Industry Overview

Indian Offshore Oilfield Industry

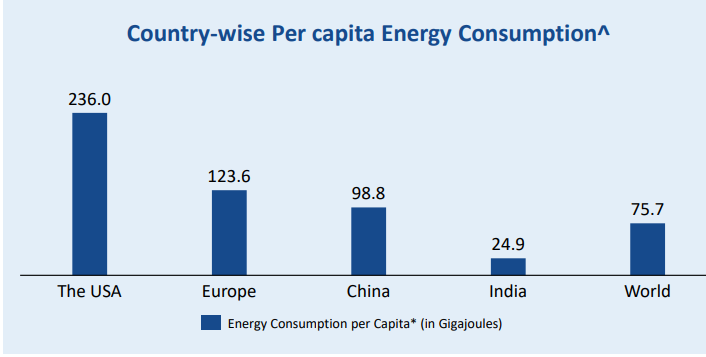

- India: 3rd largest oil consumer globally after the United States and China with ~36% of the country’s energy demand met by Oil & Gas

- Despite being 3rd largest globally, India’s per capita energy consumption stands significantly lower than the USA, China and global average, underscoring huge growth potential in energy consumption moving forward

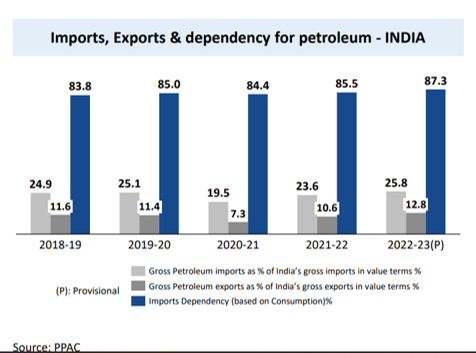

• India currently imports about 85% of oil and about 50% gas that it consumes.

Growth Drivers for Indian Oil and Gas Industry

-

Growing demand

• Oil demand in India is projected to register a 2x growth by 2045.

• Diesel demand in India is expected to double to 163 MT by 2029-30 -

Policy support and Govt initiatives (focus on reducing dependence on oil imports)

• In Union Budget 2022-23, the customs duty on certain critical chemicals such as methanol, acetic acid and heavy feed stocks for petroleum refining were reduced.

• As per the recent report of the Petroleum Ministry, India currently imports about 87% of the oil demand. Govt has announced capital commitment of Rs. 1.2 lakh crore by state and oil PSUs in oil and gas exploration, refineries; to reduce dependence on oil imports and meet the needs of our nation -

Increasing investment

• India aims to commercialize 50% of its SPR (strategic petroleum reserves) to raise funds and build additional storage tanks to offset high oil prices.

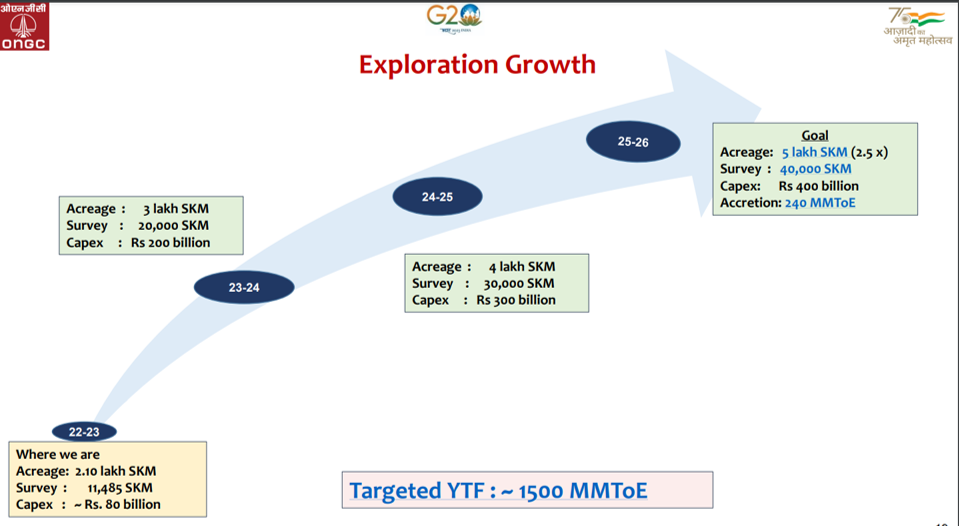

• ONGC has announced plans to invest USD 4 billion from FY 2022 to 2025 to increase its exploration efforts in India.

