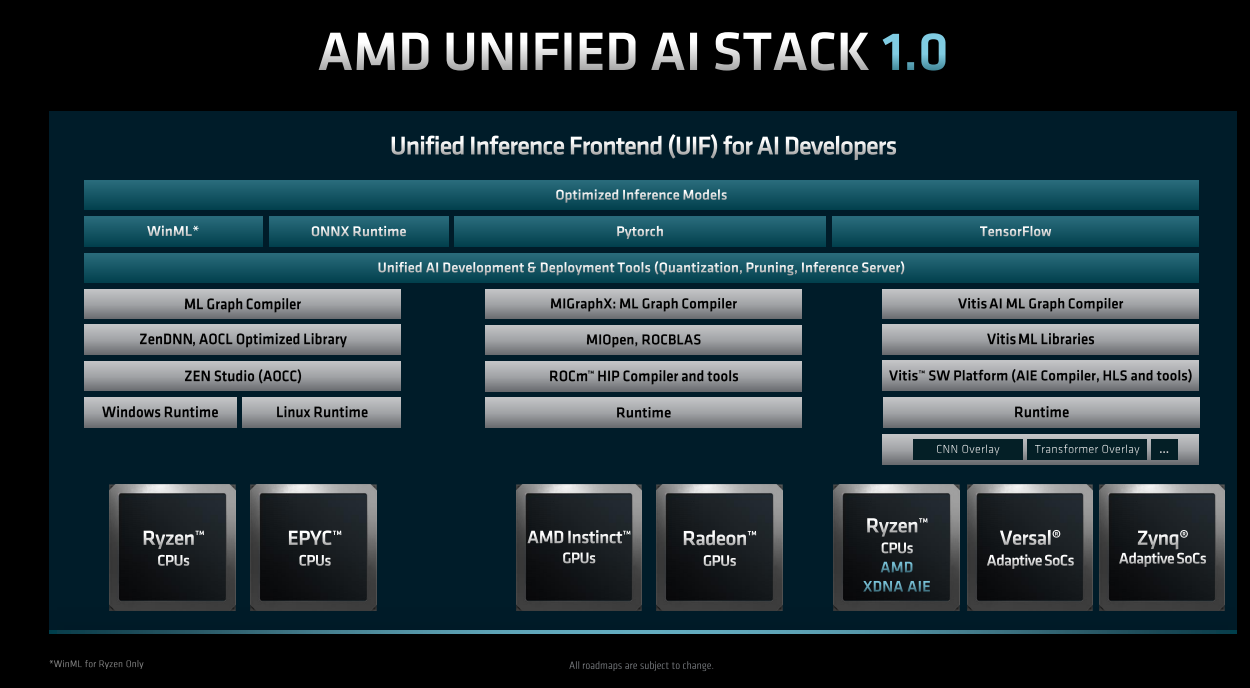

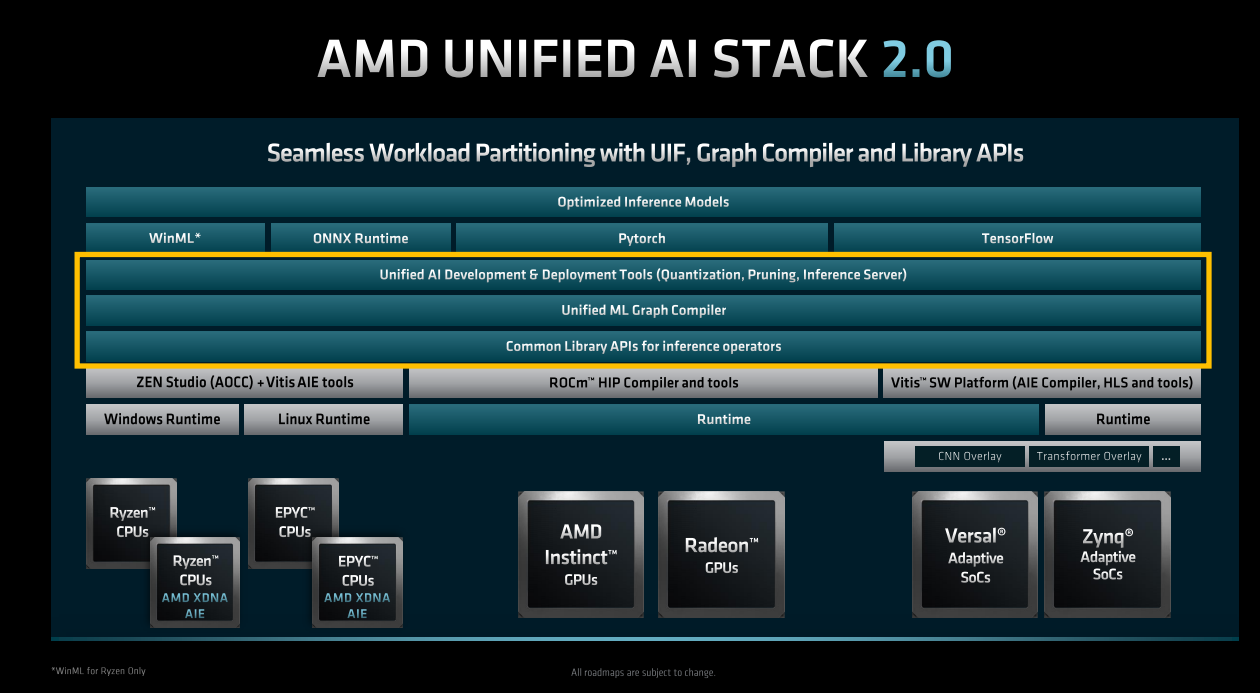

AMD situation in software stack now:

Even now, I was reading in forums that clients buy one NVDA accelerator for development with their CUDA platform. Then they try to migrate to AMD ROCm. Some complain that CUDA just works unlike ROCm. Sample: What Is AMD ROCm? | Hacker News

In light of that, I am happy to see the following slides in analyst day from Victor Peng.

They are unifying their stack, so that same code is reusable easily across multiple verticals. DATA Center AI fight will not be as easy for AMD as it was in CPU with intel. But nonetheless, it is still an opportunity. AMD only has to steal existing market share while NVDA and Intel have to make market (They are leaders).

My posts are going to increasingly focus on how AMD is faring in the compute AI space. MI300 will be keenly watched along with their software progress. Otherwise NVDA is a pure winner all along.

Disclosure (Does it matter with non Indian companies?): I already had AMD RSUs from my employment days in AMD. I am accumulating during this fall. I think the market is wrong in binning AMD with Intel and NVDA. AMD is beating Intel and it is more diversified than NVDA (especially with acquisition of xilinx).Irrespective of how it goes against NVDA in accelerators, I expect them to continue to do well in CPU. As of now a purely datacenter CPU share gain bet.

The underlying software is powered by AMD’s ROCm software stack, which stands in contrast to

NVIDIA’s CUDA thanks to its open-source approach. It also features a translation mechanism that can adapt CUDA-based code to AMD’s software stack with minimal software engineering efforts.

The highly-anticipated Intel server chips, codenamed “Sapphire Rapids,” may not ship until the second quarter of 2023, as opposed to a consensus expectation for a launch in the second half of 2022, noted tech analyst Ming-Chi Kuo said on Thursday.

Premised on a second-half launch, Morgan Stanley analyst Joseph Moore said in a December 2021 note that he expects the chip to help Intel narrow its server market share gap with rival Advanced Micro Devices, Inc.'s (NASDAQ: AMD) Milan server processor.

To make matters worse, AMD is expected to begin shipping its Genoa server chip, based on the next-gen, 5-nm processor node technology, in late 2022.

