Can someone please share the recording or key takeaways from the AGM today. Thanks

1 Like

Quick notes AGM 2023 please let me know in case I missed anything.

Operational review:

a) started a drilling campaign in three fields as oil prices were high. Nearly 10 fields drilled. Karjisan back in production and is stronger than before.

b) focused during the year on enhanced governance practices and for risk management

c) increased diversity by 30%

d) investor roadshow will be posted on website for transparency.

e) increased focused on safety. Aim to be top quartile on safety

Future strategy:

a) drilling campaign have confirmed bakrol and karjisan might have improving prospects which the company will update stakeholders in due course.

b) all capital decisions will be made assuming oil prices at a more stabilized level (not at cyclically higher price).

C) Main focus on growth! Aim to move from crude to gas over the longer term. Therefore, will focus on adding more gas asset.

d) Will not do rank exploration. The company has enough resources for 7-8 years. Will focus on discoverer resources.

e) Looking to achieve reserves replacement ratio of more than 1. Trying to increase the recoverable factor in existing fields. Next year will focus on recovery potential such as water injection pilot

Capital allocation

a) while deciding on new projects they aim for Mid to high teens irr assuming lower oil price

b) When started fy 23 they had 200 crs of cash with 500 boepd and ended up with the same amount of cash but increased production to 750 boped until now.

Q&A

Achievements: a) Getting positive result from Bakrol. Karjisan drilling wells have positively surprised the management team.

b) smooth transition of takeover. Created a strong diverse board and undertook measures on safe operations.

Disappointments: a) Lohar is a declining field. Not producing as much oil and gas. Focusing on managing the cost structure in Lohar.

Antelopus Update

a) Has four license and an onshore in assam another one from Andhra

b) no revenues currently in antelopus

c) Selan in has oil reserves in cambay basin while antelopus has offshore oil and gas assets which gives a diversified portfolio of assets.

d) The money from Sean will first go to developing : duarmara, Mumbai offshore. They will will need more money from investor shareholders and will be banking on insti shareholders on capital commitment.

e) Duarmara field had issues before with forest clearances but now things are cleared up. The production schedule is more mature and is expected to start it by Q424.

Update on Eliao

a) Waiting for transfer approval from ministry. Might start drilling by next

b) Eliao post approval looks like one well for now and then will drive more wells

c) Elias has a one year lifecycle but there an optionality

Other update:

a) Timeline on merger: swap ratio will be decided soon (few weeks possibly). The merger process will take around 15 months.

b) Bakrol ec extension has been applied for. Before second drilling by next year they will have an extra approval.

c) Looking at operating leverage to lower per bbl cost

d) will come back with capes plan for FY 24 during the course if the year

4 Likes

A good set of results. Production from Karjisan has revived. During Q1’24 guided to 800 boepd production and they have achieved that by the end of Q2’24.

5 Likes

Merger announcement https://www.bseindia.com/xml-data/corpfiling/AttachLive/79b66ddf-84c5-477d-9154-22905f5a6067.pdf

1 Like

How is this merger going to work? What will the small retail shareholders going to get? No fractional entitlement to any shareholder (of the Transferor Company) is expected pursuant to the issuance of the Amalgamation Shares

The non-promoter (ie retail) shareholding remains constant. Selan had 1.5 crs shares premerger and an additional 2 cr shares are issued to the promoter company in consideration for brining in the AEPL assets into the fold.

Retailers benefit as the intrinsic value of the company is expected to be positive impacted.

2 Likes

public share holding is being diluted from 70% to 30% for the AEPL assets… all will depend on how market values AEPL assets and potential… stock has been swimming aginst the tide of falling oil prices…

2 Likes

Oil is volatile (one can assume an average pricing of 70-80 while building expectations) and it’s a business where even though you know the 2P reserves there is uncertainty on how much oil comes out of those fields.

AEPL has significant gas assets which cater to the Eastern Regions as well.

3 Likes

i think once USA starts attempting to refill it strategic reserves which has been depleted by 50% to control inflation then OIL might make a massive upmove… i have been seeing other OIL producers like oil india ,ONGC stocks very strong despite fall in OIL prices…seems market is calling US bluff on OIL prices…

1 Like

Disclosures: No investments

Stunning, in one word!