Strong Outlook & commentary from ONGC

- Strong outlook in terms of wells drilled and the planned capex

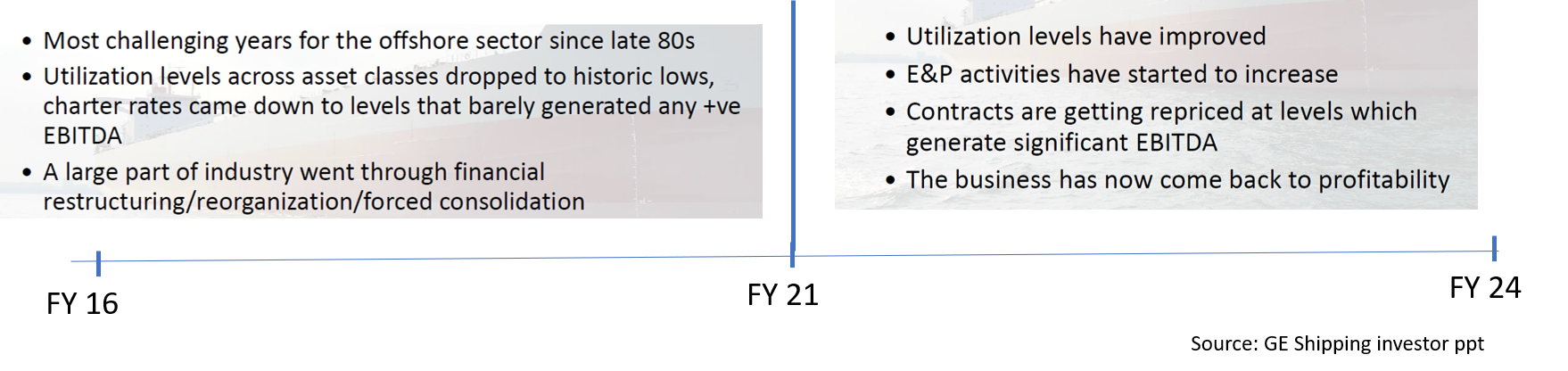

Business Cycle – offshore sector

FY 16 to FY 21 : Industry went through a down cycle, characterized by low utilization levels, low charter rates and resultantly lot of companies went through financial restructuring / consolidation, etc

Post FY 21: E & P activities are increasing, contracts are getting repriced; and business getting back to profitability

Company Background

Seamec was originally incorporated as Peerless Leasing Private Limited in 1986. In 2001, it became part of the TECHNIP Group and was rechristened as Seamec.

In 2014, HAL Offshore acquired Seamec from Technip Group. HAL currently holds around 70% of company’s share. HAL Offshore has an experience of around 25 years and is a leading end-to-end solution provider of underwater services and EPC services to the Indian oil and gas industry.

Seamec operates in two distinct verticals, offshore subsea support vessels and bulk carrier charter business.