Here you go. First MI300 news. El Capitan was announced in 2020 by AMD, Installation late 2023. A bit of system information revealed now.

El Capitan will be powered by AMD’s forthcoming MI300 APUs.

Theoretical peak is two double-precision exaflops, [and we’ll] keep it under 40 megawatts—same reason as Oak Ridge, the operating cost.

Minor Intel sapphire rapids delay news.

Argonne National Laboratory is awaiting completion of the Aurora supercomputer, a 2-exaflops HPE-Intel machine that has undergone several reconceptualizations. Aurora’s execution is also potentially beset by additional delays pertaining to its Sapphire Rapids CPU, so the exact timeline is fuzzy — but, reportedly, installation is underway.

We miss some important events in history in search of ‘where is the money’. Having an APU in server is a world first and that too at exascale is quiet an achievement.

Being APUs, El Capitan will benefit from what’s likely to be the densest performance profile ever achieved in the world of supercomputing. Make no mistake: El Capitan will represent the pinnacle of semiconductor performance, design, and integration. It’s not hyperbolic to say that it’s likely to be one of humanity’s most technologically complex endeavors.

Efficiency is showing. ‘6800U just destroys 1260P’ and such words. This is expected.

All chip design companies are cutting orders to TSMC. One curious case is AMD not reducing 5nm orders.

AMD, on the other hand, revised its orders for 7nm and 6nm wafers, reportedly lowering the amounts by around 20,000. This applies to shipments in the fourth quarter of 2022 and in the first quarter of 2023. However, AMD hasn’t changed its order for 5nm wafers intended for PCs and servers.

Nvidia could be affected badly in PC space. Combination of reducing crypto demand + resale of GPUs from last year. The prices are going to go below MSRP. Datacenter may remain strong.

The second-hand market is flooded with used GPUs that did their time mining crypto and are no longer profitable to keep running due to the crash in the cryptocurrency market.

Nvidia seems to be in a sticky spot compared to the other two tech giants. It made prepayments to TSMC to secure their 5nm wafers for the upcoming RTX 4000-series of graphics cards. Now, facing a drastic drop in consumer demand, Nvidia tried to alter its order — but according to DigiTimes, TSMC wouldn’t budge. The companies came to an agreement where the first shipments will be delayed by one quarter, but Nvidia is now supposed to find replacement customers for TSMC’s vacated production capacity. A year ago, that would have been easy, but now, it might be nearly impossible.

According to a forecast by Gartner, worldwide PC shipments are on track to decline by 9.5% in 2022.

I am holding onto AMD and waiting for conference call. Based on their guidance for server market + I have been hearing multiple twitter handles youtube handles mention the deman for milan/milan-x is still strong. And that is what the play is about. Companies cancelling tsmc orders plays right into AMD hands since Lisa Su mentioned multiple times last year that they are unable to supply the demand. If PC market is going down, it can help them further to focus on datacenter (move wafer space to EPYC)

Having created a unified AI inferencing stack, AMD has to create a unified HPC and AI training stack atop ROCm, which again is not that big of a deal, and then the hard work starts. That is getting the close to 1,000 key pieces of open source and closed source applications that run on CPUs and GPUs ported so they can run on any combination of hardware that AMD can bring to bear – and probably the hardware of its competitors, too.

This is the only way to beat Nvidia and to keep Intel off balance.

