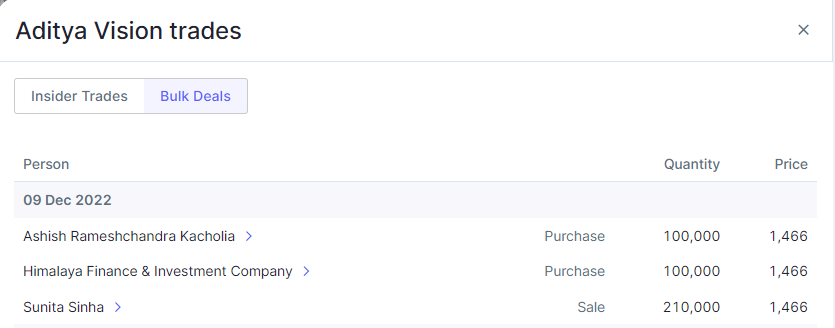

It is confusing to me Ashish R Kacholia’s investment firm is called Himalaya Finance and Investment Company.

And company said that they meet with investor “Himalaya Capital” which is Li Lui’s investment firm.

Recent Buys were from “Himalaya Finance and Investment Company”.

102 Store count by AVL

1 Like

Thanks for sharing, Have decided to sell AVL

Specially the point on including short term borrowings in operating cashflow is concerning. I had totally missed that.

No point in being a hero, 5000 other companies where i can try to better compound capital. Putting this down in the mistakes bucket.

I am honest enough to identify & admit my mistakes. Only a human.

19 Likes

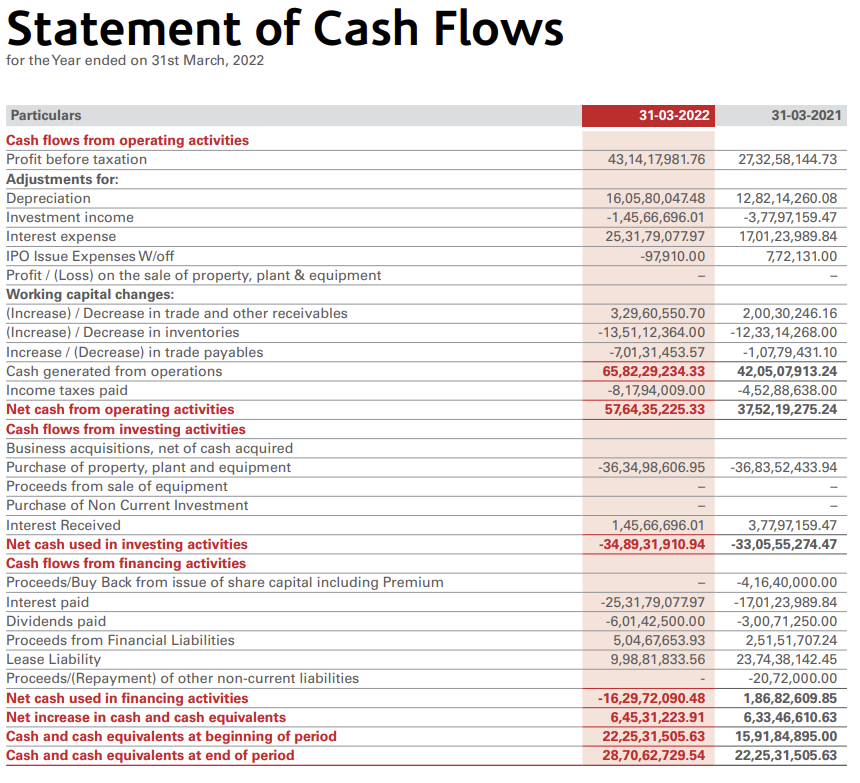

Just curious…where have they shown short term borrowing in operating cash flows? I can’t see it. Secondly even if they have shown it (which does not seem like the case) and there is a separate line item showing proceeds from short term borrowing and this has been disclosed clearly…one can easily move that to financing cash flows and do the analysis…even in this case I don’t see an accounting fraud