Offshore subsea support

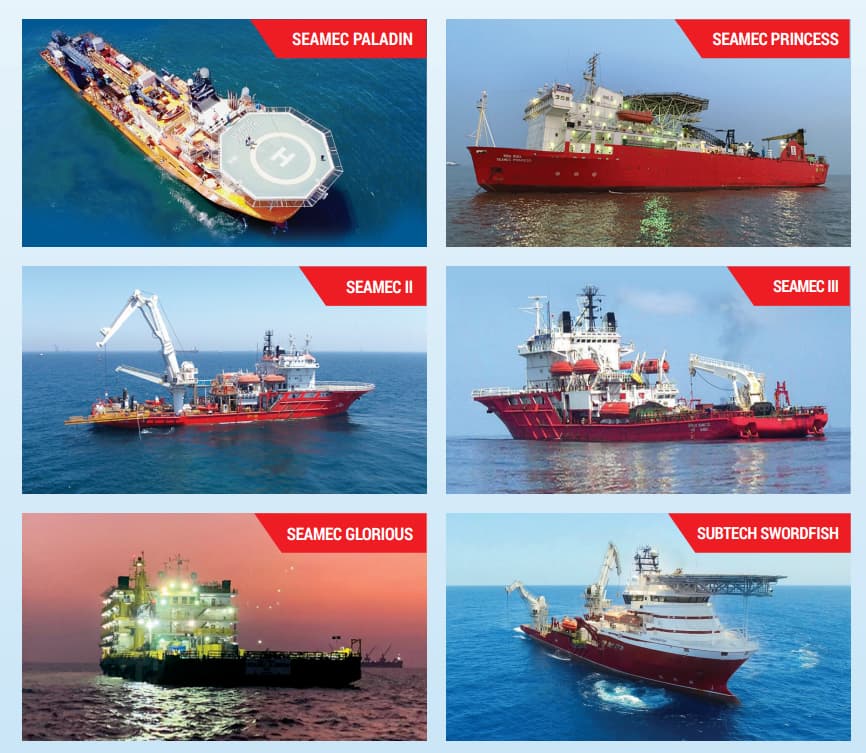

Its the leading provider of offshore oil feed services in the subsea segment. The company has five diving support vessels, one Offshore Support Vessel and one barge in the offshore subsea support business, wherein the vessels are deployed in the domestic as well as international market.

Diving support vessels

- Seamec Paladin

- Seamec Princess

- Seamec II

- Seamec III

- Seamec Swordfish

Offshore Support Vessel – Sea Diamond

Accommodation Barge – Seamec Glorious

Among these, Swordfish was acquired in 2023.

Bulk Carrier charter business

Two bulk carriers provide marine transportation services of dry bulk materials such as food staple, commodities, and industrial products

Some of the marquee clients in Bulk Carrier Services, include United Marine, Clipper , Eagle, etc

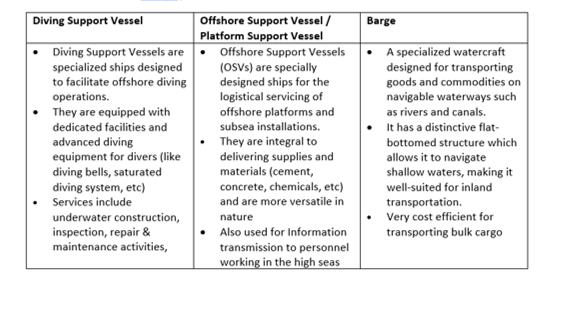

What is DSV, OSV and Barge ?

More info here - https://www.youtube.com/watch?v=AiJczimBL58

Business Overview

- Company has the biggest fleet of DSV in Middle East and India region

- Vessels are equipped with specialized equipment from where the diver goes under water upto 80 meters (Bombay Heights) or even maybe 130 to 200 meters depending on the location

- Divers go underwater and carry out the maintenance of the assets which have been installed by ENP player. Main function of these vessels is to maintain asset integrity and see to it that the assets are compliant with environment regulations, etc

- Based on number of days the vessels are deployed and the revenue rates per day, they do billing to the customer, on monthly basis.

- Out of the 6 vessels, 3 are already on a long-term charter contracts. The balance 3 are also on a spot contract for 2-year basis. This lends stability and resilience to the business.

