I had to ask couple of questions. But there was only one investor who asked all the questions. That investor was none other than our @ayushmit bhai, he had come so well prepared and asked some 15/20 odd questions which covered most of the investor questions on AVL. He came so prepared for the AGM and had infact mailed them the questions to management in advance, which is something to learn for future AGMs.

I was surprised with management response, they answered all questions one by one patiently for at least 30 to 45 mins. Even Ayush bhai got surprised as he never thought they will give so much time to one investor. I became like a management interview and Q&A session, much to the benefit of other shareholders.

It will be great if Ayush bhai shares his experience here.

I could not take the notes.

Hope company uploads the AGM video on you tube for learning to all.

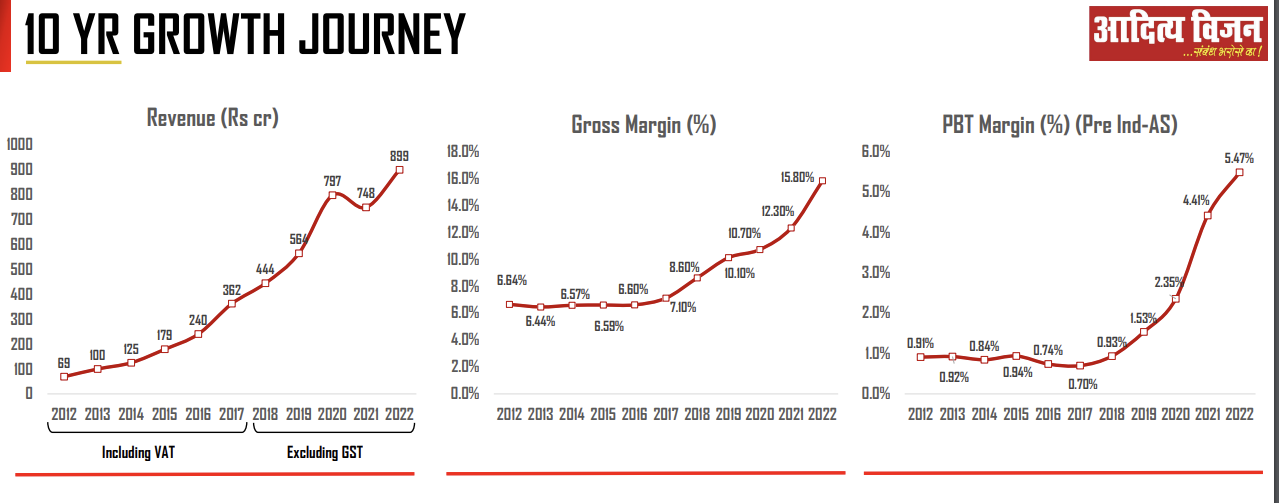

One question which was most interesting by @ayushmit as he asked out of FY 22 sales of 900 cr , how much is the contribution of old 42 stores ( up to FY 20) and new 45 stores. Management said around 850 cr i.e close to 90 -95 % of FY 22 sales were contributed by old stores up to FY 20. So new stores are yet to contribute in big way and every year they will open 25 new stores as per investor ppt. This gives lot of comfort on long run way of growth at least till FY 25.

I misspoke on the inventory point. I revisited my notes and updated understanding is that the display models in store rooms are on OEM’s books but yes, co does keep inventory. However, management has clarified in AGM that the inventory while on aditya’s books is sell or take-back model (if AVL cant sell it, OEM will take it back). Management has also added in AGM that reason for keeping high inventory is doubling of store count (new stores have not been ramped up yet - old stores contribute to 85-90% of topline in FY22). High inventory is also helping in higher margin. This could be part of explanation for GM expansion between FY20 & FY22 (see inventory levels in FY19: 70 cr & FY22: 200cr).