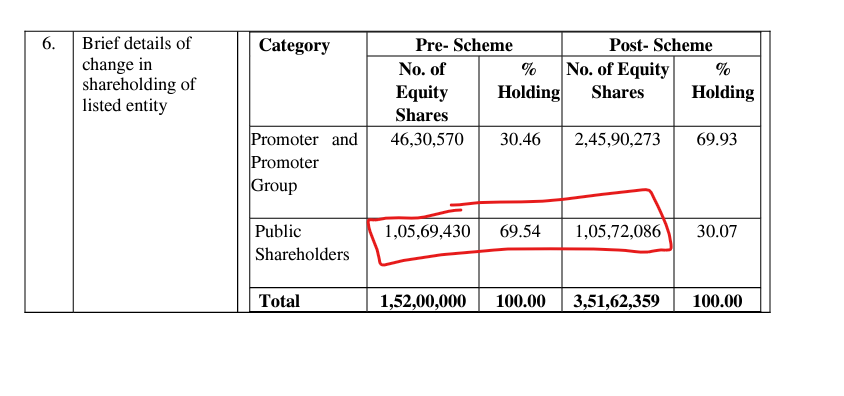

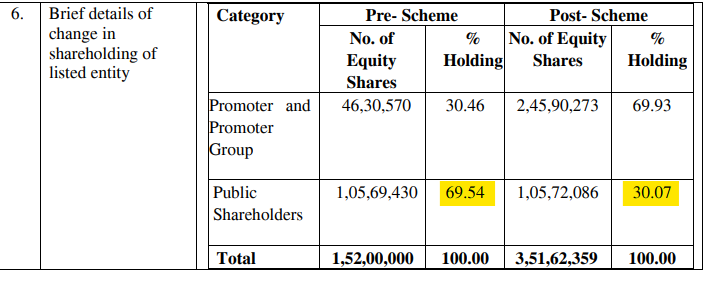

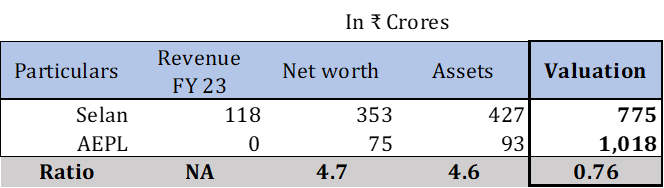

AEPL, a Promoter group company is proposing to merge with Selan Exploration, a listed company, with Promoter holding of 30.46% as on date.

Basics are as follows:

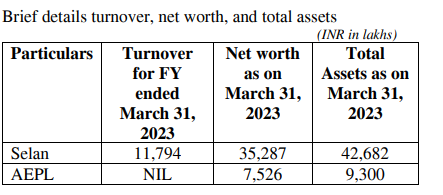

- Selan has about 4.5 - 5 times more equity and assets than AEPL; and AEPL has no revenues

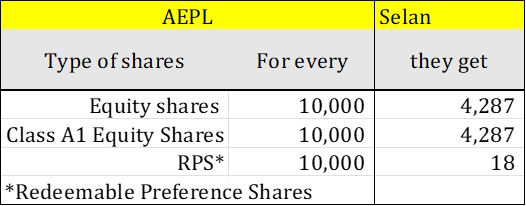

- AEPL shareholders will get the following shares from Selan for giving the above business

- Which reduces minority shareholders by a whopping 39.47% (= 69.54% - 30.07%)

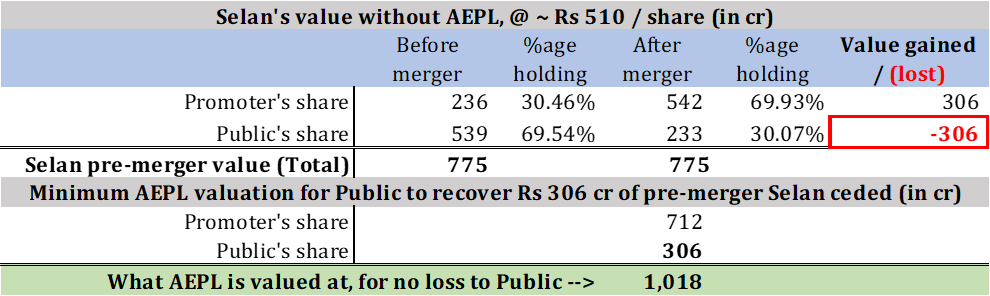

So the natural question is, what value does AEPL bring for getting in additional ~ 40% of the shares post merger. Selan has not yet said that in its filings. We can however find out the least it needs to bring in

(a) Value held by Public shareholders in today’s Selan (i.e. pre-merger) = 69.54% of MarketCap of ~ ₹ 775 cr; i.e ₹ 539 cr

(b) Value of Public shareholders in today’s Selan after the merger = 30.07% of ~₹ 775 cr = ₹ 233 cr

Thus the Public suffers a substantial reduction in the value of today’s Selan held. This loss can be calculated as ₹ 539 cr (pre-merger) - ₹ 233 cr (post merger) or ₹ 306 cr of value of today’s Selan.