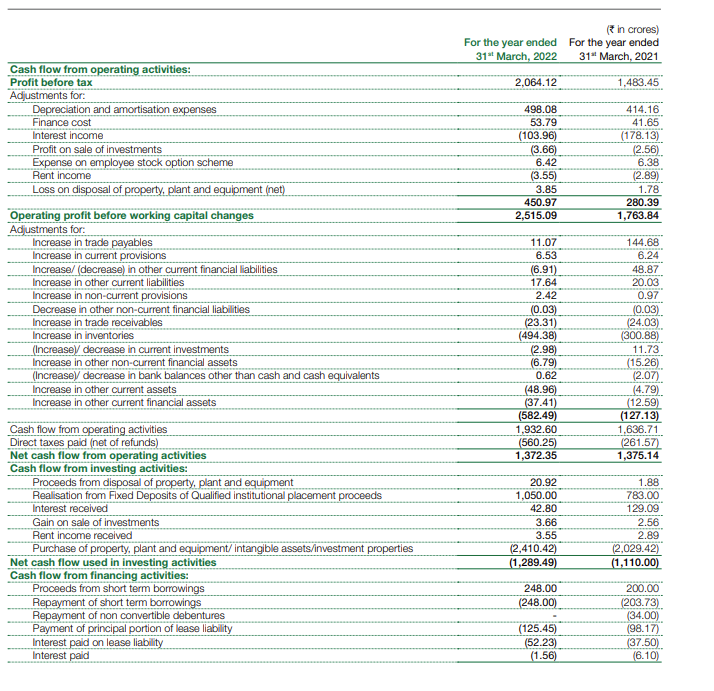

Also the principal and interest part of lease liability is included in cash flow statement (I have seen it it in D-Mart Cash Flow. See the DMART financing cash flows below)

Are we sure there are accounting shenanigans? Are we trying to say the auditors are fraud? That is a very serious allegation.

Small companies always take some extra time to move from GAAP to IndAS…this is not uncommon. FY22 is IndAS compliant. Most investors are looking at FY22 profitability and 9MFY23 profitability and extrapolating the future…can someone explain what then is the problem in this…

I was looking at the profiles of the people working in Pronirmiti who put out this tweet. All from the Doshi family. (One of the family is on valuepickr @Rushabh_Doshi). One is a graduate in dental science, one is an engineer and so on. You really think a non CA in India can figure out accounting fraud looking at annual reports? A series of statements have been made and looks like investors have panicked without checking if the statements are true and even its true if it is really an issue.

One more important thing. The company’s credit rating is being done by the best and most stringent rating agency in India CRISIL not the likes of Care or India Ratings. Please see screener.in

Allegations of storification is okay. You dont like the story that is okay. But allegations of accounting issues are different.

Yes 2000crs is small. It does not qualify as midcap in India. Its a smallcap with no institutional investors.

17 Likes

I have a question related to this Accounting fraud. This cash flow statement was out in the FY21-22 statement. How come other people till now didn’t noticed this issue?

Once this issue was out , Stock price of this company plunged more than 10% after the below thread

https://twitter.com/pro_nirmiti/status/1646031545734508544

Disclaimer: Tracking from the long time.

4 Likes

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 20 hours.

105 stores and more in next few months.

Business is growing.

Disclaimer: Invested

2 Likes

The best return comes when a good business is facing some temporary headwinds otherwise usually everything is already baked in the price. The current issue related to corporate governance practices can be one such type of a temporary issue. Or it may even turn out to be game spoiler for many. Usually the line is very thin between the two extremities of add more or sell and many times it’s not so clear and discernible. It’s always individual’s choice and decision making at the end of the day. That’s why everybody’s returns are different despite almost everyone having the access to the same information.

I am not trying to be an expert here on forensic accounting but I will continue to hold and add more on dips till the time results continue to meet expectations.

Disclosure: invested and very likely to be biased though I try not to be.

2 Likes

Be careful, PC Jeweller and Manpasand beverages fall in same category. Nobody thought PC will come down from 600 to 26, that took almost three years. Manpasand was clear Sales inflated numbers and GST fraud, still it took 18 months for stock to vanish, not doubting anything on AVL but I have made a hardline to avoid if any corporate governance issue is found.

