Dear All,

I have been reading various threads in the Value Pickr for past 2 year. I should thank each and everyone for their insights. I have gained good knowledge after visiting the forum.

I have been a silent observer. I would like to show my portfolio and get feedback.

I mainly invest in Mutual fund (90%). I want to learn equity investment and manage my portfolio on own. Hence started with 5% allocation to direct equity and moved to around 10% now.

I started my investment in 2013 end. I didn’t have enough money to deploy. I started slow and steady. Got good profits. Sold few investment too soon after getting profits (Eicher, Britania etc). I regret those decision.

I usually sell companies if I felt valuation is high and book profits in it. Now I am changing that mentality and willing to Hold good companies longer.

This is my current portfolio. Please review and suggest me any changes.

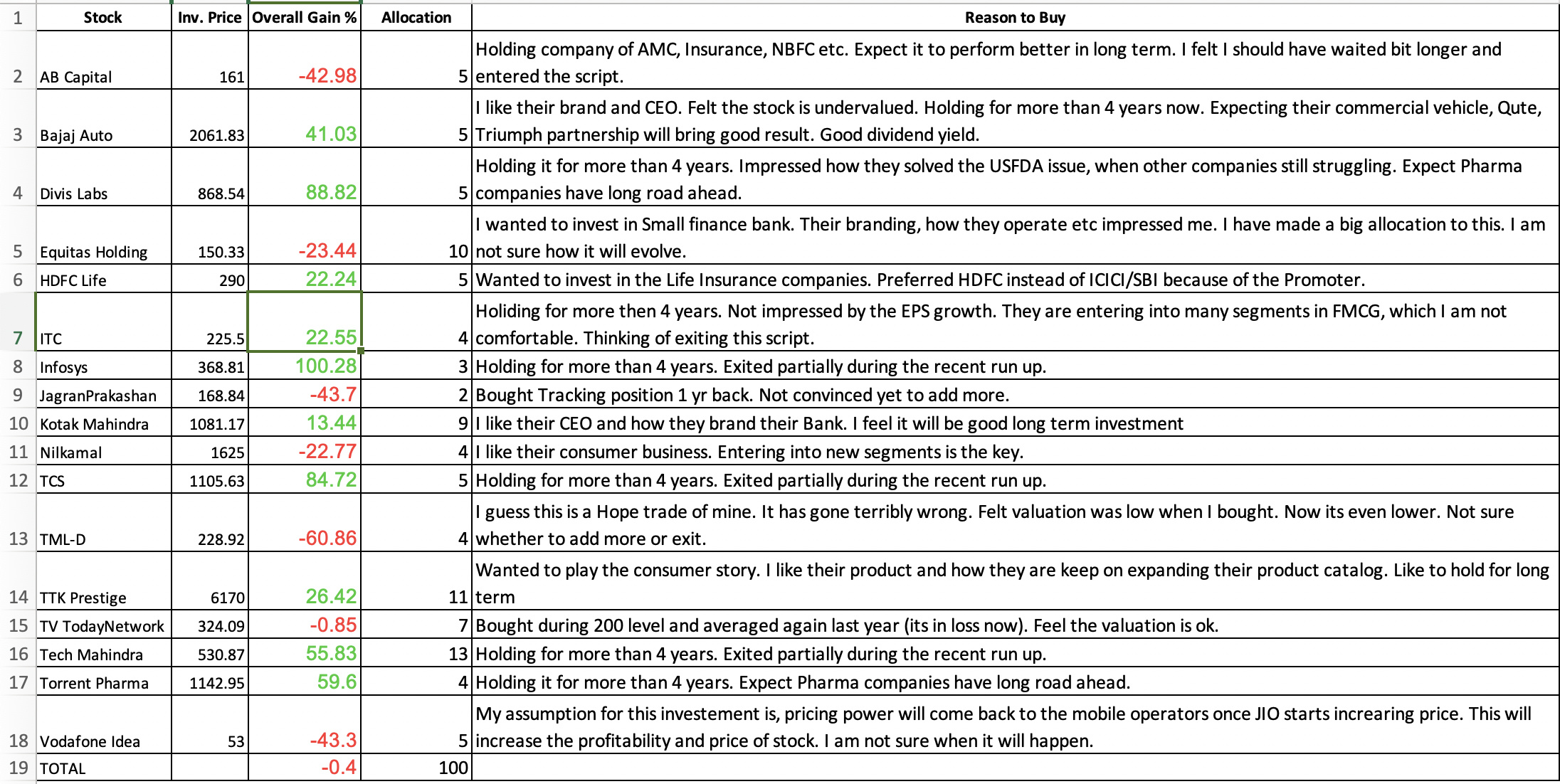

AB Capital - 5%

Holding company of AMC, Insurance, NBFC etc. Expect it to perform better in long term. I felt I should have waited bit longer and entered the script.

Bajaj Auto - 5%

I like their brand and CEO. Felt the stock is undervalued. Holding for more than 4 years now. Expecting their commercial vehicle, Qute, Triumph partnership will bring good result. Good dividend yield.

Divis Labs - 5%

Holding it for more than 4 years. Impressed how they solved the USFDA issue, when other companies still struggling. Expect Pharma companies have long road ahead.

Equitas Holding-10%

I wanted to invest in Small finance bank. Their branding, how they operate etc impressed me. I have made a big allocation to this. I am not sure how it will evolve.

HDFC Life - 5%

Wanted to invest in the Life Insurance companies. Preferred HDFC instead of ICICI/SBI because of the Promoter.

ITC - 4%

Holding for more than 4 years. Not impressed by the EPS growth. They are entering into many segments in FMCG, which I am not comfortable. Thinking of exiting this script.

Infosys - 3%

Holding for more than 4 years. Exited partially during the recent run up.

JagranPrakashan - 2%

Bought Tracking position 1 yr back. Not convinced yet to add more.

Kotak Mahindra - 9%

I like their CEO and how they brand their Bank. I feel it will be good long term investment

Nilkamal - 4%

I like their consumer business. Entering into new segments is the key.

TCS - 5%

Holding for more than 4 years. Exited partially during the recent run up.

TML-D - 4

I guess this is a Hope trade of mine. It has gone terribly wrong. Felt valuation was low when I bought. Now its even lower. Not sure whether to add more or exit.

TTK Prestige - 11%

Wanted to play the consumer story. I like their product and how they are keep on expanding their product catalog. Like to hold for long term

TV TodayNetwork - 7%

Bought during 200 level and averaged again last year (its in loss now).

Tech Mahindra - 13%

Holding for more than 4 years. Exited partially during the recent run up.

Torrent Pharma - 4%

Holding it for more than 4 years. Expect Pharma companies have long road ahead.

Vodafone Idea - 5%

My assumption for this investment is, pricing power will come back to the mobile operators once JIO starts increasing price. This will increase the profitability and price of stock. I am not sure when it will happen.