Notes from SIS AR 2019:

Key Highlights:

• Vision 2020: We aim to be number one in each of our verticals – Security, Facility Management and Cash Logistics.

• 21.6% revenue growth, 17% EBITDA growth, 31.7% PAT growth and 29.6% EPS growth

• 18.6% ROCE and 50% OCF/EBITDA

• India security, Australia & APAC security and India facility management contributed 38%,49% and 13% of revenue respectively

• The consolidated revenues and financial results include the financial results of SLV and Uniq for 7 months and 2 months respectively and hence the full effect of these acquisitions will occur only in the next financial year.

• During the year under review, we also incurred significant costs on account of deployment of the three-year contract from Cognizant Technologies and provisioning on account of the receivables from certain customers who were going through an insolvency process.

• Now, #1 security player, #2 facility management player and #2 cash logistics player in India

• 215429 employees and 17,800 sites under management

• Facility management business is 1000 cr+ business in < 10 years

• made five acquisitions across three geographies,

• In India, market growth is closer to 3x GDP for the last 15 years. see the same trend continuing in the near to mid term.

• The customer preference is clearly moving away from unorganised—non-compliant—operators to the organised service providers

• has less than 5% market share in each of these segments. In other major markets like the US, the UK and Australia, market leaders tend to have 15-20% market share. Hence, we believe that there is substantial headroom for growth

• Our inorganic strategy is centered around building partnerships and not acquisitions in the traditional sense. We believe that only by incentivising the target company founders through an earnout structure following a majority stake acquisition upfront, will they be able to grow faster. The case of DTSS is a perfect example of this; where the revenues have grown at a CAGR of 25% and EBITDA at 42% in the three years since acquisition. Our M&A programme is geared to ensure that downside is protected while sharing the upside with the target company promoters and management.

• We are bullish about the prospects of solutionbased selling as technology increasingly becomes cheaper and more efficient.

• We have delivered some interesting solutions during the year, case in point being our work on leading oil & gas companies. Solutions offer higher margin potential and longer duration contracts, and can transform the nature of the industry.

• Despite increasing competition, we have consistently grown at 1.5x the industry growth, thus gaining market share. We feel that we are making the right investments in people, technology, inorganic growth and new business solutions that establish a clear moat.

• Scope: 80,000+ Crore Indian market growing at 18-20%. Potential to be a 150,000+ Crore market by 2025.

• With acquisition of Rare Hospitality, our healthcare offerings and credentials have deepened.

Acquisitions

• SLV provides Security Solutions, electronic surveillance, event security/ management and security consulting services. The acquisition of SLV provides SIS a market-leading position in Delhi-NCR, which is among India’s top three security markets. SLV closed FY19 at 260 Crore in revenues with a majority of the revenues coming from the NCR region. Effective September 01, 2018, the Company has acquired 51% shareholding of SLV for an aggregate consideration of 505 Million.

• Uniq provides industrial Security Solutions, electronic surveillance, Facility Management and security consulting services to 430+ customers. Uniq’s acquisition provides SIS a strong position in Bangalore, the second-largest and fastest-growing market for security solutions in India. Uniq has a high quality and long-standing clientele. The business generated over 165 Crore in revenues in FY19 with a majority of the revenues coming from Karnataka region. Effective February 01, 2019, the Company has acquired 51% shareholding in Uniq Detective and Security Services Private Limited for an aggregate consideration of 515 Million.

• RARE Hospitality provides Facility Management services to 80+ customers through 4,000 employees. has an especially strong presence in Western India. It has a reputed customer base in the healthcare vertical, an area of focus for SIS. Effective November 01, 2018, the Company has acquired 80% shareholding in RHSPL for an aggregate consideration of ` 319.66 Million.