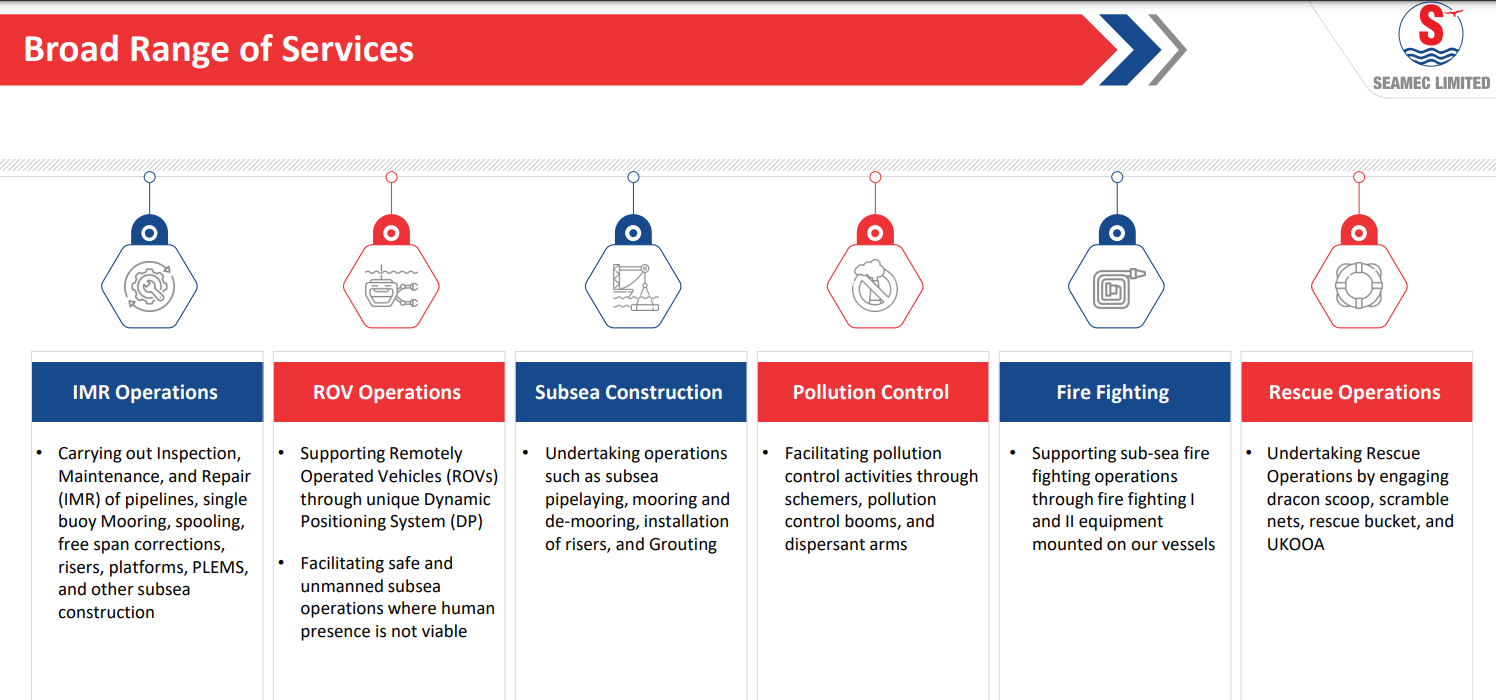

- Company has extensive experience in providing specialized services, including inspection, maintenance and repairs, remotely operated vehicles and subsea construction activities. These operations require specialized vessels and well-trained crew, with a diving team experienced in handling complex activities to ensure seamless operations for E&P companies such as ONGC, Aramco and ADNOC. ~ Entry barriers

- SEAMEC is an ISO 45001:2018, ISO 9001:2015 and ISO 14001:2015 certified Company, which conforms to Quality, Health, Safety, Environmental (QHSE) standards and occupational health along with Shore Based Management system.

