Aarti Industries Promoter - Chandrakant Vallabhaji Gogri has the major stake in the company. He invested to turnaround the company.

Expectations of turnaround look good with the majority exposure in Middle East and India - both high growth economies.

UAE - UAE seven states at Dubai, Sharjah, Abu Dhabi, Ajman, Ras AlKhaimah; then we have GCC Qatar, Bahrain, Oman; and certain 1 or 2 customers in Pakistan; then some 3 customers in Africa right now we have.

India -We are mostly right now 75% to 80% in the western India and particularly Mumbai, Pune, and a little part of that Vapi, Daman, Valsad, and Surat.

Strong Player in its segment.

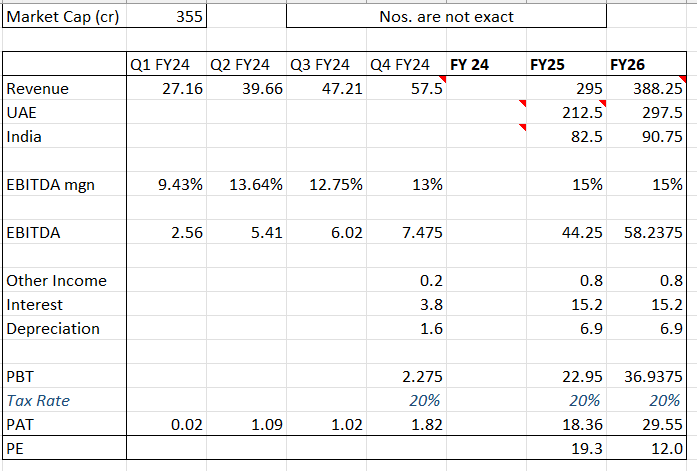

Outlook as per the company - "I will just give you the forward projections for the Q4. Consolidated, we will be around Rs. 55 crores to Rs. 60 crores for the Q4. And for financial year FY25, India operations will be around Rs. 80 crores to Rs. 85 crores and Dubai will be around Rs. 200 crores to Rs. 225 crores. "

It is confident of increasing revenue well beyond FY25 at a similar pace. (can expect 40% to be conservative.)

See 207 - 2010 Annual Report then follow up with 2011 Report (Float glass)

See 2013 and 2014 -->Secretarial auditors and Stat Auditors comments, With horrendous Float glass expansion failure a Glass company ventured in to real Estate? 3 Subsidiary were ventured into the same and funding provided did not see any revenue from there in Subsequent AR

Pre Ipo they stated Float Glass will be Import Substitute → After selling the same to Saint Gobain see the Import No.s they are decreasing as a % of sales! Questioning the Real reason why float glass expansion

2014 - 2022 4 Audtiors resigned and 3 CFOS changed!!

And the person who drove the company in NCLT is still running → Aarti Group isn’t involved in Daily Works

Many Red Flag → Space is extremely good, company is very good only anti thesis is person who is running the same is the person who was behind down fall of company between 2013 - 2019

In the concall, it seemed that they are now focused on just the next year and the glass business.

I am pretty confident that the major stakeholders will keep a check if the business activities are done in a streamlined manner and the company is not diving into different businesses

I think we should wait for another quarter to strengthen the thesis.

I will make a small position next week and increment with each good quarter.

I don’t think that much value is left in the script even if we see with forward earning. At last its a commodity glass business and re rating is not possible. Margin improvement will also be limited being commodity

Certainly the Promoter Mr. Gada (with 0% ownership now) was sounding confident of successful transition and future business. I’m sure Mr. Gogri will have close eye on it.

Hopeful of successful turnaround. Keeping watch on it. May take small bet to have ownership interest and may increase subsequently basis on quarter result as put forward by the promoter.

I recently attended the annual general meeting and con-call. The company is currently going through a transitional phase, and the previous promoter agreed to provide management support for the following three to four years.

Brief Profile: The Company is into architectural glass which is a commodity business and has an element of cyclicality. Due to stringent minimum quality criteria, the automotive glass segment enjoys greater operating margins, often between 18 and 24 percent, compared to the fiercely competitive architectural glass business, which has relatively lower margins, between 12 and 18 percent.

Company is mainly into 3 categories of products:

a) Insulated glass, [India capacity 1.8 lac sq. mtr p.a., UAE 6 lac sq. mtr p.a] – 17%

b) Laminated glass, & [India capacity 1.08 lac sq. mtr p.a., UAE 1.50 lac sq. mtr p.a] – 10%

c) Toughened glass [India capacity 7.8 lac sq. mtr p.a., UAE 21 lac sq. mtr p.a] – 73%

Considering the product profile, the company is highly concentrated into toughed glass product since toughened glass is the first process which can be utilized in Insulated glass and laminate glass, and it can be sold as a product itself.

The company might generate a topline of Rs 400cr at current capacity. The factory in Ras Al Khaimah, United Arab Emirates, operates in two shifts, as I observed during my visit. The unit is located on a 20-acre plot, of which 40% is used for built-up space and the remaining 60% will be used for future expansion.

I have asked the question from the management being an only player in architectural glass, why the company is not able to perform?

Management replied:

Hence, given the strong demand in the real estate sector and the restriction on the import of cheap glass, Sejal Glass may continue to do well domestically.

In UAE the company has an order book of approx. AED 60Mn (i.e. 120cr) at present. They are targeting a topline of Rs 200cr plus from UAE and Rs 70-80 cr from India in FY 24-25.

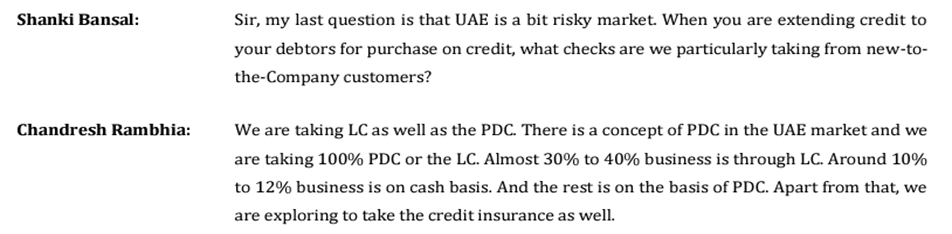

It seems they are on the right track and company is very cautious now to extend credit to their debtors.

In UAE; almost 30% to 40% business is backed by LC, 10% to 12% business is on cash basis and the rest is on the basis of PDC. Further, they are also exploring to obtain credit insurance.

Debt to equity is at 4.2x (Rs 100cr loan is extended by Aarti group (new promoters) @8-9% and rest 20cr from bank). Also, new term loan of Rs 42cr taken in Dec’23

Old promoter still running the show.

Foreign currency risks

Related parties’ transactions.

Disc: Above study is for educational purpose only and not a buy sell recommendation by any means. Invested from lower levels.

Please read forum guidelines properly before initiating a thread. FAQ - ValuePickr Forum

To nurture a vibrant community ValuePickr does not restrict anyone from starting a thread on a stock of his/her choice. Only Caveat is if you are going to introduce a discussion on a stock, we expect you to do your homework and start the thread with some basic info-set, and 1st level analysis such as growth drivers, a few positives & negatives, immediate triggers if any, and enumerate some RISKS. Nothing very heavy is required, but enough to set the tone for 2nd level of discussions.

Starting a New Thread: Please follow these guidelines - #2 by Administrator Thread initiators are usually alerted to edit their post, and make necessary changes before thread is opened up again. So you/colleague and look to edit the post in order to meet prescribed guidelines. We have the responsibility - especially the thread initiator (assumption is he/