Aditya Vision - IC - 01-02-2024 - Systematix-1 (1).pdf (2.1 MB)

Aditya-Vision-11-12-2023-emkay.pdf (2.2 MB)

2 good reports for better understanding of sector n AVL WITH lot of granularity n data

Aditya Vision - IC - 01-02-2024 - Systematix-1 (1).pdf (2.1 MB)

Aditya-Vision-11-12-2023-emkay.pdf (2.2 MB)

2 good reports for better understanding of sector n AVL WITH lot of granularity n data

Excellent reports- increases the confidence in the stock even more.

Having worked in Sales in these geographies of India- can vouch for the rising consumer spends (due to lower bases, faster penetration growths, more govt. schemes etc) in these geographies.

AVL seems to be at the right place at the right time.

Discl- Invested

We all talk about patience but very few has it… too much pessimism all of a sudden as everyone expecting 50% annual growth in PAT

Systematix research report post results…

Systematix_Aditya_Vision_Ltd_Q3_FY24_Results_Review.pdf (526.3 KB)

I have written a brief summary on the company, lot of it has been written earlier. Happy to get some feedback or questions around any particular aspect.

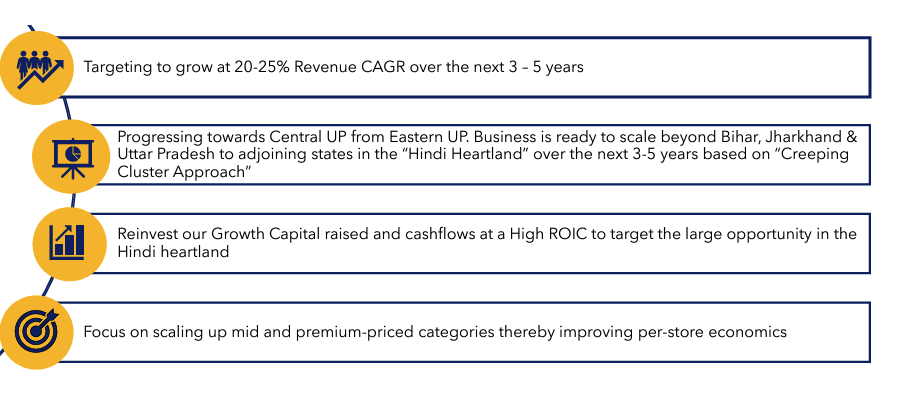

The valuation remains rich at 50x earnings (even after a 20% correction from its peak). So at this price, doesn’t seem that it will yield supernormal returns. However, with the growth lined ahead, my expectation is for it could compound at 20-25% for next 3-5 years.

They opened ~39 stores in the last 12 months (up to 3Q24) and some rough estimates (mentioned in the link), these have a negligible contribution to their EBITDA in the LTM numbers. Once these 39 stores mature, they should contribute ~INR 50Cr EBIT (vs 133Cr LTM). While a similar calculation will be true for every retailer, the pace of store opening depresses the margins and just attempted to dissect that, since store openings have been quite high for AVL in last 12 months (compared it to EMIL).

