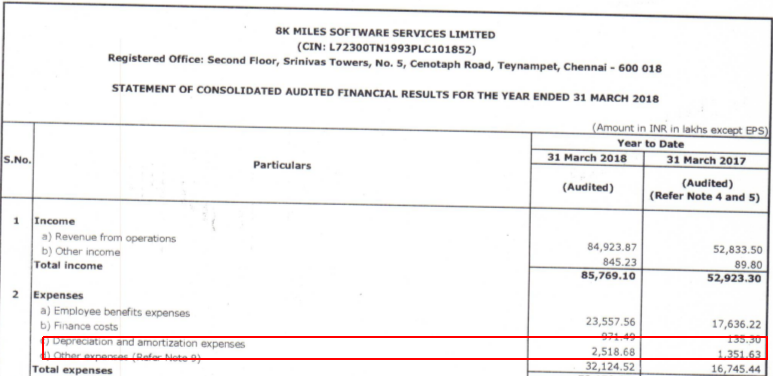

Total expenses for fy18 were 321cr which comes to 80cr/quarter. How have you estimated opex of 150cr. Total expenses for Fy18 are 592cr, which infact turns out to be 150cr / quarter.

Also receivable have increase does not mean company is not getting any money from customers.

has booked 104 days of receivables instead of 80+ days normal. On a like-to-like basis of receivables, de-growth looks substantial and can be calculated if one wants.

This is not a seasonal business for us to look Y-o-Y. If you forget for a moment that it’s 8k Miles, would you really say that below Q-o-Q sales growth profile is coming because of base effect ?

Reference was to Quarterly depreciation, You need to reverse calculate the quarterly P&L from the 2018 yearly P&L and last 3 quarters P&L.

You need to add Employee expenses as well.

It is not about whether company is getting “any money” from customers. It is about whether company is getting sufficient money timely from customers. For a fast growing company high receivables are justified because the receivables belong to the high sales done in the recent months. But growth slowing down + increasing receivables is the most dangerous combination.

There are all the signs that company has issues - slowing growth, moving to government business (both the newly inducted directors seem to be inducted to fetch government business if one looks at their profile) , increasing receivables, debt levels increasing continuously and no cash on the Balance Sheet.

If the auditors did not go deeper and check the subsidiary audited accounts and how they have been reconciled, then why have they taken more than a month to come out with consolidated financials after releasing the standalone financials. I mean if we are assuming that the auditors only ‘plainly’ took the numbers from management and reconciled and presented - without applying any intellect - then why did it take so long for them to consolidate these accounts.

Additionally, if auditors were uncomfortable, they could have resigned just like they have done in some other companies this year - which has not happened in 8k miles!

Further, I would commend the management to appoint a big four auditor and open its books to them after pretty sketchy set of reports in previous years. They could have easily continued the status quo with earlier auditors.

So, I am tending towards believing that there is no ‘cooking of books’ to the extent enabled by auditor oversight. There could be a deeper issue which is possible (with a relatively lower probability but which still exists) but has not been unearthed yet.

However, this does not mean there is no disappointment on the part of the results for Q4 as has been highlighted by fellow members. Some developments have seriously gone in opposite direction to my original investment thesis.

Finally, to stay invested, I am trying to answer the two questions?

‘What is the downside left from here?’

‘What is the potential upside if this fog on the authenticity of financials clears?’

The reason given by Management is they have to comply with IND-AS and they erred in terms of resource requirement for same.

The issues highlighted by @h_nazkani seems more real to me that blanket statement like “cooking of books”. The challenges to the business are real but all businesses have challenges. Investors have to weigh in for themselves risk/return in this particular case. For all the shortcoming highlighted look at the price at which this business is available.

I have some observations and unless these are adequately addressed, to me this is a clear avoid stock.

Cash + borrowings sucked into intangibles and receivables. What are these intangibles? what’s behind the internally generated goodwill. The company hasn’t made any acquisitions during FY18, so how much of incremental cash & borrowings is locked into intangibles?

Receivables ageing needs a close look whenever it is released, especially dues > 1 year.

Jump in loans and advances (assets). Who has the group lend money to? strange line item in an IT company Balance Sheet. Lent to promoter group while the company pays the interest? Does the loans & advances carry any interest?

12 months’ FY18 staff cost less than 9 months’ FY18 staff costs. Why?

