Has anyone attended AGM. If yes, please share the new Management commentary about extracting oil from new wells in Bakrol

6 Likes

“The rate paid for gas produced from old fields, which make up for about two-thirds of all gas produced in the country, was hiked to USD 8.57 per million British thermal units from the current USD 6.1, according to an order from the oil ministry’s Petroleum Planning and Analysis Cell (PPAC).”

we are on to something here…

Disclose: Invested from lower levels of 192…

3 Likes

Results + First investor presentation. That’s good progress towards disclosures (committed during the AGM) but leaves a lot to be desired (such as field-wise production data etc). Good trend hopefully it continues.

4 Likes

My understanding from the latest Earnings Presentation…

- Management gives clear outline of their development / operational plans for the next 18 months.

- Explicitly states the name of Antelopus Energy and hints at a forthcoming merger. @P2018 had predicted precisely this last year. Hats off to him.

Disc: Invested; views biased.

5 Likes

Thank you that’s kind of you!

I have been developing a framework around management changes investing so this case fit lot of those filters. Things are moving quicker than i expected but will down some interesting aspects on Selan’s operational numbers (things seem to be turning around).

2 Likes

8 Likes

But since there is no disclosure from company on crude and gas breakup, hard to gauge the impact.

Disc: Invested from lower levels. No transaction in last month.

2 Likes

Even after the company shows 50% increase in Sales, more than 3X EPS increase, PE 50% lower than median PE, we are still not seeing Stock price re-rating. When will this stock turn-around?

@P2018

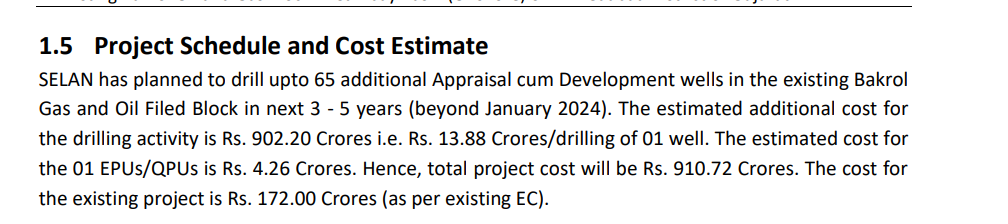

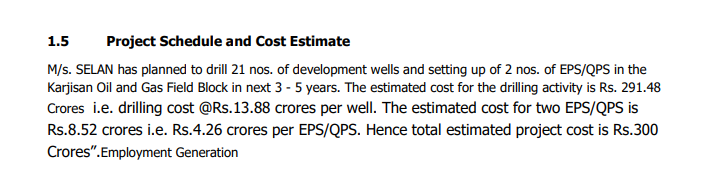

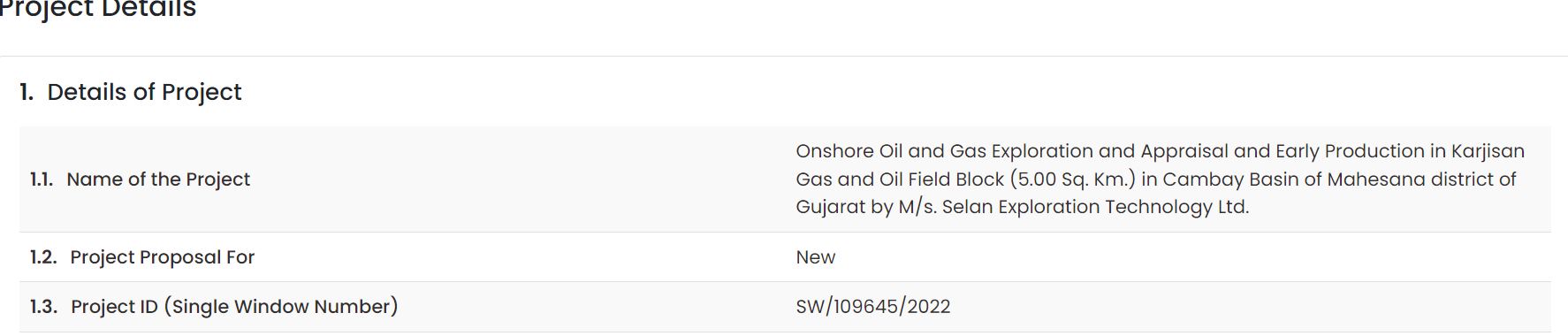

what do you make out of the 1200 cr investment that co. is doing in Karjisan and Bakrol oilfields. do you think it really means something. as per latest investor presentation they are drilling 530 barrels of oil per day but per the 1200 cr investment (900 cr in Karjisan and 300 cr in Bakrol)- they are saying to increase it to 50k barrels per day. Can it change the top line/bottom line by a lot? Pls share your views? Thanks a lot.

