It is based upon stand alone result. PE for consolidated is much lower.

Any insights - what were the issues raised and clarified during the AGM yesterday?.

Hi All,

Any idea on conference call details for Investor/Analyst call today. Please share

Source: http://www.bseindia.com/xml-data/corpfiling/AttachHis/2e6ae569-3c67-40a7-b6da-f7855a07abc3.pdf

This seems to be the analyst/investor group meeting happening in Sofitel Mumbai BKC. Not sure if someone from the ValuePickr community is attending the same.

Analyst meet seems to have lasted for 4.5 hours (from 4:00 pm - 8:30 pm) as per management disclosure. In case someone attended, please do share your experience.

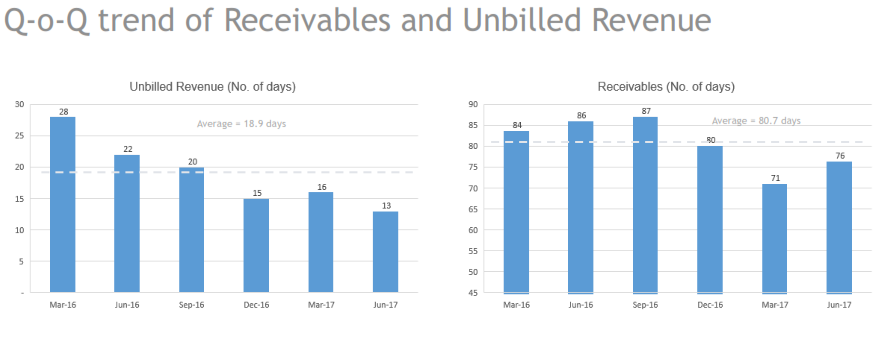

Also, management has shared a corporate presentation - last 10-15 slides are pretty interesting and revolve around business model, recurring revenue stream, receivables, cash flows etc.

Presentation link:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/f340f2d0-6603-441a-b23a-d1d4d479ea64.pdf

1 Like

8K Miles conducted an Analyst/Investors Meet today. Following are a few key takeaways:

-

Public Cloud Computing industry size stands at $246 Bn as of FY17

-

8K Miles specializes in Cloud Migration, Cloud Security and Transformation with a revenue CAGR of over 100% over the last 5 years.

-

The company has consistently invested in developing platforms for its cloud services and its flagship platforms are CloudEZ for orchestration, Automaton it’s AI platform, MISP for Identity Services and ezRWE.

-

The company primarily deals in Cloud Services for the Pharmaceutical and Healthcare industry (49% of FY17 revenues) followed by Manufacturing (27% of revenues).

-

8K Miles supports Cloud Transformation and partners with major cloud enablers such as AWS, Microsoft Azure, Google, etc.

-

Huge opportunity exists in the shift from Private cloud to Public/Hybrid Cloud structure as Enterprises can save upto 40-60% of their expenditure in the process. 8K Miles primary promotes this transformation.

-

Basically, Media and E-commerce industries were early adopters of cloud whereas Healthcare, Financial Services and Government agencies have been laggards in Cloud due to heavy regulations and security issues. However, these industries are gradually but steadily adopting Cloud Transformations as US government has definitely laid out policies in CY16-17. 8K Miles is primarily targeting these industries and is dealing with atleast 3 out 5 top Healthcare institutions in the US.

-

AWS, Microsoft, Oracle and Google basically offer discrete and individual Softwares on a SaaS model. 8K Miles Management is confident of its ability to bundle these individual Softwares (on SaaS model) and offer them as a package, which is where their USP lies. Management is also confident of solutions in the Pharma space such as GxP validations which are currently done physically however can be replaced by being conducted on Cloud Platforms. 8K Miles is one of the first few companies driving such solutions in the market. Additionally, the company has impeccable capability in providing security solutions within the Cloud environment. Solutions such as Electronic Medical Records (EMR) hold immense growth potential.

-

Management also showcased it’s Automaton platform which uses bot technology to identify risks and errors and remedy it within a span of few minutes versus the traditional methods which are still used by certain IT vendors. We believe that such platforms give the company an immense edge over traditional players.

-

Business model is largely de-linear and platform centric and hence margins are rich with 33% average EBITDA margins over the last 3-4 years.

-

The company’s revenue mix consists of Cloud Transformation (39% of FY17 revenues) , Managed Services (26%) , Security Solutions (12%) and Consulting Services (22%). Managed Services and Security Solutions are largely repetitive revenues.