• Henderson Security is the third largest security company in Singapore. Effective February 28, 2019, SIS Group International Holdings Pty Ltd., a subsidiary of the Company has acquired 60% of shareholding in SIS Henderson Holdings Pte. Ltd. for an aggregate consideration of ` 2,280 Million

• Platform 4 Group is a relatively small but important vehicle that provides us a foothold in New Zealand. Many customers in Australia look at combined contracts across the region and a New Zealand presence was vital to bid for these contracts. Effective February 28, 2019, SIS Australia Group Pty Limited, a subsidiary of the Company has acquired 51% shareholding in P4G for an aggregate consideration of ` 66 Million.

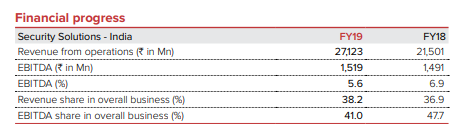

Security Management – India

• Recorded 17.6% organic growth on the back of strong customer wins and retentions.

• The EBITDA margin declined from 6.9% in FY18 to 5.6% in FY19 primarily due to significant costs incurred by us on account of deployment of the three-year contract from Cognizant Technologies and provisioning on account of the receivables from certain customers who were going through an insolvency process

• Registered customer retention ratio at 95%.

• Crossed 200 Crore monthly revenue run rate and ended the year at a monthly revenue run rate of 265 Crore (including SVL and Uniq)

• Won the single largest contract ever in India’s security industry with the Cognizant contract.

• Rolled out M-Trainer—our digital learning platform—on tab/app and on wheels, enhancing on-job-training for our field staff.

• Being India’s largest Security Solutions player with 4% market share, we continue to enjoy significant growth headroom

• Going forward, we will continue to optimise synergies in the acquired companies, strengthen brand salience and build more traction in Man-Tech solutions. Additionally, we will focus on consolidating our position in key regions and enhance our working capital management.

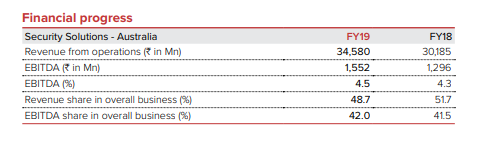

Security Management – International

• On a consolidated basis, the Security services – International segment, comprising MSS, SXP, Henderson Group and P4G recorded revenues of AUD 691.35 Million during the year under review against AUD 603.46 Million in the previous year. This represents a growth of 14.56% over the previous year. In Australia, our revenues grew by 13.64%, which is noteworthy considering that the Australian industry is a fairly developed and stable market and its economy grew at 2.9% in 2017-18.

• New contracts representing annualised revenue of AUD 45 Million were won during the year and an overall retention rate of 96% was achieved

• 20% market share in Australia

• During FY19, we forayed into New Zealand and Singapore with the acquisition of Platform 4 Group Ltd. (51% holding) and Henderson Group (60% holding), respectively. The acquisition of Platform 4 Group Ltd. will enable us to bid for customers who require joint contracts for Australia and New Zealand while Henderson Group offers significant opportunities to bid for large government and quasi-government contracts in Singapore. Henderson enables us to access regional APAC level contracts, which are decided out of Singapore.

• A mandatory increase in the minimum wage is the most significant driver of revenue growth for security solutions.

• Executed Commonwealth Games contract.

• Ended the year with Days Sales Outstanding (DSO) of 46 days – in the process, generating free cashflow of AUD 27.3 Million

• Our present strategy will focus on strong organic growth in these regions and integrate these entities to realise optimum synergies and cost savings. Going forward, we will concentrate on delivering solution-based service offerings that will enable cost-effectiveness.

Facility Management – India

• The year saw a significant increase in our facility management business with revenues going up from 6,744.85 Million in FY18 to 9,499.17 Million in FY19, an increase of 40.84%.

• The consolidated EBITDA of this segment also went up from 332.50 Million in FY18 to 639.90 Million in FY19, an increase of 92.45%, and the EBITDA margin also went up from 4.9 % in FY18 to 6.7 % in FY19. All businesses contributed to this increase in revenues and EBITDA.