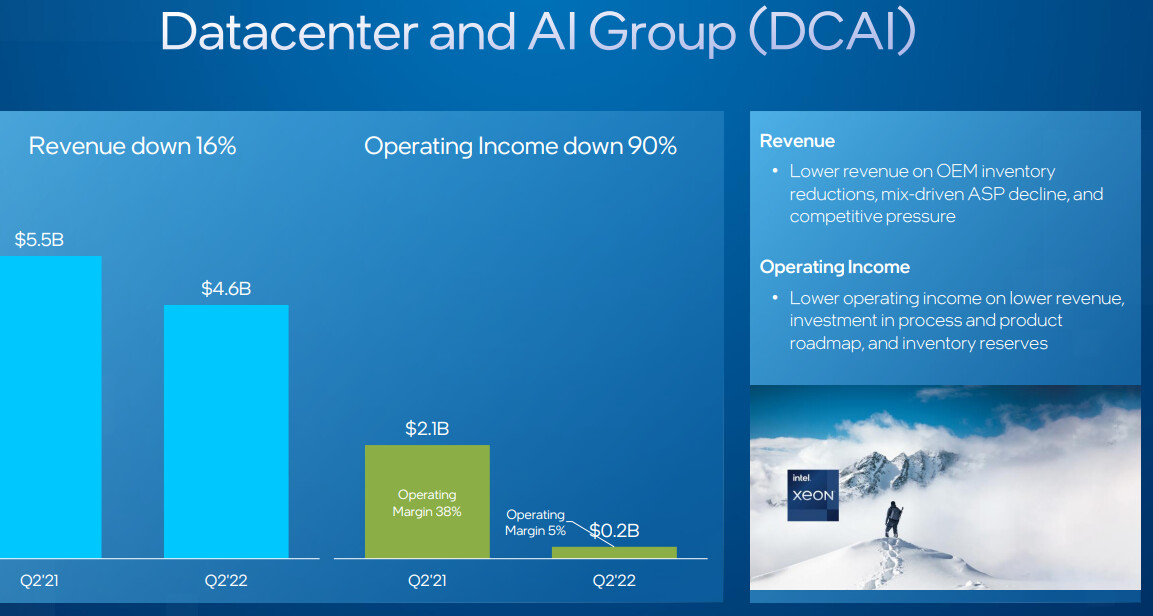

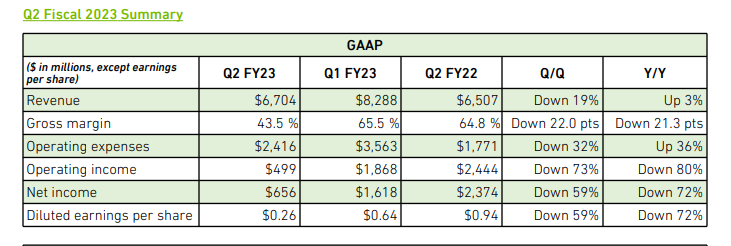

BOOM. Intel posts the worst results in near term memory. Reported loss.

Both client and datacenter down. Degrowth was expected but not this much. Client was a surprise for me. Not sure what is going on there.

Since our focus is datacenter, we knew intel is going to lose market share. The real news is that Saphire rapids are delayed in 2023. Some SKUs are ramping up in 2023. All the while, the message was that ramp up is late 2022. But we get to know now that some SKUs are later. Analysts had to grill the company in analyst call (https://edge.media-server.com/mmc/p/6zdpcntm) to get that out. All guidance now changes or the year t 2.3$ EPS.

We gave the following rationale for this thread in the 2nd post.

What do you care?

Secular growth possibility: Well, it would not be a big deal during normal times. But, if you think covid is disrupting workplace like never before and that online work is the future, then you cannot miss the brains behind every single cloud infrastructure – The processors. Games, virtual reality, Cloud, Computing.Research folks know. Especially if you had to book slots in super computers in 90s and 2000s for doing some big compute. If the growth is fast enough, then not one company will be able to supply all datacenter processor needs. To top it off, Intel the giant is faltering in its ‘fab’.

Finally, it had its first major hit. Well summarized in the article below as to why it is a steep hill to climb for Intel to get back to its former hegemony.

“(But) Unless and until AMD, Nvidia, and the Arm collective screw up and unless TSMC screws up, Intel can never recreate the conditions that allowed it to have hegemony in the PC and in the datacenter ever again. This is like the United States after Europe and Asia were destroyed after World War II, or Rome after the fall of Carthage. These are once in a lifetime opportunities for monopoly, and they just don’t come around again. The Holy Roman Empire was a pale shadow of the glory that was Rome. But still effective, mind you, give the times many centuries after the fall of Rome.”

