Sealmatic India Limited (Further referred as “Sealmatic”)., is pleased to announce that it has secured a prestigious order for the critical parts of Stern Gland Seal for the Kalvari Class Submarine (Project P-75) from Mazagon Dock Shipbuilders Ltd.

45efcd7b-2767-4806-b961-b9ed0df888ce.pdf (772.6 KB)

It is the first order they have received in defence. Looks like they can secure good orders even from this sector.

3 Likes

Sealmatic has come out with excellent results. Topline, net profit has gone up by more than 50%. Though cash flow is still negative, it is negligible as compared to operating profit figures.

Sealmatic-25.pdf (2.1 MB)

In FY 2024-25 they earned eps of Rs. 17.5. If growth momentum is maintained, we can expect an eps of Rs. 25 in the current financial year. They have already started getting some orders from defence sectors. Things look good.

7 Likes

It seems Sealmatic is going to establish a third unit, which is expected to add approximately 25,000 square feet of working space by the end of the year. At present Sealmatic has 60,000 square feet of working space spread into two units, one in Mira Road and other in Kaman.

source: https://www.youtube.com/watch?v=OMLnxQ3raSQ&t=4s

5 Likes

Sealmatic is likely to issue bonus shares. Board meeting is scheduled on 03.10.2025.

16ec0ef2-2ff5-41f6-b485-afe9797daf05.pdf (290.1 KB)

what is the need for issuance of bonus shares. The price is 460 odd as I write this and MCap is just 420 crs, seems an attempt to prop up share price

6 Likes

Sealmatic India ltd.

Why no one is talking about CFO/PAT which is essential and negative.

It have NP of 53 crore for last 4 years combined and operating cash flow of minus 4 crore for last 4 years combined.

Means no bargain power in business, inventory piled up.

Can any one explain about it.

Disc - not invested

2 Likes

Company is just emphasizing “we’re growing”, new seals are getting sold below cost to acquire customers, high exhibition costs to improve visibility.

The main concern to worry IMO is company is constantly pushing back the target year for replacement and refurbishment business. In 1st concall it was FY26 (if i can recollect well) and the latest concall it was FY28.

Good part is Sealmatic is the only Indian mechanical seals company approved by NPCIL.

Let’s see how the future unfolds.