• has been focusing on the healthcare, hospitality and commercial facility segments

• We also increased our B2G business with our Railways vertical expanding significantly with more services and more stations under coverage.

• We also launched our Total Facility Management (TFM) programme which will target selling integrated services to our customers

• Our FM business has the largest branch network among all FM companies in India.

• We have made steady investments in technology across onboarding, payroll, audit, quality assessment, training etc. to establish a clear differentiator for customers while also improving productivity.

• Also, the market is witnessing a significant shift from unorganised sector to organised sectors owing to the increased regulatory interventions.

• We operate three brands in India’s Facility Management industry: ServiceMaster Clean (SMC) Dusters Total Solutions Services (DTSS) and Rare Hospitality (Rare). While SMC has been in operation for the past ten years, we acquired DTSS in August 2016.

• Growing preference for integrated players who provide a one-stop shop for facility management needs, rather than unorganised companies that are incapable of providing integrated services and do not have a good track record of compliance.

• Increased overall revenues on the back of strong wins in Railways, corporate and Integrated Facility Management (IFM) contracts.

• Our priority is to work towards expanding our revenues through pan-India presence, high-value large contracts and integrated Facility Management contracts. We will continue to focus on healthcare, pharmaceutical, hospitality, manufacturing and IT & ITES sectors with ‘smart solutions’, based on digital drives and smart mechanised cleaning, aimed towards productivity and process improvements.

• The biggest opportunity in Facility Management is in offering more technical services, more vertical specialisation and integrated services. Newer models of facility management are evolving which are more output oriented and we are working actively to develop and make changes to our business and contractings model and internal systems to adapt to this changing requirement from the customers. Government outsourcing can be a big opportunity for facility management in India and we have won significant business from the Railways who have now commenced outsourcing certain facility services in railway stations.

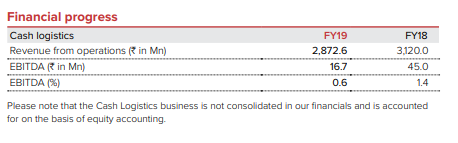

Cash Logistic

During FY19, the segment grew by 46.7% and recorded a five-year CAGR of 83%.

Risks:

• Our security services business is expected to see an increasing role of technology in the way we deliver our services and also run our operations. We have been making significant investments in offering security solutions through technology

• The revenue streams in the security or facility management industry are recurring in nature, which gives a high degree of predictability to the revenue and cash flows. However, with a widespread operational network covering close to 17,000 sites, we need to ensure that each of these sites operates to the same exacting quality standards across the length and breadth of the country.

• The Group’s operations expose it to market risk, credit risk and liquidity risk. The Group’s focus is to reduce volatility in financial statements while maintaining balance between providing predictability in the Group’s business plan along with reasonable participation in market movement