Another article summarizing the sudden drop in financials as being due to capital offsets.

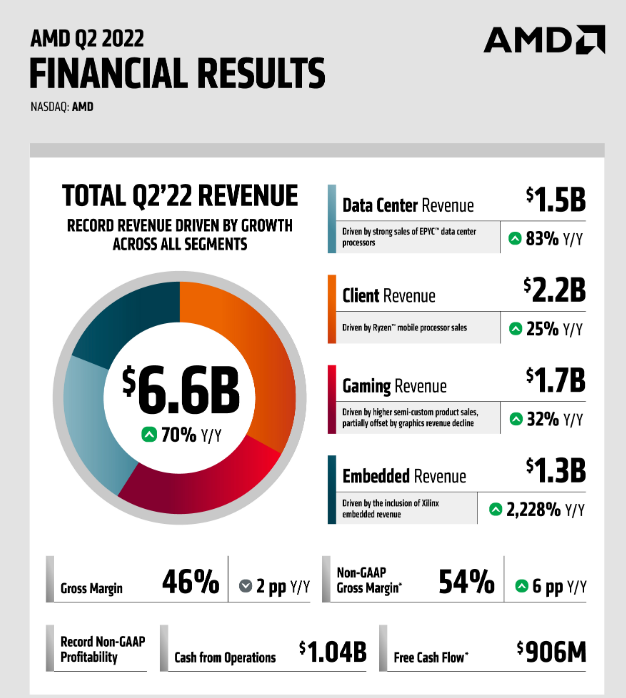

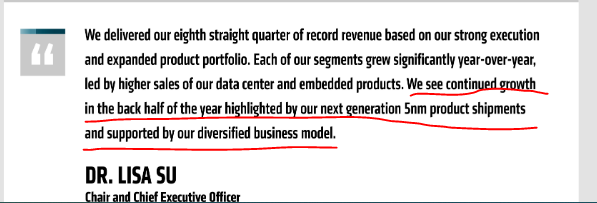

I will post a full commentary of the status in datacenter after AMD posts earnings tommorow.

While retail is slowing down, datacenter will continue to see growth as they take market share from intel. Some other surprises like though gaming GPU sales is down, consoles they are expecting demand. Diversity in company is helping this downturn.

Datacenter will continue to be stable/grow. Visibility for 4-6 quarters.

“And then we see Genoa coming in toward the end of the year into 2023…() …

And we’re planning really for the next 4 to 6 quarters, and that gives us good visibility.”