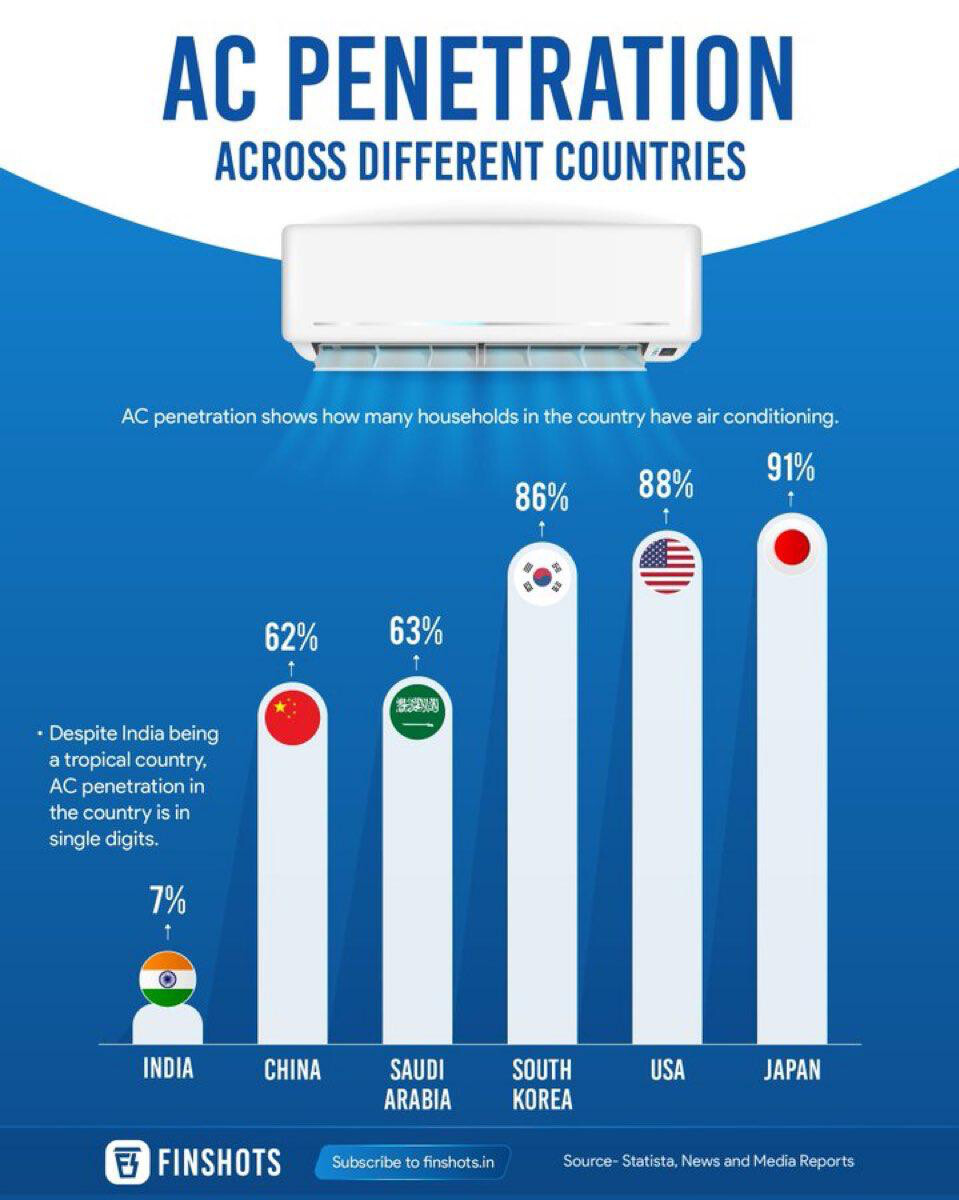

The business derives 70% revenue from the home appliances segment which largely consists of ACs, fridge etc. The sales of these goods in summer depends on the temperature and climate. Due to the delayed summer in CY ‘23, the sales in April and May were up ~15% and when summer picked up in June ‘23, the sales were up ~70% in June ‘23. This year, based on meteorological forecasts, the summer is expected to be hotter than normal from April-June ‘24. So we can expect a good Q1 for AVL which contributes almost 40% of annual EBITDA. This could act as a short term trigger.

Disclosure : Invested

I initiated a small position in AVL when it was trading around 800 levels and recently exited. My primary concern with the company revolves around corporate governance and the ongoing trend of the Sinha family members selling their shares.

I believe this could be attributed to the rich valuations at which the stock is trading. However, it does shake my confidence in maintaining a long-term investment in this company.

Given that they operate in a fairly mature industry and in a region that may not attract the interest of giants like Reliance or Croma anytime soon, it is a decent bet in the near term.

d2cfb97c-d9ec-440a-8261-6755d1f900bb.pdf (313.4 KB)

Raid at their warehouses in UP

The Uttar Pradesh State GST has canceled its previous order to seize 7 temporary warehouses and prohibit 3 stores. Now, all showrooms and warehouses in Uttar Pradesh are back to normal operations.

Emkay revises target upwards to 5150. Growth intact.

Systematix revises target downwards to 4900

Nuvama’s target is 4000 based on Dec 2023 report.

Looks like best play on white goods growth in hinterland as best white goods companies are not listed. Easy to understand business mode. Long runway of atleast a decade. Valuations are ok based on growth anticipated and execution so far.