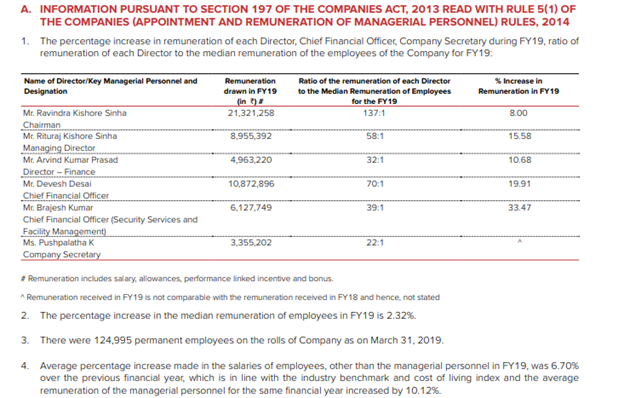

Management and Employee Salary Growth

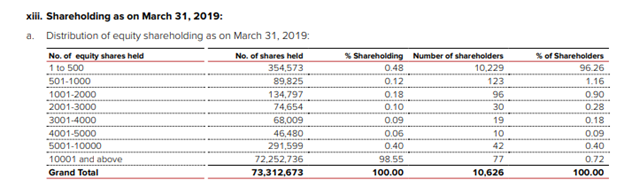

Shareholding

Consolidated Audited Financial Results

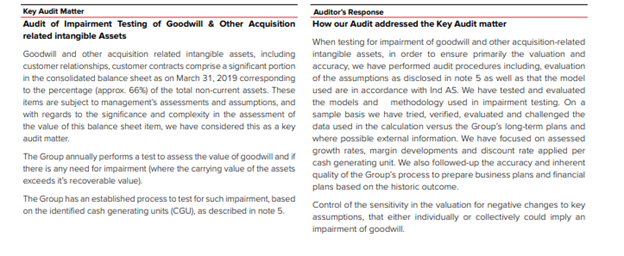

Goodwill and Intangibles

• We did not audit the financial statements/ financial information of 38 subsidiaries, whose financial statements/ financial information reflect total assets of 31,127.53 Mn as at March 31, 2019, total revenues of 46,168.04 Mn, total net profit after tax of 1,439.40 Mn and total comprehensive income of 1,423.42 Mn for the year ended on that date, as considered in the Consolidated Results included in the Statements. The Consolidated Results also include the Group’s share of net profit of ` (-)135.39 Mn for the year ended March 31, 2019, as considered in the consolidated Ind AS financial statements, in respect of 3 associates and 2 jointly controlled entities, whose financial statements have not been audited by us.

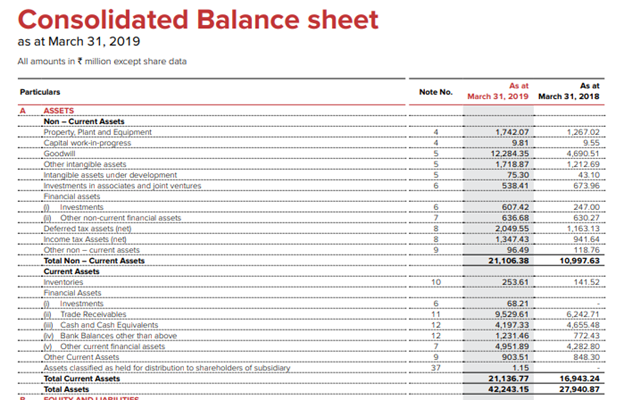

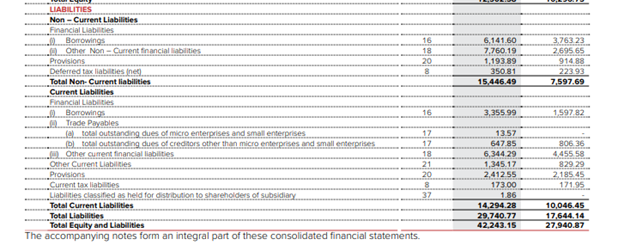

Balance Sheet

- Service sector-based acquisitions creating lot of goodwill creation on balance sheet

