Background:

Schneider Electric Infrastructure Ltd (SEIL), is part of Schneider Electric France. in 2010. Alstom Schneider consortium finalised on the joint acquisition of Areva’s transmission and distribution (T&M) businesses, together worth €2.29bn ($2.73bn). Alstom acquired about two thirds of the transmission business while Schneider transferred the distribution business to Schneider Electric.

The AREVA T&D India Limited announces Demerger of its Distribution (Medium Voltage) Business Operations. AREVA T&D India Limited’s promoters, ALSTOM Sextant 5 SAS, along with certain other entities, made an open offer to the public shareholders of the Company, according to the requirements of the Securities and Exchange Board of India [Substantial Acquisition of Shares and Takeovers] Regulations, 1997, as amended up to date.

This open offer provided that the Transmission activities (High Voltage systems, equipment, Power Electronics and Automation) will be separated from the Distribution activities (Medium Voltage systems, equipment and related Automation) of the Company.

In2011, the the demerged entity (Medium Voltage systems, equipment and related Automation, power distribution) became "Smartgrid Automation Distribution and Switchgear Limited ", then changed the name to Schneider Electric Infrastructure Limited.

In 2012, AREVA T&D (High Voltage systems, equipment, power transmission) India changed the name to ALSTOM “T&D India”, in 2016, Alstom T&D India became the “GE T&D India”, following its acquisition by US giant General Electric.

Present:

SEIL is in good position to take the advantage of infra push, power distribution area, Electrification, Metals, Mining & Minerals, Mobility, hyperscale data centre, Industry and building. They also trying for Digital Transformation in these areas.

In Q1FY24, the company announced many wins in some of these areas.

One good thing about the company is that they are not restricting the products to the ones they got as part of AREVA T&D, they are also offering the products and software platforms which were developed as part of parent company across the globe. This list contains lot of new age innovative products, platforms and services which they got by acquiring companies across the geographies. Just think of the capability addition, no other companies in India can match this. Can it be a moat ?, not sure.

The company makes money in these areas: Products, Solutions and Services

#1 Products

Transformers

Components

Ring Main Units

Automation

#2 Solutions:

EcoStruxure- Entry Level

GridPower

EcoStruxur for Business

Electric UtilitiesMining-Minerals-MetalsOil & GasSmart cities

EcoStruxure for Partners

ContractorsGlobal Strategic AlliancePanel Builders

#3 Services:

Partner Managed ServicesManage Maintenance: EcoStruxure™ Facility Expert

Electrical Distribution ServicesEcoStruxure™ Asset Advisor

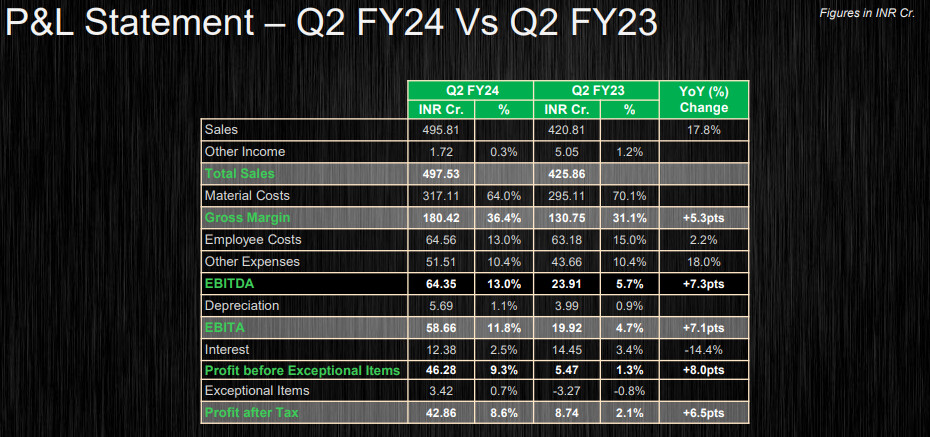

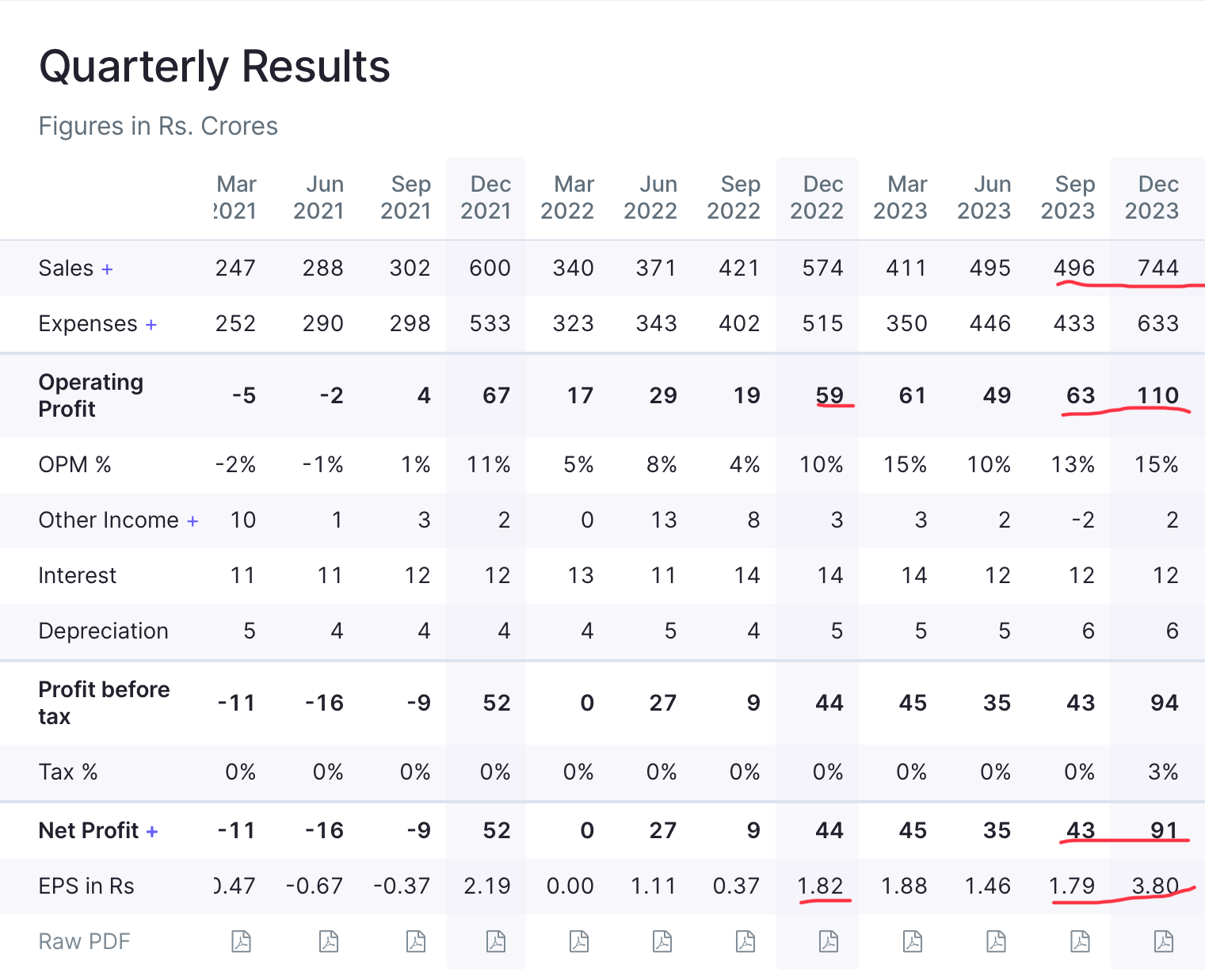