One addition from earnings call - The question had this -

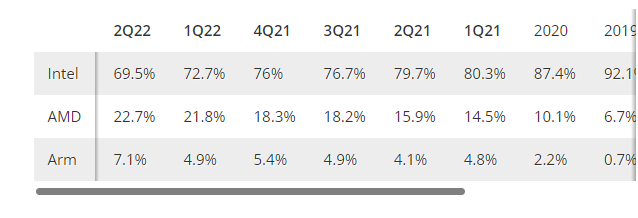

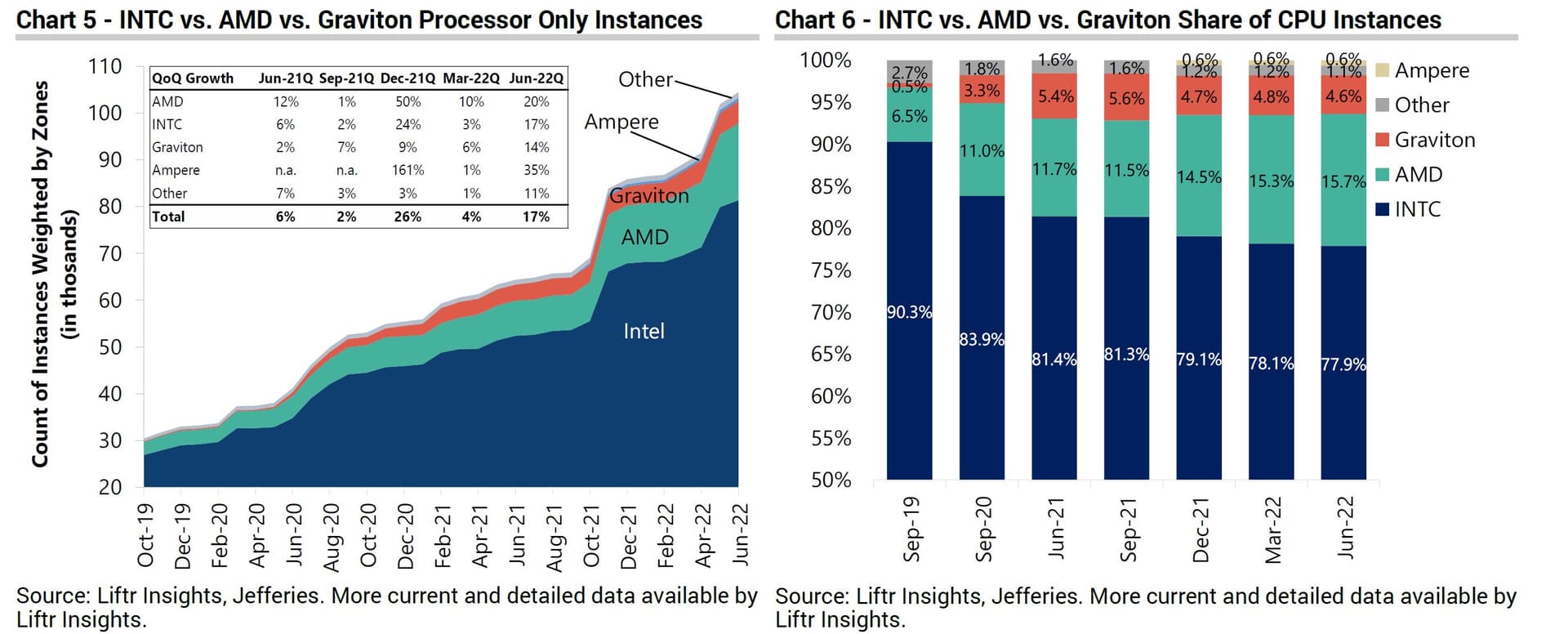

"If I look at the spreadsheet that Saresh sent around with the restated data center numbers. And it looks like your data center business kind of aligns apples-to-apples to Intel’s pretty closely. It looks like you guys gained 6.6% share from Intel.

And if I kind of take a guess about the pro forma contribution of Xilinx, what it would have been in Q1, it’s about 6% share gain. And that would be – I think that would be the highest share gain in that data center business that you guys ever reported even going back to 2005. Admittedly, two-thirds of that is from Intel declining. I guess since that would put you against until, I guess, in the like kind of the mid-20s, … "

6.6% market share gain (if true) and that too in data center in a single quarter is quiet something to put it mildly.

Intel faltering in data center when we are seeing a cloud boom.

QC Bought nuvia 2021 - PC market is dead - So now let us put nuvia folks in data center market.

Backup plan for cloud folks - As far as cloud are concerned, this is a backup if the processor market stagnates without competition like it did when intel was monopoly.

My opinion:

Upcoming CPUs for datacenter from AMD are going to blow away existing processors in both performance and efficiency. Genoa and Bergamo. Bergamo is a cloud optimized 128 core processor. Zen 4c cores specifically targeted for cloud. All newbies are going to realise why datacenter biz is tough. The 5nm arm chips look good against AMD Rome. But against bergamo?? What is in the pipeline for arm??