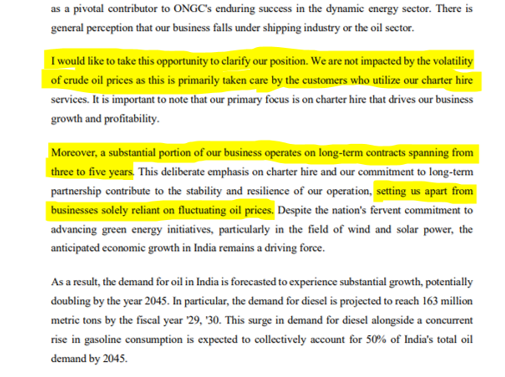

- Company has stated during calls, that they are not impacted by the volatility of crude oil prices as its primarily taken care by customers like ONGC who are utilizing charter hire services. But this is a monitorable.

Range of Services offered –

Overview of Vessels

| Name of vessel | Type | Built year | Procurement year | Tonnage |

|---|---|---|---|---|

| Seamec II | DSV | 1982 | 1993 | 4500 |

| Seamec III | DSV | 1983 | 1993 | 4300 |

| Seamec Princess | DSV | 1984 | 2006 | 11,100 |

| Seamec Paladin | DSV | 2008 | 2021 | 5600 |

| Seamec Swordfish | DSV | 2007 | 2023 | 5400 |

| Seamec Diamond | OSV | 2011 | 2023 | 1922 |

| Seamec Glorious | Barge | 2006 | 2021 | 9850 |

Three of the vessels are a little older. So they are looking to replace these vessels, over next 2-3 years.

Further, they have recently acquired Seamec Pearl and NPP Nusantara (covered in detail, later); in addition to Seamec Diamond (in 2023).

Revenue split

Currently 85% revenue from offshore assets and 15% from dry bulk… Targeting to increase it to 90% from offshore assets since the offshore support services are niche services, there is a higher EBITDA margin compared to dry bulk

Business linkage to ONGC

- Preferred partner to ONGC (the largest player) in maintaining their oil fields

- ONGC plans to invest, almost $4 billion in the medium term. Business is linked with that. And even if there is a slowdown in further investment by ONGC, company will keep doing maintenance work for ONGC

Comfortable operating performance

- Long-term contracts spanning 3-5 years, executed to charter the MSVs, offer medium-term revenue visibility.

- A healthy gross margin of 50-60% is earned on the MSV fleet.

- While the company has secured long-term contracts for its MSV fleet and diving support vessel (DSV); barge and bulk carriers are on short-term/spot basis

Capex plans

- Capex plan of 200 to 300 cr for FY 26. And around 300 to 350 cr for FY 27. This is likely to be incurred for replacement of the ageing current vessels.

- Major part of capex will be funded by internal accruals

Seasonality impact

- During monsoon, 3 of the vessels are not deployed; dry docking is caried out during that period. Q1 and Q2 are a little muted (Q2 weakest).

- Q4 and Q3 are the best quarters, particularly Q4

Not impacted much by Red Sea Crisis

All vessels are operating on Indian coast only and one vessel is operating in Saudi Arabia (other side of Red Sea) , so minimal impact

Tonnage tax company- Negligible tax

Company enjoys an incentive by Government under Indian Income Tax Act where companies are taxed on the basis of the tonnage. Its a very low tax rate. Tax provisions are very less.

Recent updates on new fleet

- Sea Diamond

- Takeover completed on 2nd January 2024.

- Expected to be deployed with ONGC from Q1 FY25 for a period of 3 years at USD 8,750/- per day

- Revenue contribution from Q2 FY 25

- Seamec Pearl

- Entered into agreement to purchase this OSV for USD 7 million.

- Delivery of the vessel is expected to completed on or before 22nd June 2024

- Expected to be deployed with ONGC from Q2 FY25 for a period of 3 years at USD 8,750/- per day

- NPP Nusantara

- Seamec International FZE has entered into an MOA for purchase of OSV - NPP Nusantara

- Delivery is expected to be around mid-September 2025

These have been finalized within a span of last 2-3 months; an indicator that the company sees strong revenue visibility and might well be at an inflection point in terms of growth trajectory.