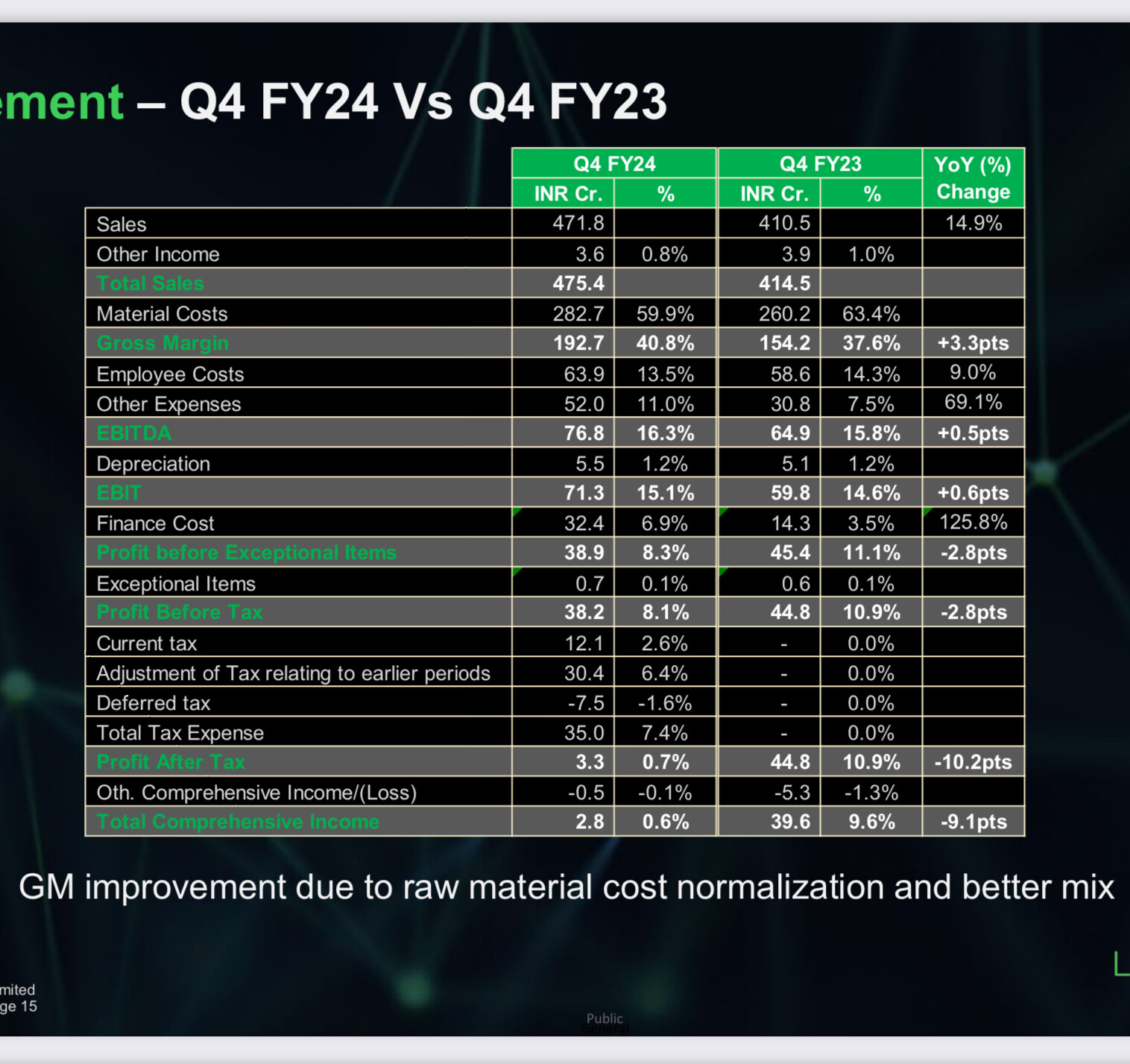

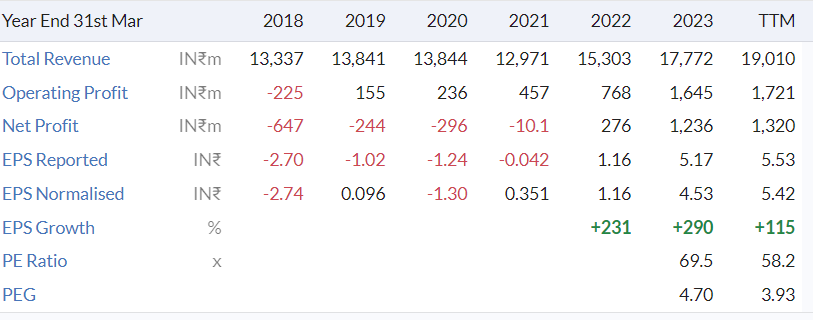

Financial Summery:

Profitability

Cashflow:

Balancesheet:

The company was not profitable till 2021 but from FY22 it became profitable.