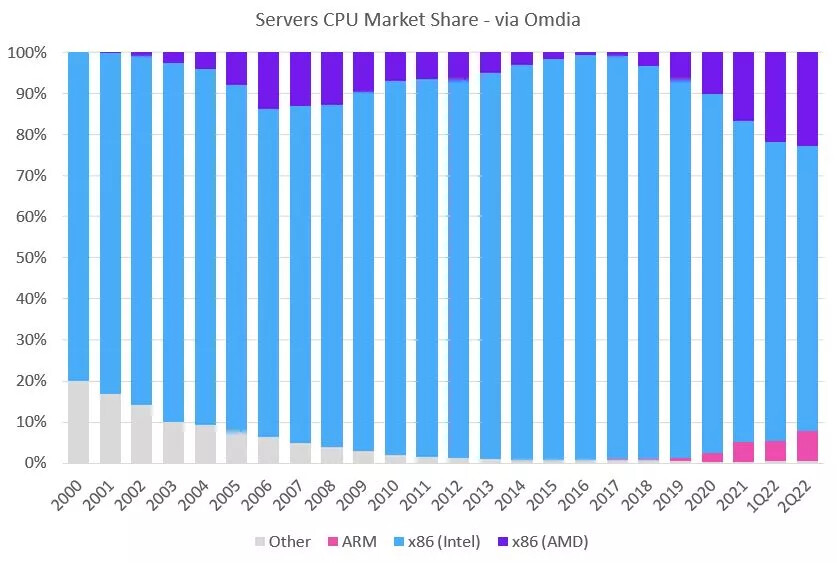

Data center biz is not like retail. The customers need confidence of years of supply. They look for visibility into future. You need to get customers to buy into your road-map. Sticky. That is why it has taken 3 years of consistent processor perf beat + delivery on promise + intel to screw up for AMD to reach 25% share . Also, AMD is a little lucky (or smart) that they do x86 (They did not move to their ARM K12 processors). For a lot of server customers, the software stack does not change on a move to AMD.

So basically QC vying for the non intel market share until PC market comes back up again? DC requires consistent delivery for years.

Edit: Not downplaying arm incursion → Only that arm will continue to chug along as long as intel does not fix its issues. If intel fixes itself, we could again see a road full of dead server CPU projects few years down the line (history will repeat). Next 3-4 quarters can decide. intel needs to get its sapphire rapids server CPU out.

More competition is always good for a customer so that no single vendor dictates price and other terms. Let’s wait and see how things pan out.

QC will be trying to do what Apple did with their M1 chip for the Mac desktops and laptops but in the Windows, Linux side. And Microsoft is receptive too by giving ample support for arm based architecture.

Nuvia CEO Gerard Williams, who was former Apple’s chief CPU architect for nearly a decade, is now Qualcomm’s SVP of engineering. If the Nuvia chip designs are half as successful as Apple’s industry-leading chips, Qualcomm could become a major server chip competitor.

There’s no timeline for when Qualcomm’s server chips will be available, but Qualcomm’s current schedule has Nuvia technology showing up in laptops in “late 2023.”

Post the pre announcement of earnings… the gross margin will be a shocker for the market. Because nvda has set the bar for > 60% gross margins for long.

Intel Sapphire rapids delay has created some problem

OK. Our Hopper supports previous-generation CPUs. But I guess, next-generation GPUs – CPUs, Sapphire Rapids and Genoa after that, as well as Graviton. And so we certify and test across all of the CPUs because the cloud service providers demand it.

And they intend to deploy NVIDIA accelerators, NVIDIA Hoppers, across a large number of CPUs. There is no question that the delay is disruptive and a lot of engineers have to scramble. It would have been a lot easier if next-generation CPUs were to have executed more perfectly. However, Hopper goes into an environment with CSPs where they connect our PCI Express connectors to old-generation, current-generation CPUs as well.