The Synergy and Audit Committee however have said the merger may “Enhance value for Company’s shareholders, resulting in creation of a leading energy company in India”

So the Public needs to see atleast commensurate value of what it has today; i.e ₹ 539 cr; post merger. But today’s Selan would contribute only ₹ 233 cr post merger. So the merger has to see the value held by the Public increase by atleast ₹ 306 cr.

An increase of ₹ 306 cr of Public value, with reduced holding to 30.07%, means that the overall value brought in by AEPL is ₹ 1,018 cr (i.e. ₹ 306 cr / 30.07%). We can infer thus that AEPL is valued at ₹ 1,018 cr for the merger, while Selan is valued at ~ ₹ 775 crore today (as I write this). Thie fundamentals are below

Which is why I am really stunned!!!

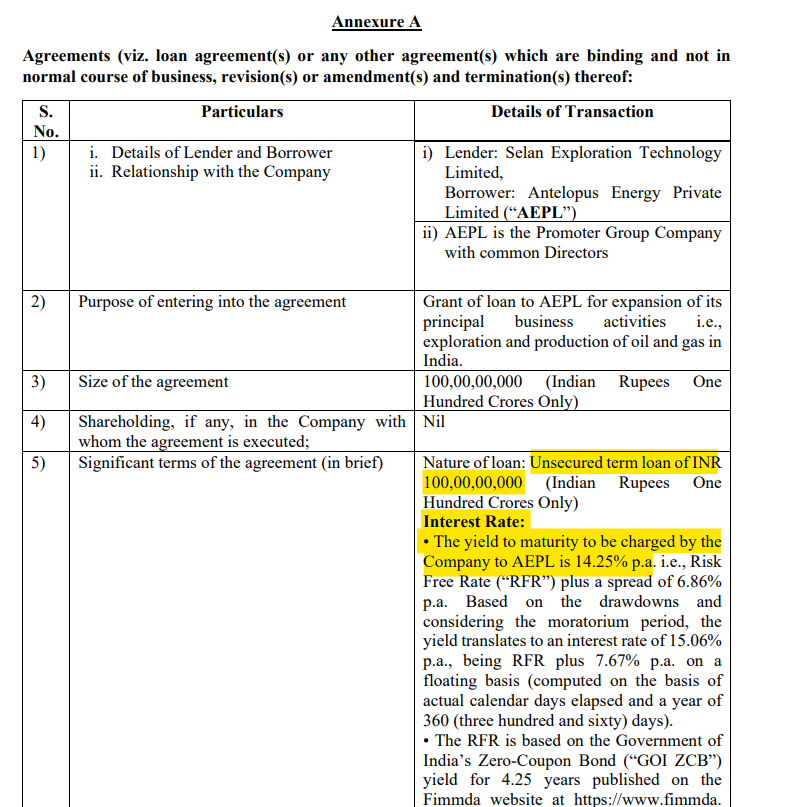

But that’s not all. This “bigger than Selan” company entered into a loan agreement with Selan to borrow upto ₹ 100 cr of Unsecured loans at an effective rate of 14.25%!

It’s surprising that a better valued company than Selan could not get a better rate from the market and had to come back to Selan!!

Putting all of the above in an Excel sheet

Sources: All BSE filings

*could not understand how Pubic shares go up by 3,156 on account of the merger

5 Likes

Thank you for putting in excel . I was also wondering the same.

Sold my tracking position.

1 Like

Thanks for sharing this. As per the latest presentation, Antelopus Energy has ~20x more 2P reserves vs. Selan i.e. 54.65 vs. 2.57 mm boe.

3 Likes

Thank you for zoning in this very interesting slide. We were invested in Selan before Antelopus, so I happened have many investor presentations, including 2P of Selan’s portfolio before Antelopus. I opened one of them to see what the 2P numbers were on Bakhrol oilfield presented by Selan before Antelopus took over. I was curious because those numbers, I recalled from memory, were much hgher than the 1.77 mmbls above.

Can I ask you to take a guess on what they were? Were they higher or lower? If so, by what degree?

Some other points to note are that (a) currently Selan has performing wells, Antelopus portfolio does not, (b) we do not know the economics of drilling these new potential but unproducing wells whereas Selan was making good money; the Capex, PSCs and management plans (c) adding up 2P of Oil / Gas reserves and comparing the ratios of pre / post Antelopus Selan is quite erroneous, if you think about it.