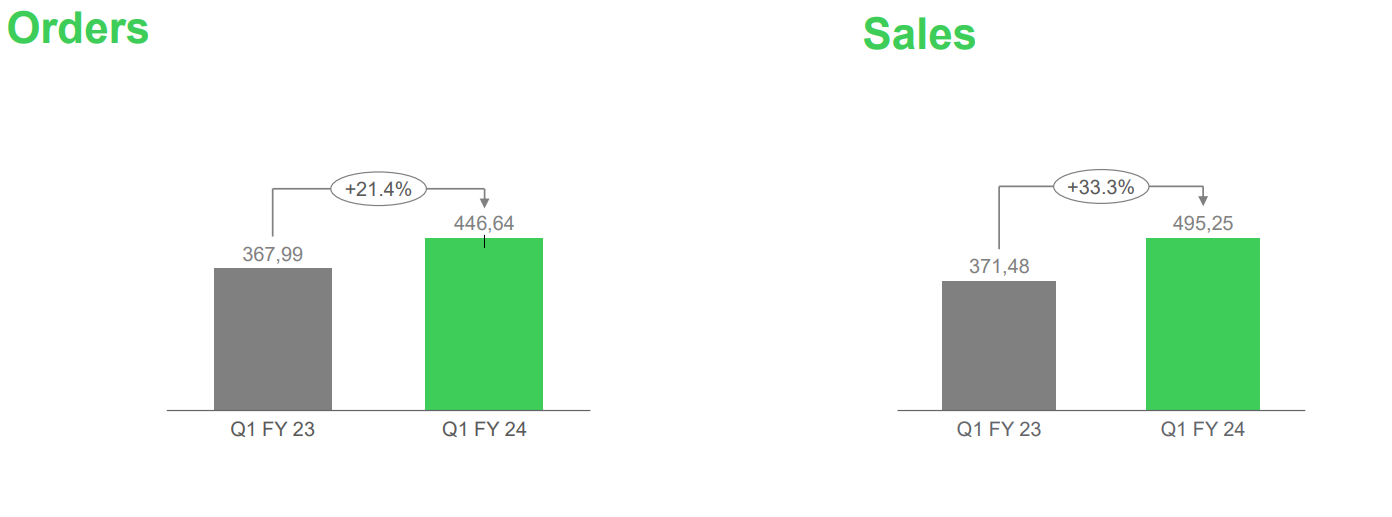

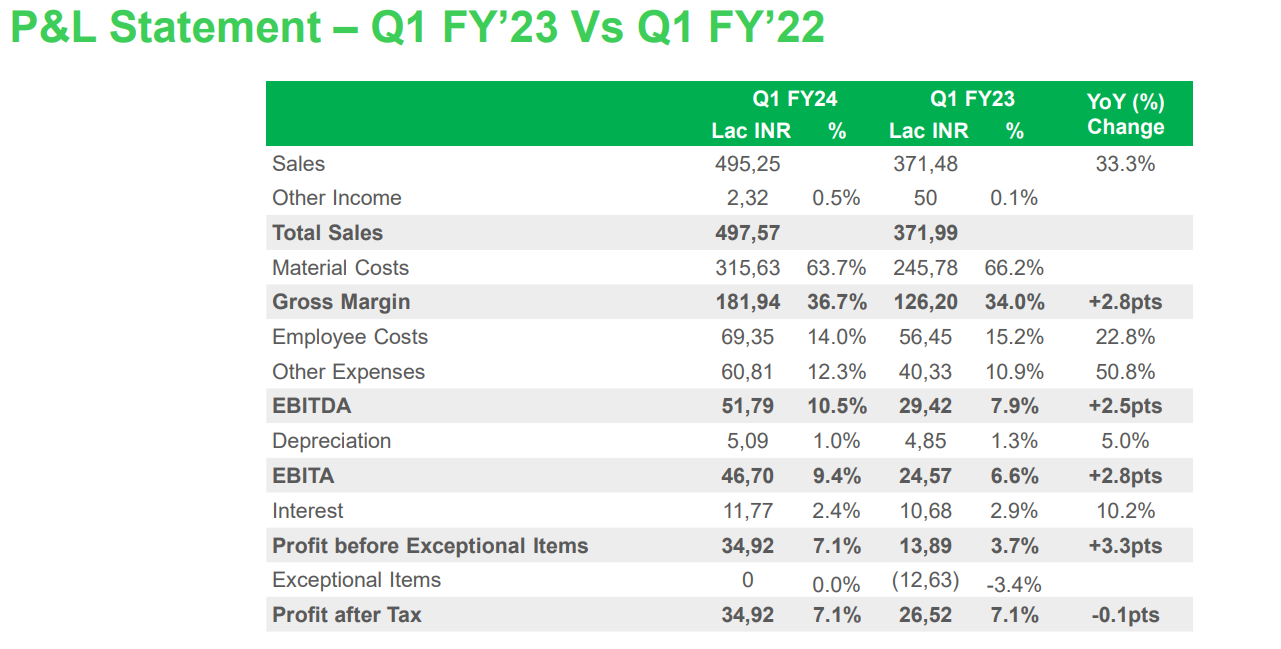

In Q1FY2024

Company management is reasonably bullish on future prospects and gave a healthy guidance for FY24

Antithesis

There are some more unlisted companies in India, it is difficult to find out which company do what and transactions between them, it will be good if they are consolidated and company defines clear areas of each companies.

Debt to equity: 3.15

Valuation:

P/E is at 58 as on 12Aug23, which looks on the higher side.

Disclosure: Not invested, watching