-

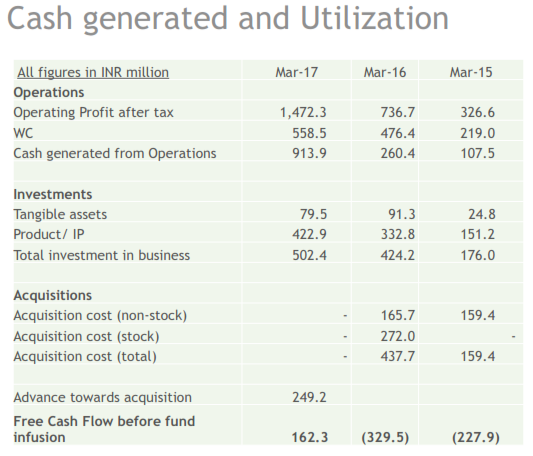

The company’s FCF stood at INR 162 MN in FY17 and was the first year in which the yield was positive post investments in platforms and IPs. The company does not pay dividends as it is focused on growth and believes in consistent investment in IPs to hold an edge in such a dynamic environment.

5 Likes

Infrastructure-as-a-service registered a 2015-16 growth of 31% with AWS on top.

The mgt comment on Dividends is inconsistent and fishy…they had initially declared Rs 7 dividend (last month), then they abruptly revised it to Re 1 within a few days…the explanation they gave then was that Rs 7 was based on consol profits, but as per professional advice they can only pay from standalone profits and were hence forced to reduce to Re 1. And that they intend to transfer profits from their subsidiary to the parent within this fiscal to allow them to make up for this mistake and will then pay the balance Rs 6 as interim dividend. Now in this investor meet, they’ve come up with a completely different position of not paying dividends to focus on growth. The issue is not about whether or not they pay, but the constant changes and discrepancies in their statements and past accounting makes them v. suspect.

Disclosure: I found the co. and valuation too good to be true but despite that I bought shares a month ago; but there has been a niggling discomfort all through. And then post-facto I read this blog and the Ambit forensic report on their accounting issues as well as the recent news on SEBI investigation into past price manipulation. Hence, used this price rise (post investor meet) to exit the co.

1 Like

@achalarora:

Hi Achal, do you recall management clarifying further on below items during the meet:

-

Dividend reduction and rationale (probably post Deloitte got on boarded, they got the professional advice from them, just guessing)

-

R.S. Ramani (CFO )selling huge quantity - was that to some institutional holder (IIFL etc.) or open market sale ?

-

Promoter’s (Suresh Venkatachari’s) compensation related disclosures missing in annual report.

Other major issues mentioned in the Ambit’s forensic report (last year) or this thread seems to have been broadly taken care of, either in annual report or the presentation shared this week on BSE website.

Business of Ambit is to create fear and make money. I don’t trust anything they say. They only can see doomsday in whatever they analyze. I have never in my life seen a balanced report from them.

1 Like

You do not need to believe them but validate their thesis. On the contrary , I don’t rely on Ambit numbers based verdict but like the quality of analysis though have my in disagreements on qualitative and quantitative conclusions

1 Like

I have seen a number of such software companies over the years. I am not saying anything wrong about 8k mikes as I know nothing about this. But I have seen companies like HOV where the standalone entity kept making losses and consol entity kept making huge profit to ridiculous PE of 2 or 3. But one thing is for sure, investor never seen even a single penny of this profit either through dividend or share price appreciation. How is this company any different?

I can name a number of others like Aftek, Helios, Megasoft etc which were supposedly the latest niche areas which went nowhere. Even heavily backed and recognized among the best payroll tech Ramco hadn’t gone anywhere over the last 10 years. Add NIIT tech to it. Only company I saw succeed was Vakrangee which wasn’t obvious like MindTree. My bet is MindTree and LandT infotech will succeed due to its management quality as compared to a hundred other so called niche software firms.

4 Likes

Suresh Venkatachari on CNBC:

1 Like

Hello dear friends. I am currently working as Finance controller for the IT expenses of an MNC. Given my background, I have some understanding of what this companies does and its potential. I have considered this company as good value stock with immense growth potential, thus had a small amount invested for tracking purpose. I have also been tracking discussions on this thread and doing my personal analysis. While I was bullish on this stock I could not help reviewing the negatives presented about it, particularly the Ambit capital report. I do not take free reports at face value, hence did my own research.