Financials

- 3 year Sales CAGR 41%

- Last FY Sales growth 67%

- ROCE : 17%

- Debt / equity : 0.36

- No equity dilution in recent times

- Promoter holding: 72%

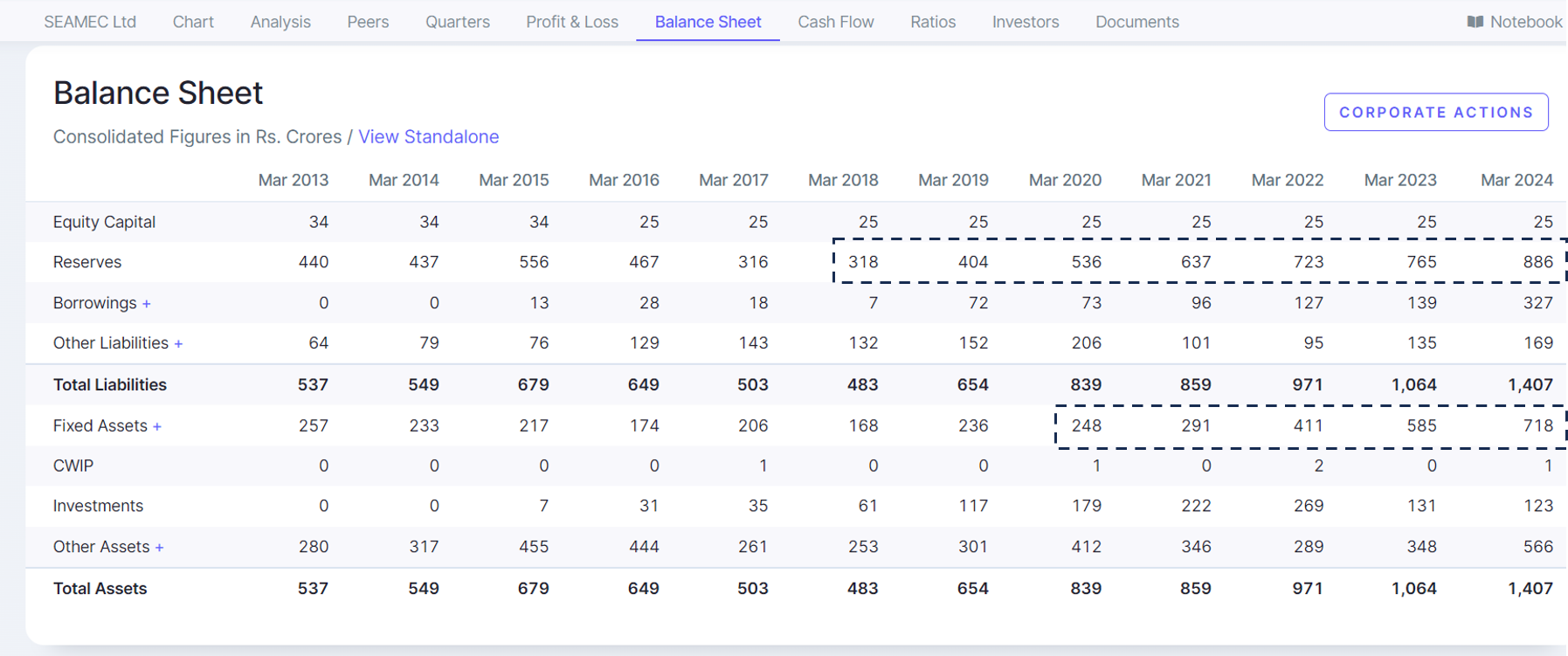

Balance sheet

- Healthy cash reserves- has almost tripled in last 6 years

- Negligible debt on balance sheet during the downcycle (till FY 21).

- Fixed assets have grown more than 2x in last 3 years

Outlook & Guidance

• Company expects new contracts to be signed and executed over the next 2 to 5 years.

• Also repricing of contracts too is expected as charter rates are firming up.

• Revenue growth guidance of 15-20% for next FY and about 15% CAGR over next 3 years

• Looking to sustain EBITDA margin of around 35 to 40% as company will look to maintain higher number of deployment days of its fleet.