7 Likes

Well noted. Whatever you saying is 100% true. Trying to mitigate the risk through position sizing is the key here for me. Depends on how much price I am comfortable paying, if proven wrong. Definitely views have to change when your thesis is broken. But my thesis in this story was not based on this company having the best of the accounting practices. Doesn’t look like such a grave thing or a scam. Highlighting issues like this may even help them in improving their accounting and corporate governance standards.

3 Likes

Yes please if the original posters of the article could clarify on the accounting treatment of lease as mentioned by poster above.

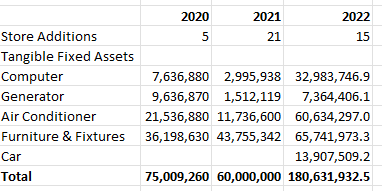

Another clarification is mentioned re inconsistencies around the number of store additions and Gross Block. It does seem that in 2022 they did invest heavily in stores (new + old).

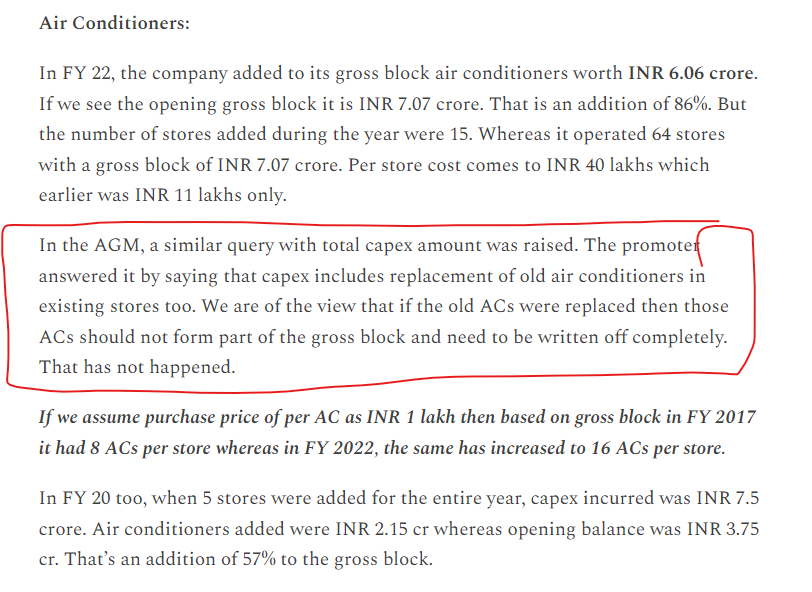

A comment was made that replacement of Air Conditioners was a one-off capex for replacement in old stores. Now when the air conditioners (in the old stores) were capitalized they would have also been depreciated over a period of time. I generally agree that the Net Block (Gross Block - Depreciation) should have been eliminated from the books which is a possible accounting oversight. Though management should clarify and state how much pertains to refurbishment and how much for new stores.

If there are concerns about management siphoning off funds I think one should look at the disclosures where management (and family) state the remuneration they take out from the business (which appears a bit high). I don’t like it but I think it’s in plain sight for everyone to see.

7 Likes

Both Aditya Vision and Electronics Mart are look alike. However the margins for Aditya Vision are much better. Surprisingly the capex per store for Electronic Mart appears lower and even it’s inventory turnover is much higher but still Aditya Vision has much better ROCE and ROE. One of the reasons could be that Aditya Vision sells more of A/Cs and Washing Machines vs phones and other smaller electronic items. Larger Appliances have 16-20% margin while smaller ones have 6-10% margin

Source:Which is the coolest one..

8 Likes

Reliance Digital is also Now entering into tier 3 cities… given the size, can Reliance Retail be a threat to Aditya Vision growth in coming years

1 Like

Every hard working and creative business is a competition in trade. That is what as investor we have to see; who is better at it?

1 Like

Company results conference call recording that answers all question raised by the hitjob put out on twitter.

The call is super insightful and worth a hear

13 Likes

112 stores now and counting…

Disc: Invested

1 Like

Aditya Vision has opened its 112th Showroom at Ara Road, Bikramganj, Bihar. Earlier, the company had opened its 111th Showroom at Mohania, Kaimur, Bhabua, Bihar. https://www.moneyworks4me.com/company/news/index/id/575390

Disc: Invested

3 Likes

Total store count 114 Varanasi and Mughal Sarai added.

1 Like