2 Likes

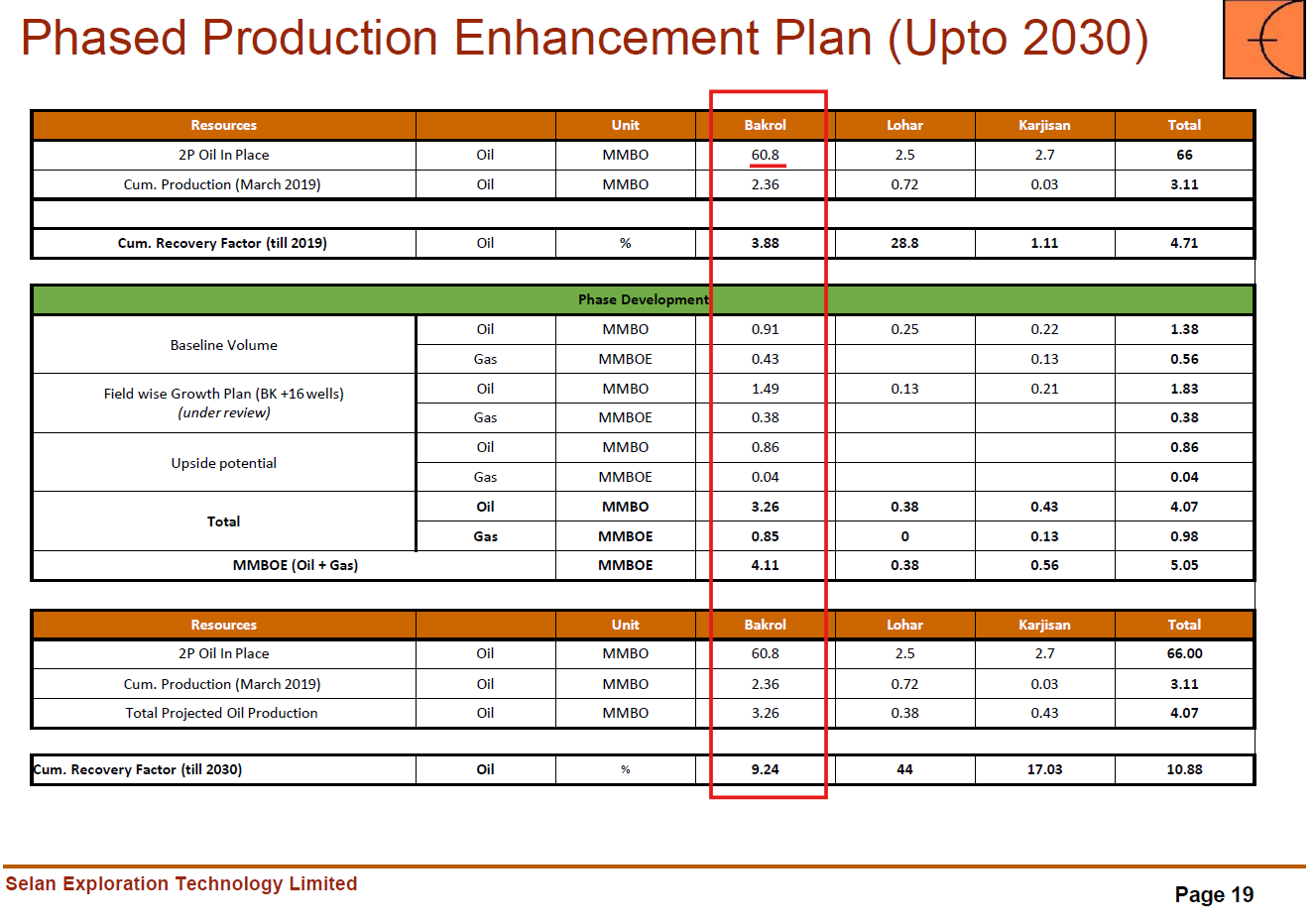

only place i found mention of 2P reserves for Bakrol, was in AR of FY09.

it says " The Proven and Probable Reserves of Bakrol Oilfield are 73.60 mmbbls after the completion of the current drilling campaign in Bakrol Oilfield."

in Q3 FY23 Investor Presentation, it mentions 2P reserves of Bakrol fields at 1.77 mmbbls.

i have already sent an email to the company to clarify.

also, i looked into the valuation report at selanoil website, for this amalgamation. the CA firm Bansi Mehta & Co seem reputed enough to not mess the valuation on purpose. but, they have valued Selan and Antelope only on DCF basis. Not on Market Price (as Antelope is not listed) or NAV method that considers reserve, tenure etc. The most important part in this report is that the DCF-based valuation is based on “projections and business plans provided by the management”. The new CEO Suniti Bhat was a director at Blackbuck Energy Investments, and a founder of Antelopus Energy. Hence, there surely is a conflict of interest, if the same person is on both sides of the company.

those who are invested in Selan and interested in forming a forum to research further and accordingly vote on the merger, please DM me.

Hi Rajul,

I have attached the presentation made by the company following Sept quarter of FY 2021. Here is the snip of the key slide. Bakrol 2P is at 60.8 MMBO vs 1.77 MMBO in Q3 FY 23.

092020 selan corp presn.pdf (2.1 MB)

1 Like