Thanks for the question but where did you get the 1200 cr no from? Their BS isn’t that big to make that kind of investment.

2 Likes

Sir, i got the info from the recenty filed EC by them.

Karjisan

https://parivesh.nic.in/newupgrade/#/report/ec-part-b?id=1900684&caf=1897447&ecId=1899334

Bakrol

https://parivesh.nic.in/newupgrade/#/report/ec-part-b?id=4505328&caf=4447465&ecId=4449317

i took the investment details idea from the project cost estimate.

4 Likes

forgot to attach the snippet for Karjisan

Kindly share your views since the investment is planned in next 5 years or so. So i am guessing it would be done in phases and as you mentioned they do not have the capacity to do a big investment of this size in one go. but what do you make out of this. does it mean something or nothing?

2 Likes

Ah thanks for sharing these. I wasn’t aware of these filings.

Yeah so generally EC’s are notoriously slow to approve this kind of project so it’s possible that this is the grand vision of the management team they want to take a large approval all at once. See the example of ELAO that they took over last year from the Poddar family office which was allotted under the NELP scheme in 2016 (i think) and they EC took 4 years to clear. Now when the approval comes in will be a key monitorable. They could clear soon it earlier but I wouldn’t hang my hat on that and start making forward projections just yet but strategically they seem to be headed in the right direction.

Secondly, Selan’s BS has c.a. 200 crores of cash. The Antelops entity raised around 1000 crs which they are planning to merge with Selan at some point but Antelopus has its own share of committed capex and it’s not like the promoter group will shy away from committing further capex (if it makes sense). So I am presuming that the grand plan will take place only after the merger comes thru as they will have larger balance sheet strength and will be able to leverage the Balance sheet.

Hope that helps!

6 Likes

Thank you for the info. As always very insightful and helpful.

Actually, Selan has put in 3 approvals. The first proposal was to drill 10 wells in Karjisan.

This was submitted for EC on 30th nov 2022.

The EC for the same was granted on 6th April 2023.

this was reasonably fast i think as given in 4 months. The total capital outlay is 140 cr in this one per the co.