- Higher share of deferred tax asset

- Significant increase in debt

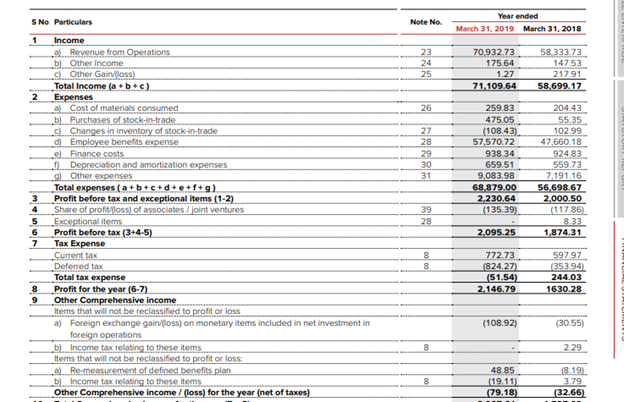

P&L

Current taxation has regulatory benefits but not sure how long it will last

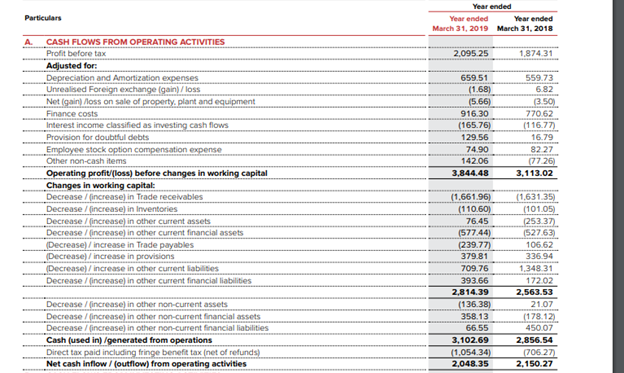

Cashflows

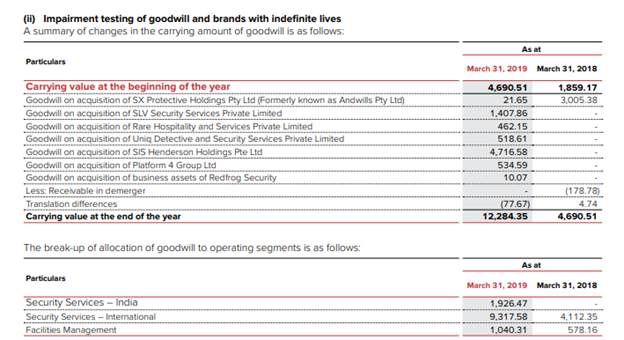

Goodwill

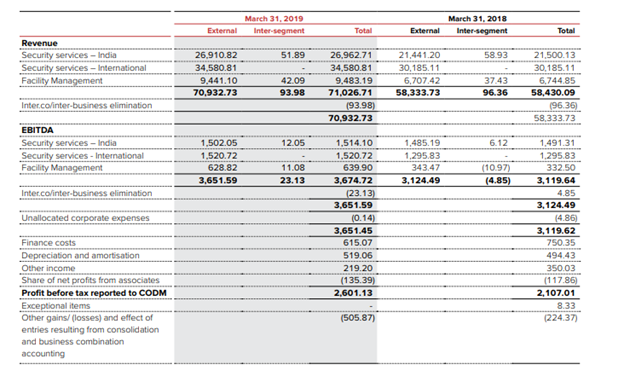

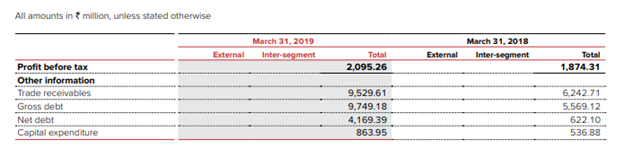

Segment wise Info

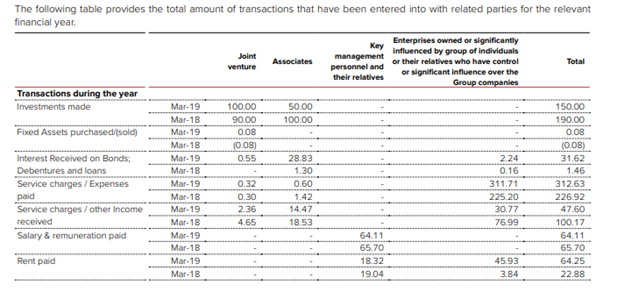

Related Party Transactions

Overall, slowly valuation concerns are getting addressed personally but the risk items highlighted above through various posts are still open , continues to be accumulate with execution at reasonable valuation story for me

Disc: Invested