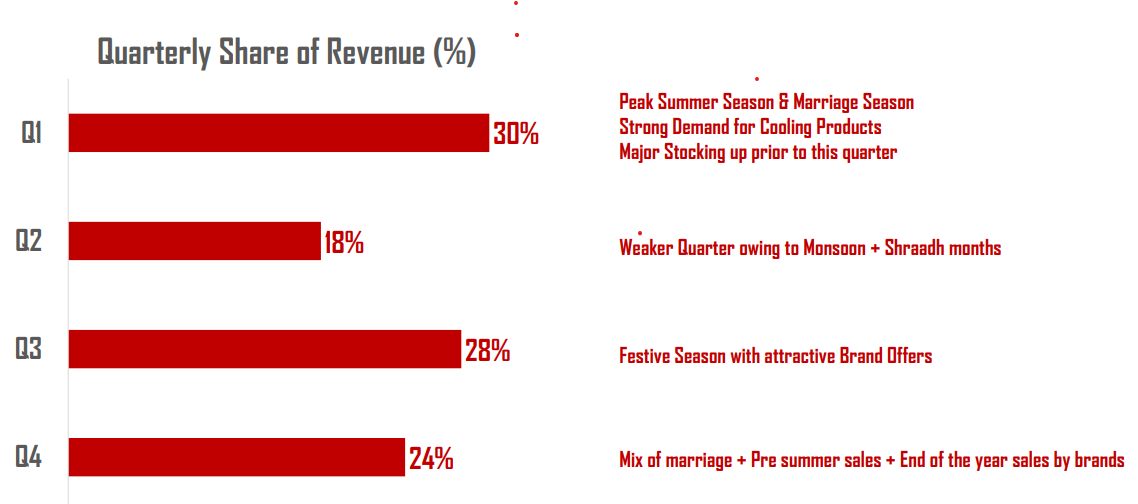

the interest outgo is not for the borrowings alone but might include financing for inventories & payables. Also, do remember that interest payment is for the year whereas inventory & borrowings is a point in time number (Q4). Inventory would be peak around summer time, then around festive season time. Q4 is generally their third worst quarter.

Point well taken on the inexplicability of interest outgo in FY20 though. This is something we need to keep in mind, possibly ask management if they start doing concalls (seems to be headed in that direction given that they have started to open up).

The interest outgo in Fy22 seems more reasonable i think.

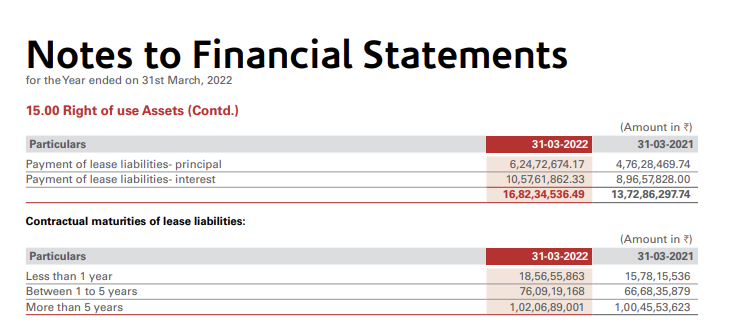

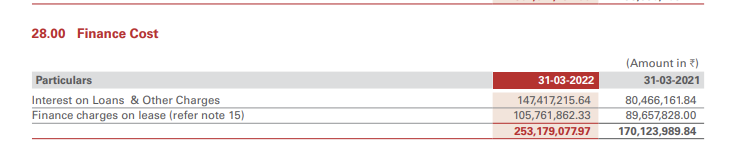

On a borrowing of 240cr, interest outgo is 25 cr in FY22. That is a 10% interest outgo. The missing part is lease liabilities. The interest outgo for lease liabilities is large.

At the same time we must recognize that the scale up in profit & revenue has also been exponential. The scale up in price with fundamentals give some more comfort to investors, i think.

If we divide 1Q23 sales by 30% we get Rs1463crs. Last year PAT margin across quarters are as below

5.2%

3.8%

4.2%

3.1%

3.9%

6.2%

1Q21

2Q21

3Q21

4Q21

FY22

1Q22

So 1Q PAT margin is higher by 1% v/s last due to scale. If I assume similar scale advantage for full year could expect 3.9% +1% =4.9% PAT margins for FY23.

4.9% X Rs1463crs = Rs72crs which you rightly pointed out is lower than Rs90crs I had earlier estimated. So stock would trade at 26.2x FY23E

i bought three large ticket items ( Samsung TV (price 70k) , fridge (50k) and mobile(80k) and in all these cases i got best deal from croma , reliance digital and croma respectively. better than vijay sales , online ( even during online sale) . This gives me sign of coming time where croma and reliance digital would become serious competitor to aditya vision , bajaj electronics sales and vijay sales. again , under watchlist because every stock offer some value at some price .

You are perhaps not getting the drift of my question. Amrutanjan is the no. 1 pain balm in south India. Lets say someone on this forum says…I bought Zandu balm as that is the best pain balm in India. He is a north Indian and has done this purchase in Delhi. Do you think his personal experience and anecdote is relevant for Amrutanjan’s business in south India? Based on this will you say prospects for Amrutanjan’s business in south India is poor?

It is also similar to saying that people is south India will prefer seeing Ranveer and Ranbir over an Allu Arjun (of Pushpa fame) or Yash (of KGF fame)

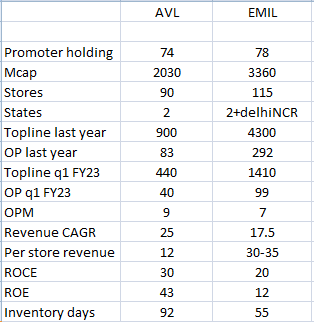

One major risk I’m finding is the GM of Aditya Vision. Don’t know if it can go any higher. EMIL’s DRHP also caps GMs for organized players at ~15%. Maybe this is peak gross margins, although management is saying sustainable, is it really sustainable?

Aditya Vision is running on the growth story (read number of showrooms added every month) in urban, semi urban, emerging urban, good income rural area. Margins will sustain between 4% to 9%. Multi-brand Retail has its challenges.