5 Likes

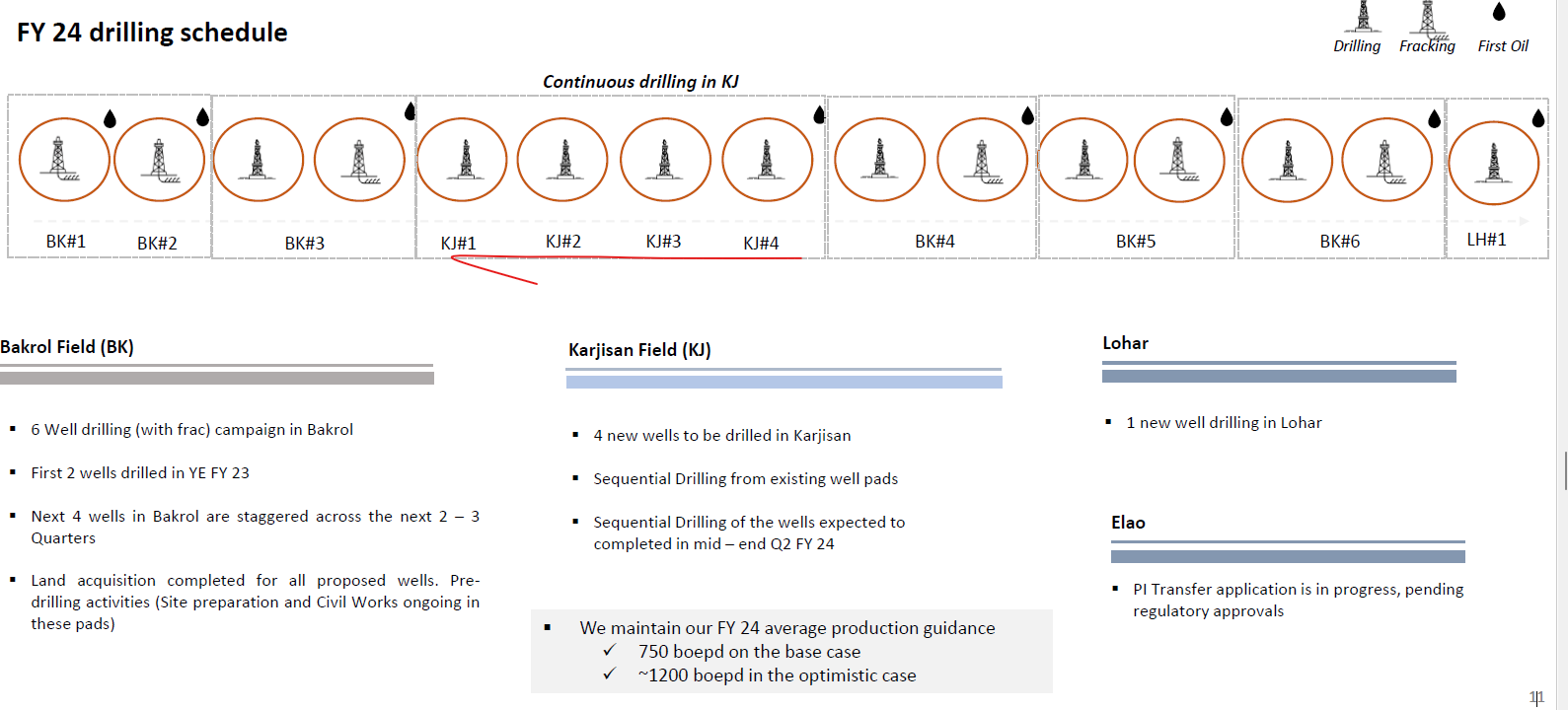

That’s a great find even management corroborates that in their investor presentation. Of the 10 wells they have an EC for they have started working on 4 I guess. It’s good to see that they will use the cash finally which should lead to improving roics and growth.

On estimating revenues from these oil fields. It gets hard for me to estimate how much product comes from these fields because these are exploratory drills. I am just not sure how much can be extracted from here. We have an overall idea of 2P reserves but it’s very ballpark.

I am just going with management’s base guidance here and will improvise as they execute.

5 Likes

P2018, your statement of 23rd June came true in just three months exactly. Selan management has declared merger of Selan with Antelopus Energy today.

What I couldn’t find in their announcement is, how it affects us small shareholders? What can we expect in terms of Market Cap, cash utilization, impact on shareholding or EPS? or anything that we are not able to visualize?

5 Likes

We will have more clarity from the management at the AGM later this week. The merger valuation is a complicated exercise in terms of valuation, tax impact, NCLT, BSE and NSE approval etc. so it will take about a year. The terms will come in due course but the management. I don’t expect them to be unreasonable to Minority shareholders as I always say that the majority shareholder (i.e. Oaktree) wouldn’t want to ruin its reputation over a $10 mn transaction.

The interesting thing is that they don’t want to wait and plan to use the cash (via an inter-co loan) to develop offshore assets in Antelopus which would have been concerning if the merger wasn’t on the cards.