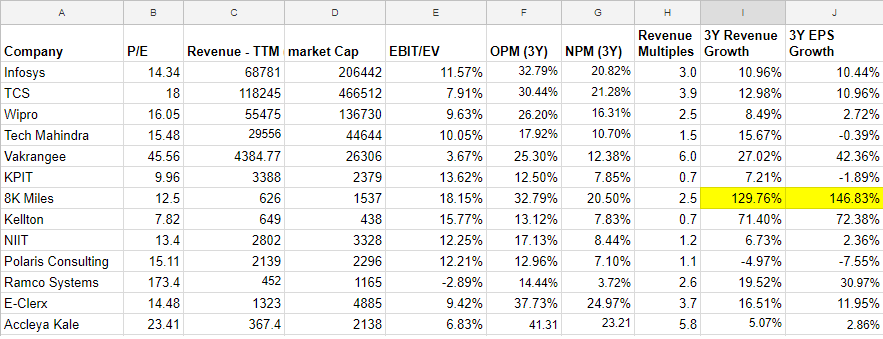

I took the financials of 3yrs from all spectrum of IT compaines (sample) considered the following parameters,

- Operating cash flow as % of Operating profit (adjusted for Tax) - To know how much the company really earns in cash and the impact of WC changes

- Receivables / Revenue - To know how much of the declared revenue per year does not convert to cash

- Receivables growth - How has the receivables grown

- Revenue growth - How has the Revenue grown

For 1& 2 I have used 3 yr average and for 3&4 I have used 3yr CAGR in below table,

8k Miles has the lowest figures in most ratio except revenue growth, where they are the best - which rings a warning bell to me. I know this is not a very comprehensive check, nor am I comparing companies with the same revenue model/product mix. Thus please do not use this for your investment decision.

I am going to check this stock with one of my colleague who is a CA and has done a course on forensic accounting to cross check my analysis. Please feel free to share your views.

Disclamer: I have exited from the stock and currently tracking it for academic purpose - as I was not comfortable with its financials. My analysis above does not closely match Ambit report - my data source is Screener also I am not sure what Ambit incl/excl in their analysis.

4 Likes

The most worrying aspect from your table is that receivables are growing at a much faster rate than the revenue growth.

5 Likes

Operating cash to operating profit is not the right ratio to evaluate a

holding co with a few subsidiaries. Because their operating cash has gone

as investment cash flow into subsidiaries…And into funding acquisitions.

Receivable days is a red flag. But the same was true for Infosys too for

the first 5 - 7 years till they established a credibility and had better

bargaining power with customers. Infact Infosys did not have money to even

pay salaries several times in the early years. Just my view.

So now the co had engaged a big 4 to audit their accounts…If they are

hiding something why would they do this.

Disc: Invested. Views are biased…

2 Likes

Would tend to agree with @rvetri as they do generate significant CFO and a lot of that gets ploughed back to develop their platform/IP/product and acquisitions. This, I believe, is required for a high growth company.

Also, they seem to be showing consistent improvement on their receivables side so not sure if 3 year averages are the right metrics to choose. This improvement seems to indicate that company is grabbing incremental business/new clients on better credit terms and probably has some bargaining power.

Disc: Invested. Views might be biased.

I tried to put the performance of a few IT companies listed in India and tried to compare 8K Miles

Source for numbers: valueresearchonline

The points that look attractive are

- Cloud migration is a very attractive segment and lot of companies are now moving to cloud cutting down their maintenance costs. 8K Miles is attractively positioned with its niche presence.

- For a company which is growing 100% YoY, the P/E is quite low.

- Operating/Net Margins are on par with Industry best

- Stock lost 32% in the last one year. Before the AGM it was even available at 379ish range (-52% since last year). Stock has appreciated 100% in the last 3 Years.

I believe the stock has much upside.

Cons:

- Acquisition based growth. They are doing targeted acquisitions to get headway into health/fin sectors. Integration can be a challenge.

- Past irregularities of the promoters.

As Mohnish Pabrai notes that one can fall in love with the stock while doing research and have prejudice. Request the experts in the forum to balance the view.

I am new to the forum. Feel free to post suggestions so that I can post better analysis.

Disc: Invested - Tracking Position

Can you please elaborate on above?

Thanks

Hi Gaurav,

They are already referenced in the historical posts above.