Disc - Booked losses on the day of latest concall, in the watchlist now

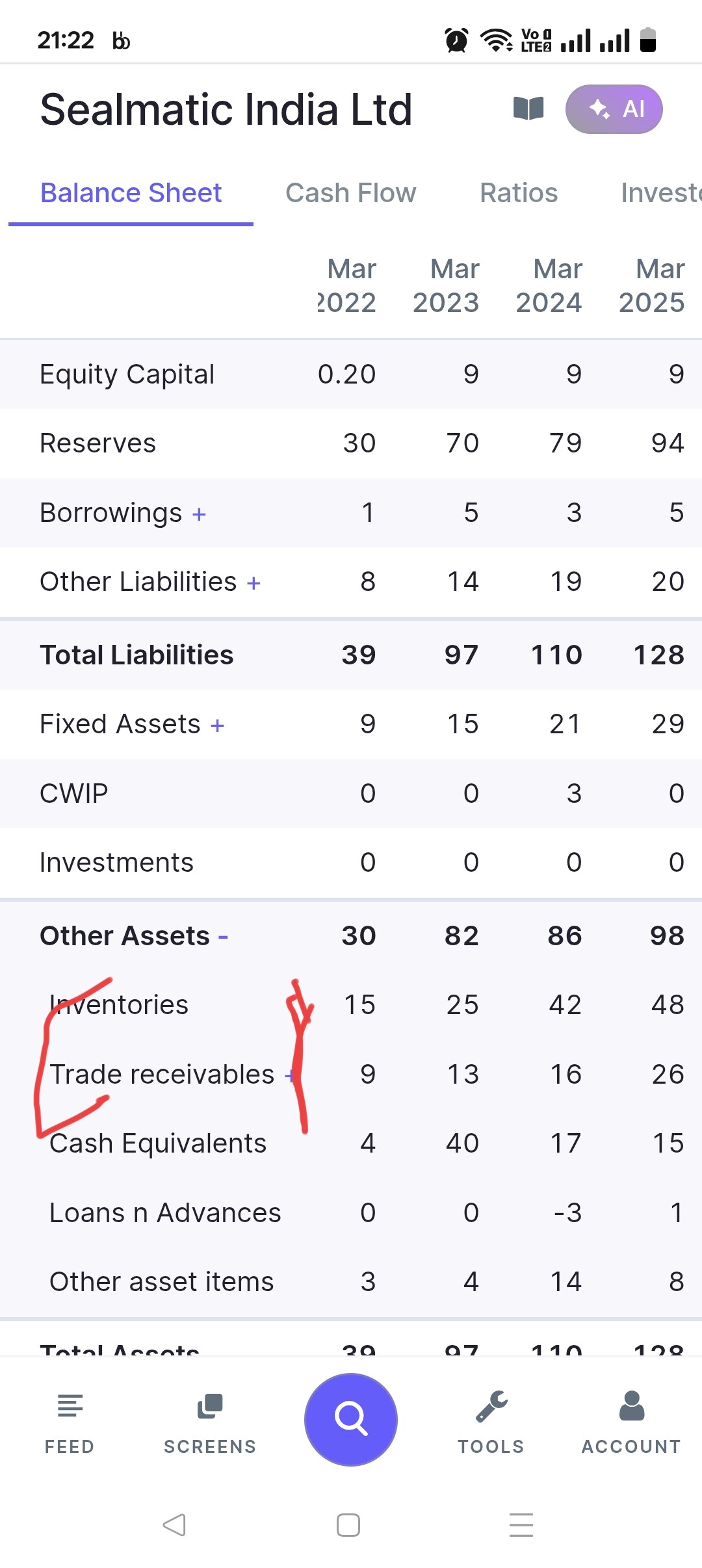

If we look at the last 4 years PNL, we see that topline has gone up by 2.5 times, from 42 crores to 101 crores.

When we look at the inventory and trade receivables, it has gone up by 3 times, almost equal to 2.5 times topline growth.

Looking at the cash flow figures, there is an loss from operating expenses of Rs. 4 crores. Through this operating loss, the company has grown by 2.5 times, have acquired numerous prestigious certifications, started project business, started a second manufacturing plant (with third in pipeline), started defence supplies, participated in many exhibitions… Not a bad performance for a 4 crores operating loss. It also shows a decent cash flow management in a growing phase in an highly capital intensive business.

Economy has seen recessionary pressure in last 1-2 years. Due to elections and disturbance in geopolitical situations, many big investment decisions have been postponed. I feel that the company has done well in this situations.

The company is likely to be cash flow negative for a foreseeable future, as long as it is growing at this pace. With 23 percent operating margin, one can grow at the rate of 15-20 percent without much capital infusion, it is not possible to grow @ 50% without capital infusion. Looks like the company is preferring to grow at high pace. It further shows that the company has scope to invest surplus at high ROCE.

I see these things as positive.

(Disclosure: Invested and biased)

3 Likes

While all you said, is true to the business but the company has not been able to deliver te things they were confident about in their first and second concall. A mechanical seal has an average life of 1.5 years to which company themselves said seals sold in FY2024 should come up for replacement in FY2026 and now FY2028 is the target year for revenue from replacement.

While the planning, certifications and approvals all seems good but execution looks like an issue.

I’m positive on the company in the longer term.

1 Like

My simple observations are, the company’s P&L looks good…sales growth, good margins (though margins have been falling and H1’26 have come at 17%), profit growth. However, the profits are not getting converted to cash, as pointed earlier by other members. So was wondering how the company if funding its operations because there is no major debt, especially short term debt. I noticed that the cash which was 40cr in 2023, has steadily come down to 10cr as per Sep’25 balance sheet. I suspect soon the company will have to resort to borrowing in absence of sustained cash flows. If the replacement cycle starts from FY’27 (starting April '26, honestly there is a lot of confusion in the management’s explanations) and cash also starts flowing in then they should be good, otherwise if they run into the receivables issue for replacement then the borrowing need will become more pressing.

Overall, the company looks good (based on the various certifications they have obtained), but lack of cash flows doesnt inspire much confidence. Also, sometimes the way the management replies to queries, feel it could be done in a better way. Net net, I am observing and am skeptical, and not invested.

4 Likes

The company needs one more round of funding. Last year the planned to issue 3.93 lakh shares @637 to one of a marquee investor, Aegis Investment Fund. However, the deal could not be finalized probably due to market fall. These things happen.