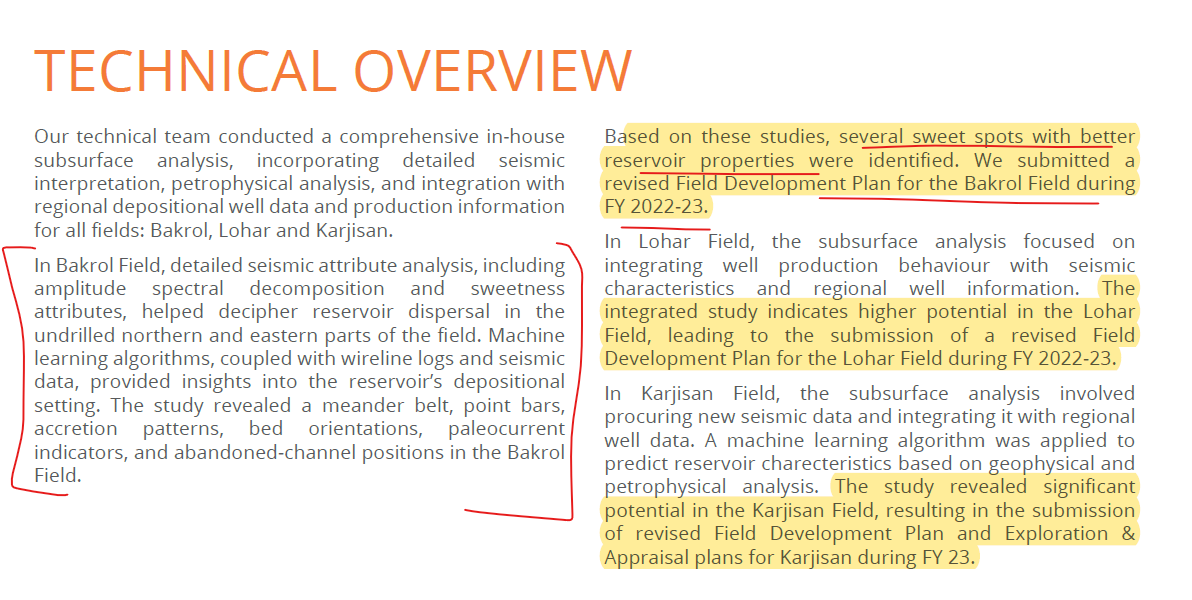

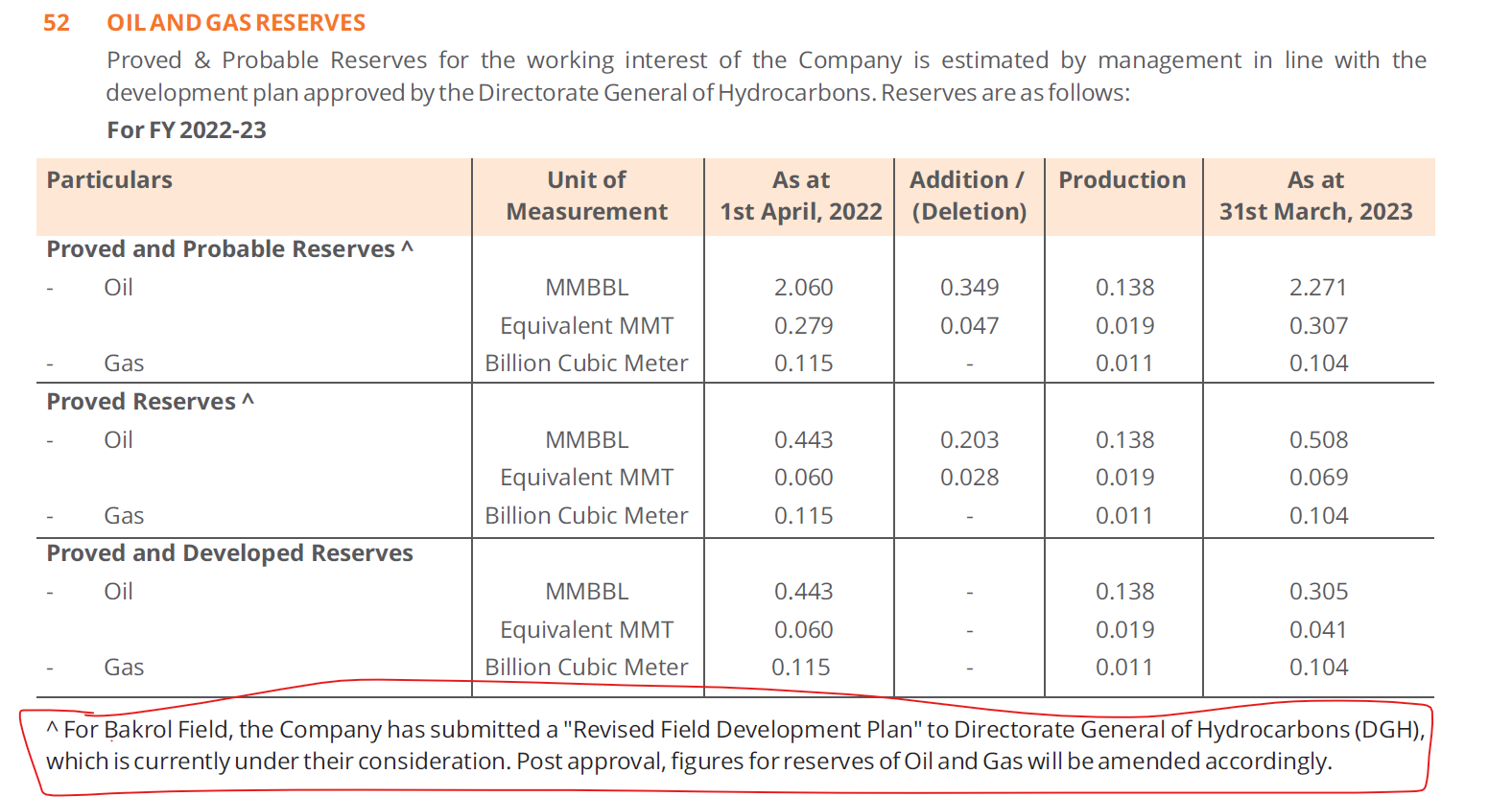

As an aside, I don’t think anyone noticed a particular disclosure in their current annual report under Technical Overview section followed by Note 52 where they disclose the oil and gas reserves. My reading is that they have found a higher reserve than expected. Hopefully, management clarifies during the AGM. Lots of optionality still in the asset. ![]()

Disclosure: invested and biased.

6 Likes

https://www.youtube.com/watch?v=rLg-hSw1B6E first management interview

3 Likes