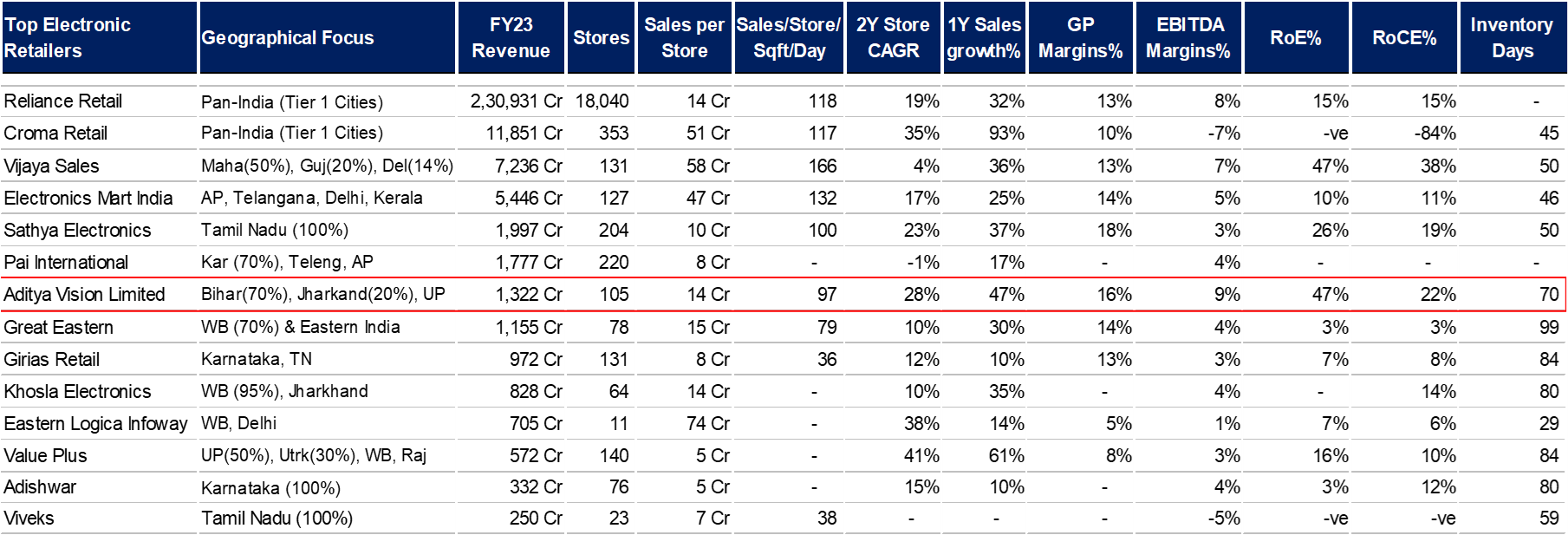

Created a comparison of all electronic retailers:

a) AVL has one of the highest gross margins, which is attributed to volume discounts from OEMs, premium pricing & better product mix

b) Better EBITDA margins are led by lower rentals and labor cost. Rental costs are lower than other retailers, as they are located more in Tier 2/3 cities and prefer opening stores in high streets rather than in malls.

c) Efficient store economics and higher margins translate to a superior RoCE and RoE for the company

d) Store Sales/sqft/day remain low at ~INR 97, compared to peer’s ~INR 115-125, due to aggressive store expansion over the last 3 years. Similarly, inventory days are inflated at 70 days (vs ~40 days in FY18-20)

e) The avg. store size of AVL is 50% smaller compared to its peers, as most of the stores are located in Tier 2/3 cities.

f) AVL generates ~40% of revenues through the financing option (low compared to listed competitor, Electronic Mart, which generates 55%+ of its sales via financing). A store typically pays ~25% of the financing cost (subvention cost).

g) While the giants Reliance Digital & Croma have store only in Tier 1/2 cities like Patna, Gaya, Jamshedpur, Ranchi, etc. both are now focusing on increasing presence in Tier 2/3 cities & have recently opened stores in smaller cities like Vijayapura, Vadodara, Solapur etc. Reliance/Croma aims to add 3,000+/100+ stores each year, majorly in these smaller cities

Valuation seems ok to enter now considering Q1 results going to be very good because of the extreme heat conditions which may have expected to rake in more & more ACs and ancillary appliances in the consumer households.

Looks so. Q4 PAT was impacted due to high inventory built up. Management seems to have positioned itself for weather forecast.

Reliance/Croma opening stores in Tier 3 cities of south-west India is like Vijayapura, Vadodara, Solapur is more like Tier 2 of Bihar like Gaya and Muzaffarpur, from operating skill perspective. Whereas Aditya vision has stores in all districts in Bihar and going to sub-division level. So their penetration level is deep. Very difficult for a national player to operate at that level as they will always look at going deeper in south-west first as operating challenges are lower and they have more bandwidth at state level in those states.

Another point about online threat apart from obvious touch and feel difference. Now most white goods companies are offering slight variation in models online and offline. So that they don’t cannibalize offline sales by comparison. If you buy something offline and search for same model online you are not likely to find it. There will be model with same capacity/size. It can be exactly same (not sure) but model number will not match.

This is a big moat in fastest growing and second most populous state.

Some excellent inputs.

Spoke to a AVL employee in eastern UP. Record tod sales . expect v good qtr june due to hot weather. sufficient inventory available with AVL so no AC shortage unlike other parts of India.

AVL at new high now may be because one of few Bihar based cos listed in stock mkt. May benefit due to expected Bihar package by NDA govt where Nitish Kumar is playing a critical support role . June qtr nos expectations also good due to scorching summer.

How is placed technically now ? Views invited.

With Revenue @1000 Cr EPS to rise by ~₹16 for Q1 YoY basis and PE to be at ~52.

PAT considered at ~6%

The long term benefit will be in holding this stock than trading. A confirm multibagger. UP and Bihar will be big time business.

Disc: Invested.

can the conference calls edited post the live session & released without any explanations . Does anyone was there on the live conference call of Aditya vision for q4fy24 ? Does The released conference call differs from what was said live ?

I was there on the call…

No changes, tone of the management is the same in transcript and on the call.

May be there is some grammar related editing and some language editing from Hindi to English. That’s all

The Board of Aditya Vision at its meeting held on 03 July 2024 has approved stock split of equity shares of face value of Rs 10 into Re 1 each. The Board also approved the proposal for listing of equity shares of the company on the National Stock Exchange of India without any public offer or further issue of shares.