I think that the company can dilute 4-5 percent equity for around 25 crores investment, which may be sufficient to take the topline to around 200 crores in next 2-3 years. Once they reach a topline of 200 crores, internal accruals shall be sufficient to propel growth at a moderate pace.

But yes, they will need some capital in near future.

1 Like

In the recent concall, Mr. Umar kept on repeating April 2027 and FY27 until a participant put up a query that April 2027 means FY28 to which Umar said “Yeah you’re right”.

Now what to make out of this, is upto an individual.

The very moment I squared off the position but the business stays in the list

1 Like

Rently promoters brought some shares of the company. Small amounts. Not very significant. Promoters holding being 72.5%. For the last two odd years, the company is in correcttion phase. Let us examine the order book of the company and business going forward.

In H1-FY2026 the company has declared a topline of 54 crores with net profit of 6 crores. If the company can maintain similar growth rate going forward in H2-2026, the company is likely to end the current financial year at 120 crores topline with 14 crores net profit. Based on this estimate, the company is trading at 390 crores Mcap, a p/e of 28. Not cheap for a company showing growth of 22-23 percent.

Profits are not growing as fast as sales due to high spending on exhibitions & marketing. The company is currently “spending to grow.” They purposely sacrificed 3% margins in FY26 to fund aggressive participation in global exhibitions (Abu Dhabi, Russia, USA).

They are currently executing orders for ~70–80 new API seals to be delivered in the next 6 months. 490 API Seals have been supplied in the last 2.5 years (including to giants like ADNOC). Management estimates this “replacement demand” alone will generate ₹15–25 Crore annually starting FY27. This revenue comes at very high margins (no marketing cost). The high-profit service revenue from the ADNOC contract will only start reflecting in the books from April 2027 (FY28), though some initial service income may trickle in during FY27.

They Successfully executed an order for 175 API Mechanical Seals for ADNOC (Abu Dhabi National Oil Company). These seals are currently being installed via pump OEMs. This is a “Reference Order.” Once these seals are commissioned (expected late 2026), Sealmatic becomes a verified supplier for ADNOC’s massive replacement market. Their new Joint Venture (SealTech) in Abu Dhabi goes fully operational this month. This facility allows them to bid for Maintenance & Repair Contracts (MARC) directly from oil refineries in UAE, Kuwait, and Qatar. This moves them from “one-time sales” to “recurring service income.”

They Delivered critical B750 Type Seals (for Demineralized Water Service) to Nuclear Power Corporation of India Ltd (NPCIL) for the Tarapur plant. Nuclear orders have the highest “Entry Barrier.” Winning this proves their technical capability is on par with global players like John Crane or Eagle Burgmann.

Secured orders for “Supercritical Power Plants” (660 MW) including the DVC Raghunathpur project. These were won against stiff competition for critical Boiler Feed Pumps.

The Indian government is building 14 new Nuclear Reactors (700 MW each). Sealmatic is targeting a 15% market share of this expansion. Management estimates this will require 1,400 new critical seals. Since they are already an approved vendor for NPCIL (as per the recent Tarapur win), they are front-runners for these tenders.

They are seeing inquiries for specialized seals for Green Hydrogen projects (high pressure, high safety) where margins are significantly higher than water pumps.

the marine defense sector has recently transformed from a “potential scope” into a “proven revenue stream” for Sealmatic. In 2025 , Sealmatic successfully broke into the elite club of defense suppliers, moving beyond just standard industrial pumps to critical submarine applications. They are not just supplying standard pump seals; they secured orders for critical parts of the Stern Gland Sealing System. They also supplied seals for MDL’s “Arowana” Midget Submarine program (a flagship R&D project for special operations).

Historically, Indian Navy ships (Russian/Western origin) relied on imported seals from companies like John Crane (UK) or EagleBurgmann (Germany). Under the “Make in India” mandate, defense shipyards (like MDL, Goa Shipyard, GRSE) are actively replacing these expensive imported spares with Indian equivalents. Destroyers (Visakhapatnam class) and Frigates use hundreds of pumps (bilge, ballast, fire-fighting, fuel transfer). Sealmatic can now bid for all of these replacement seals.

Things look good in petroleum, enegy and defence sectors; however, it will take some time before these developments can appear in the balance sheet. Let us keep the fingers crossed.

10 Likes

Agree. Company needs one more round of equity infusion for growth to be expedited. Alternative is to use internal accruals which will take time - but will happen over next 2 years.

this story may take some time to play out but once it does its margins and sales will go up.

2 Likes