→ More sales for AMD CPUs until intel SPR/nvidia grace CPUs come in.

Unable to say how much the decline is contributed by crypto!!!

We are unable to accurately quantify the extent to which reduced crypto money contributed to the decline in Gaming demand. While Gaming navigates significant short-term macroeconomic challenges, we believe the long-term fundamentals in Gaming remain strong.

→ We will know in two quarters. This cannot be hidden like earlier when only NVDA was running the show. Since now AMD gaming data will come in and we can see how much gaming recovers from Q4 onwards - Some history. https://www.sec.gov/news/press-release/2022-79

So our gross margins outside of the inventory charges in Q2, as well as going into Q3 is really about our sales mix that we have and probably also to understand that our sales mix in the next quarter for GPUs is not in the high end. And so that has impacted our gross margin as we move into Q3.

You are correct. We do expect that Data Center will assist in our gross margins, but we also have growth plans in Auto. Auto is below our company average, and so that will tend to offset some of those upper-bound things that we will see in terms of Data Center.

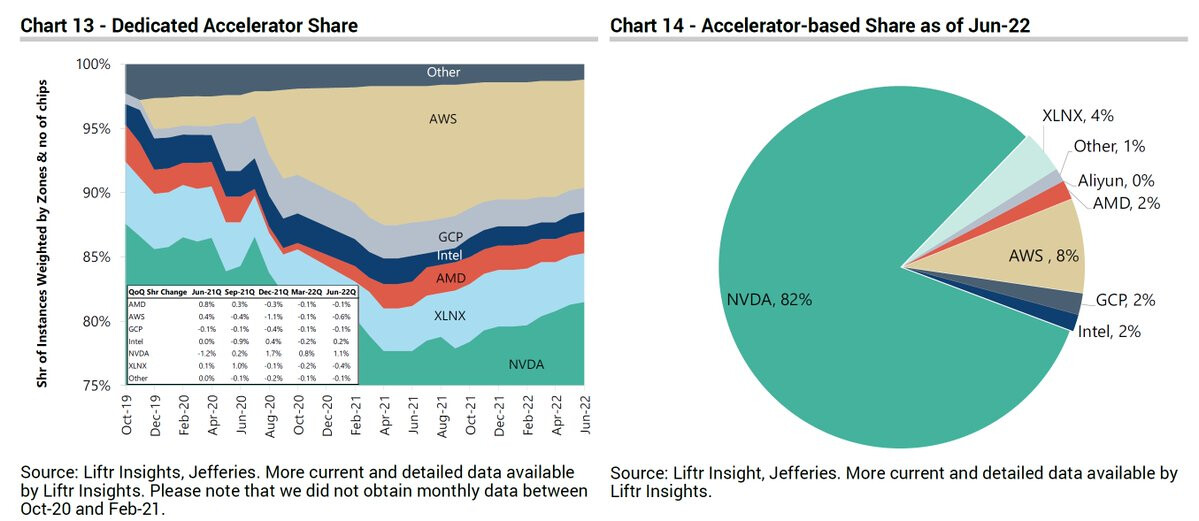

Long term still good. Also notice the stickiness of data center. One reason we focus on datacenter. Data center accelerator space, nvidia owns it… based on the charts shown below

Settle or close biz? It appears qc refused to settle before this.

Because Qualcomm attempted to transfer Nuvia licenses without Arm’s consent, which is a standard restriction under Arm’s license agreements, Nuvia’s licenses terminated in March 2022. Before and after that date, Arm made multiple good faith efforts to seek a resolution. In contrast, Qualcomm has breached the terms of the Arm license agreement by continuing development under the terminated licenses. Arm was left with no choice other than to bring this claim against Qualcomm and Nuvia

Nvidia said that it was working with customers in China to divert its purchases to alternative products, and may seek a license where replacements wouldn’t work. AMD sells far fewer AI chips into China and does not believe the restrictions would have a material effect on its revenue.