Impressive P & L with negative free cash flows. Where is the money?

Higher other income on lower cash balance. How come?

@h_nazkani Thanks a ton for the reverse engineering of Q4 consolidated figures! As also the valid points flagged.

PAT grows slower also, but at 55% YoY and 20% QoQ, seems fast enough!

Receivables days does rise 20% above Median, but Receivables also grow 100%, seems reasonable. Govt business can be slow to get paid.

March quarters can throw up some strange figures, being end of FY.

That is true also when comparing figures of 2016 to 2015.

Obama publicly branded the entire Indian IT industry of body-shopping, makes no difference.

Maybe they depreciate fast.

Ok, so they borrow at real cheap (US) rates to pay for operating expenses. Mortgages where I stay are at historic low of 1% pa. American rates may be a bit higher though. It might be a sin not to leverage your growth with borrowed funds at such throwaway rates.

Discl: Invested since Oct 2017, average price of 340, 12% of PF. (60% done in past few weeks)

Most of the discussions here of late has focused on the Q4 numbers. Not much has been discussed on the impact of Ind-AS on the overall financials.

I’m still going through this EY report which has some interesting insights on revenue recognition, change in value of acquisition, estimation of fair value and host of other issues. It is a big document more suitable for someone with sound accounting knowledge. It would be great if someone with accounting background can shed light on current and future impact of the transition, from GAAP to Ind-AS, on financials.

During the recent interview with CNBC, they had announced that Q1 would be declared within couple of weeks of Q4 results. Is there any update on it. We should start hosing them with emails/calls to get that out at the earliest.

I have gone through multiple Linkedin profiles of employees of 8K Miles, read posts of many senior executives on Microsoft azure blog. I myself work in IT domain. I am an experienced Big data engineer. From their profile , it can be easily gauged that they are doing genuine work in Cloud, Bigdata. Many employees have also mentioned client names like Pfizer in their job roles. If you believe me , Cloud migration is very hot these days. Managing a dedicated IT infrastructure is very costly and organisations often require third party support for migration. Also they have Saas products which provide recurring revenue. I invested in this company without looking into price, balance sheet but i considered its products. It is very easy to blame management but running a business is another thing. Today i saw many people saying it a chor company just because share price has fallen. For doing expansion they have to spend a lot of money, they can easily get caught wrong footed. But thats how startups/small companies work. I may be wrong, but i think balance sheet alone is not sufficient to judge a company otherwise all accountants would have been millionaires.

Agreed, your post is very practical. You can’t take decision on just balance sheet, or financial, PE ratio etc. I myself work in Telecom domain and my company asking senior executive to learn cloud, block chain, and big data. Don’t find much issues here. Revenue breakup is very interesting, AMC revenue ahge been increasing fast which is good , this will.grow at 40-50 % for next 4-5 years.

I suggest people to go read BQ and MQ related threads/posts on VP and see where a business/management like 8k miles slots. It has become fashionable to add AI/ML/IoT/Blockchain etc. even if the companies do no real work on said fields. I am an IT consultant and I have worked with quite a few companies and have seen how the companies sell themselves with all the buzzwords but when it comes to closing a pre-sales deal, seek consultants to fill the gaps while proposing solutions, so I won’t go by buzzwords meant for people who have no clue what they are talking about.

Then I suggest going through AR of Subex and Tata Elxsi back to back and then go through 8k miles’ AR and see which of the two companies 8k miles comes close to. Slotting a business based on a spectrum of traits requires a handful of mental models and unless one learns vicariously by going through similar cases in the past, there is no way to develop these hunches and instincts. This vicarious learning is why I hang around so much in threads like Fiberweb, Manpasand, Vakrangee etc.

My belief that the company is cooking its books doesn’t come solely from the balance sheet but from my field experience in working with SMEs in migration of legacy systems to AWS/Azure, of customer acquisition costs in such businesses, mismatch between head count and topline growth, lack of IP and competition from other AWS/Azure migration partners, past price/action in this scrip (check this post from Sept. when technicals first got me interested here), Suresh Venkatachari’s interviews on CNBC, dispatches to exchanges and keen interest in stock price management etc.

I am no expert and please don’t go by my views. The brain can seek cognitive ease and take these conclusions at face value and these conclusions may stick if you don’t question them yourself so I leave it to you to research this with the valuable resources on VP on BQ/MQ.