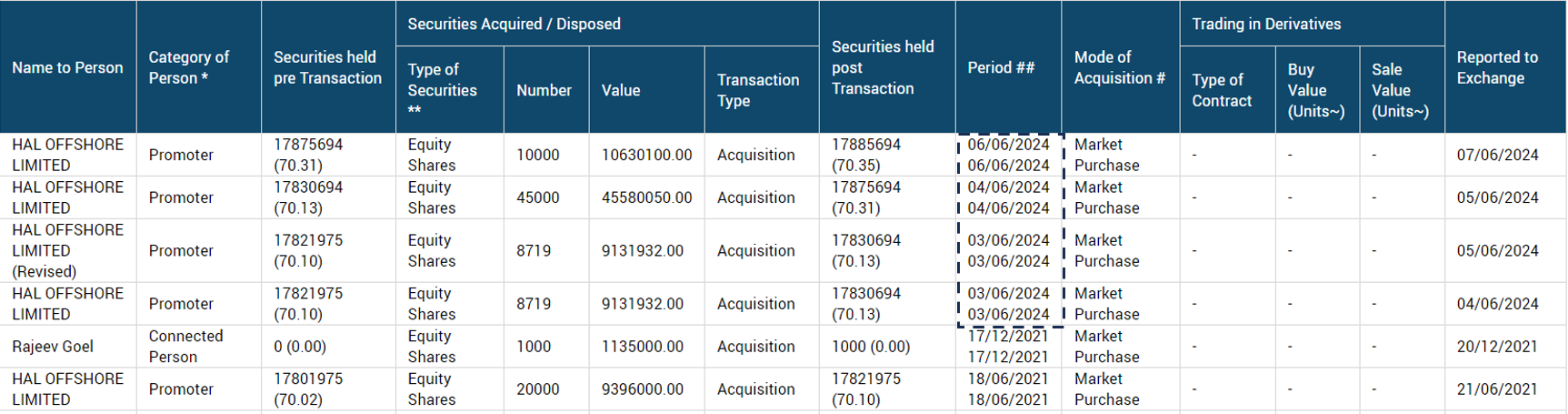

Promoter Buying

Promoter has been buying from open market recently

Valuations

- GE shipping can be considered as a peer. Though Seamec operates in a more niche area of diving support vessels whereas GE Shipping mainly provides supply vessels and platform support vessels.

- For Seamec, offshore business contributes the majority (almost around 75% to 80%) of the revenue mix, which is not the case in case with GE.

| Name | Sales growth 3Yrs % | Sales growth % | P/E | M. Cap / Sales |

|---|---|---|---|---|

| SEAMEC Ltd | 41.61 | 66.79 | 21.64 | 3.55 |

| GE Shipping Co | 16.35 | -7.65 | 5.75 | 2.86 |

On FY 25 estimated earnings, it trades at about 15 to 16 PE multiple. Considering the better operational performance based on deployment of new vessels and revenue visibility over next 2-3 years, it seems to be trading at a reasonable multiple currently

Likely Risks

-

Susceptibility of operating performance to redeployment risk, due to some ageing vessels

- Amongst the vessels owned, three vessels are more than 40 years old. This increases the redeployment risk of these vessels as they may not meet the bidding criteria of E&P players such as ONGC.

- They have replaced one of its vessels with a younger fleet, with the balance expected to be replaced over the next 2-3 years. Timely replacement is a key monitorable.

-

Cyclical and Asset heavy industry -

-

Susceptibility of charter rates due to inherent volatility in crude oil prices

- Offshore and deep-water block investments, are sensitive to crude oil prices. In the past, the slowdown in global oil and gas E&P capex has led to a decline in demand for offshore equipment.

- Though the company has mentioned in the last call that charter rates are holding firm and they foresee the pricing trend to continue in the future years

Disc: Invested

Reference Links:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dceece21-e8b3-453e-aa37-4d263d19b05e.pdf

ONGC ppt